|

시장보고서

상품코드

1773440

절삭 공구 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Cutting Tools Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

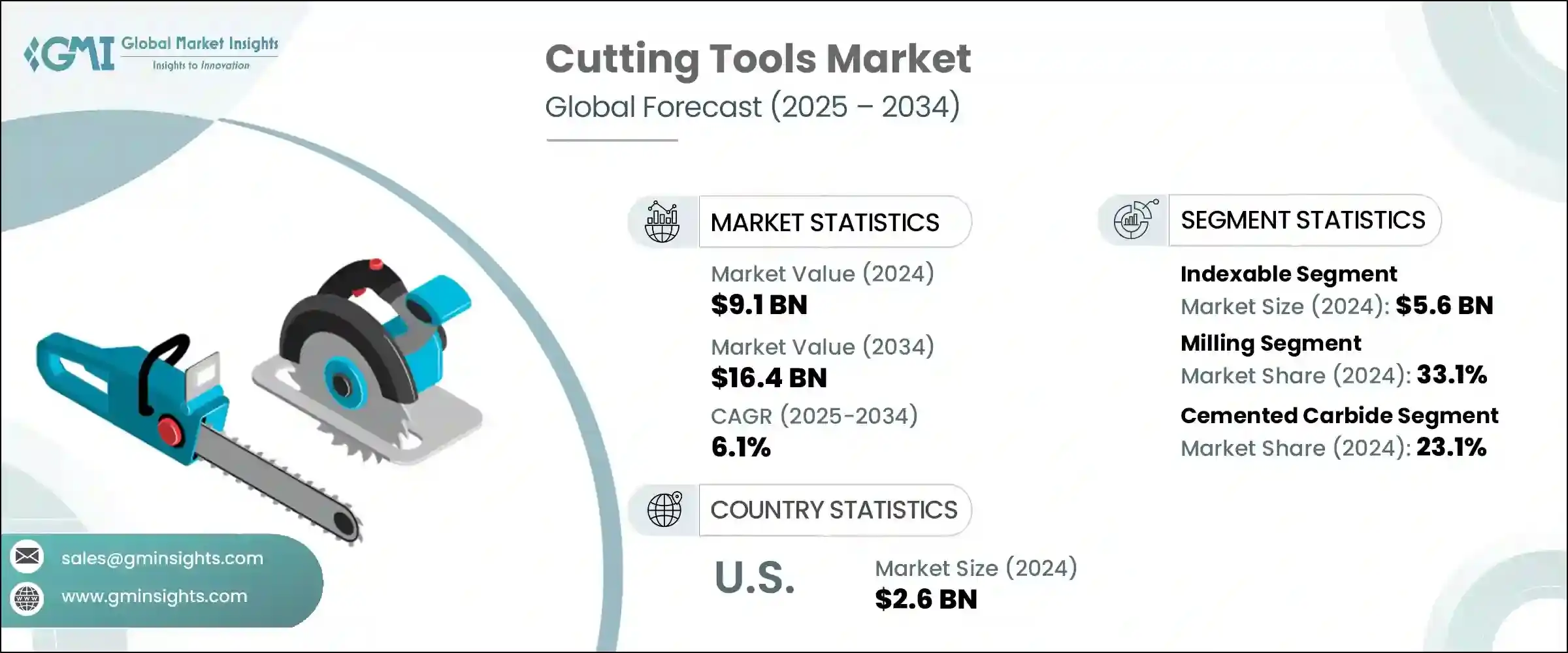

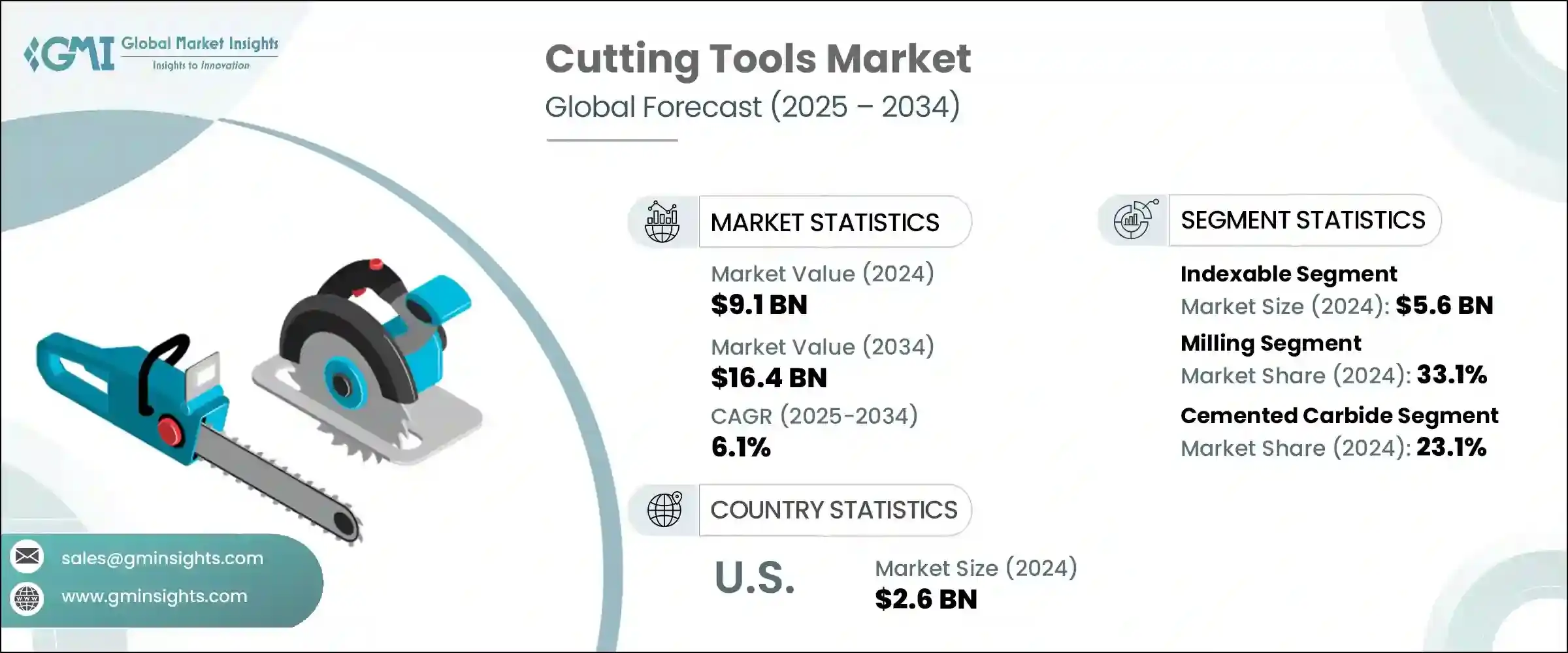

절삭 공구 세계 시장 규모는 2024년에 91억 달러로 평가되었고, CAGR 6.1%로 성장하여 2034년에는 164억 달러에 이를 것으로 예측됩니다.

이 시장은 제조 방법의 발전에 따라 크게 성장하고 있습니다. 자동화와 인더스트리 4.0 관행의 부상으로 결함 없는 부품을 생산할 수 있는 정밀 공구에 대한 수요가 증가하고 있습니다. 자동차, 항공우주, 전자 산업은 특히 이러한 정밀도의 혜택을 누리고 있습니다.

또한, 복합재료, 고강도 합금 등 보다 가볍고 강도가 높은 재료를 사용하는 방향으로 전환되고 있어, 이러한 강인한 재료를 다룰 수 있는 보다 진보된 절삭 공구가 요구되고 있습니다. 또한, 특히 신흥 경제국에서 인프라 붐이 지속되고 있어 대형 기계 및 현장 설비에 적합한 공구에 대한 수요가 증가하고 있는 것도 중요한 원동력이 되고 있습니다. 또한, 원자재 사용량을 최적화하고 폐기물을 최소화하는 것이 중요시되고 있어 내구성이 높고 비용 효율적인 절삭 공구가 요구되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 91억 달러 |

