|

시장보고서

상품코드

1773478

플렌옵틱 카메라 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Plenoptic Camera Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

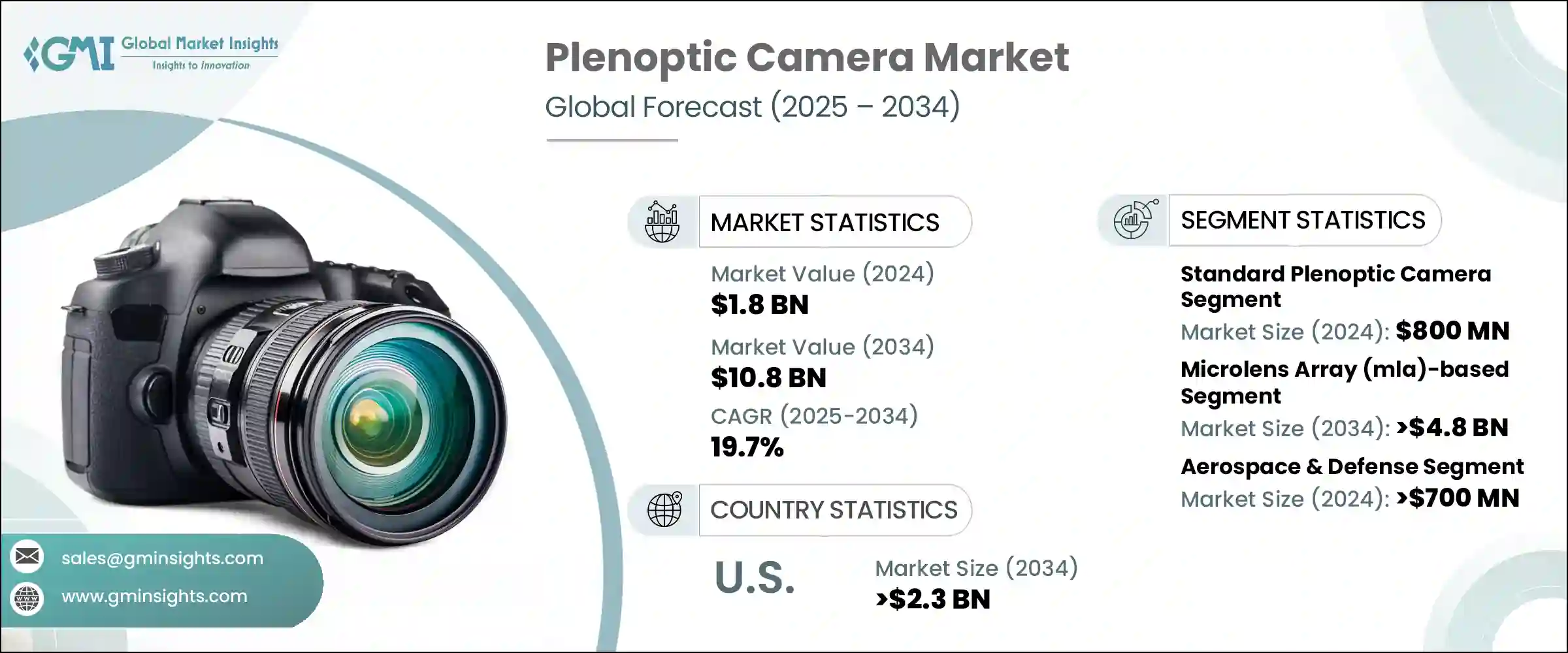

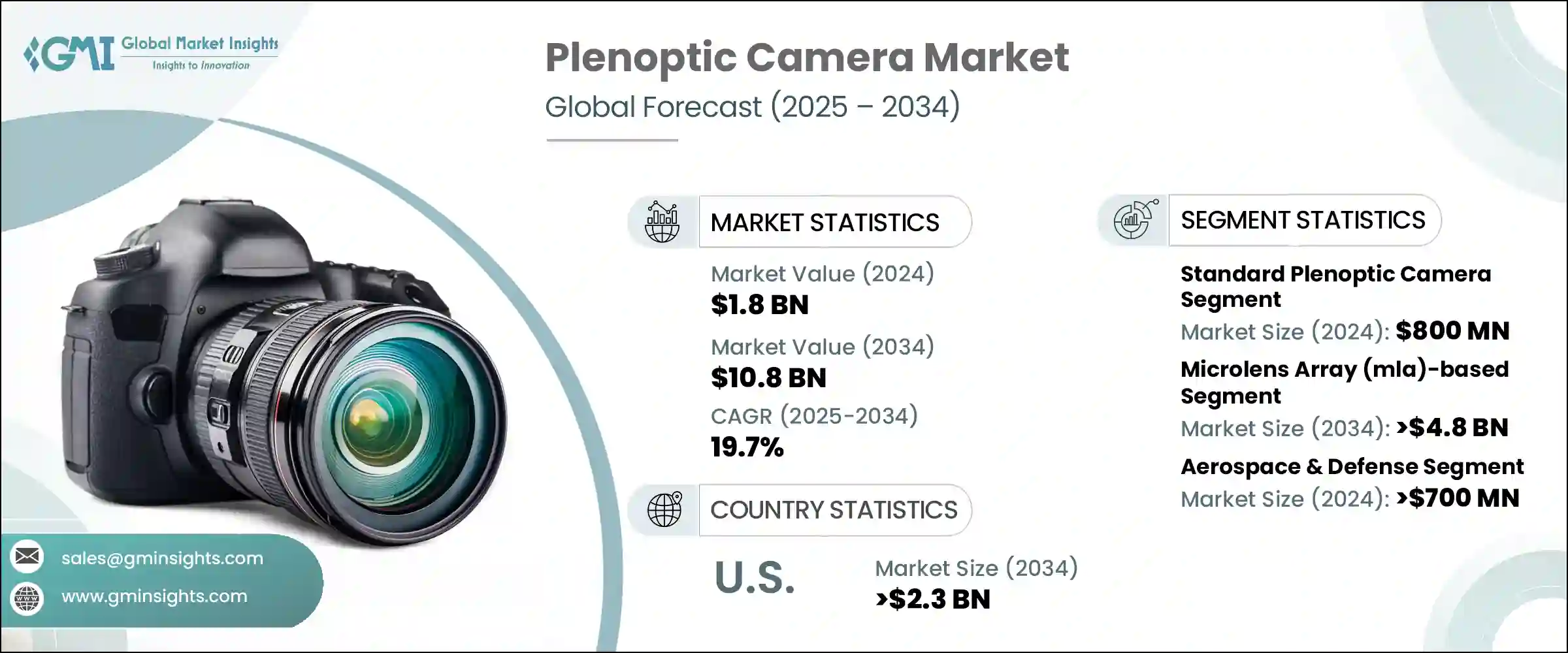

세계의 플렌옵틱 카메라 시장은 2024년에는 18억 달러로 평가되며, CAGR 19.7%로 성장하며, 2034년에는 108억 달러에 달할 것으로 예측됩니다.

이미징 시스템, 특히 마이크로 렌즈와 카메라 어레이 기술의 발전은 깊은 공간 정보를 가진 고해상도 영상을 촬영하는 방법을 재구성하고 있습니다. 산업 자동화, 가전기기, 의료 진단, 몰입형 미디어 등에서 채택이 확대되고 있으며, 시장 성장을 촉진하고 있습니다. 이러한 카메라는 캡처 후 재초점 및 3D 이미징과 같은 고유한 기능으로 사용자에게 힘을 실어주며, AR/VR, 로봇 공학, 머신 비전과 같은 용도에 매력적으로 작용하고 있습니다.

