|

시장보고서

상품코드

1782109

요관경 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Ureteroscope Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

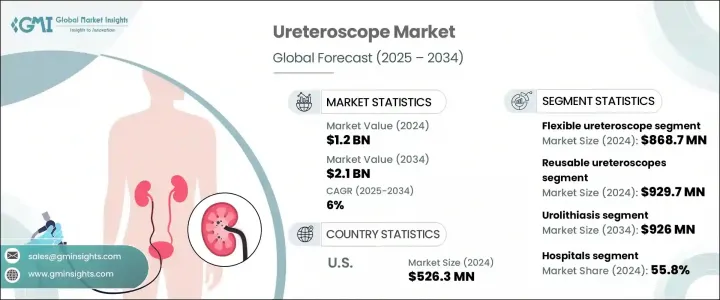

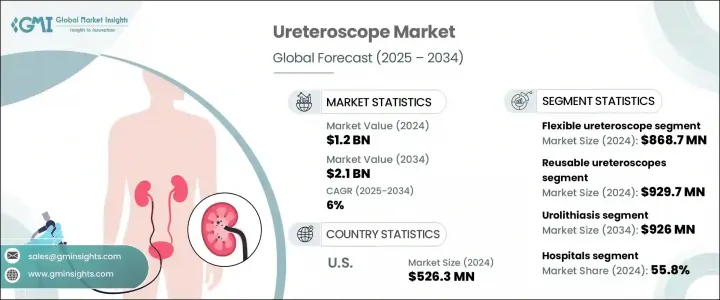

세계의 요관경 시장은 2024년에는 12억 달러로 평가되었으며 CAGR 6%를 나타내 2034년에는 21억 달러에 이를 것으로 추정됩니다.

이 성장 궤도는 주로 신장 결석 및 기타 요로 관련 질병의 세계 발생률 증가에 의해 견인됩니다. 이와 병행하여 보다 나은 임상결과, 수술후 합병증의 감소, 입원기간의 단축에 힘입어 저침습기술의 채용이라는 헬스케어 전체의 동향도 계속 가속화되고 있습니다. 이러한 이점은 건강 관리 제공업체와 환자 모두 기존 수술보다 내시경 개입을 선호합니다. 요관경은 요관이나 신장의 상태를 진단·치료하기 위한 기기이지만, 그 설계가 진화해 유연성이 향상되어, 고도의 화상 진단이 가능하게 됨으로써, 점점 중요성을 증가하고 있습니다. 이러한 기술 혁신은 환자의 쾌적성과 안전성을 향상시키면서 보다 정밀한 치료를 가능하게 하고, 세계의 헬스케어 시스템에서 채용이 확대되고 있습니다.

요로 감염과 신결석 증가는 현대 생활습관, 비만률 상승, 유전적 영향, 특정 집단에서의 수분 보충 부족 등이 복합적으로 얽혀 있기 때문이라고 생각됩니다. 이러한 건강 문제가 보편화됨에 따라 의료계는 효과적이고 침습성이 낮은 솔루션으로 요관경 검사에 주목하고 있습니다. 이 범위는 협착, 종양, 결석과 같은 광범위한 비뇨기과 문제를 해결할 수 있도록 설계되었습니다. 최첨단 시각화와 조작성을 갖추고 요로 전역의 철저한 진단과 저침습 치료를 가능하게 합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 12억 달러 |

| 예측 금액 | 21억 달러 |

| CAGR | 6% |

2024년 연성 요관경 시장 규모는 8억 6,870만 달러였습니다. 적응성이 높고 복잡한 요로를 쉽게 통과할 수 있으므로 복잡한 비뇨기과 사례의 진단 및 관리에 최적입니다. 재료 및 시각화의 기술적 진보는 이러한 장치의 성능을 더욱 향상시키고 널리 임상적으로 받아들여지는 데 이르게 되었습니다. 비뇨기과 의사가 보다 안전하고 효율적인 절차를 가능하게 하는 정밀 기기를 요구하게 되어 연성 요관경 수요가 증가하고 있습니다.

