|

시장보고서

상품코드

1773474

늑골 골절 수복 시스템 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Rib Fracture Repair Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

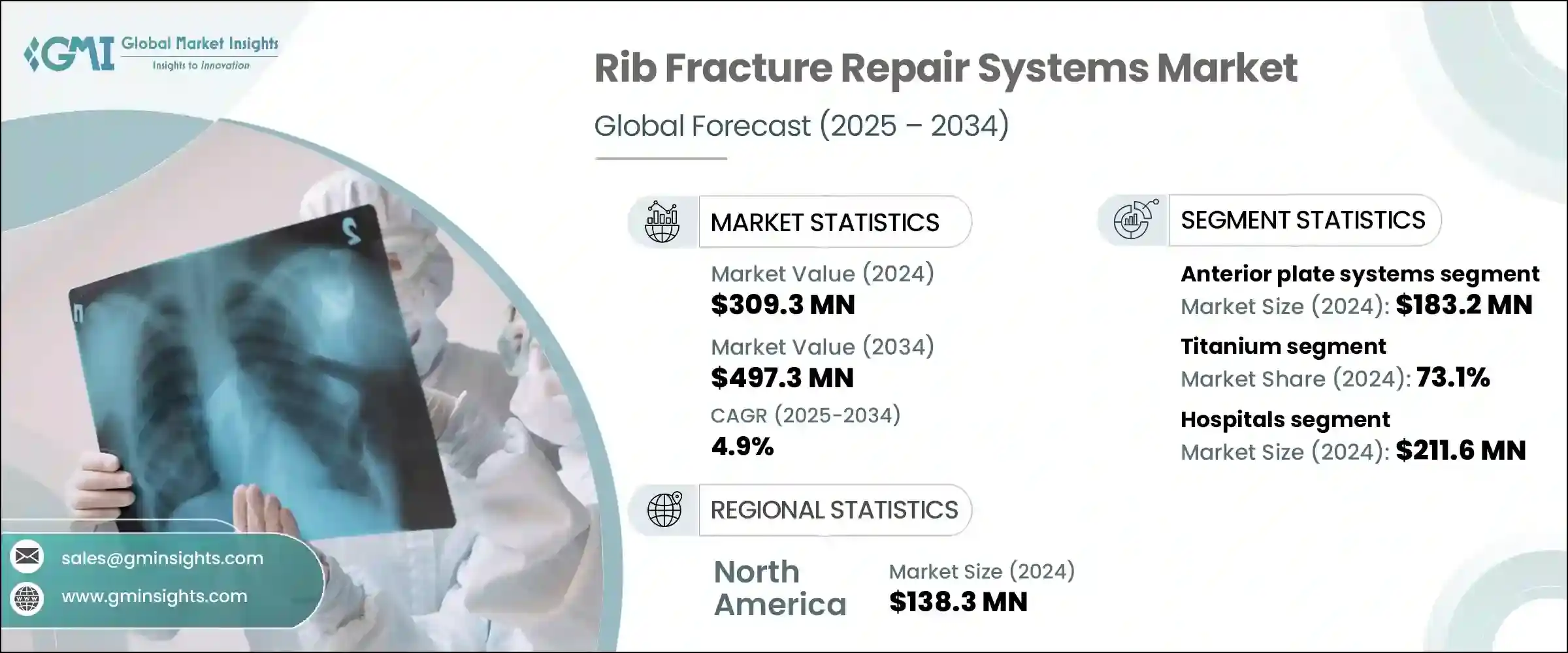

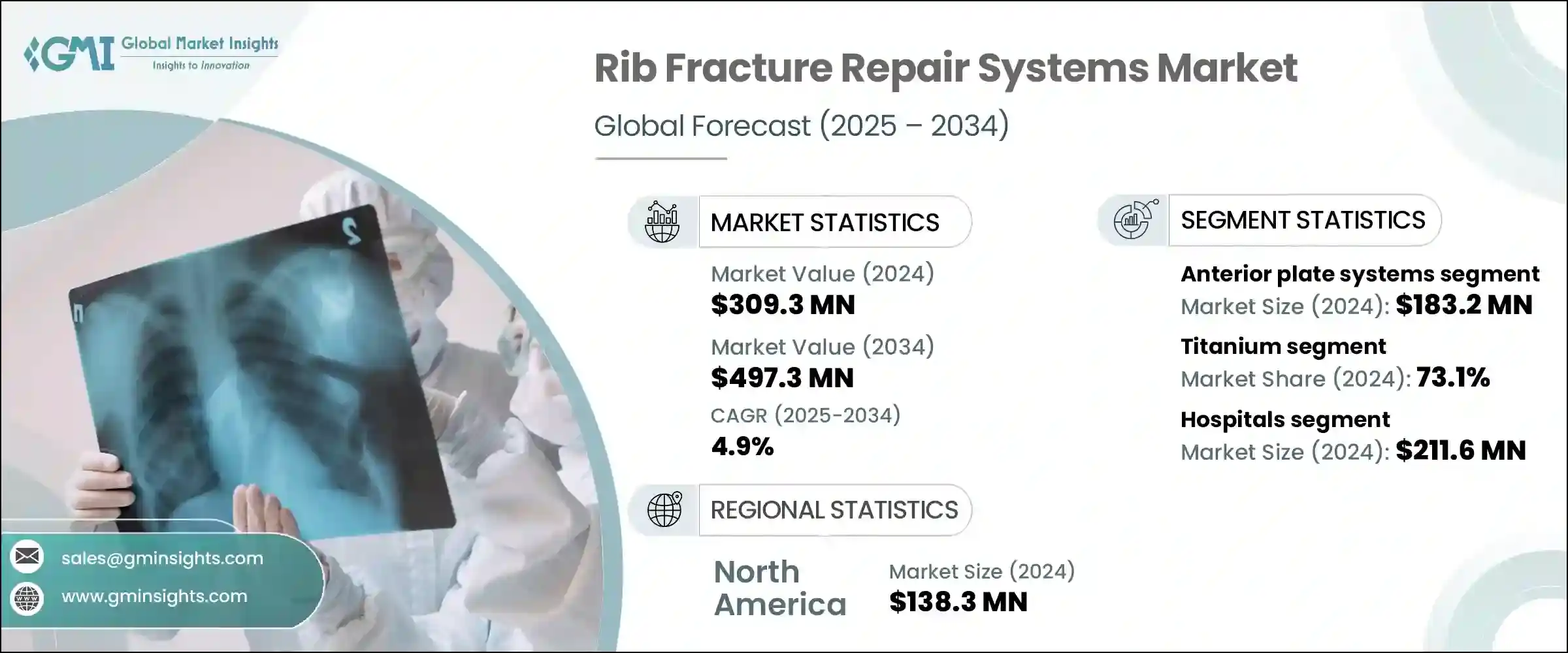

세계의 늑골 골절 수복 시스템 시장은 2024년에 3억 930만 달러로 평가되며, CAGR 4.9%로 성장하며, 2034년에는 4억 9,730만 달러에 달할 것으로 예측됩니다.

골절된 갈비뼈를 안정시키고 복원하도록 설계된 이 시스템은 전 세계에서 외상 관련 부상이 계속 증가함에 따라 수요가 증가하고 있습니다. 자동차 사고, 스포츠 관련 부상, 낙상으로 인한 사고는 특히 노인들 사이에서 신뢰할 수 있는 흉부 외상 중재의 필요성을 증가시키고 있습니다. 의료진이 조기 회복과 수술 후 합병증 감소를 우선시함에 따라 첨단 늑골 고정 기술에 대한 관심이 높아지고 있습니다. 병원과 외상 부서는 수술 시간을 단축할 뿐만 아니라 환자의 회복 결과를 개선하는 최소 침습 시스템에 투자하고 있습니다. 해부학적인 모양의 플레이트와 얇은 티타늄 시스템 등 개선된 임플란트 디자인은 수술의 정확도를 높이고 통증과 입원 기간을 줄입니다.

