|

시장보고서

상품코드

1782092

흉부외과 기기 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Thoracic Surgery Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

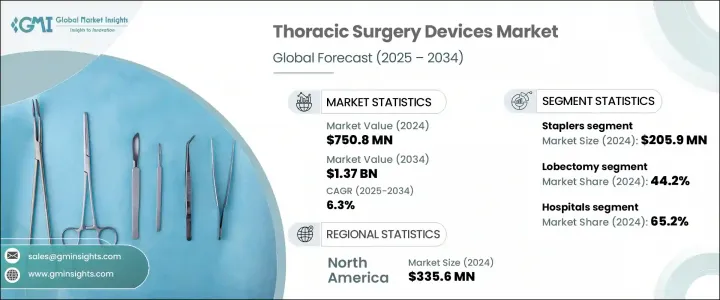

세계의 흉부외과 기기 시장은 2024년에는 7억 5,080만 달러로 평가되었고, 2034년에는 13억 7,000만 달러에 이를 것으로 예측되며 CAGR 6.3%로 성장할 전망입니다.

이 시장의 성장세는 만성 폐쇄성 폐 질환(COPD), 폐암 및 기타 외과적 개입이 필요한 질병과 같은 흉부 질환의 발병률 증가에 의해 촉진되고 있습니다. 고령화 인구 증가, 환경 오염 물질에 대한 노출, 지속적인 흡연 습관 등이 이러한 질환의 유병률 증가에 기여하고 있습니다. 이러한 사례의 급증은 더 나은 결과를 제공할 수 있는 첨단 흉부 수술 장치에 대한 수요를 직접적으로 증가시키고 있습니다. 비디오 보조 및 로봇 보조 흉부 수술과 같은 최소 침습적 시술은 회복 시간 단축, 수술 후 불편함 최소화, 합병증 위험 감소와 같은 이점으로 인해 널리 보급되고 있습니다.

이러한 첨단 수술 기법은 환자의 회복을 개선할 뿐 아니라 입원 기간을 크게 단축하여 외래 환자 환경에서 더 다양한 시술을 수행할 수 있게 합니다. 이러한 변화로 인해 외래 수술 센터(ASC)가 급속히 성장하고 있으며, 이제 ASC는 기존의 입원 치료에 비해 효율적이고 비용 효율적이며 환자 친화적인 대안으로 인식되고 있습니다. ASC는 환자 처리 속도를 높이고, 간접비를 절감하며, 일정 조정 유연성을 개선하여 의료 서비스 제공자와 환자 모두에게 점점 더 매력적인 옵션이 되고 있습니다. 최소 침습 기술이 더욱 정교해지고 장비가 더 소형화되고 전문화됨에 따라 ASC는 예전에는 고도 의료 시설에서만 가능했던 복잡한 흉부 수술을 처리할 수 있는 역량을 확대하고 있으며, 이러한 시설에 맞춤화된 첨단 수술 기기에 대한 시장 수요를 더욱 가속화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 7억 5,080만 달러 |

| 예측 금액 | 13억 7,000만 달러 |

| CAGR | 6.3% |

2024년에는 스테이플러 부문이 2억 590만 달러를 창출하며 가장 큰 비중을 차지할 것으로 보입니다. 전동식, 디지털식, 관절식 스테이플러와 같은 지속적인 디자인 혁신은 정밀도를 높이고 조직 누출과 같은 합병증을 줄이며 수술 효율성을 높이고 있습니다. 이러한 고급 기능은 조직 처리를 개선하고 수술 시간을 단축하는 동시에 외과의가 복잡한 흉부 해부학을 보다 자신감 있고 안전하게 관리할 수 있도록 지원합니다.

폐엽 절제술 부문은 2024년에 44.2%로 가장 큰 점유율을 차지했습니다. 이 기술은 폐암 진단의 상당 부분을 차지하는 초기 비소세포 폐암에 대한 선호되는 치료법으로 남아 있습니다. 선별 검사 기술과 진단 방법이 개선됨에 따라, 특히 고령자 및 고위험군 환자들이 더 일찍 발견되어 수술 치료의 대상이 되고 있습니다. 수술이 가능한 사례의 증가로 인해 혈관 실링 장치, 절개 장치, 고성능 스테이플러 등 폐엽 절제술에 사용되는 특수 기기의 수요가 촉진되고 있습니다.

