|

시장보고서

상품코드

1773438

건설용 스트로 베일 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Straw Bale for Construction Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

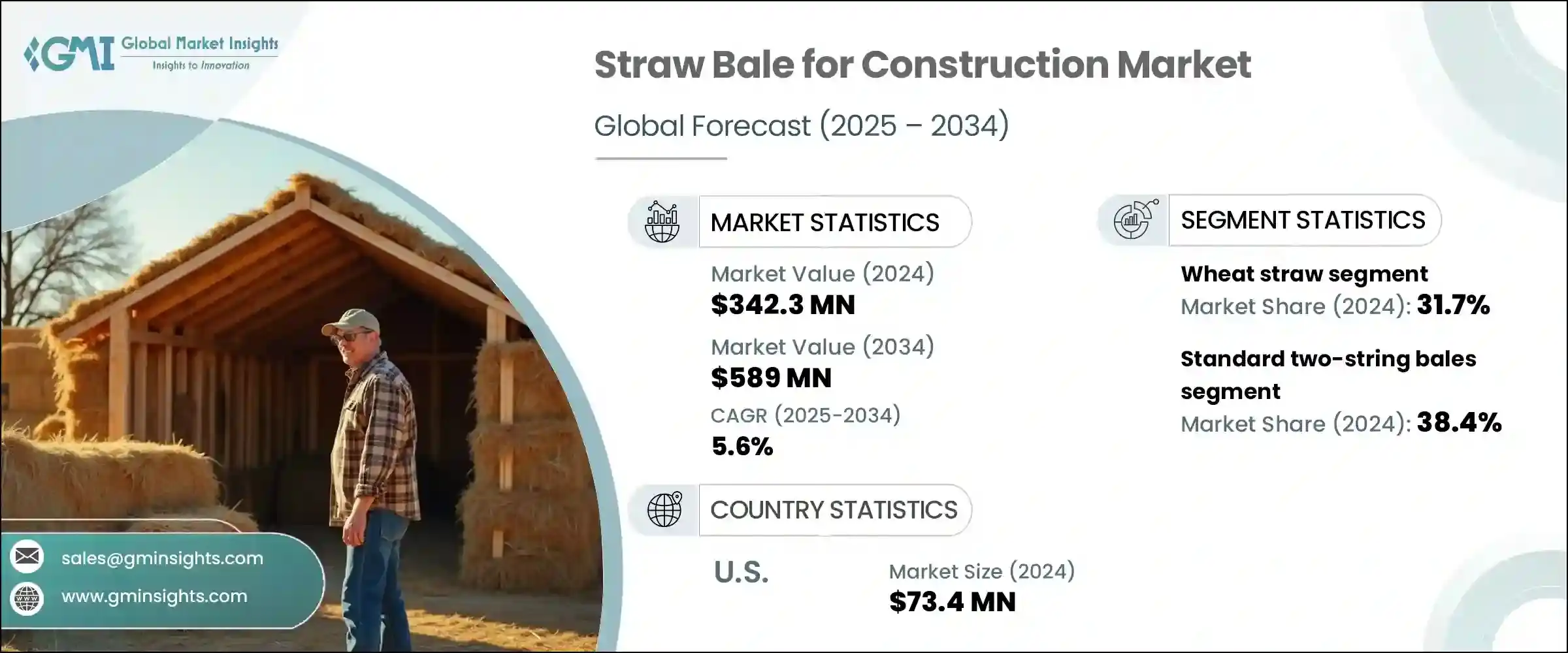

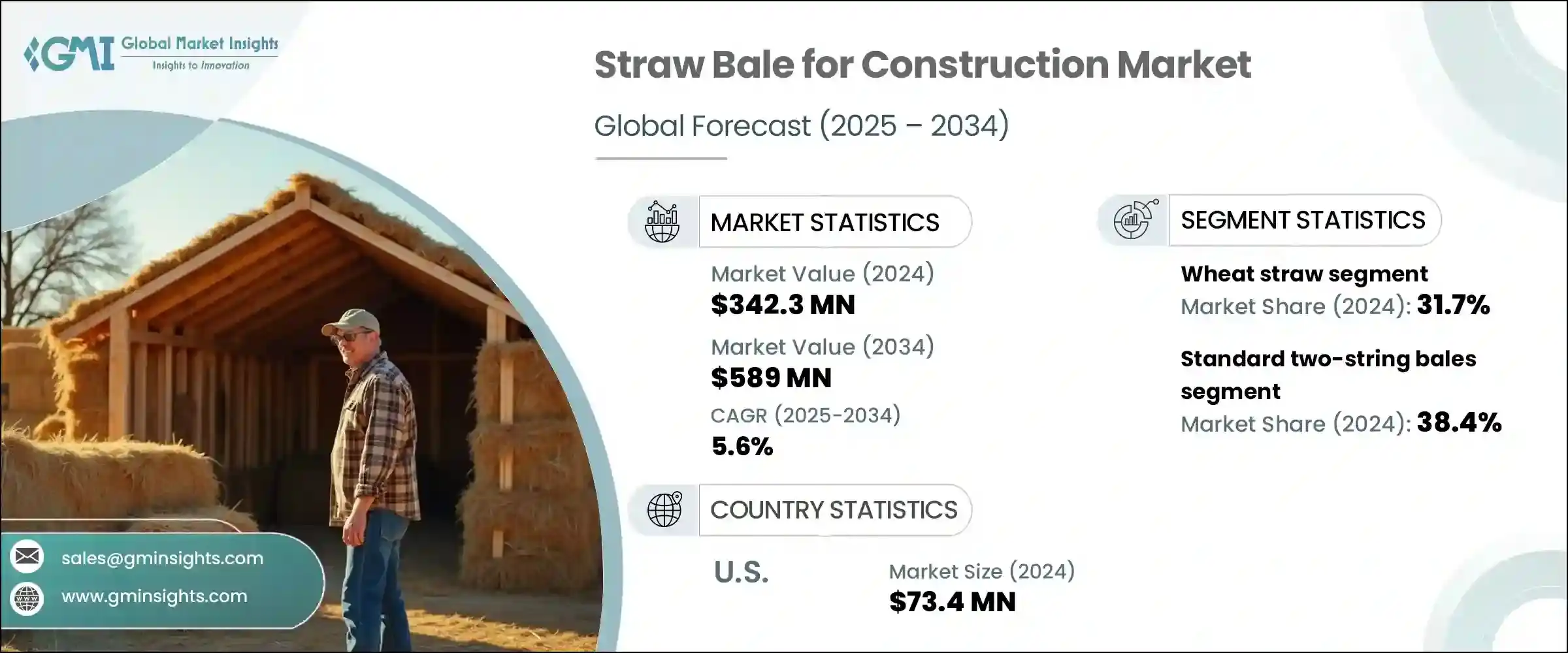

세계의 건설용 스트로 베일 시장은 2024년에 3억 4,230만 달러로 평가되고 CAGR 5.6%로 성장하며, 2034년에는 5억 8,900만 달러에 달할 것으로 추정되고 있습니다.

이러한 성장은 스트로 베일 건축의 친환경적이고 에너지 효율이 높은 특성에 기인한 바가 큽니다. 밀도 있게 압축된 짚단을 주요 벽재로 활용하고, 천연 소재의 석고와 코팅으로 마감하는 이 기술은 환경에 미치는 영향이 적다는 점이 장점으로 꼽히고 있습니다. 농산물의 일종인 밀짚은 구할 수 있는 양이 풍부하고 가격도 저렴해 건축에 있으며, 지속가능한 대안으로 떠오르고 있습니다. 스트로 베일 구조가 두드러지는 것은 우수한 단열 성능으로, 베일의 밀도와 벽의 두께에 따라 다르지만 R값은 보통 R-30에서 R-35 사이입니다.

