|

시장보고서

상품코드

1773453

자동차용 압전 연료 분사 장치 시장 기회와 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Automotive Piezoelectric Fuel Injectors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

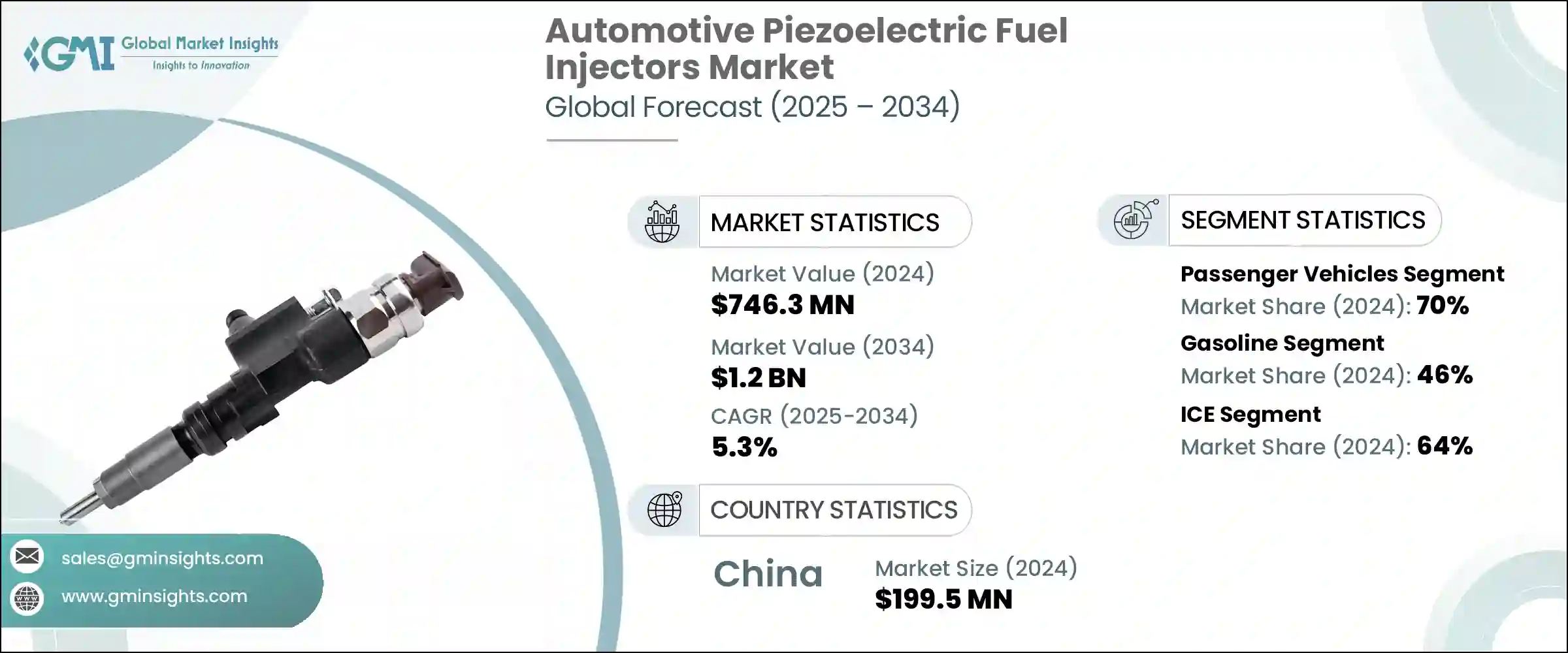

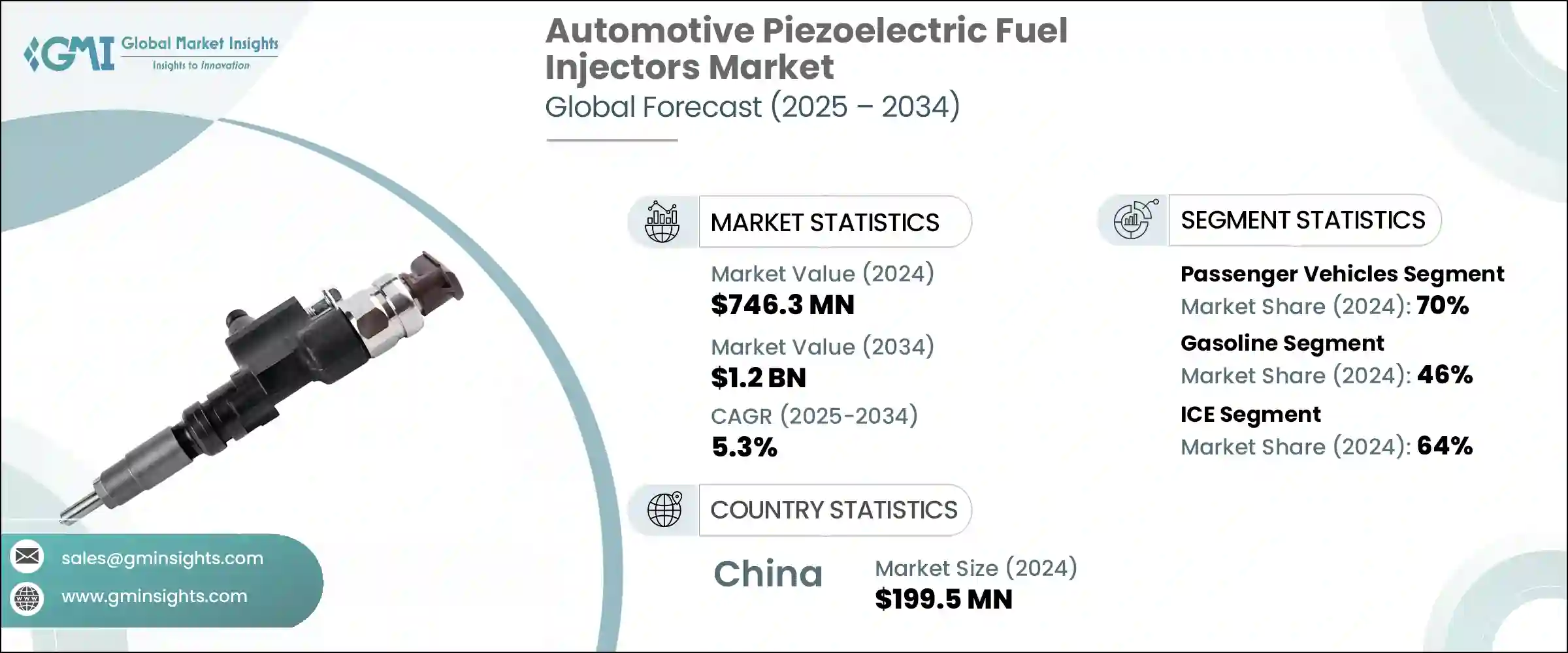

세계의 자동차용 압전 연료 분사 장치 시장은 2024년에는 7억 4,630만 달러에 달했고, CAGR 5.3%를 나타내 2034년에는 12억 달러에 달할 것으로 예측되고 있습니다.

이 시장 성장은 CRDI나 GDI 등의 첨단 엔진 기술의 도입이 진행됨과 동시에 자동차의 배기가스에 관한 세계의 규제가 엄격해지고 있는 것이 배경에 있습니다. 이 분사 장치는 빠르고 매우 정확한 연료 공급을 가능하게 하고 연소 효율을 높이고 오염물질을 줄이는 데 크게 기여합니다.

압전 분사 장치는 적극적인 환경 기준을 가진 지역에서 기존의 솔레노이드 식으로 꾸준히 대체하고 있습니다. 스마트 전자 제어 장치 및 고급 진단 기능과의 통합으로 연료 유량을 실시간으로 조정할 수 있어 엔진 성능을 최적화하고 미립자 배출량을 줄일 수 있습니다. 또한 보다 깨끗한 이동성 솔루션으로의 전환은 모든 유형의 차량 플랫폼에서 내연 응용 분야의 제어와 효율성을 높이기 위해 이러한 고정밀 부품의 필요성을 가속화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 7억 4,630만 달러 |

| 예측 금액 | 12억 달러 |

| CAGR | 5.3% |

압전 분사 장치는 단일 연소 사이클 내에서 여러 개의 초고속 연료 분사를 가능하게 함으로써 엔진 관리를 재정의합니다. 다음 규제 등 각국이 보다 엄격한 규제를 도입함에 따라 이러한 특성은 점점 더 중요해지고 있습니다.