컴퓨팅 포토그래피가 부상함에 따라 스마트폰과 의료기기에 통합되는 것이 일반화되고 있습니다. 또한 스타트업과 기술 대기업의 지속적인 연구개발 투자는 전체 광학 이미지 시스템의 한계를 뛰어넘어 그 속도를 더욱 가속화하고 있습니다. 트럼프 행정부에서 시작된 관세 분쟁은 수입 부품에 의존하는 제조업체에 가격 측면의 도전을 가져오고 있습니다. 필수 부품의 비용이 상승함에 따라 미국 제조업체는 마진 감소에 직면하거나 가격 인상을 고객에게 전가해야 합니다. 국내 대체품이 없기 때문에 이들 기업은 경쟁력을 유지하기 위해 생산 비용을 최적화하고 조달 전략을 전환해야 하는 상황에 직면해 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034 |

| 시작 금액 | 18억 달러 |

| 예측 금액 | 108억 달러 |

| CAGR | 19.7% |

표준 프레노픽 카메라 부문은 2024년 8억 달러로 평가되었습니다. 이 카메라는 메인 렌즈와 센서 사이에 배치된 마이크로 렌즈 어레이를 특징으로 하며, 공간과 각도의 광학 데이터를 모두 기록합니다. 이 구성은 4D 프리노픽 데이터를 생성하여 사용자가 촬영 후 초점과 원근감을 조정할 수 있도록 합니다. 이러한 기능으로 인해 표준 프레노픽 카메라는 이미지 깊이와 후처리의 유연성이 중요한 연구, 크리에이티브 미디어, 사진 촬영에 이상적입니다. 그러나 각도 해상도와 공간 해상도의 균형을 맞출 필요성은 이미지의 선명도에 계속 영향을 미치고 있습니다.

