|

시장보고서

상품코드

1782152

백신 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Vaccines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

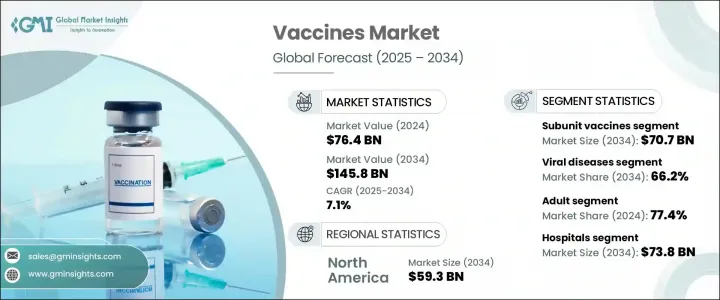

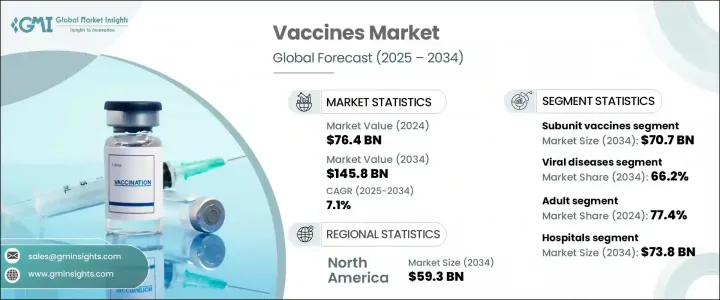

세계의 백신 시장은 2024년에 764억 달러로 평가되었으며 CAGR 7.1%를 나타내 2034년에는 1,458억 달러에 이를 것으로 추정됩니다.

이 성장은 간염, 계절성 인플루엔자, 신형 바이러스 균주와 같은 감염의 지속적인 출현으로 크게 뒷받침됩니다. 이러한 질병은 공중 보건에 대한 끊임없는 위협이기 때문에 정부와 의료 기관은 감염률을 낮추기 위해 예방 접종 노력을 강화하고 있습니다. 지원 공공 이니셔티브, 개발 도상 지역에서 건강 관리 예산 증가, 백신 연구 개발의 진보는 확장을위한 유리한 환경을 계속 형성하고 있습니다. 또한 한 번의 접종으로 여러 질병에 대한 면역력을 얻을 수 있는 혼합 백신의 세계 증가는 기술 혁신을 가속화하고 예방접종 프로토콜을 단순화합니다.

암, 만성 감염, 자가면역 질환 등의 복잡한 병태를 표적으로 한 차세대 백신의 개발은 시장의 치료 범위를 확대하고 있습니다. 특히 선진국에서는 고령화가 진행되고 있어 감염증에 걸리기 쉬운 상황이 계속되고 있기 때문에 세계의 백신 수요가 더욱 높아지고 있습니다. 민간기업과 공중위생기관과의 강력한 협력관계와 mRNA나 재조합 단백질 플랫폼 등의 진화하는 기술도 함께 백신의 유효성, 전달, 이용 용이성이 향상되고 있습니다. 이러한 요인들이 결합되어 장기적인 시장 기세가 커지고 있습니다.

| 시장 규모 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 764억 달러 |

| 예측 금액 | 1,458억 달러 |

| CAGR | 7.1% |

2024년 서브유닛 백신 부문은 376억 달러로 평가되었고 CAGR 6.9%를 나타내 2034년에는 707억 달러에 이를 것으로 추정됩니다. 이들 백신에는 재조합형, 다당류형, 컨쥬게이트형이 있으며, 각각 병원체 전체를 사용하지 않고 면역원성을 높이는데 기여하고 있습니다. 질병을 일으키는 유기체로부터 특정 단백질을 표적화하는 이러한 능력은 안전성 프로파일을 향상시키고 원치 않는 면역 반응을 감소시킵니다. T 세포 의존적 면역 활성화는 더 강력한 기억 반응을 촉진하고 장기간 방어가 가능하며 유아와 같은 취약한 집단에 적합하기 때문에 이 분야는 계속 견인 역할을 하고 있습니다.

바이러스성 질환 분야는 2024년에 66.2%의 점유율을 차지했으며, 2034년까지 강력한 성장을 유지할 것으로 예측됩니다. 이 범주에는 간염, 인플루엔자, HPV, 로타바이러스, 대상포진, MMR, COVID-19 및 기타 바이러스에 대한 백신이 포함됩니다. 인식과 예방 노력이 확대됨에 따라 예방접종 프로그램은 전 세계적으로 규모를 확대하고 접종률과 접근성을 향상시키고 있습니다. mRNA나 서브유닛 기술과 같은 제조 플랫폼에서의 최근 진보로 바이러스 발생 시 신속한 대응 능력이 강화되어 세계에서 견고한 공중 위생 전략을 지원함과 동시에 모든 연령층에서 예방접종의 보급이 진행되고 있습니다.