이러한 높은 단열 성능은 특히 냉난방시 에너지 소비를 줄여 비용 절감과 환경적 이점을 제공합니다. 또한 짚은 천연 탄소 흡수원 역할을 하여 식물의 성장주기 동안 흡수된 이산화탄소를 격리하는 역할을 합니다. 이러한 탄소 저장 능력은 건물의 전체 탄소 배출량을 줄이는 데 있으며, 이 소재의 역할을 증가시킵니다. 저부하 건축 솔루션에 대한 관심이 높아짐에 따라 스트로 베일 건축은 특히 녹색 인프라, 지속가능한 주택, 재생한 재료를 중시하는 지역에서 다양한 지역에서 점점 더 인기있는 선택이 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작 금액 | 3억 4,230만 달러 |

| 예측 금액 | 5억 8,900만 달러 |

| CAGR | 5.6% |

밀짚 부문은 가용성과 구조적 이점으로 인해 2024년 31.7%의 점유율을 차지할 것으로 예측됩니다. 평행한 섬유 배향은 컴팩트한 포장, 안정된 단열성, 구조적 용도에서 내구성을 가능하게 합니다. 또한 생분해가 용이하고 건설 환경에 적응하기 쉬운 점도 밀짚의 활용 확대에 기여하고 있습니다. 밀짚은 내습성과 친환경 건축공법에 대한 적합성을 인정받고 있습니다. 이 소재는 오랜 기간 중 전통 건축 기법에 접목되어 왔으며, 현대의 지속가능한 건축에서 입증된 성능으로 인해 다양한 지역에서 채택이 더욱 활발하게 이루어지고 있습니다.

표준 2단 베일 부문은 2024년 38.4%의 점유율을 차지했습니다. 이 베일은 하중을 견디는 건축 시스템에 쉽게 통합할 수 있으므로 널리 사용되고 있습니다. 균형 잡힌 크기와 무게는 취급 효율을 향상시키고, 기존 베일링 장비와의 호환성을 통해 매우 쉽게 사용할 수 있습니다. 건설업자, 계약자, 셀프 빌더는 비용 효율성과 운송의 용이성 때문에 이러한 베일을 선호합니다. 또한 지속가능한 건축을 장려하기 위한 교육 프로그램이나 교육 구상에서 이 베일은 종종 교재로 사용되어 친환경 건축에 대한 지역 사회의 이해를 높이는 데 도움을 주고 있습니다.

미국 건설용 스트로 베일의 2024년 시장 규모는 7,340만 달러에 달할 것입니다. 스트로 베일 건축에 대한 이 국가의 리더십은 친환경 주택에 대한 관심 증가와 저탄소 건축 공법을 장려하는 지역 구상에 의해 지원되고 있습니다. 농업의 제품별로 이용 가능한 짚은 지속가능한 오프 그리드 주택 및 주문형 주택에 대한 수요 증가와 함께 지속적으로 보급을 촉진하고 있습니다. 친환경 주택 개발을 장려하는 정부 프로그램과 청정 소재에 초점을 맞춘 주정부 차원의 에너지 정책 지원은 이러한 추세를 강화하여 전 세계 교외 및 반농촌 지역으로의 확장을 촉진하고 있습니다.

세계 건설용 스트로 베일 산업은 여전히 상당히 세분화되어 있으며, Endeavour Centre, Strawcture Eco, ModCell Straw Technology, Ecococon, Straw-Bale Building UK 등의 주요 업체들이 틈새 시장에서 적극적으로 사업을 전개하며 지역 수요를 지원하고 있습니다. 스트로 베일 건축 시장의 기업은 시장에서의 존재감을 높이고 환경과 소비자 수요의 변화에 적응하기 위해 표적화 전략을 채택하고 있습니다.

많은 기업이 물류비용과 탄소배출을 줄이기 위해 짚의 현지 생산과 조달에 집중하고 있습니다. 제품의 표준화는 지역 건축법규를 준수하고 주요 건설 부문의 신뢰를 얻기 위해 진행되고 있습니다. 건축가 및 지속가능성에 중점을 둔 개발업체와의 전략적 협력을 통해 기업은 최신 친환경 주택에 스트로 베일 구조의 이용 사례를 소개했습니다. 교육 중심의 캠페인과 지역 기반 워크숍을 통해 시장 인지도를 더욱 높이고, 현장 실습을 통해 계약자 및 셀프빌더의 신뢰를 높이고 있습니다.

