|

시장보고서

상품코드

1773479

터렛 시스템 시장 기회, 성장 촉진요인, 산업 동향 분석과 예측(2025-2034년)Turret System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

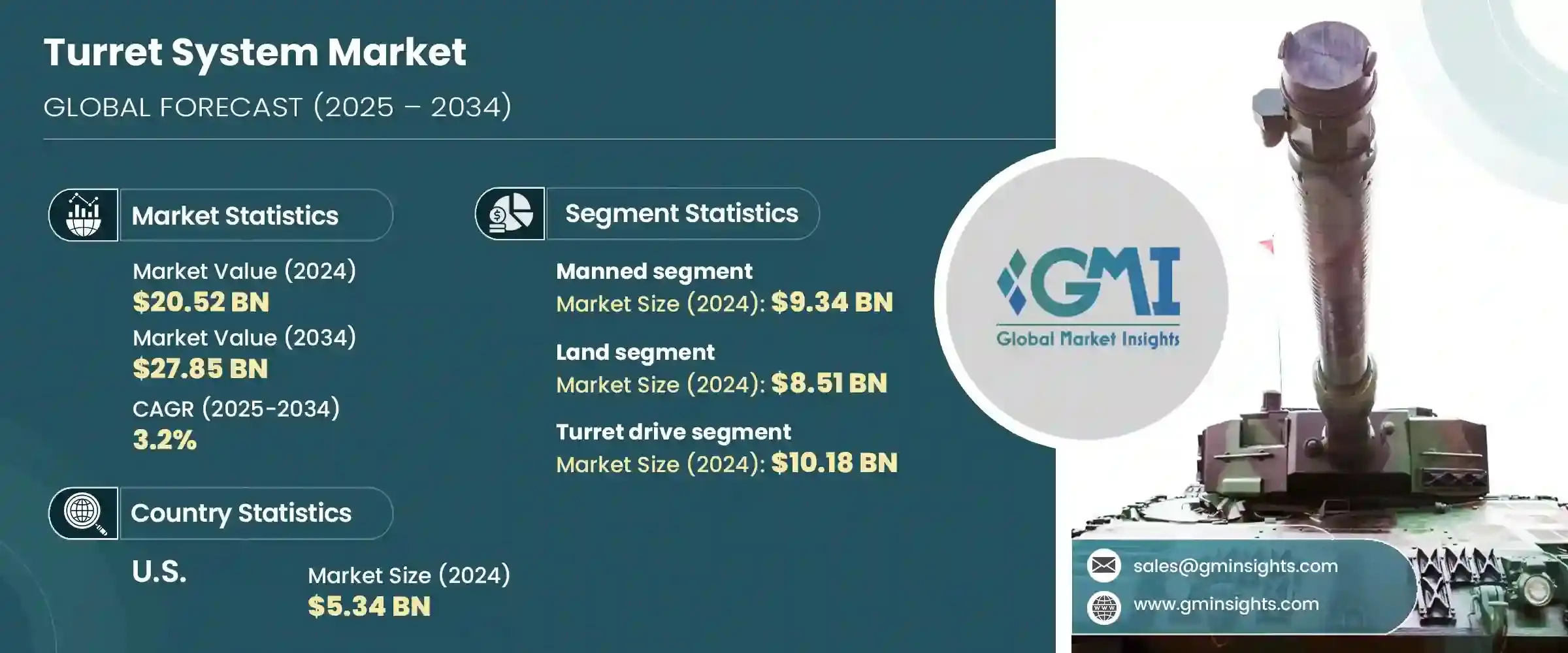

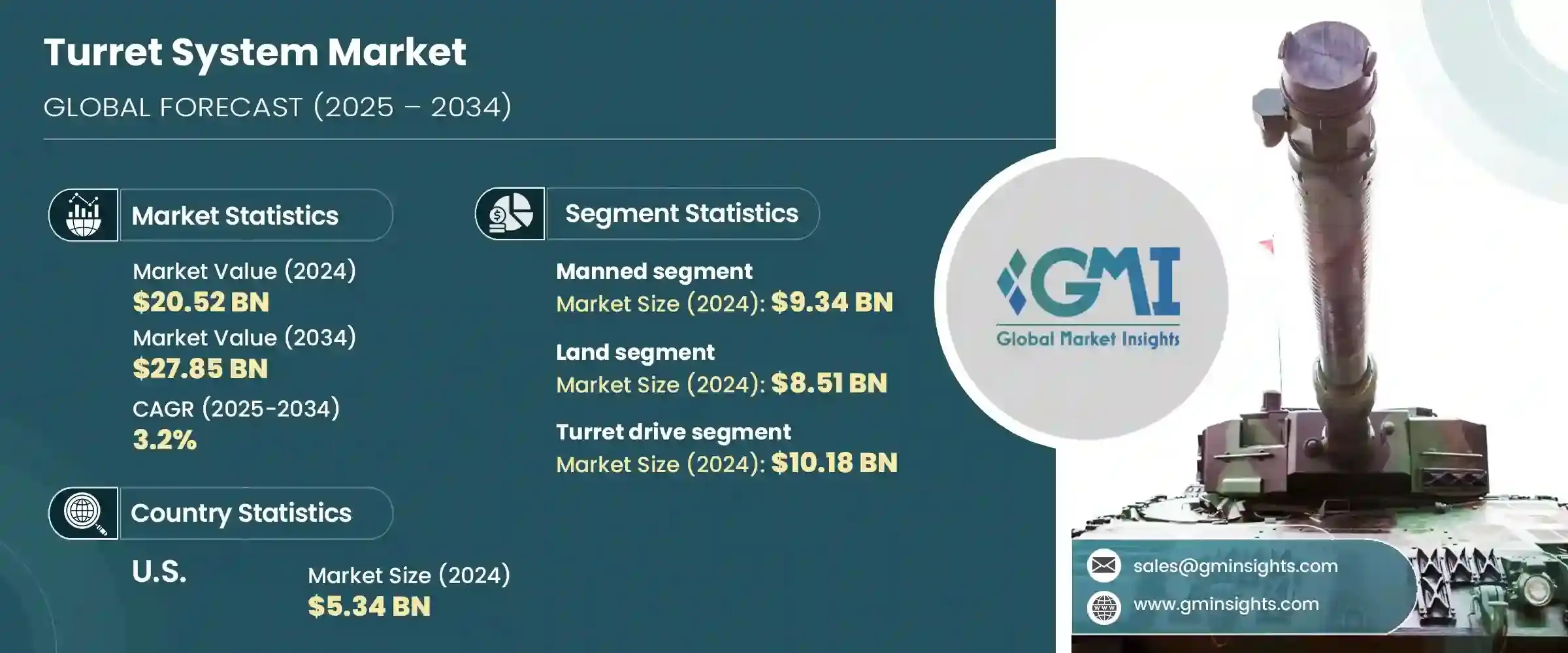

세계의 터렛 시스템 시장은 2024년에는 205억 2,000만 달러에 달하며, CAGR 3.2%로 성장하며, 2034년에는 278억 5,000만 달러에 달할 것으로 예측됩니다.

이러한 성장은 전 세계 군비 증가에 따른 것으로, 북미, 유럽, 아시아태평양 등의 지역에서 수요가 크게 증가하고 있습니다. 국방 예산이 계속 확대됨에 따라 군의 현대화와 전투 준비태세 강화에 초점이 맞추어지고 있습니다. 첨단 포탑 시스템, 특히 무인 포탑 시스템은 임무 수행 능력을 향상시키고, 인원에 대한 위험을 줄이며, 역동적인 작전 환경에서 전략적 효율성을 가능하게 하는 능력으로 인해 많은 지지를 받고 있습니다.

