|

시장보고서

상품코드

1782097

고무-금속 결합 물품 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Rubber-To-Metal Bonded Articles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

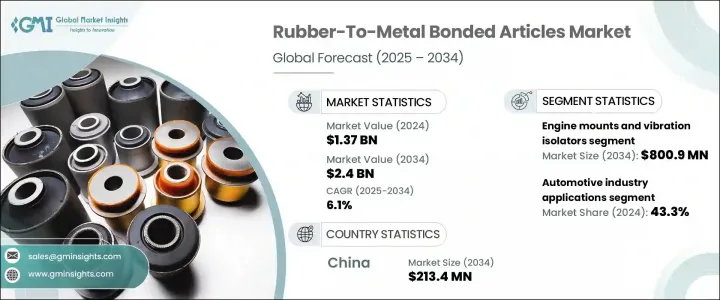

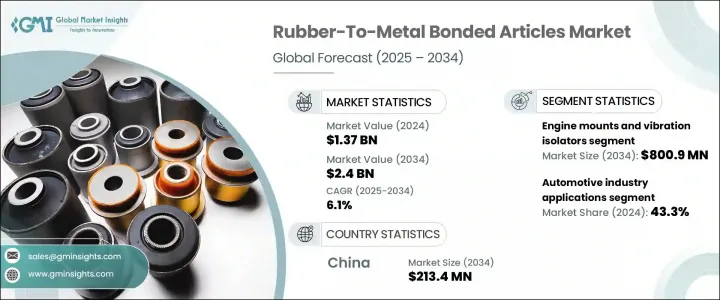

세계의 고무-금속 결합 물품 시장 규모는 2024년에 13억 7,000만 달러로 평가되었고, CAGR 6.1%를 나타내 2034년에는 24억 달러에 이를 것으로 예측됩니다.

이러한 강력한 기세는 산업기계, 항공우주, 자동차 등 다양한 최종 이용 산업에서 수요가 증가하고 있기 때문에 이러한 부품은 소음을 최소화하고 충격을 흡수하며 진동을 완화하는 데 필수적입니다. 자동차 산업은 연비 효율과 배기 가스 규정 준수를 지원하는 고성능, 경량 부품에 대한 선호도가 높아짐에 따라 수요를 견인하는 지배적인 힘이 되고 있습니다.

특히 배출가스와 자동차의 안전성에 관한 규제가 강화됨에 따라 제조업체는 진화하는 표준에 대응하기 위해 고급 접합 솔루션에 기울고 있습니다. 항공우주 산업은 또한 중요한 구조 및 기능 분야에서 이러한 접합 부품의 사용을 확대하고 있습니다. 게다가 건설, 헬스케어, 일렉트로닉스등의 분야에서도 새로운 응용의 길이 태어나고 있어, 다양한 성장 패턴을 나타내고 있습니다. 접착 기술, 특히 시아노아크릴레이트계 접착제의 기술 혁신은 이미 시장의 40% 이상을 차지하고 있어 더욱 추풍이 되고 있습니다. 그러나 원재료와 에너지 가격 상승은 특히 소규모 시장 기업들에게 어려움을 겪고 있습니다. 대기업이 공급망의 수직 통합 및 안정화를 목표로 하는 동안 통합의 움직임이 가속될 수 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 13억 7,000만 달러 |

| 예측 금액 | 24억 달러 |

| CAGR | 6.1% |

엔진 마운트 및 방진장치 분야는 2024년에 4억 4,030만 달러를 창출했고, 2034년에는 8억 90만 달러로 성장할 것으로 예측되며 CAGR 6.2%를 나타낼 전망입니다. 이러한 부품은 구조적 안정성 유지 및 엔진과 관련된 진동 최소화가 필수적인 자동차 및 산업기계 응용 분야에서 중요한 역할을 합니다. 경량화와 NVH(소음·진동·하슈네스) 특성의 개선이 우선되는 전기차와 하이브리드차에서는 그 중요성이 높아집니다.