디지털 영상 기술의 발전과 최첨단 수술 기구의 조합은 갈비뼈 복원 시스템의 사용을 가속화하는 데 중요한 역할을 하고 있습니다. 이러한 기술 혁신은 외과의사에게 수술 중 더 높은 정확도와 더 나은 가시성을 제공하여 환자 결과를 개선하고 회복 시간을 단축하는 데 기여하고 있습니다. 그 결과, 갈비뼈 골절의 수복은 외상 치료뿐만 아니라 정형외과 및 흉부외과에서도 선호되는 솔루션이 되고 있습니다. 실시간 영상과 개선된 임플란트 설계를 기반으로 한 최소침습적 시술에 대한 신뢰가 높아지면서 시장 확대에 더욱 박차를 가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034 |

| 시작 금액 | 3억 930만 달러 |

| 예측 금액 | 4억 9,730만 달러 |

| CAGR | 4.9% |

2024년 전방 플레이트 시스템 분야 시장 규모는 1억 8,320만 달러에 달했습니다. 해부학적 형태로 인해 조직에 대한 자극을 최소화하고 수술 후 합병증 발생 가능성을 줄일 수 있으며, 인기가 높아지고 있습니다. 이러한 임플란트는 더 높은 편안함을 필요로 하는 환자나 심미성을 중시하는 환자들에게 선호되고 있습니다. 외과 의사들이 기능성과 편안함의 균형을 갖춘 효율적인 고정 시스템을 찾고 있는 가운데, 일상적인 수술이나 응급 수술에서 전방 플레이트가 점점 더 많이 선택되고 있습니다.

티타늄 기반 시스템 부문은 2024년 73.1%의 점유율을 차지했는데, 이는 주로 이 소재의 독보적인 강도 대 중량 비율에 기인합니다. 티타늄은 추가 하드웨어의 부피가 크지 않으면서도 강성을 제공하고, 호흡시 늑골의 자연스러운 움직임을 지원합니다. 흉곽 구조에 대한 적응성과 입증된 기계적 일관성은 치유 과정 동안 갈비뼈의 정렬을 효과적으로 유지하는 데 도움이 됩니다. 티타늄의 뛰어난 생체 적합성과 낮은 면역 반응 및 염증 유발 가능성은 외과적 수복에 있으며, 안전한 장기적인 솔루션으로, 늑골 골절 수복 솔루션에서 티타늄의 지속적인 우위를 지원하고 있습니다.

미국은 흉부 외상 발생률이 높고 의료 인프라가 발달되어 있으며, 2024년 미국 갈비뼈 골절 수리 시스템 시장 규모가 1억 2,480만 달러로 평가되었습니다. 자동차 충돌 사고, 노화에 따른 낙상, 스포츠 외상으로 인한 부상이 빈번하게 발생하면서 병원 및 외상 센터의 갈비뼈 고정 솔루션에 대한 수요가 증가하고 있으며, 3D 영상 시스템, 최소 침습 임플란트 등 첨단 수술 기술이 널리 보급된 미국 의료기관은 최첨단 갈비뼈 안정화 기술을 가장 먼저 채택하고 있습니다. 안정화 기술을 가장 먼저 도입하고 있습니다. 이러한 환경은 수술센터 전체에 티타늄 기반 정밀 엔지니어링 임플란트를 지속적으로 통합하는 것을 지원하여 국내 시장 확대에 기여하고 있습니다.