| 예측 금액 | 164억 달러 |

| CAGR | 6.1% |

또한, 절삭 공구 업계에서는 보다 친환경적인 생산 방식에 대한 요구가 가속화되고 있으며, 기업들은 성능과 함께 지속가능성을 우선순위로 삼고 있습니다. 제조업체들은 원자재 조달부터 제조 공정의 에너지 효율 개선에 이르기까지 모든 단계에서 환경 친화적인 방법을 채택하고 있습니다. 절삭 공구의 코팅과 소재의 발전은 공구 수명을 연장하고 폐기물을 줄이며 절삭 효율을 향상시키고 있습니다. 또한, 재활용과 재사용에 대한 관심이 높아지면서 전체 환경 발자국이 감소하고 있습니다. 또한, 많은 기업들이 제조 공정에서 유해 배출물을 줄이고 유해 화학물질의 사용을 최소화하는 데 주력하고 있습니다.

2024년, 교환식 공구 부문은 56억 달러의 매출을 기록했습니다. 이 분야는 비용 효율성과 다재다능함으로 인해 인기가 높아지고 있습니다. 교환식 공구는 전체 공구를 폐기하는 대신 마모된 칩을 교체할 수 있기 때문에 운영 비용을 절감할 수 있어 자동차 및 항공우주와 같은 정밀 구동 산업에서 매우 매력적입니다. 또한, 이러한 공구는 고속 가공을 지원하여 제조업체에게 중요한 효율성과 내구성을 향상시킵니다. 교체 가능한 칩을 사용하면 고철 발생을 줄이고 폐기물을 줄일 수 있기 때문에 친환경 제조 공정에 대한 수요 증가와 일치하여 지속가능성으로의 전환이 더욱 매력적입니다.