2024년에는 서스펜션 부시, 방진 시스템, 배기 브래킷 등의 결합 부품이 널리 사용되어 자동차 분야가 43.3%를 나타내 최대 시장 점유율을 차지했습니다. 인도, 독일, 중국, 미국 등 지역에서 시장 확대로 고성능, 내구성 있는 부품에 대한 수요가 증가하고 있습니다. 개발 중인 자동차 기술이 제품 요구사항을 재구성하고 있으며, 제조업체는 최신 안전 및 배출 가스 기준을 충족하는 보다 통합된 효율적인 부품을 개발할 필요가 있습니다.

2024년 중국의 고무-금속 결합 물품 시장 규모는 1억1,430만 달러로 평가되었고, CAGR 6.5%를 나타내 2034년에는 2억1,340만 달러에 달할 것으로 예측됩니다. 수입 침체에도 불구하고 이 지역은 여전히 세계 최대의 소비지이며 현지 수요는 계속 증가하고 있습니다. 유리한 무역 정책과 인프라 투자는 국내 생산으로의 전환을 촉진하고 중국이 이 산업에서 자립에 접근할 수 있도록 합니다. 한편 미국은 동기간에 큰 시장 성장을 이루었습니다.

고무-금속 결합 물품 시장의 주요 기업으로는 Continental AG, Hutchinson SA, Trelleborg AB, Sumitomo Institute, Vibracoustic GmbH 등이 있습니다. 고무-금속 결합 물품 시장에서의 지위를 강화하기 위해, 최고 기업은 몇 가지 핵심 전략에 주력하고 있습니다. 각 회사는 전기자동차와 하이브리드 자동차 플랫폼의 진화하는 요구에 부응하는 고도의 경량 접합 솔루션을 만들기 위해 연구 개발에 많은 투자를 하고 있습니다. 전략적 M&A는 공급망을 더 잘 제어하고 시장 점유율을 확대하기 위해 진행되고 있습니다. 주요 기업은 또한 생산 능력을 강화하고 자동화를 활용하여 효율성을 향상시키고 있습니다. 또한 안정적인 수요를 확보하고 세계의 존재를 강화하기 위해 많은 기업들이 OEM과 장기 계약을 맺고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 유형별

- 향후 시장 동향

- 기술과 혁신의 상황

- 현재 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(주 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적인 노력

- 탄소발자국의 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계·예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 엔진 마운트 및 제진기

- 자동차 엔진 마운트

- 승용차 엔진 마운트

- 상용차 엔진 마운트

- 전기자동차 전용 마운트

- 산업용 제진기

- 기계 마운트 및 아이솔레이터

- HVAC 시스템 아이솔레이터

- 펌프 및 컴프레서 마운트

- 항공우주 엔진 마운트

- 항공기 엔진 마운트

- 헬리콥터 진동 시스템

- UAV 및 드론 애플리케이션

- 자동차 엔진 마운트

- 부싱 및 서스펜션 부품

- 자동차 부싱

- 컨트롤 암 부싱

- 스웨이 바 부싱

- 스트럿 마운트 부싱

- 리프 스프링 부싱

- 산업용 부싱

- 기계 부싱

- 컨베이어 시스템 구성품

- 중장비 부싱

- 해양 및 오프로드 부싱

- 해양 엔진 마운트

- 건설 장비 부싱

- 농업 기계 부품

- 자동차 부싱

- 씰 및 개스킷

- 자동차 씰

- 엔진 씰 및 개스킷

- 트랜스미션 씰

- 차동 씰

- 항공우주 씰

- 항공기 엔진 씰

- 유압 시스템 씰

- 환경 제어 시스템 씰

- 산업용 씰

- 펌프 및 밸브 씰

- 파이프라인 씰

- 공정 장비 씰

- 자동차 씰

- 커플링 및 플렉서블 커넥터

- 자동차 드라이브 커플링

- CV 조인트 부츠

- 드라이브 샤프트 커플링

- 트랜스미션 커플링

- 산업용 플렉서블 커플링

- 모터 커플링

- 펌프 커플링

- 발전기 커플링

- 해양 및 항공우주용 커플링

- 프로펠러 샤프트 커플링

- 항공기 시스템 커플링

- 특수 결합 부품

- 자동차 드라이브 커플링

- 진동 방지 패드 및 마운트

- 쇼크 업소버 및 댐퍼

- 유연한 조인트 및 커넥터

- 맞춤형 엔지니어링 솔루션

제6장 시장 추계·예측 : 본딩 기술별(2021-2034년)