이 시장에 참여하고 있는 주요 기업에는 Able Medical Devices, Acumed, Arthrex, Jeil Medical, Johnson & Johnson, KLS Martin, Medtronic, Neuro France Implants, Orthofix, OsteoMed, Selective Surgical, Smith & Nephew, Stryker, Waston Medical, Zimmer Biomet 등이 있습니다. 이 분야의 선도적인 기업은 외과 의사의 선호도와 환자 고유의 해부학적 요구 사항을 모두 충족하는 혁신적이고 얇은 임플란트 디자인을 개발하는 데 주력하고 있습니다.

또한 티타늄 및 하이브리드 합금과 같은 생체적합성과 내구성이 뛰어난 소재를 생산하기 위한 연구개발에도 주력하고 있습니다. 외상센터 및 교육 병원과의 전략적 파트너십을 통해 조기 도입 및 피드백을 통한 제품 개선에 박차를 가하고 있습니다. 회사는 FDA 및 CE 승인을 통해 세계 입지를 확장하고 새로운 지역 시장에서 최소침습적 임플란트에 대한 접근성을 강화하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

- 에코시스템 분석

- 공급업체의 상황

- 밸류체인에 영향을 미치는 요인

- 업계에 대한 영향요인

- 촉진요인

- 흉부 외상의 발생률 상승

- 외과 고정 시스템의 기술적 진보

- 외래 및 통원 수술에 대한 선호도의 증가

- 신흥 시장에서 헬스케어비 지출과 인프라 개발의 증가

- 업계의 잠재적 리스크 & 과제

- 외과수술과 임플란트 시스템의 고비용

- 늑골 고정 솔루션의 인지도와 입수 용이성이 한정되어 있다.

- 시장 기회

- 외상 발생률이 높은 미개척 시장으로의 진출

- 3D 프린팅과 맞춤형 임플란트 기술의 통합

- 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 테크놀러지와 혁신의 상황

- 현재 기술 동향

- 신규 기술

- 향후 시장 동향

- 특허 분석

- 가격 분석

- 제품 유형별

- 지역별

- 갭 분석

- Porter의 산업 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십과 협업

- 신제품 발매

- 확장 계획

제5장 시장 추산·예측 : 제품 유형별, 2021 – 2034

- 주요 동향

- 전방 플레이트 시스템

- U 플레이트 시스템

제6장 시장 추산·예측 : 재료별, 2021 – 2034

- 주요 동향

- 티타늄

- 폴리에테르에테르케톤(PEEK)

- 기타 재료

제7장 시장 추산·예측 : 최종 용도별, 2021 – 2034

- 주요 동향

- 병원

- 외래 수술 센터

- 전문 클리닉

제8장 시장 추산·예측 : 지역별, 2021 – 2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트

제9장 기업 개요

- Able Medical Devices

- Acumed

- Arthrex

- Jeil Medical

- Johnson &Johnson

- KLS Martin

- Medtronic

- Neuro France Implants

- Orthofix

- OsteoMed

- Selective Surgical

- Smith &Nephew

- Stryker

- Waston Medical

- Zimmer Biomet

The Global Rib Fracture Repair Systems Market was valued at USD 309.3 million in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 497.3 million by 2034. These systems, designed to stabilize and realign fractured ribs, are seeing growing demand as trauma-related injuries continue to rise across the globe. Incidents stemming from vehicular accidents, sports-related injuries, and falls-particularly among the elderly-are increasing the need for reliable chest trauma interventions. As healthcare providers prioritize quicker recovery and reduced post-operative complications, the focus on advanced rib fixation techniques is intensifying. Hospitals and trauma units are investing in minimally invasive systems that not only minimize surgical duration but also improve patient recovery outcomes. Enhanced implant designs, such as anatomically shaped plates and low-profile titanium systems, are improving surgical precision while reducing pain and hospital stays.