미국의 흉부외과용 디바이스 2024년 시장 규모는 3억 280만 달러로 평가되었습니다. 이 국가에서는 폐암과 만성 폐쇄성 폐질환(COPD)의 발생률이 높으며, 이 질환들은 진행 단계에서 수술적 개입이 자주 필요합니다. 수백만 명이 이 질환으로 고통받고 있는 미국에서 의료진은 병원 및 암 센터에서 흉부 수술을 지속적으로 수행하고 있습니다. 수술적 치료에 대한 지속적인 수요는 전국의 의료 기관에서 흉부 기기 수요가 강하게 유지되도록 합니다.

이 시장을 형성하는 주요 업체로는 GE Healthcare, Biolitec, Medela, Fujifilm Holdings, Olympus, MicroPort, Cook Medical, ConMed, B. Braun, Intuitive Surgical, Medtronic, Cardinal Health, Boston Scientific, Karl Storz 및 Johnson & Johnson이 있습니다. 흉부외과 기기 시장에서 입지를 공고히 하기 위해 주요 기업들은 혁신을 촉진하는 전략에 집중하고 있습니다. 여기에는 인체 공학, 정밀도 및 실시간 피드백이 개선된 차세대 수술 기기의 출시가 포함됩니다. 많은 업체들이 전략적 파트너십과 지역 유통 계약을 통해 전 세계로 사업을 확장하고 있습니다. 다른 업체들은 최소 침습 및 로봇 보조 시술과 호환되는 기기를 개발하기 위해 연구 개발에 투자하고 있습니다. 특정 수술 용도에 맞는 맞춤형 솔루션을 제공하고 외래 환자 환경에 대한 비용 효율성을 최적화하는 것도 최우선 과제입니다. 또한, 기업들은 수술의 정확성과 수술 후 결과를 개선하기 위해 디지털 기술을 기기에 통합하여 더 다양한 의료 서비스 제공자를 유치하기 위해 노력하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 폐암 및 만성 호흡기 질환의 유병률 증가

- 최소 침습적 기술의 채택 증가

- 흉부외과 기기의 기술적 진보

- 외래수술센터(ASC)의 확대

- 업계의 잠재적 위험 및 과제

- 첨단 흉부외과용 기기 및 로봇 시스템의 높은 비용

- 숙련된 흉부외과 의사의 부족 및 전문 교육의 부족

- 시장 기회

- 신흥 경제국의 의료 투자 증가

- 수술 계획 및 기기에 AI 및 디지털 플랫폼의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 장래 시장 동향

- 특허 분석

- 가격 분석

- 제품별

- 지역별

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품별(2011-2034년)

- 주요 동향

- 클램프

- 집게

- 글래스퍼

- 스테이플러

- 가위

- 스프레더

- 바늘 홀더

- 기타 제품

제6장 시장 추계 및 예측 : 수술유형별(2011-2034년)

- 주요 동향

- 폐엽 절제술

- 쐐기 절제술

- 폐 절제술

- 기타 수술의 유형

제7장 시장 추계 및 예측 : 최종 용도별(2011-2034년)

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 기타 용도

제8장 시장 추계 및 예측 : 지역별(2011-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- B. Braun

- Biolitec

- Boston Scientific

- Cardinal Health

- ConMed

- Cook Medical

- Fujifilm Holdings

- GE Healthcare

- Intuitive Surgical

- Johnson &Johnson

- Karl Storz

- Medela

- Medtronic

- MicroPort

- Olympus

The Global Thoracic Surgery Devices Market was valued at USD 750.8 million in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 1.37 billion by 2034. The market's momentum is being fueled by the rising incidence of thoracic conditions such as chronic obstructive pulmonary disease (COPD), lung cancer, and other diseases requiring surgical intervention. A growing aging population, exposure to environmental pollutants, and persistent smoking habits are contributing to the increased prevalence of these conditions. This surge in cases is directly raising the demand for advanced thoracic surgical instruments that can deliver better outcomes. Minimally invasive procedures such as video-assisted and robot-assisted thoracic surgeries are gaining ground due to benefits like reduced recovery time, minimized postoperative discomfort, and lower risks of complications.