마이크로 렌즈 어레이(MLA) 기반 카메라 분야는 2034년까지 48억 달러 규모에 달할 것으로 예측됩니다. 이 시스템은 주 렌즈와 센서 사이에 배치된 마이크로 렌즈 어레이를 사용하여 다방향의 빛을 포착하여 평면적인 2D 캡처를 상세한 전천후 이미지로 변환합니다. 이 이미지 처리 방법은 촬영 후 재초점 및 깊이 매핑과 같은 기능을 지원하여 영화 제작, 과학 연구, 가상 시각화 등의 분야에서 필수적이며, MLA를 통해 광선 경로를 재현할 수 있는 능력은 사용자에게 깊이와 정확도가 향상된 풍부하고 몰입감 있는 시청 경험을 제공합니다. 제공합니다.

미국 프레노픽 카메라 시장은 2034년까지 23억 달러에 달할 것으로 예측됩니다. 미국은 탄탄한 기술 환경과 혁신 주도형 생태계로 인해 세계 수요에 중요한 기여를 하고 있으며, AR 및 VR 기술에 대한 높은 관심은 몰입감 있고 반응성이 뛰어난 시각적 환경을 만들 수 있는 카메라에 대한 수요를 계속 증가시키고 있습니다. 첨단 연구센터와 미래형 이미지 처리 툴의 빠른 도입으로 미국은 이 분야에서 우위를 유지할 것으로 예측됩니다.

시장에 영향을 미치는 주요 기업에는 Canon Inc., Adobe Inc., Apple Inc., Raytrix GmbH, Google LLC 등이 있으며, 이들 기업이 함께 기술 혁신과 기술 리더십을 추진하고 있습니다. 프레노픽 카메라 시장의 주요 기업은 기술 혁신을 우선시하고 응용 범위를 확대하여 발판을 다지고 있습니다. 각 업체들은 심도 매핑, 실시간 3D 렌더링, 촬영 후 편집 기능을 강화한 차세대 영상 솔루션 개발을 위한 R&D 투자를 확대하고 있으며, AR/VR, 헬스케어, 자율 시스템 분야 기업과의 전략적 파트너십도 인기를 끌고 있습니다. 이러한 파트너십을 통해 기업은 특정 이용 사례에 맞게 프레노픽 기술을 조정할 수 있습니다. 또한 기업은 실시간 성능을 향상시키기 위해 소프트웨어 통합과 엣지 컴퓨팅의 호환성에 초점을 맞추었습니다.

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

- 에코시스템 분석

- 트럼프 정권 관세에 대한 영향

- 무역에 대한 영향

- 무역량 혼란

- 보복 조치

- 업계에 대한 영향

- 공급측 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구축

- 생산비용에 대한 영향

- 수요측 영향(판매 가격)

- 최종 시장에 대한 가격 전달

- 시장 점유율 동향

- 소비자 반응 패턴

- 공급측 영향(원재료)

- 영향을 받는 주요 기업

- 전략적 업계 대응

- 공급망 재구성

- 가격결정과 제품 전략

- 정책 관여

- 전망과 향후 검토 사항

- 무역에 대한 영향

- 업계에 대한 영향요인

- 촉진요인

- 영상 기술의 진보

- 몰입형 컨텐츠(VR/AR)의 수요 증가

- 의료 영상에서 사용의 증가

- 산업용 애플리케이션(머신 비전, 로봇 공학)에서의 채택 증가

- 가전제품에 대한 통합

- 업계의 잠재적 리스크 & 과제

- 높은 생산비용

- 기술에 대한 소비자의 인지도와 이해가 한정되어 있다.

- 성장 가능성 분석

- 규제 상황

- 테크놀러지의 상황

- 향후 시장 동향

- 갭 분석

- Porter의 산업 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추산·예측 : 유형별, 2021-2034

- 표준 플렌옵틱 카메라(예 : lytro illum)

- 포커스 플렌옵틱 카메라

- Coded aperture 플렌옵틱 카메라

- 스테레오 플렌옵틱 카메라

제6장 시장 추산·예측 : 기술별, 2021-2034

- 마이크로 렌즈 어레이(MLA) 기반

- Multi-aperture 이미징

- 플렌옵틱 이미징

- 기타

제7장 시장 추산·예측 : 최종 용도별, 2021-2034

- 항공우주 및 방위

- 자동차·운송

- 일렉트로닉스 및 반도체

- 헬스케어와 생명과학

- 기타

제8장 시장 추산·예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트

제9장 기업 개요

- Adobe Inc.

- Apple Inc.

- Avegant Corporation

- Canon Inc.

- FoVI 3D, Inc.

- Google LLC

- Japan Display Inc.

- OTOY Inc.