정부의 국방 연구개발에 대한 투자 증가는 특히 AI, 자동화, 감각 통합과 같은 포탑 시스템 기술의 혁신을 촉진하고 있습니다. 이러한 발전은 로봇 시스템 및 차량 탑재형 포탑이 달성할 수 있는 한계에 도전하고 있으며, 그 결과 계약 체결이 빨라지고 민간 방산업체들의 생산이 증가하고 있습니다. 자율 내비게이션 및 AI 기반 위협 인식과 같은 기술은 전장을 재구성하고 있습니다. 이들은 실시간 상황 인식, 지능형 의사결정, 자율적 기동, 위험한 임무에 대한 인간의 개입을 최소화하고 다양한 지형과 시나리오에서 작전 효과를 극대화하는 데 필수적인 요소입니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034 |

| 시작 금액 | 205억 2,000만 달러 |

| 예측 금액 | 278억 5,000만 달러 |

| CAGR | 3.2% |

유인 터렛 시스템 부문은 2024년 93억 4,000만 달러를 창출했습니다. 이러한 시스템은 인간의 판단이 매우 중요한 복잡한 실시간 상황에서의 운용 적응성으로 인해 계속해서 우위를 점하고 있습니다. 유인 포탑의 신뢰성은 이미 입증되었으며, 많은 군는 유인 포탑을 그대로 교체하는 대신 기존 장갑차 포대를 차세대 유인 솔루션으로 업그레이드하는 것을 선택하고 있습니다. 도심 전투나 대반란 작전 등 첨단 상황 인식이 필요한 임무는 앞으로도 유인 시스템에 크게 의존할 것으로 예측됩니다.

육상 포탑 부문은 2024년 85억 1,000만 달러를 창출했습니다. 전 세계 국방 지출 증가와 진화하는 위협에 대한 신속한 대응의 필요성이 증가함에 따라 육상 차량은 유인 및 무인 플랫폼 모두에 첨단 포탑 시스템을 장착하고 있습니다. 무인 지상 차량(UGV)의 배치가 증가함에 따라 원격으로 조작할 수 있는 포탑 시스템의 필요성이 증가하고 있습니다. 자동화, 고정밀 센서, AI 구동 제어 시스템의 혁신으로 육상 포탑 플랫폼의 치사율, 정확도, 비용 효율성이 향상되고 있습니다.

독일 터렛 시스템 2024년 시장 규모 9억 5,000만 달러. 인더스트리 4.0과 디지털 주권을 향한 국가적 추진으로 자율 및 반자율 군 시스템에 대한 투자가 확대되고 있습니다. 여기에는 육상 차량과 공중 방어 플랫폼에 사용되는 첨단 포탑 시스템의 조달 증가도 포함됩니다. 무기 수출 강국인 독일은 세계 경쟁력을 유지하기 위해 기술 혁신을 지속적으로 강화하고 있습니다. 감시 및 국경 방어와 같은 임무에서 AI 기반 로봇 공학에 대한 의존도가 높아지는 것은 보안 요구 사항의 변화와 운영의 복잡성에 적응할 준비가 되어 있다는 것을 입증합니다.

시장 상황을 형성하는 주요 기업으로는 BAE Systems, Elbit Systems, General Dynamics Land Systems 등이 있습니다. 터렛 시스템 시장의 주요 기업은 무인화 및 AI 통합 포탑 기술의 혁신을 추진하기 위해 연구개발에 많은 투자를 하고 있습니다. 국방부 및 정부 기관과의 전략적 협력 관계는 장기 조달 계약을 확보하는 데 도움이 됩니다. 경쟁력을 강화하기 위해 제조업체는 생산 능력을 확장하고, 모듈식 포탑 아키텍처를 최적화하고, 성능을 유지하면서 무게를 줄이기 위해 최첨단 소재를 도입하고 있습니다. 또한 합병, 인수, 제휴를 통해 새로운 지역 시장을 개발하고 제품 포트폴리오를 다양화하고 있습니다. 또한 기업은 완전한 교체보다는 차세대 기능을 갖춘 레거시 플랫폼의 업그레이드에 중점을 두어 기존 방산 고객과의 관계를 유지하고, 수명주기 지원 및 시스템 리노베이션을 통해 지속적인 매출을 확보하는 데 도움을 주고 있습니다.