승용차 부문은 2024년 시장을 선도해 70%의 점유율을 차지했으며 2034년까지 연평균 복합 성장률(CAGR) 5.5%를 나타낼 것으로 예측됩니다. 이 우위는 승용차, 소형 트럭, 유틸리티 차량의 세계 생산 및 판매 대수가 많아 아시아, 유럽, 북미와 같은 지역에서 엄격한 배기가스 규제는 이러한 차량 클래스에 고급 연료 분사 시스템을 통합하는 것을 연료로 하고 있습니다. 경제성을 향상시키면서 규제 기준을 충족시키는 데 도움이 되어 전력과 환경 의식 모두에 대한 소비자의 기대에 부응합니다.

가솔린 자동차 부문은 46%의 점유율을 차지하며 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 5.7%를 나타낼 것으로 예측됩니다. 여러 대륙의 규제기관이 소형차의 배기가스 규제를 진행하는 가운데, 디젤에 비해 입자상 물질이나 질소산화물의 배출량이 비교적 적은 가솔린 엔진이 매력적이 되고 있습니다. 강화된 가솔린 직접 분사 시스템에 기울어져 있습니다. 가솔린 엔진은 경량, 정숙성, 생산 비용이 낮게 지지되고 있으며, 압전 분사 장치는 이러한 엔진의 연소 개선과 스로틀 응답의 향상에 도움이 되어 가솔린 부문의 중요한 구성 요소로서의 지위를 확보하고 있습니다.

아시아태평양 자동차용 압전 연료 분사 장치 시장은 67%의 점유율을 차지해 1억 9,950만 달러를 창출했습니다. 중국의 선진적인 배기가스 규제의 채용은 보다 깨끗한 연소에의 포커스를 강화해, 압전 분사 장치 시스템에의 강한 수요를 낳고 있습니다. 지멘스 등 Tier-1 부품 제조업체는 지역 시장의 요구에 맞는 솔루션을 제공하기 위해 국내 기업과 제휴하여 이 지역에서의 대처를 강화하고 있습니다.

세계의 자동차용 압전 연료 분사 장치 시장을 적극적으로 형성하는 주목할만한 기업으로는 교세라, 콘티넨탈, 지멘스, 인피니언, 히타치 아스테모 인디애나, 아프티 부, 로버트 보쉬, 덴소, 일본 특수 도업, 무라타 제작소등이 있습니다. 이러한 제조업체는 연료 공급 요건이나 배기가스 규제의 진화에 대응하기 위해, 기술 혁신과 투자를 실시했습니다.

자동차용 압전 연료 분사 장치 시장의 주요 제조업체는 강력한 경쟁력을 구축하기 위해 몇 가지 전략적 분야에 주력하고 있습니다. 가솔린 직분분 시스템이나 하이브리드 시스템에 최적화된 용도별 분사 장치를 개발하기 위해, 자동차 OEM과의 공동 개발이 행해지고 있습니다.

목차

제1장 조사 방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역/국가

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- GDI 및 CRDI 엔진 채용 증가

- 압전 재료의 기술적 진보

- 프리미엄 및 고급차 부문의 성장

- 보다 엄격한 배출 규제

- OEM 및 Tier 1 공급업체에 의한 R&D 투자 증가

- 업계의 잠재적 위험 및 과제

- 압전 분사 장치의 고비용

- 개량형 솔레노이드 분사 장치와의 경쟁

- 시장 기회

- 하이브리드 파워트레인의 채용 증가

- 상용차에 있어서의 디젤 엔진 최적화

- 가솔린 직접 분사(GDI) 엔진으로의 광범위한 전환

- 디지털 엔진 관리와 AI 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출과 수입

- 코스트 내역 분석

- 특허 분석

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적인 노력

- 탄소발자국의 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병(M&A)