- 주요 동향

- 화학적 결합 기술

- 접착제 기반 접착 시스템

- 에폭시 접착제

- 폴리우레탄 접착제

- 실리콘 기반 시스템

- 특수 화학 접착제

- 가황 본딩

- 유황 가황 시스템

- 과산화물 가황

- 방사선 가황

- 금속 산화물 가황

- 프라이머 및 코팅 시스템

- 금속 표면 프라이머

- 고무 호환 코팅

- 다층 본딩 시스템

- 접착제 기반 접착 시스템

- 기계적 본딩 기술

- 오버몰딩 공정

- 인서트 몰딩

- 투샷 성형 시스템

- 다중 재료 성형

- 캡슐화 기술

- 완전한 캡슐화 시스템

- 부분 캡슐화 방법

- 선택적 본딩 영역

- 기계적 연동

- 텍스처 표면 본딩

- 기계적 체결 시스템

- 하이브리드 본딩 접근 방식

- 오버몰딩 공정

- 첨단 접착 기술

- 플라즈마 처리 본딩

- 대기 플라즈마 시스템

- 저압 플라즈마 처리

- 코로나 치료

- 레이저 보조 본딩

- 레이저 표면 활성화

- 레이저 용접

- 선택적 레이저 가공

- 나노기술 강화 본딩

- 나노입자 강화 접착제

- 탄소 나노 튜브 응용

- 그래핀 기반 시스템

- 플라즈마 처리 본딩

- 새로운 접착 기술

- 자가 치유 본딩 시스템

- 스마트 접착 기술

- 바이오 기반 본딩 시스템

- 재활용 가능한 본딩 솔루션

제7장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 자동차 산업 용도

- 승용차

- 엔진 및 파워트레인 구성 요소

- 서스펜션 및 섀시 시스템

- 차체 및 인테리어

- 전기자동차 전용 구성 요소

- 상용차

- 대형 트럭

- 버스 및 코치 시스템

- 특수 차량 구성 요소

- 오토바이 및 이륜차

- 엔진 마운트 시스템

- 서스펜션 구성 요소

- 진동 제어 시스템

- 자동차 애프터마켓

- 교체 부품 시장

- 성능 업그레이드 구성 요소

- 유지 보수 및 수리

- 승용차

- 항공우주 및 방위산업

- 상업용 항공

- 엔진 마운트 시스템

- 랜딩 기어 구성 요소

- 객실 및 인테리어

- 환경 제어 시스템

- 군사 및 방위 항공기

- 전투기 구성 요소

- 운송 항공기 시스템

- 헬리콥터

- UAV 및 드론 시스템

- 우주 및 위성

- 발사체 구성품

- 위성 시스템

- 우주 정거장

- 항공우주 애프터마켓

- 유지보수, 수리 및 정비(MRO)

- 부품 교체 시장

- 업그레이드 및 현대화 프로그램

- 상업용 항공

- 산업기계 및 장비

- 제조설비

- 공작기계

- 자동화 시스템 구성 요소

- 로봇 공학

- 공정산업

- 화학처리장비

- 석유 및 가스 산업

- 발전 시스템

- 건설 및 광업 장비

- 중장비 부품

- 토목기계

- 광업 기계

- 해양

- 선박 엔진 마운트

- 해외 플랫폼 구성 요소

- 해양 추진 시스템

- 제조설비

- 인프라 및 건설

- 건축 및 건설

- HVAC 시스템 구성 요소

- 엘리베이터 및 에스컬레이터 시스템

- 구조 진동 제어

- 교통 인프라

- 철도 시스템 구성 요소

- 교량 및 터널

- 공항 인프라

- 유틸리티 및 에너지

- 발전소 구성 요소

- 재생에너지 시스템

- 전송 및 분배

- 건축 및 건설

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- 3M Company

- BASF SE

- Bridgestone Corporation

- Continental AG

- Cooper Standard

- ElringKlinger AG

- Freudenberg Group

- HB Fuller Company

- Henkel AG &Co. KGaA

- Hutchinson SA

- Parker Hannifin Corporation

- Sumitomo Riko Company Limited

- Trelleborg AB

- Vibracoustic

- ZF Friedrichshafen AG

The Global Rubber-To-Metal Bonded Articles Market was valued at USD 1.37 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 2.4 billion by 2034. This strong momentum is attributed to the growing demand across a range of end-use industries, including industrial machinery, aerospace, and automotive, where these components are essential in minimizing noise, absorbing shocks, and dampening vibrations. The automotive sector continues to be a dominant force in driving demand, owing to the increasing preference for high-performance, weight-saving components that support fuel efficiency and emissions compliance.