2024년 북미의 백신 시장 규모는 323억 달러로 평가되었고, 2034년에는 CAGR 6.6%를 나타내 593억 달러에 이를 전망입니다. 이 지역의 리더십은 종합적인 건강 관리 인프라, 지속적인 공공 예방 접종 캠페인 및 예방 의료에 대한 엄청난 투자로 인한 것입니다. 일관된 정책 수준의 노력, 높은 인지도, HPV 및 기타 바이러스 위협을 대상으로 한 백신에 대한 강한 수요가 지속적으로 매출을 이끌고 있습니다. 미국에서는 학교 단위의 예방접종 프로그램과 성인에 대한 예방접종이 널리 실시되고 있어 인구층 전체에서의 액세스와 컴플라이언스가 강화되고 있습니다.

세계의 백신 시장 경쟁 역학에 기여하는 주요 제조업체는 Sanofi, Serum Institute of India, Valneva, CSL Seqirus, Emergent Biosolutions, Pfizer, Modernna, Novavax, GlaxoSmithKline(GSK), AstraZeneca, Biofarma, Sinovac, Bharat Bio Bio-Pharmaceutical, VBI 백신, Merck 등이 있습니다. 백신 부문의 주요 기업들은 연구 개발, 특히 mRNA, 재조합 서브유닛, 벡터 기반 제제 등 신규 플랫폼에 대한 지속적인 투자를 통해 파이프라인을 적극적으로 진화시키고 있습니다.

생명공학기업, 학술기관, 정부보건기관과의 제휴 및 합작사업은 차세대 백신의 개발과 규제 당국의 인가를 가속화하는 데 도움이 됩니다. 기업은 또한 아웃브레이크 시 신속한 확장성을 확보하고 충분한 서비스를 받지 못한 시장에 효율적으로 대응하기 위해 생산 능력을 세계로 확대하고 있습니다. 제제 및 치료 백신의 개발을 포함한 전략적 제품의 다양화는 기업이 보다 광범위한 질병 부담을 해결하는 데 도움이 됩니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 감염증의 발생률의 상승

- 예방접종 보급 프로그램의 확대

- 신흥 경제 국가에서 소아 인구 증가

- 백신의 처방과 생산 효율의 진보

- 업계의 잠재적 위험 및 과제

- 엄격한 규제 승인 프로세스

- 백신의 보관 및 운송에 걸리는 고비용

- 시장 기회

- 백신 배포를 위한 관민 파트너십 확대

- 조합에 대한 주목이 높아지는 백신

- 성장 촉진요인

- 성장 가능성 분석

- 기술의 상황

- 파이프라인 분석

- 규제 상황

- 향후 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 확장 계획

제5장 시장 추계·예측 : 백신 유형별(2021-2034년)

- 주요 동향

- 서브 유닛 백신

- 재조합 백신

- 접합 백신

- 다당류 백신

- 톡소이드 백신

- 불활화 백신

- 약독화 생백신

- 기타 백신 유형

제6장 시장 추계·예측 : 질환 유형별(2021-2034년)

- 주요 동향

- 바이러스성 질환

- 간염

- 인플루엔자

- HPV

- 홍역, 유행성이하선염, 풍진(MMR)

- 로타 바이러스

- 대상포진

- COVID-19

- 기타 바이러스성 질환

- 세균성 질환

- 수막 구균성 질환

- 폐렴구균 질환

- DPT

- 기타 세균성 질환

제7장 시장 추계·예측 : 연령별(2021-2034년)

- 주요 동향

- 소아

- 성인

제8장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 공공

- 개인

- 전문 클리닉

- 기타 용도

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- AstraZeneca

- Bharat Biotech

- Biofarma

- CSL Seqirus

- Emergent Biosolutions

- GlaxoSmithKline(GSK)

- Haffkine Bio-Pharmaceutical

- Merck

- Moderna

- Novavax

- Pfizer

- Sanofi

- Serum Institute of India

- Sinovac

- Valneva

- VBI Vaccines

The Global Vaccines Market was valued at USD 76.4 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 145.8 billion by 2034. This growth is largely propelled by the continuous emergence of infectious diseases such as hepatitis, seasonal influenza, and novel virus strains. As these diseases remain a constant threat to public health, governments and health organizations are ramping up immunization efforts to reduce infection rates. Supportive public initiatives, increasing healthcare budgets in developing regions, and advancements in vaccine R&D continue to shape a favorable environment for expansion. Additionally, the global rise in combination vaccines, which deliver immunity for multiple diseases through a single dose, is accelerating innovation and simplifying immunization protocols.

Development of next-generation vaccines targeting complex conditions such as cancers, chronic infections, and autoimmune diseases is expanding the market's therapeutic scope. A growing aging population, especially across developed nations, remains highly susceptible to infections, further fueling global vaccine demand. Strong collaborations between private firms and public health bodies, coupled with evolving technologies such as mRNA and recombinant protein platforms, are enhancing vaccine efficacy, delivery, and accessibility. Collectively, these factors are reinforcing long-term market momentum.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $76.4 Billion |

| Forecast Value | $145.8 Billion |

| CAGR | 7.1% |

In 2024, subunit vaccines segment was valued at USD 37.6 billion and is estimated to reach USD 70.7 billion by 2034, growing at a CAGR of 6.9%. These vaccines include recombinant, polysaccharide, and conjugate types, each contributing to heightened immunogenicity without using whole pathogens. Their ability to target specific proteins from disease-causing organisms improves safety profiles and reduces unwanted immune responses. The segment continues to gain traction due to its T cell-dependent immune activation, which promotes stronger memory responses, long-lasting protection, and suitability for vulnerable populations like infants and young children.