- 파트너십 및 협업

- 신제품 발매

- 확장계획과 자금조달

제5장 시장 추계·예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제6장 시장 추계·예측 : 연료별(2021-2034년)

- 주요 동향

- 가솔린

- 디젤

- 기타

제7장 시장 추계·예측 : 판매 채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제8장 시장 추계·예측 : 추진력별(2021-2034년)

- 주요 동향

- ICE

- 하이브리드

제9장 시장 추계·예측 : 기술별(2021-2034년)

- 주요 동향

- 직접 주입(DI)

- 커먼 레일 직접 분사(CRDI)

- 가솔린 직접 분사(GDI)

- 포트 연료 분사(PFI)

제10장 시장 추계·예측 : 동작 압력 범위별(2021-2034년)

- 주요 동향

- 저압(200bar 미만)

- 중압(200-1,000bar)

- 고압(1,000bar 초과)

제11장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제12장 기업 프로파일

- Aptiv

- Continental

- Delphi Technologies

- Denso Corporation

- Edelbrock LLC

- Fuzhou Ruida Machinery

- GB Remanufacturing

- Hitachi Astemo Indiana

- Infineon

- Keihin

- KYOCERA

- Magneti Marelli Parts and Services.

- Mikuni American

- Murata Manufacturing

- Robert Bosch

- Siemens

- Stanadyne

- Valley Fuel Injection &Turbo

- Woodward

- WUZETEM

The Global Automotive Piezoelectric Fuel Injectors Market was valued at USD 746.3 million in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 1.2 billion by 2034. Growth in this market is being fueled by the increasing implementation of advanced engine technologies such as CRDI and GDI, alongside stricter global regulations around vehicle emissions. These injectors allow for rapid and extremely precise fuel delivery, which contributes significantly to enhanced combustion efficiency and reduced pollutants.

Piezoelectric injectors are steadily replacing traditional solenoid types in regions with aggressive environmental standards. Their integration with smart electronic control units and advanced diagnostics enables real-time adjustment of fuel flow, allowing for optimized engine performance and fewer particulate emissions. The shift toward cleaner mobility solutions is also accelerating the need for these high-precision components, as they offer greater control and efficiency in internal combustion applications across all types of vehicle platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $746.3 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 5.3% |

Piezoelectric injectors are redefining engine management by enabling multiple ultra-fast fuel injections within a single combustion cycle. This level of control helps engineers fine-tune the air-fuel mixture with unmatched accuracy, boosting fuel efficiency and significantly lowering emissions. These attributes are becoming increasingly important as countries implement tighter regulations like Euro 7, BS-VI Stage II, and EPA Tier 3. The automotive sector is evolving rapidly, with piezo-based systems positioned to address the limitations of solenoid injectors, especially in scenarios demanding faster response times and higher injection precision.

The passenger vehicles segment led the market in 2024, contributing 70% share, and is projected to grow at a CAGR of 5.5% through 2034. This dominance stems from the high global production and sales volumes of cars, light trucks, and utility vehicles. Stringent emission controls in regions like Asia, Europe, and North America are pushing manufacturers toward incorporating advanced fuel injection systems in these vehicle classes. Piezoelectric fuel injectors help meet regulatory thresholds while improving performance and economy, aligning with consumer expectations for both power and environmental consciousness. Their application is expanding in hybrid and plug-in hybrid platforms, where rapid on-off cycles and start-stop operation demand injectors that respond quickly and efficiently-qualities that piezo technology delivers consistently.

The gasoline vehicle segment held a 46% share, and it is projected to grow at a CAGR of 5.7% between 2025 and 2034. As regulatory bodies across multiple continents move to restrict emissions from light-duty vehicles, gasoline engines are becoming more attractive due to their relatively lower particulate and nitrogen oxide output compared to diesel. Automotive manufacturers are leaning into gasoline direct injection systems, enhanced with piezoelectric injectors, to meet both performance goals and emission benchmarks. With gasoline engines favored for their lighter weight, quieter operation, and lower cost of production, piezo injectors help these engines deliver improved combustion and better throttle response, securing their position as a key component in the gasoline segment.