As regulations tighten, especially around emissions and vehicle safety, manufacturers are leaning into advanced bonding solutions to meet evolving standards. The aerospace industry is also expanding its use of these bonded parts in critical structural and functional areas. Additionally, sectors such as construction, healthcare, and electronics are creating new pathways for application, signaling a diversified growth pattern. Innovations in bonding technologies, especially with cyanoacrylate adhesives-which already command over 40% of the market-are providing a further lift. However, rising raw material and energy prices pose challenges, particularly for smaller market players. This may accelerate consolidation efforts, as larger firms look to integrate and stabilize their supply chains vertically.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.37 Billion |

| Forecast Value | $2.4 Billion |

| CAGR | 6.1% |

The engine mounts and vibration isolators segment generated USD 440.3 million in 2024 and is projected to grow to USD 800.9 million by 2034, growing at a CAGR of 6.2%. These components are critical across automotive and industrial machinery applications, where maintaining structural stability and minimizing engine-related vibrations are essential. Their relevance is heightened in both electric and hybrid models, where manufacturers prioritize reduced weight and improved NVH (Noise, Vibration, and Harshness) characteristics.

In 2024, the automotive segment held the largest market share at 43.3%, owing to the extensive usage of bonded components like suspension bushings, anti-vibration systems, and exhaust brackets. Market expansion in regions such as India, Germany, China, and the United States has led to increased demand for high-performance, durable components. Emerging vehicle technologies are reshaping product requirements, pushing manufacturers to develop more integrated, efficient parts that align with updated safety and emissions standards.

China Rubber-To-Metal Bonded Articles Market generated USD 114.3 million in 2024 and is forecasted to grow at a CAGR of 6.5%, to reach USD 213.4 million by 2034. Despite a dip in imports, the region remains the largest global consumer, with local demand continuing to rise. Favorable trade policies and infrastructure investment are driving a shift toward domestic production, allowing China to move closer to self-reliance in this industry. Meanwhile, the United States experienced significant market growth during the same period.

Leading players in the Rubber-To-Metal Bonded Articles Market include Continental AG, Hutchinson SA, Trelleborg AB, Sumitomo Riko Co., Ltd., and Vibracoustic GmbH. To strengthen their position in the rubber-to-metal bonded articles market, top companies are focusing on several core strategies. They are heavily investing in research and development to create advanced, lightweight bonding solutions that cater to the evolving needs of electric and hybrid vehicle platforms. Strategic mergers and acquisitions are being pursued to gain better control of supply chains and expand market share. Key players are also enhancing their manufacturing capabilities and leveraging automation to improve efficiency. Furthermore, many are entering long-term contracts with OEMs to ensure consistent demand and strengthen their global presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics( Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.7 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million) (Tons)