The viral diseases segment held 66.2% share in 2024 and is expected to maintain strong growth through 2034. The category comprises vaccines for hepatitis, influenza, HPV, rotavirus, herpes zoster, MMR, COVID-19, and other viruses. As awareness and prevention efforts have expanded, immunization programs have scaled globally, improving coverage and access. Recent advancements in manufacturing platforms like mRNA and subunit technologies have enhanced rapid-response capabilities during viral outbreaks, supporting robust public health strategies worldwide and increasing uptake across all age groups.

North America Vaccines Market generated USD 32.3 billion in 2024 and is expected to reach USD 59.3 billion by 2034 at a CAGR of 6.6%. The region's leadership stems from its comprehensive healthcare infrastructure, ongoing public immunization campaigns, and significant investment in preventive care. Consistent policy-level initiatives, high levels of awareness, and strong demand for vaccines targeting HPV and other viral threats continue to drive sales. The U.S. has implemented widespread school-based programs and adult immunization drives, enhancing access and compliance across population segments.

Key manufacturers contributing to the competitive dynamics of the Global Vaccines Market include Sanofi, Serum Institute of India, Valneva, CSL Seqirus, Emergent Biosolutions, Pfizer, Moderna, Novavax, GlaxoSmithKline (GSK), AstraZeneca, Biofarma, Sinovac, Bharat Biotech, Haffkine Bio-Pharmaceutical, VBI Vaccines, and Merck. Leading companies in the vaccines sector are actively advancing their pipelines through sustained investments in R&D, particularly in novel platforms like mRNA, recombinant subunits, and vector-based formulations.

Partnerships and joint ventures with biotech firms, academic institutions, and government health agencies are helping expedite development and regulatory clearance for next-gen vaccines. Firms are also expanding production capabilities globally to ensure rapid scalability during outbreaks and to serve underserved markets efficiently. Strategic product diversification, including development of combination and therapeutic vaccines, is helping companies address broader disease burdens.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vaccine type

- 2.2.3 Disease type

- 2.2.4 Age group

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of infectious disease

- 3.2.1.2 Growing immunization coverage programs

- 3.2.1.3 Increasing pediatric population in developing economies

- 3.2.1.4 Advancements in vaccine formulation and production efficiency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory approval processes

- 3.2.2.2 High cost of storage and transportation of vaccine

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding public-private partnerships for vaccine distribution

- 3.2.3.2 Growing focus on combination vaccines

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.5 Pipeline analysis

- 3.6 Regulatory landscape

- 3.7 Future market trends

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 Expansion plans

Chapter 5 Market Estimates and Forecast, By Vaccine Type, 2021-2034 ($ Mn)

- 5.1 Key trends

- 5.2 Subunit vaccines

- 5.2.1 Recombinant vaccines

- 5.2.2 Conjugate vaccines

- 5.2.3 Polysaccharide vaccines

- 5.3 Toxoid vaccines

- 5.4 Inactivated vaccines

- 5.5 Live attenuated vaccines

- 5.6 Other vaccine types

Chapter 6 Market Estimates and Forecast, By Disease Type, 2021-2034 ($ Mn)

- 6.1 Key trends

- 6.2 Viral diseases

- 6.2.1 Hepatitis

- 6.2.2 Influenza

- 6.2.3 HPV

- 6.2.4 Measles, mumps, and rubella (MMR)

- 6.2.5 Rotavirus

- 6.2.6 Herpes zoster

- 6.2.7 Covid-19

- 6.2.8 Other viral diseases

- 6.3 Bacterial diseases

- 6.3.1 Meningococcal diseases

- 6.3.2 Pneumococcal diseases

- 6.3.3 DPT

- 6.3.4 Other bacterial diseases

Chapter 7 Market Estimates and Forecast, By Age Group, 2021-2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pediatric

- 7.3 Adult

Chapter 8 Market Estimates and Forecast, By End Use, 2021-2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.2.1 Public

- 8.2.2 Private

- 8.3 Specialty clinics

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AstraZeneca

- 10.2 Bharat Biotech

- 10.3 Biofarma

- 10.4 CSL Seqirus

- 10.5 Emergent Biosolutions

- 10.6 GlaxoSmithKline (GSK)

- 10.7 Haffkine Bio-Pharmaceutical

- 10.8 Merck

- 10.9 Moderna

- 10.10 Novavax

- 10.11 Pfizer

- 10.12 Sanofi

- 10.13 Serum Institute of India

- 10.14 Sinovac

- 10.15 Valneva

- 10.16 VBI Vaccines