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

- 에코시스템 분석

- 공급업체의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 촉진요인

- 업계의 잠재적 리스크 & 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter의 산업 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 짚의 유형별

- 향후 시장 동향

- 테크놀러지와 혁신의 상황

- 현재 기술 동향

- 신규 기술

- 특허 상황

- 무역통계(HS 코드)(주 : 무역통계는 주요 국가에 대해서만 제공됩니다.)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능 관행

- 폐기물 삭감 전략

- 생산에서의 에너지 효율

- 친환경 구상

- 탄소발자국 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카 항공

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십과 협업

- 신제품의 발매

- 확장 계획

제5장 시장 추산·예측 : 스트로 유형별, 2021-2034년

- 주요 동향

- 밀짚

- 볏짚

- 보리 짚

- 귀리 짚

- 호밀 짚

- 기타

제6장 시장 추산·예측 : 베일 형식, 2021-2034년

- 주요 동향

- 표준적인 2 스트링 베일

- 3 스트링 베일

- 점보 베일

- 커스텀 사이즈 베일

- 프리패브 스트로 패널

제7장 시장 추산·예측 : 공법별, 2021-2034년

- 주요 동향

- 내하중/네브래스카 스타일

- 주량접합부(Post-and-beam infill)

- 하이브리드 방식

- 프리패브 패널 시스템

- 기타

제8장 시장 추산·예측 : 용도별, 2021-2034년

- 주요 동향

- 외벽

- 내벽

- 지붕 단열재

- 바닥 단열재

- 방음

- 기타

제9장 추정·예측 : 용도별, 2021-2034년

- 주요 동향

- 주택 건설

- 단독주택

- 집합주택

- 작은 집과 오두막

- 증축과 개수

- 상업 건설

- 교육 시설

- 생태관광(Eco-tourism) 시설

- 소매점과 오피스 스페이스

- 기타

- 농업용 건물

- 커뮤니티와 공공 건물

- 기타

제10장 추정·예측 : 마감 유형별, 2021-2034년

- 주요 동향

- 석회 회반죽

- 점토 회반죽

- 시멘트 스투코

- 토벽(Earthen plasters)

- 사이딩과 클래딩

- 기타

제11장 시장 추산·예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카 지역

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트

- 기타 중동 및 아프리카 지역

제12장 기업 개요

- BRAR AGRO WORKS

- CalFibre

- Ecococon

- Endeavour Centre

- Grass Land Gold Pvt. Ltd

- Gruppo Carli

- ModCell Straw Technology

- Profodd Private Limited

- Straw-Bale Building UK

- Strawcture Eco

The Global Straw Bale for Construction Market was valued at USD 342.3 million in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 589 million by 2034. This growth is largely attributed to the eco-friendly and energy-efficient characteristics of straw bale construction. Utilizing tightly compacted straw bales as primary wall material, the technique is finished with natural plasters or coatings and has gained traction for its low environmental impact. As an agricultural by-product, straw is abundantly available and affordable, making it a sustainable alternative in construction. What makes straw bale structures stand out is their impressive insulation capability, with R-values typically ranging between R-30 and R-35, depending on bale density and wall thickness.

These high insulation values reduce energy consumption, especially in heating and cooling, resulting in cost savings and environmental benefits. Additionally, straw serves as a natural carbon sink, sequestering carbon dioxide absorbed during the plant's growth cycle. This carbon-storing ability enhances the material's role in reducing the overall carbon footprint of buildings. With rising interest in low-impact building solutions, straw bale construction is becoming an increasingly popular choice across different geographies, particularly in areas emphasizing green infrastructure, sustainable housing, and renewable materials.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $342.3 Million |

| Forecast Value | $589 Million |

| CAGR | 5.6% |

The wheat straw segment held a 31.7% share in 2024 due to its availability and structural advantages. Its parallel fiber orientation enables compact packing, consistent insulation, and durability in structural applications. Furthermore, its ease of biodegradation and adaptability to construction environments contribute to its growing use. Wheat straw is recognized for its moisture-resistant properties and compatibility with eco-construction methods. The material's long-standing integration into traditional building techniques and its proven performance in contemporary sustainable construction further boost its adoption across various regions.