- 5.1 Key trends

- 5.2 Engine mounts and vibration isolators

- 5.2.1 Automotive engine mounts

- 5.2.1.1 Passenger vehicle engine mounts

- 5.2.1.2 Commercial vehicle engine mounts

- 5.2.1.3 Electric vehicle specialized mounts

- 5.2.2 Industrial vibration isolators

- 5.2.2.1 Machinery mounts and isolators

- 5.2.2.2 Hvac system isolators

- 5.2.2.3 Pump and compressor mounts

- 5.2.3 Aerospace engine mounts

- 5.2.3.1 Aircraft engine mounts

- 5.2.3.2 Helicopter vibration systems

- 5.2.3.3 Uav and drone applications

- 5.2.1 Automotive engine mounts

- 5.3 Bushings and suspension components

- 5.3.1 Automotive bushings

- 5.3.1.1 Control arm bushings

- 5.3.1.2 Sway bar bushings

- 5.3.1.3 Strut mount bushings

- 5.3.1.4 Leaf spring bushings

- 5.3.2 Industrial bushings

- 5.3.2.1 Machinery bushings

- 5.3.2.2 Conveyor system components

- 5.3.2.3 Heavy equipment bushings

- 5.3.3 Marine and off-highway bushings

- 5.3.3.1 Marine engine mounts

- 5.3.3.2 Construction equipment bushings

- 5.3.3.3 Agricultural machinery components

- 5.3.1 Automotive bushings

- 5.4 Seals and gaskets

- 5.4.1 Automotive seals

- 5.4.1.1 Engine seals and gaskets

- 5.4.1.2 Transmission seals

- 5.4.1.3 Differential seals

- 5.4.2 Aerospace seals

- 5.4.2.1 Aircraft engine seals

- 5.4.2.2 Hydraulic system seals

- 5.4.2.3 Environmental control system seals

- 5.4.3 Industrial seals

- 5.4.3.1 Pump and valve seals

- 5.4.3.2 Pipeline seals

- 5.4.3.3 Process equipment seals

- 5.4.1 Automotive seals

- 5.5 Couplings and flexible connectors

- 5.5.1 Automotive drive couplings

- 5.5.1.1 Cv joint boots

- 5.5.1.2 Driveshaft couplings

- 5.5.1.3 Transmission couplings

- 5.5.2 Industrial flexible couplings

- 5.5.2.1 Motor couplings

- 5.5.2.2 Pump couplings

- 5.5.2.3 Generator couplings

- 5.5.3 Marine and aerospace couplings

- 5.5.3.1 Propeller shaft couplings

- 5.5.3.2 Aircraft system couplings

- 5.5.3.3 Specialty bonded components

- 5.5.1 Automotive drive couplings

- 5.6 Anti-vibration pads and mounts

- 5.6.1 Shock absorbers and dampers

- 5.6.2 Flexible joints and connectors

- 5.6.3 Custom engineered solutions

Chapter 6 Market Estimates and Forecast, By Bonding Technology, 2021 - 2034 (USD Million) (Tons)

- 6.1 Key trends

- 6.2 Chemical bonding technologies

- 6.2.1 Adhesive-based bonding systems

- 6.2.1.1 Epoxy-based adhesives

- 6.2.1.2 Polyurethane adhesives

- 6.2.1.3 Silicone-based systems

- 6.2.1.4 Specialty chemical adhesives

- 6.2.2 Vulcanization bonding

- 6.2.2.1 Sulfur vulcanization systems

- 6.2.2.2 Peroxide vulcanization

- 6.2.2.3 Radiation vulcanization

- 6.2.2.4 Metal oxide vulcanization

- 6.2.3 Primer and coating systems

- 6.2.3.1 Metal surface primers

- 6.2.3.2 Rubber-compatible coatings

- 6.2.3.3 Multi-layer bonding systems

- 6.2.1 Adhesive-based bonding systems

- 6.3 Mechanical bonding technologies

- 6.3.1 Overmolding processes

- 6.3.1.1 Insert molding applications

- 6.3.1.2 Two-shot molding systems

- 6.3.1.3 Multi-material molding

- 6.3.2 Encapsulation technologies

- 6.3.2.1 Complete encapsulation systems

- 6.3.2.2 Partial encapsulation methods

- 6.3.2.3 Selective bonding areas

- 6.3.3 Mechanical interlocking

- 6.3.3.1 Textured surface bonding

- 6.3.3.2 Mechanical fastening systems

- 6.3.3.3 Hybrid bonding approaches

- 6.3.1 Overmolding processes

- 6.4 Advanced bonding technologies

- 6.4.1 Plasma treatment bonding

- 6.4.1.1 Atmospheric plasma systems

- 6.4.1.2 Low-pressure plasma treatment

- 6.4.1.3 Corona treatment applications

- 6.4.2 Laser-assisted bonding

- 6.4.2.1 Laser surface activation

- 6.4.2.2 Laser welding applications

- 6.4.2.3 Selective laser processing

- 6.4.3 Nanotechnology-enhanced bonding

- 6.4.3.1 Nanoparticle-enhanced adhesives

- 6.4.3.2 Carbon nanotube applications

- 6.4.3.3 Graphene-based systems

- 6.4.1 Plasma treatment bonding

- 6.5 Emerging bonding technologies

- 6.5.1 Self-healing bonding systems

- 6.5.2 Smart adhesive technologies

- 6.5.3 Bio-based bonding systems

- 6.5.4 Recyclable bonding solutions

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 Automotive industry applications