밀링 공구 부문은 2024년 33.1%의 점유율을 차지했습니다. 이 부문의 급격한 성장은 밀링 공구가 여러 산업 분야에서 다양한 작업을 처리할 수 있기 때문입니다. 밀링 공구는 복잡한 프로파일을 고정밀도로 제작하는 데 필수적이며, 자동차, 항공우주, 전자제품에 널리 사용되고 있습니다. 제품 설계에서 더 가볍고 내구성이 뛰어난 부품이 요구되는 가운데, 밀링 공구는 첨단 소재를 절단할 수 있는 능력으로 인해 인기를 얻고 있습니다. 다목적 설계 및 개선된 코팅과 같은 기술 혁신도 공구 수명 연장 및 운영 비용 절감으로 이 부문의 성장에 기여하고 있습니다.

미국의 절삭 공구 2024년 시장 규모는 26억 달러로 세계 시장을 선도했습니다. 미국의 제조업은 다양한 산업에 걸쳐 있으며, 이는 이러한 우위를 뒷받침하는 중요한 요소입니다. 자동차 산업과 항공우주 산업은 엄격한 품질 기준을 충족하는 고정밀 공구에 대한 수요를 촉진하고 있습니다. 또한, 로봇 공학, 센서, 클라우드 분석이 제조업에 통합되어 운영 효율성을 향상시킴으로써 시장 성장을 더욱 촉진하고 있습니다.

주요 기업들은 공구의 성능을 향상시키고 수명을 연장하기 위해 연구개발에 많은 투자를 하고 있습니다. 또한, 환경 규제와 친환경 제품을 원하는 소비자의 요구에 부응하기 위해 지속 가능한 제조 기술을 적극적으로 모색하고 있습니다. 또한, 전략적 파트너십, 합병, 인수를 통해 제품 제공 확대와 공급망 강화를 위해 노력하고 있습니다. 기업들은 또한 스마트 센서, IoT 지원 장치와 같은 디지털 도구를 도입하여 제조의 정확성과 업무 효율성을 높이고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 미치는 요인

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 기회

- 성장 가능성 분석

- 향후 시장 동향

- 기술 및 혁신 상황

- 현재 기술 동향

- 신기술

- 가격 동향

- 지역별

- 툴 유형별

- 규제 상황

- 표준과 컴플라이언스 요건

- 지역 규제 구조

- 인증 기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추산·예측 : 툴 유형별, 2021년-2034년

- 주요 동향

- Indexable

- Solid Round

제6장 시장 추산·예측 : 공정별, 2021년-2034년

- 주요 동향

- Milling

- Drilling

- Boring

- Turning

- Grinding

- 기타

제7장 시장 추산·예측 : 재료별, 2021년-2034년

- 주요 동향

- 초경합금

- 고속도강(HSS)

- 세라믹

- 입방정 질화붕소(CBN)

- 다결정 다이아몬드(PCD)

- 이그조틱 재료

- 스테인리스 스틸

제8장 시장 추산·예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 자동차

- 항공우주 및 방위

- 건설

- 일렉트로닉스

- 발전

- 석유 및 가스

- 목공

- 금형 제조

제9장 시장 추산·예측 : 유통 채널별, 2021년-2034년

- 주요 동향

- 직접

- 간접

제10장 시장 추산·예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 말레이시아

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카공화국

제11장 기업 개요

- Ceratizit S.A.

- Cougar Cutting Tools

- Emuge Corporation

- Greenleaf Corporation

- Ingersoll Cutting Tools

- Iscar Ltd.

- Kennametal Inc.

- Mapal Inc.

- Mitsubishi Materials Corporation

- Mohawk Special Cutting Tools

- OSG Corporation

- Sandvik Coromant

- Seco Tools AB

- Tungaloy Corporation

- Walter Technologies

The Global Cutting Tools Market was valued at USD 9.1 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 16.4 billion by 2034. This market is experiencing significant growth, driven largely by advancements in manufacturing methods. With the rise of automation and Industry 4.0 practices, there is an increasing demand for precision tools that can produce defect-free parts. Industries like automotive, aerospace, and electronics particularly benefit from such accuracy.