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

- 에코시스템 분석

- 트럼프 정권 관세에 대한 영향

- 무역에 대한 영향

- 무역량 혼란

- 보복 조치

- 업계에 대한 영향

- 공급측 영향

- 주요 부품의 가격 변동

- 공급망 재구축

- 생산비용에 대한 영향

- 수요측 영향(판매 가격)

- 최종 시장에 대한 가격 전달

- 시장 점유율 동향

- 소비자 반응 패턴

- 공급측 영향

- 영향을 받는 주요 기업

- 전략적 업계 대응

- 공급망 재구성

- 가격결정과 제품 전략

- 정책 관여

- 전망과 향후 검토 사항

- 무역에 대한 영향

- 업계에 대한 영향요인

- 촉진요인

- 국방 예산의 증가와 군 현대화

- 기술 혁신과 자동화

- 지정학적 긴장과 안보 위협

- 안보·방위 인프라의 확대

- 애플리케이션의 다양화

- 업계의 잠재적 리스크 & 과제

- 높은 개발과 조달비

- 급속한 기술 진부화

- 촉진요인

- 성장 가능성 분석

- 규제 상황

- 테크놀러지의 상황

- 향후 시장 동향

- 갭 분석

- Porter의 산업 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추산·예측 : 유형별, 2021-2034

- 주요 동향

- 유인

- 무인

제6장 시장 추산·예측 : 컴포넌트별, 2021-2034

- 주요 동향

- 포탑 구동장치

- 포탑 제어

- 안정화 유닛

제7장 시장 추산·예측 : 플랫폼별, 2021-2034

- 주요 동향

- 토지

- 모바일/차량

- 고정식/고정형

- 낙하산

- 공격 헬리콥터

- 전투기

- 특수 임무 항공기

- 무인항공기(UAV)

- 해군

- 구축함

- 프리깃함

- 해양지원선(Oosts)

- 콜벳

- 초계·기뢰 소해정

- 수륙양용선

- 잠수함

- 무인 수상정(미국)

제8장 시장 추산·예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트

제9장 기업 개요

- BAE Systems

- Elbit Systems Ltd.

- General Dynamics Corporation

- Leonardo S.p.A.

- Lockheed Martin Corporation

- Moog Inc.

- Northrop Grumman

- RAFAEL Advanced Defense Systems Ltd.

- Rheinmetall AG

- Thales

The Global Turret System Market was valued at USD 20.52 billion in 2024 and is estimated to grow at a CAGR of 3.2% to reach USD 27.85 billion by 2034. This growth is largely fueled by increasing global military expenditures, with significant demand coming from regions like North America, Europe, and Asia-Pacific. As defense budgets continue to expand, the focus shifts toward military modernization and enhanced combat readiness. Advanced turret systems, especially unmanned ones, are gaining traction due to their ability to enhance mission performance, reduce risks to personnel, and enable strategic efficiency in dynamic operational environments.

Increased investments in defense R&D from government sources are propelling innovation in turret system technologies, particularly in AI, automation, and sensory integration. These advancements are pushing the boundaries of what robotic systems and vehicle-mounted turrets can achieve, resulting in faster contract awards and increased production from private defense firms. Technologies like autonomous navigation and AI-based threat recognition are reshaping the battlefield. They provide real-time situational awareness, intelligent decision-making, and autonomous maneuvering-all critical for minimizing human involvement in dangerous missions and maximizing operational effectiveness across varied terrains and scenarios.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $20.52 Billion |

| Forecast Value | $27.85 Billion |

| CAGR | 3.2% |

The manned turret system segment generated USD 9.34 billion in 2024. These systems continue to dominate due to their operational adaptability in complex, real-time situations where human judgment remains crucial. Manned turrets offer proven reliability, and instead of replacing them outright, many armed forces are opting to upgrade existing armored fleets with next-gen manned solutions. Missions requiring heightened situational awareness-such as urban combat or counterinsurgency operations-are expected to continue relying heavily on manned systems.