Asia Pacific Automotive Piezoelectric Fuel Injectors Market held a 67% share, generating USD 199.5 million. The country's massive internal combustion vehicle output and increasingly rigorous environmental mandates are driving the widespread integration of high-precision injection technology. China's adoption of advanced emission standards has intensified the focus on cleaner combustion, creating a strong demand for piezoelectric injector systems. Additionally, Tier-1 component manufacturers such as Infineon, KYOCERA, Aptiv, and Siemens are intensifying their efforts in the region by collaborating with domestic firms to tailor solutions for regional market needs. These partnerships focus on optimizing injector performance for both commercial and passenger applications, ensuring durability and efficiency at elevated pressure thresholds while maintaining competitive costs.

Notable companies actively shaping the Global Automotive Piezoelectric Fuel Injectors Market include KYOCERA, Continental, Siemens, Infineon, Hitachi Astemo Indiana, Aptiv, Robert Bosch, Denso, NGK Spark Plug Co, and Murata Manufacturing. These players are innovating and investing to keep pace with the industry's evolving fuel delivery requirements and emissions legislation.

Major manufacturers in the automotive piezoelectric fuel injectors market are focusing on several strategic areas to build a strong competitive position. First, they are investing heavily in research and development to refine injector speed, response precision, and fuel atomization, enabling better emissions control and combustion efficiency. Second, collaborations with vehicle OEMs are being formed to develop application-specific injectors optimized for gasoline direct injection and hybrid systems.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Fuel type

- 2.2.4 Sales channel

- 2.2.5 Propulsions

- 2.2.6 Technology

- 2.2.7 Operating pressure range

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of GDI and CRDI engines

- 3.2.1.2 Technological advancements in Piezo materials

- 3.2.1.3 Growth of premium and luxury vehicle segments

- 3.2.1.4 Stricter emission regulations

- 3.2.1.5 Increased R&D investments by OEMs and Tier-1 suppliers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of piezoelectric injectors

- 3.2.2.2 Competition from improved solenoid injectors

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of hybrid powertrains

- 3.2.3.2 Diesel engine optimization in commercial vehicles

- 3.2.3.3 The widespread shift to gasoline direct injection (GDI) engines

- 3.2.3.4 Digital engine management and AI integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($ Mn, units)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.2.1 Hatchbacks

- 5.2.2 Sedans

- 5.2.3 SUVs

- 5.3 Commercial vehicles

- 5.3.1 Light commercial vehicles (LCV)

- 5.3.2 Medium commercial vehicles (MCV)

- 5.3.3 Heavy commercial vehicles (HCV)

Chapter 6 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.1.1 Gasoline

- 6.1.2 Diesel

- 6.1.3 Others

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 ICE

- 8.3 Hybrid

Chapter 9 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Direct injection (DI)

- 9.3 Common rail direct injection (CRDI)

- 9.4 Gasoline direct injection (GDI)

- 9.5 Port fuel injection (PFI)

Chapter 10 Market Estimates & Forecast, By Operating Pressure Range, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 Low pressure (<200 bar)

- 10.3 Medium pressure (200–1000 bar)

- 10.4 High pressure (>1000 bar)

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Aptiv

- 12.2 Continental

- 12.3 Delphi Technologies

- 12.4 Denso Corporation

- 12.5 Edelbrock LLC

- 12.6 Fuzhou Ruida Machinery

- 12.7 GB Remanufacturing

- 12.8 Hitachi Astemo Indiana

- 12.9 Infineon

- 12.10 Keihin

- 12.11 KYOCERA

- 12.12 Magneti Marelli Parts and Services.

- 12.13 Mikuni American

- 12.14 Murata Manufacturing

- 12.15 Robert Bosch

- 12.16 Siemens

- 12.17 Stanadyne

- 12.18 Valley Fuel Injection & Turbo

- 12.19 Woodward

- 12.20 WUZETEM