These advanced surgical approaches have not only improved patient recovery but also significantly reduced hospitalization time, enabling a broader range of procedures to be performed in outpatient environments. This shift has spurred the rapid growth of ambulatory surgical centers (ASCs), which are now seen as efficient, cost-effective, and patient-friendly alternatives to conventional inpatient hospital care. ASCs allow for quicker patient turnaround, lower overhead costs, and improved scheduling flexibility, making them an increasingly attractive option for both healthcare providers and patients. As minimally invasive techniques become more refined and equipment more compact and specialized, ASCs are expanding their capabilities to handle complex thoracic surgeries that were once only possible in high-acuity hospital settings, further accelerating market demand for advanced surgical devices tailored to these facilities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $750.8 Million |

| Forecast Value | $1.37 Billion |

| CAGR | 6.3% |

In 2024, the staplers segment emerged as the top contributor, generating USD 205.9 million. Ongoing innovations in design, such as powered, digital, and articulating staplers, are enhancing precision, reducing complications like tissue leaks, and increasing surgical efficiency. These advanced features improve tissue handling and reduce operative time while assisting surgeons in managing complex thoracic anatomy with greater confidence and safety.

The lobectomy procedures segment held the largest share at 44.2% in 2024. This technique remains the preferred treatment for early-stage non-small cell lung cancer, which accounts for a significant majority of lung cancer diagnoses. As screening technologies and diagnostic methods improve, more patients, particularly older individuals and those with higher risk factors-are being identified earlier and becoming candidates for surgical treatment. This rise in operable cases is driving demand for specialized tools used in lobectomies, including vessel sealing instruments, dissection devices, and high-performance staplers.

United States Thoracic Surgery Devices Market was valued at USD 302.8 million in 2024. The country continues to see high rates of lung cancer and COPD, both of which frequently require surgical intervention during advanced stages. With millions affected by these conditions, healthcare providers in the U.S. are steadily performing thoracic surgeries in hospitals and cancer center settings. The consistent demand for surgical treatment ensures that the need for thoracic devices remains strong across healthcare institutions nationwide.

Key players shaping this market include GE Healthcare, Biolitec, Medela, Fujifilm Holdings, Olympus, MicroPort, Cook Medical, ConMed, B. Braun, Intuitive Surgical, Medtronic, Cardinal Health, Boston Scientific, Karl Storz, and Johnson & Johnson. To solidify their position in the thoracic surgery devices market, leading companies are focusing on innovation-driven strategies. These include launching next-generation surgical tools with enhanced ergonomics, precision, and real-time feedback. Many players are expanding their global footprint through strategic partnerships and regional distribution agreements. Others are investing in R&D to create devices compatible with minimally invasive and robotic-assisted procedures. Offering customized solutions for specific surgical applications and optimizing cost-effectiveness for outpatient settings are also top priorities. Additionally, companies are integrating digital technology into devices to improve surgical accuracy and postoperative outcomes, helping them attract a broader range of healthcare providers.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Surgery type

- 2.2.4 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of lung cancer and chronic respiratory diseases

- 3.2.1.2 Growing adoption of minimally invasive techniques

- 3.2.1.3 Technological advancements in thoracic surgical instruments

- 3.2.1.4 Expansion of ambulatory surgical centers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced thoracic surgical devices and robotic systems

- 3.2.2.2 Shortage of skilled thoracic surgeons and specialized training

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing healthcare investments in emerging economies

- 3.2.3.2 Integration of AI and digital platforms in surgical planning and instrumentation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Patent analysis

- 3.8 Pricing analysis

- 3.8.1 By product

- 3.8.2 By region

- 3.9 Gap analysis

- 3.10 Porter’s analysis

- 3.11 PESTLE analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Clamps

- 5.3 Forceps

- 5.4 Graspers

- 5.5 Staplers

- 5.6 Scissors

- 5.7 Spreaders

- 5.8 Needle holders

- 5.9 Other products

Chapter 6 Market Estimates and Forecast, By Surgery Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Lobectomy

- 6.3 Wedge resection

- 6.4 Pneumonectomy

- 6.5 Other surgery types

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profile

- 9.1 B. Braun

- 9.2 Biolitec

- 9.3 Boston Scientific

- 9.4 Cardinal Health

- 9.5 ConMed

- 9.6 Cook Medical

- 9.7 Fujifilm Holdings

- 9.8 GE Healthcare

- 9.9 Intuitive Surgical

- 9.10 Johnson & Johnson

- 9.11 Karl Storz

- 9.12 Medela

- 9.13 Medtronic

- 9.14 MicroPort

- 9.15 Olympus