The standard two-string bales segment held a 38.4% share in 2024. These bales are widely used because of their ease of integration into load-bearing construction systems. Their balanced size and weight improve handling efficiency, and their compatibility with conventional baling equipment makes them highly accessible. Builders, contractors, and self-builders favor these bales for their cost-effectiveness and ease of transport. Additionally, training programs and educational initiatives aimed at promoting sustainable building often feature these bales as teaching tools, helping to enhance community understanding of eco-friendly construction practices.

United States Straw Bale for Construction Market generated USD 73.4 million in 2024. The country's leadership in straw bale construction is supported by a growing emphasis on environmentally conscious housing and regional initiatives promoting low-carbon building methods. The availability of straw as a farming by-product, combined with evolving demand for sustainable off-grid and custom-built homes, continues to push adoption forward. Support from governmental programs encouraging ecological housing development, alongside state-level energy policies focused on clean materials, reinforces this trend and fosters expansion in suburban and semi-rural areas globally.

The Global Straw Bale for Construction Industry remains moderately fragmented, with key players such as Endeavour Centre, Strawcture Eco, ModCell Straw Technology, Ecococon, and Straw-Bale Building UK actively operating in niche markets and supporting localized demand. Companies in the straw bale construction market are employing targeted strategies to bolster their market presence and adapt to changing environmental and consumer demands.

Many firms are focusing on local production and sourcing of straw to reduce logistics costs and carbon emissions. Product standardization efforts are being pursued to comply with regional building codes and gain trust from mainstream construction sectors. Strategic collaborations with architects and sustainability-focused developers help companies showcase use cases of straw bale construction in modern eco-homes. Education-driven campaigns and community-based workshops further promote market awareness, while hands-on training initiatives increase confidence among contractors and self-builders.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Straw type

- 2.2.2 Bale format

- 2.2.3 Construction method

- 2.2.4 Application

- 2.2.5 End use sector

- 2.2.6 Finishing type

- 2.2.7 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By straw type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Straw Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Wheat straw

- 5.3 Rice straw

- 5.4 Barley straw

- 5.5 Oat straw

- 5.6 Rye straw

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Bale Format, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Standard two-string bales

- 6.3 Three-string bales

- 6.4 Jumbo bales

- 6.5 Custom-sized bales

- 6.6 Prefabricated straw panels

Chapter 7 Market Estimates and Forecast, By Construction Method, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Load-bearing/nebraska style

- 7.3 Post-and-beam infill

- 7.4 Hybrid methods

- 7.5 Prefabricated panel systems

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Exterior walls

- 8.3 Interior walls

- 8.4 Roof insulation

- 8.5 Floor insulation

- 8.6 Sound insulation

- 8.7 Others

Chapter 9 Estimates and Forecast, By End Use Sector, 2021 - 2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Residential construction

- 9.2.1 Single-family homes

- 9.2.2 Multi-family buildings

- 9.2.3 Tiny homes and cabins

- 9.2.4 Additions and renovations

- 9.3 Commercial construction

- 9.3.1 Educational facilities

- 9.3.2 Eco-tourism facilities

- 9.3.3 Retail and office spaces

- 9.3.4 Others

- 9.4 Agricultural buildings

- 9.5 Community and public buildings

- 9.6 Others

Chapter 10 Estimates and Forecast, By Finishing Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 Lime plaster

- 10.3 Clay plaster

- 10.4 Cement stucco

- 10.5 Earthen plasters

- 10.6 Siding and cladding

- 10.7 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 BRAR AGRO WORKS

- 12.2 CalFibre

- 12.3 Ecococon

- 12.4 Endeavour Centre

- 12.5 Grass Land Gold Pvt. Ltd

- 12.6 Gruppo Carli

- 12.7 ModCell Straw Technology

- 12.8 Profodd Private Limited

- 12.9 Straw-Bale Building UK

- 12.10 Strawcture Eco

(주말 및 공휴일 제외)