임상 응용 분야에서는 요로 결석증 분야가 2024년에 가장 높은 시장 점유율을 차지했으며, 2034년에는 9억 2,600만 달러에 이를 것으로 예측됩니다. 요로 결석증은 광범위한 층을 앓고 있으며 치료하지 않으면 심각한 합병증을 유발할 수 있습니다. 요관경의 정확성과 효율성은 특히 침습성이 낮은 수술 수단으로 결석을 제거하거나 파쇄해야 하는 경우 이 질환의 치료에 필수적인 도구입니다.

2024년 미국의 요관경 시장 규모는 견고한 헬스케어 인프라와 비뇨기 질환에 대한 높은 인식으로 5억 2,630만 달러에 달했습니다. 첨단 의료기술과 신결석과 요로의 문제를 안고 있는 환자수가 많아져 일관된 수요를 견인하고 있습니다. 게다가, 최상급 의료기기 제조업체가 존재하고 새로운 이미징 툴의 도입이 급속히 진행되고 있는 것도, 이 분야에 있어서의 이 나라의 리더십을 확고하게 하고 있습니다.

요관경 시장 경쟁 구도에 기여하는 주요 기업은 Boston Scientific, STORZ, Ambu, PUSEN, Coloplast, BD, Stryker, Dornier MedTech, Neoscope, OLYMPUS, OPCOM Medical, RICHARD WOLF 등입니다. 시장 포지션을 강화하기 위해 요관경 업계의 각 회사는 장비 유연성, 소형화 및 광학 투명성 향상에 중점을 두고 기술 혁신에 많은 투자를 하고 있습니다. 선진국 시장과 신흥국 시장 모두 수요에 대응하기 위해 전략적 파트너십과 제품 출시를 통해 제품 포트폴리오를 적극적으로 확대하고 있습니다. 일회용 및 디지털 요관경 기술의 지속적인 개선은 또한 중요한 중점 분야입니다. 또한 각 회사는 세계 유통망을 강화하고 임상 도입을 지원하기 위한 교육 프로그램을 추진하고 있으며, 이를 통해 장기적인 경쟁력과 지속적인 시장 성장을 보장하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 신장 결석 및 요로 질환의 이환율 증가

- 요관경 검사에 있어서의 기술적 진보

- 저침습 디바이스의 채용 확대

- 업계의 잠재적 위험 및 과제

- 고급 디지털 요관경의 고비용

- 기회

- 신흥 시장 진출

- 요관경과 로봇 수술 시스템의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 기술과 혁신의 상황

- 현재 기술 동향

- 신흥기술

- 제품별 가격 동향

- 향후 시장 동향

- 상환 시나리오

- 소비자 행동 분석

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계·예측 : 제품별(2021-2034년)

- 주요 동향

- 연성 요관경

- 경성 요관경

제6장 시장 추계·예측 : 사용성별(2021-2034년)

- 주요 동향

- 재사용 가능한 요관경

- 일회용 요관경

제7장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 요로 결석증

- 요도 협착

- 요로 감염

- 기타 용도

제8장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 기타 최종 용도

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Ambu

- BD

- Boston Scientific

- Coloplast

- Dornier MedTech

- neoscope

- OLYMPUS

- OPCOM Medical

- PUSEN

- RICHARD WOLF

- STORZ

- Stryker

The Global Ureteroscope Market was valued at USD 1.2 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 2.1 billion by 2034. This growth trajectory is primarily being driven by the rising global incidence of kidney stones and other urinary tract-related conditions. Alongside this, the broader healthcare trend of adopting minimally invasive technologies continues to gain pace, fueled by better clinical outcomes, reduced post-operative complications, and shorter hospital stays. These advantages are pushing both healthcare providers and patients to prefer endoscopic interventions over traditional surgery. Ureteroscopes-devices designed to diagnose and treat ureteral and renal conditions-have become increasingly important as their designs evolve to offer improved flexibility and advanced imaging. These innovations allow for more precise treatments with greater patient comfort and enhanced safety, supporting their growing adoption across healthcare systems worldwide.