- 7.2.1 Passenger vehicles

- 7.2.1.1 Engine and powertrain components

- 7.2.1.2 Suspension and chassis systems

- 7.2.1.3 Body and interior applications

- 7.2.1.4 Electric vehicle specific components

- 7.2.2 Commercial vehicles

- 7.2.2.1 Heavy-duty truck applications

- 7.2.2.2 Bus and coach systems

- 7.2.2.3 Specialty vehicle components

- 7.2.3 Motorcycle and two-wheeler applications

- 7.2.3.1 Engine mount systems

- 7.2.3.2 Suspension components

- 7.2.3.3 Vibration control systems

- 7.2.4 Automotive aftermarket

- 7.2.4.1 Replacement parts market

- 7.2.4.2 Performance upgrade components

- 7.2.4.3 Maintenance and repair applications

- 7.2.1 Passenger vehicles

- 7.3 Aerospace and defense industry

- 7.3.1 Commercial aviation

- 7.3.1.1 Engine mount systems

- 7.3.1.2 Landing gear components

- 7.3.1.3 Cabin and interior applications

- 7.3.1.4 Environmental control systems

- 7.3.2 Military and defense aircraft

- 7.3.2.1 Fighter aircraft components

- 7.3.2.2 Transport aircraft systems

- 7.3.2.3 Helicopter applications

- 7.3.2.4 Uav and drone systems

- 7.3.3 Space and satellite applications

- 7.3.3.1 Launch vehicle components

- 7.3.3.2 Satellite systems

- 7.3.3.3 Space station applications

- 7.3.4 Aerospace aftermarket

- 7.3.4.1 Maintenance, repair, and overhaul (MRO)

- 7.3.4.2 Component replacement market

- 7.3.4.3 Upgrade and modernization programs

- 7.3.1 Commercial aviation

- 7.4 Industrial machinery and equipment

- 7.4.1 Manufacturing equipment

- 7.4.1.1 Machine tool applications

- 7.4.1.2 Automation system components

- 7.4.1.3 Robotics applications

- 7.4.2 Process industries

- 7.4.2.1 Chemical processing equipment

- 7.4.2.2 Oil and gas industry applications

- 7.4.2.3 Power generation systems

- 7.4.3 Construction and mining equipment

- 7.4.3.1 Heavy machinery components

- 7.4.3.2 Earth moving equipment

- 7.4.3.3 Mining machinery applications

- 7.4.4 Marine and offshore

- 7.4.4.1 Ship engine mounts

- 7.4.4.2 Offshore platform components

- 7.4.4.3 Marine propulsion systems

- 7.4.1 Manufacturing equipment

- 7.5 Infrastructure and construction

- 7.5.1 Building and construction

- 7.5.1.1 Hvac system components

- 7.5.1.2 Elevator and escalator systems

- 7.5.1.3 Structural vibration control

- 7.5.2 Transportation infrastructure

- 7.5.2.1 Railway system components

- 7.5.2.2 Bridge and tunnel applications

- 7.5.2.3 Airport infrastructure

- 7.5.3 Utilities and energy

- 7.5.3.1 Power plant components

- 7.5.3.2 Renewable energy systems

- 7.5.3.3 Transmission and distribution

- 7.5.1 Building and construction

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 3M Company

- 9.2 BASF SE

- 9.3 Bridgestone Corporation

- 9.4 Continental AG

- 9.5 Cooper Standard

- 9.6 ElringKlinger AG

- 9.7 Freudenberg Group

- 9.8 H.B. Fuller Company

- 9.9 Henkel AG & Co. KGaA

- 9.10 Hutchinson SA

- 9.11 Parker Hannifin Corporation

- 9.12 Sumitomo Riko Company Limited

- 9.13 Trelleborg AB

- 9.14 Vibracoustic

- 9.15 ZF Friedrichshafen AG