- Panasonic Corporation

- Raytrix GmbH(Germany)

- Ricoh Innovations Corporation

- Samsung Electronics Co., Ltd.

- Sony Group Corporation

- Xiaomi Corporation

The Global Plenoptic Camera Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 19.7% to reach USD 10.8 billion by 2034. Advancements in imaging systems, especially in microlens and camera array technologies, are reshaping how high-resolution visuals with deep spatial information are captured. Growing adoption across industrial automation, consumer electronics, medical diagnostics, and immersive media is fueling market growth. These cameras empower users with unique features like post-capture refocusing and 3D imaging, making them attractive for applications in AR/VR, robotics, and machine vision.

As computational photography gains ground, integration into smartphones and medical devices is becoming more common. Additionally, ongoing investments in R&D by startups and tech leaders are pushing the boundaries of plenoptic imaging systems, further driving momentum. The tariff conflict initiated during the Trump administration has created pricing challenges for manufacturers relying on imported components. As the cost of essential parts rises, manufacturers in the U.S. either face reduced margins or must pass price increases to customers. Without viable domestic alternatives, these companies are under pressure to optimize production costs or shift sourcing strategies to remain competitive.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $10.8 Billion |

| CAGR | 19.7% |

The standard plenoptic cameras segment was valued at USD 800 million in 2024. These cameras feature a microlens array placed between the main lens and the sensor to record both spatial and angular light data. This configuration produces 4D plenoptic data, enabling users to adjust focus or perspective after capture. These capabilities make standard plenoptic cameras ideal for research, creative media, and photography, where image depth and post-processing flexibility matter. However, the need to balance angular and spatial resolution continues to influence image clarity.

The microlens array (MLA)-based camera segment is poised to reach USD 4.8 billion by 2034. These systems use a microlens array placed between the primary lens and sensor to trap light from multiple directions, transforming flat 2D captures into detailed plenoptic images. This imaging method supports functions like post-capture refocusing and depth mapping, which are essential in fields such as film production, scientific research, and virtual visualization. The ability to replicate light ray pathways through MLA offers users a rich, immersive viewing experience with enhanced depth and precision.

United States Plenoptic Camera Market is expected to reach USD 2.3 billion by 2034. The country remains a vital contributor to global demand thanks to its robust technological landscape and innovation-driven ecosystem. Strong interest in AR and VR technologies continues to elevate the demand for cameras capable of creating immersive and responsive visual environments. With advanced research centers and the rapid adoption of futuristic imaging tools, the U.S. is expected to maintain its dominance in this space.

Key players influencing the market include Canon Inc., Adobe Inc., Apple Inc., Raytrix GmbH, and Google LLC, who collectively drive innovation and technological leadership. Leading companies in the plenoptic camera market are strengthening their foothold by prioritizing innovation and expanding their application scope. They are increasing R&D investments to develop next-generation imaging solutions that offer enhanced depth mapping, real-time 3D rendering, and post-capture editing capabilities. Strategic partnerships with firms in the AR/VR, healthcare, and autonomous systems sectors are also gaining traction. These collaborations allow companies to tailor their plenoptic technologies for specific use cases. Additionally, firms are focusing on software integration and edge computing compatibility to boost real-time performance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Advancements in imaging technology

- 3.3.3 Growing demand for immersive content (VR/AR)

- 3.3.4 Increasing use in medical imaging

- 3.3.5 Rising adoption in industrial applications (machine vision, robotics)

- 3.3.6 Integration into consumer electronics

- 3.3.7 Industry pitfalls and challenges

- 3.3.8 High production costs

- 3.3.9 Limited consumer awareness and understanding of the technology

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion)

- 5.1 Standard plenoptic camera (e.g., lytro illum)

- 5.2 Focused plenoptic camera

- 5.3 Coded aperture plenoptic camera

- 5.4 Stereo plenoptic camera

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Billion)

- 6.1 Microlens array (mla)-based

- 6.2 Multi-aperture imaging

- 6.3 Plenoptic imaging

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion)

- 7.1 Aerospace & defense

- 7.2 Automotive & transportation

- 7.3 Electronics & semiconductors

- 7.4 Healthcare & life sciences

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Adobe Inc.

- 9.2 Apple Inc.

- 9.3 Avegant Corporation

- 9.4 Canon Inc.

- 9.5 FoVI 3D, Inc.

- 9.6 Google LLC

- 9.7 Japan Display Inc.

- 9.8 OTOY Inc.

- 9.9 Panasonic Corporation

- 9.10 Raytrix GmbH (Germany)

- 9.11 Ricoh Innovations Corporation

- 9.12 Samsung Electronics Co., Ltd.

- 9.13 Sony Group Corporation

- 9.14 Xiaomi Corporation