The increase in urinary tract infections and renal calculi can be attributed to a mix of modern lifestyle habits, rising obesity rates, genetic influences, and poor hydration in certain populations. As these health issues become more common, the medical community is turning to ureteroscopy as an effective and less invasive solution. These scopes are engineered to address a wide range of urological concerns such as strictures, tumors, and calculi. Equipped with cutting-edge visualization and maneuverability, they enable thorough diagnosis and minimally invasive treatment across the urinary tract.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.2 Billion |

| Forecast Value | $2.1 Billion |

| CAGR | 6% |

The flexible ureteroscopes segment was valued at USD 868.7 million in 2024. Their adaptability and ease of navigation through the intricate urinary pathways make them ideal for diagnosing and managing complex urological cases. Technological advancements in materials and visualization further enhance the performance of these devices, leading to widespread clinical acceptance. The demand for flexible ureteroscopes is increasing as urologists seek precision instruments that allow for safer and more efficient procedures.

In terms of clinical application, the urolithiasis segment commanded the highest market share in 2024 and is expected to reach USD 926 million by 2034. Urolithiasis affects a broad demographic and can result in serious complications if untreated. The precision and efficiency of ureteroscopes make them essential tools in treating this condition, particularly when stone removal or fragmentation is required through less invasive surgical means.

U.S. Ureteroscope Market was valued at USD 526.3 million in 2024 due to its strong healthcare infrastructure and high awareness of urological disorders. Advanced medical technology, combined with a significant patient population dealing with kidney stones and urinary tract issues, drives consistent demand. Additionally, the presence of top-tier medical device manufacturers and the rapid adoption of newer imaging tools solidify the country's leadership in this space.

Key players contributing to the competitive landscape of the Ureteroscope Market include Boston Scientific, STORZ, Ambu, PUSEN, Coloplast, BD, Stryker, Dornier MedTech, Neoscope, OLYMPUS, OPCOM Medical, and RICHARD WOLF. To strengthen their market position, companies in the ureteroscope industry are investing heavily in innovation, focusing on enhancing device flexibility, miniaturization, and optical clarity. They are actively expanding their product portfolios through strategic partnerships and product launches tailored to meet the demands of both developed and emerging healthcare markets. Continuous improvement in disposable and digital ureteroscope technology is also a key focus area. Additionally, players are ramping up their global distribution networks and engaging in training programs to support clinical adoption, thereby ensuring long-term competitiveness and sustained market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Usability

- 2.2.4 Application

- 2.2.5 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of kidney stones and urinary tract diseases

- 3.2.1.2 Technological advancements in ureteroscopy

- 3.2.1.3 Growing adoption of minimally invasive devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced and digital ureteroscopes

- 3.2.3 Opportunities

- 3.2.3.1 Expansion into emerging markets

- 3.2.3.2 Integration of ureteroscopes with robotic surgical systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends, by product

- 3.7 Future market trends

- 3.8 Reimbursement scenario

- 3.9 Consumer behaviour analysis

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Flexible ureteroscope

- 5.3 Rigid ureteroscope

Chapter 6 Market Estimates and Forecast, By Usability, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Reusable ureteroscopes

- 6.3 Disposable ureteroscopes

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Urolithiasis

- 7.3 Urethral stricture

- 7.4 Urinary tract infections

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Ambu

- 10.2 BD

- 10.3 Boston Scientific

- 10.4 Coloplast

- 10.5 Dornier MedTech

- 10.6 neoscope

- 10.7 OLYMPUS

- 10.8 OPCOM Medical

- 10.9 PUSEN

- 10.10 RICHARD WOLF

- 10.11 STORZ

- 10.12 Stryker