Additionally, the shift toward using lighter and stronger materials, including composites and high strength alloys, necessitates more advanced cutting tools that can handle these tough materials. Another key driver is the ongoing infrastructure boom, especially in rapidly developing economies, which raises the need for tools suitable for large machines and site equipment. Along with this, the focus on optimizing raw material use and minimizing waste continues to push manufacturers toward more durable, cost-effective cutting tools.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.1 Billion |

| Forecast Value | $16.4 Billion |

| CAGR | 6.1% |

Furthermore, the drive for greener production methods is accelerating within the cutting tools industry, as companies increasingly prioritize sustainability alongside performance. Manufacturers are adopting eco-friendly practices at every stage, from sourcing raw materials to improving energy efficiency during the manufacturing process. Advances in cutting tool coatings and materials are enabling longer tool lifespans and reduced waste, while also enhancing cutting efficiency. Additionally, there is a growing emphasis on recycling and reusing cutting tools, reducing the overall environmental footprint. Many companies are also focusing on reducing hazardous emissions and minimizing the use of harmful chemicals during the production process.

In 2024, the indexable tools segment generated USD 5.6 billion. This segment is growing in popularity due to its cost-effectiveness and versatility. Indexable tools allow users to replace worn-out inserts instead of discarding the entire tool, which helps lower operational costs, making them highly attractive in precision-driven industries like automotive and aerospace. These tools also support high-speed machining, enhancing efficiency and durability, which are crucial for manufacturers. The shift toward sustainability further adds to their appeal, as using replaceable inserts generates less scrap metal and reduces waste, aligning with the growing demand for greener manufacturing processes.

The milling tools segment accounted for a 33.1% share in 2024. The rapid expansion of this segment can be attributed to the wide range of tasks milling tools are capable of handling in multiple industries. These tools are essential for producing complex profiles with high precision, and they are commonly used in automotive, aerospace, and electronics. As product designs demand lighter yet more durable parts, milling tools are gaining popularity due to their ability to cut through advanced materials. Innovations, such as multi-purpose designs and improved coatings, have also contributed to the segment's growth by extending tool life and reducing operational costs.

United States Cutting Tools Market was valued at USD 2.6 billion in 2024, leading the global market. The U.S. manufacturing sector, which spans a wide range of industries, is a key factor driving this dominance. The automotive and aerospace sectors fuel the demand for highly accurate tools that meet stringent quality standards. Additionally, the integration of robotics, sensors, and cloud analytics in manufacturing further boosts market growth by enhancing operational efficiency.

Key companies in the Cutting Tools Industry include Ceratizit S.A., Cougar Cutting Tools, Emuge Corporation, Greenleaf Corporation, Ingersoll Cutting Tools, Iscar Ltd., Kennametal Inc., Mapal Inc., Mitsubishi Materials Corporation, Mohawk Special Cutting Tools, OSG Corporation, Sandvik Coromant, Seco Tools AB, Tungaloy Corporation, and Walter Technologies. In response to the increasing demand for cutting-edge products, companies in the cutting tools market are focusing on technological advancements to enhance their market position.

Leading players are investing heavily in research and development to improve the performance of their tools and increase their lifespan. They are also actively exploring sustainable manufacturing techniques to meet environmental regulations and consumer demands for greener products. Additionally, strategic partnerships, mergers, and acquisitions are being utilized to expand product offerings and strengthen supply chains. Companies are also incorporating digital tools, such as smart sensors and IoT-enabled devices, to enhance precision and operational efficiency in manufacturing.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Tool type

- 2.2.3 Process

- 2.2.4 Material Type

- 2.2.5 End Use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By tool type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 MEA

- 4.2.1.5 LATAM

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Tool Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Indexable

- 5.3 Solid Round

Chapter 6 Market Estimates & Forecast, By Process, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Milling

- 6.3 Drilling

- 6.4 Boring

- 6.5 Turning

- 6.6 Grinding

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Material Type, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Cemented Carbide

- 7.3 High-Speed Steel (HSS)

- 7.4 Ceramics

- 7.5 Cubic Boron Nitride (CBN)

- 7.6 Polycrystalline Diamond (PCD)

- 7.7 Exotic Materials

- 7.8 Stainless Steel

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Aerospace & Defense

- 8.4 Construction

- 8.5 Electronics

- 8.6 Power Generation

- 8.7 Oil & Gas

- 8.8 Woodworking

- 8.9 Die and Mold Manufacturing

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Malaysia

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Ceratizit S.A.

- 11.2 Cougar Cutting Tools

- 11.3 Emuge Corporation

- 11.4 Greenleaf Corporation

- 11.5 Ingersoll Cutting Tools

- 11.6 Iscar Ltd.

- 11.7 Kennametal Inc.

- 11.8 Mapal Inc.

- 11.9 Mitsubishi Materials Corporation

- 11.10 Mohawk Special Cutting Tools

- 11.11 OSG Corporation

- 11.12 Sandvik Coromant

- 11.13 Seco Tools AB

- 11.14 Tungaloy Corporation

- 11.15 Walter Technologies