Advancements in digital imaging technologies combined with state-of-the-art surgical instruments are playing a crucial role in accelerating the use of rib repair systems. These innovations provide surgeons with enhanced precision and better visualization during procedures, which leads to improved patient outcomes and shorter recovery times. As a result, rib fracture repair is becoming a preferred solution not only in trauma care but also within orthopedic and thoracic surgery units. The growing confidence in minimally invasive techniques, supported by real-time imaging and improved implant designs, is further driving market expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $309.3 Million |

| Forecast Value | $497.3 Million |

| CAGR | 4.9% |

The anterior plate systems segment was valued at USD 183.2 million in 2024. Their growing popularity comes from their anatomical shaping, which helps minimize tissue irritation and reduce the chance of post-surgical complications. These implants are preferred in patients who require enhanced comfort or for those where aesthetics is a consideration. With surgeons seeking efficient fixation systems that balance functionality and comfort, anterior plates are increasingly selected for both routine and emergency procedures.

The titanium-based systems segment captured a 73.1% share in 2024, largely due to the material's unmatched strength-to-weight ratio. Titanium offers rigidity without excess hardware bulk, supporting the rib's natural motion during respiration. Its adaptability to the thoracic structure and proven mechanical consistency help maintain rib alignment effectively throughout the healing process. Titanium's exceptional biocompatibility and low likelihood of causing immune responses or inflammation make it a safe long-term solution in surgical repairs, fueling its continued dominance in rib fracture repair solutions.

United States Rib Fracture Repair Systems Market was valued at USD 124.8 million in 2024 due to its high rate of chest trauma cases and its advanced healthcare infrastructure. Frequent injuries caused by motor vehicle collisions, aging-related falls, and sports trauma are driving hospital and trauma center demand for rib fixation solutions. With the widespread adoption of high-end surgical technologies, including 3D imaging systems and minimally invasive implants, U.S. institutions are early adopters of cutting-edge rib stabilization technologies. This environment supports the continuous integration of titanium-based, precision-engineered implants throughout surgical centers, contributing to national market expansion.

Key players involved in the market include Able Medical Devices, Acumed, Arthrex, Jeil Medical, Johnson & Johnson, KLS Martin, Medtronic, Neuro France Implants, Orthofix, OsteoMed, Selective Surgical, Smith & Nephew, Stryker, Waston Medical, Zimmer Biomet. Prominent companies in this space are intensifying their focus on developing innovative, low-profile implant designs that meet both surgeon preferences and patient-specific anatomical requirements.

They are also emphasizing R&D to produce biocompatible and durable materials like titanium and hybrid alloys. Strategic partnerships with trauma centers and teaching hospitals help drive early adoption and feedback-driven product refinement. Firms are expanding their global footprint through FDA and CE approvals, enhancing access to minimally invasive implants in new regional markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360º synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Material

- 2.2.4 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of chest trauma injuries

- 3.2.1.2 Technological advancements in surgical fixation systems

- 3.2.1.3 Growing preference for outpatient and ambulatory surgical procedures

- 3.2.1.4 Increased healthcare spending and infrastructure development in emerging markets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of surgical procedures and implant systems

- 3.2.2.2 Limited awareness and availability of rib fixation solutions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into underpenetrated markets with high trauma incidence

- 3.2.3.2 Integration of 3D printing and personalized implant technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Patent analysis

- 3.8 Pricing analysis

- 3.8.1 By product type

- 3.8.2 By region

- 3.9 Gap analysis

- 3.10 Porter's analysis

- 3.11 PESTLE analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Anterior plate systems

- 5.3 U-plate systems

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Titanium

- 6.3 Polyether ether ketone (PEEK)

- 6.4 Other materials

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty clinics

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profile

- 9.1 Able Medical Devices

- 9.2 Acumed

- 9.3 Arthrex

- 9.4 Jeil Medical

- 9.5 Johnson & Johnson

- 9.6 KLS Martin

- 9.7 Medtronic

- 9.8 Neuro France Implants

- 9.9 Orthofix

- 9.10 OsteoMed

- 9.11 Selective Surgical

- 9.12 Smith & Nephew

- 9.13 Stryker

- 9.14 Waston Medical

- 9.15 Zimmer Biomet