The land-based turret segment generated USD 8.51 billion in 2024. With global defense spending on the rise and the growing need for rapid response to evolving threats, land vehicles are being equipped with advanced turret systems for both manned and unmanned platforms. The rise in deployment of Unmanned Ground Vehicles (UGVs) has amplified the need for turret systems capable of remote operation. Innovations in automation, precision sensors, and AI-driven control systems are making land turret platforms more lethal, accurate, and cost-effective.

Germany Turret System Market generated USD 950 million in 2024. A national push toward Industry 4.0 and digital sovereignty has led to expanded investment in autonomous and semi-autonomous military systems. This includes increased procurement of advanced turret systems for use in both land vehicles and aerial defense platforms. As one of the top arms-exporting countries, Germany continues to boost innovation to remain competitive globally. A growing reliance on AI-powered robotics for tasks like surveillance and border defense underlines the nation's readiness to adapt to shifting security demands and operational complexity.

Key players shaping the Turret System Market landscape include BAE Systems, Elbit Systems, and General Dynamics Land Systems. Leading companies in the turret system market are investing heavily in R&D to drive innovation in unmanned and AI-integrated turret technologies. Strategic collaborations with defense ministries and government agencies help secure long-term procurement contracts. To strengthen their competitive position, manufacturers are expanding production capabilities, optimizing modular turret architectures, and incorporating cutting-edge materials to reduce weight while maintaining performance. Mergers, acquisitions, and partnerships also allow players to tap into new regional markets and diversify their product portfolios. Furthermore, companies are focusing on upgrading legacy platforms with next-gen capabilities rather than full replacements, helping them maintain relationships with established defense clients and ensure recurring revenue through lifecycle support and system retrofitting.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the Industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising defense budgets and military modernization

- 3.3.1.2 Technological innovations and automation

- 3.3.1.3 Geopolitical tensions and security threats

- 3.3.1.4 Expansion of security and defense infrastructure

- 3.3.1.5 Diversification of applications

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High development and procurement costs

- 3.3.2.2 Rapid technological obsolescence

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Manned

- 5.3 Unmanned

Chapter 6 Market Estimates and Forecast, By Component, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Turret drive

- 6.3 Turret control

- 6.4 Stabilization unit

Chapter 7 Market Estimates and Forecast, By Platform, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Land

- 7.2.1 Mobile/vehicular

- 7.2.2 Fixed/stationary

- 7.3 Airborne

- 7.3.1 Attack helicopters

- 7.3.2 Fighter aircrafts

- 7.3.3 Special mission aircrafts

- 7.3.4 Unmanned aerial vehicles (UAVs)

- 7.4 Naval

- 7.4.1 Destroyer

- 7.4.2 Frigates

- 7.4.3 Offshore support vessels (Oosts)

- 7.4.4 Corvettes

- 7.4.5 Patrol & mine countermeasure vessels

- 7.4.6 Amphibious vessels

- 7.4.7 Submarines

- 7.4.8 Unmanned surface vehicles (USAs)

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BAE Systems

- 9.2 Elbit Systems Ltd.

- 9.3 General Dynamics Corporation

- 9.4 Leonardo S.p.A.

- 9.5 Lockheed Martin Corporation

- 9.6 Moog Inc.

- 9.7 Northrop Grumman

- 9.8 RAFAEL Advanced Defense Systems Ltd.

- 9.9 Rheinmetall AG

- 9.10 Thales