|

시장보고서

상품코드

1797687

바닥재용 화학제품 시장 기회, 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Flooring Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

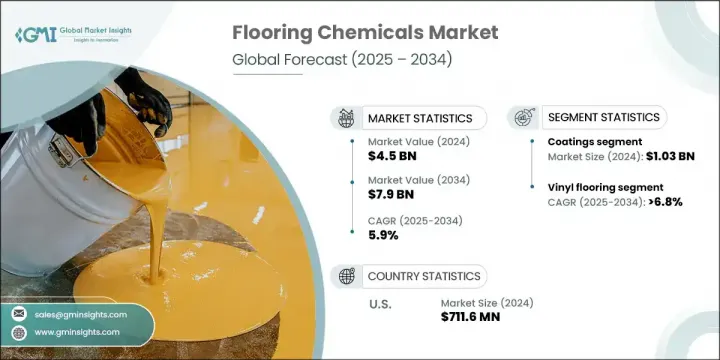

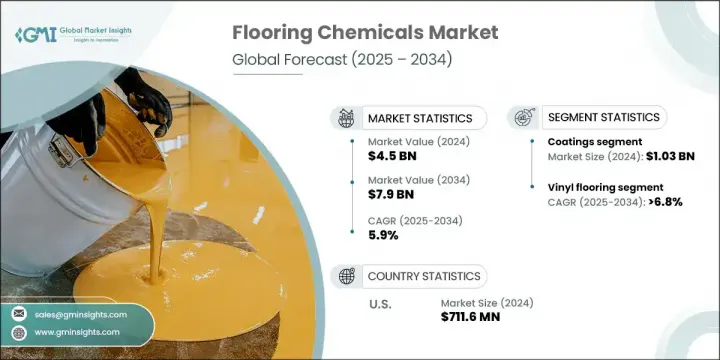

세계의 바닥재용 화학제품 시장 규모는 2024년에는 45억 달러에 달하고, CAGR 5.9%로 성장할 전망이며 2034년에는 79억 달러에 이를 것으로 예측됩니다.

이 시장은 친환경 소재와 저배출 화학 제형으로 전환으로 시장이 급속히 진화하고 있습니다. 지속가능성이 핵심 관심사로 부상함에 따라 제조업체들은 환경 규제와 변화하는 소비자 기대를 모두 충족시키기 위해 VOC 수준을 낮추고 바이오 기반 함량을 높인 고급 바닥재 솔루션을 개발하고 있습니다. 스마트 제조 기술과 디지털 도구가 생산 공정에 통합되어 공정 효율성, 품질 관리 및 수요 대응력을 강화하고 있습니다.

디지털화 확대는 실시간 모니터링, 공급망 조정 개선 및 고객 요구의 정밀 타겟팅을 가능하게 합니다. 고성능, 내구성, 지속가능성을 갖춘 바닥재 소재에 대한 수요 증가는 주거용, 상업용, 산업용 건설 전반에 걸쳐 광범위한 수요를 촉진하고 있습니다. 수지, 코팅제, 접착제와 같은 바닥재용 화학제품은 다양한 환경적 부하 하에서 바닥의 미적 요소, 내마모성, 기능성을 개선하는 핵심 요소입니다. 탄력성, 쉬운 유지보수, 최소한의 환경 영향을 결합한 바닥재 시스템의 강력한 혁신과 빠른 채택으로 시장이 혜택을 보며, 이는 선진국과 신흥 지역을 아우르는 전 세계 확장을 더욱 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 45억 달러 |

| 예측 금액 | 79억 달러 |

| CAGR | 5.9% |

코팅 부문은 2024년 10억 3,000만 달러를 창출했으며, 2034년까지 7.2%의 연평균 성장률(CAGR)로 지속 성장할 것으로 예상됩니다. 코팅, 접착제 및 실란트는 목재, 타일, 라미네이트, 비닐 등 다양한 소재의 바닥 설치 및 보호에 여전히 핵심적입니다. 배출에 대한 인식이 높아짐에 따라 기업들은 저휘발성 유기화합물(VOC) 및 속숙성 접착제 제형을 혁신하여 주거 및 상업 건설 전반에 걸쳐 수요를 촉진하고 있습니다. 수성 및 바이오 기반 접착제의 고급 제품 발전은 최소한의 환경적 영향과 다양한 바닥재 유형에 대한 적응성으로 주목받고 있습니다.

비닐 바닥재 부문은 2025년부터 2034년까지 연평균 6.8%의 성장률을 보일 것으로 예상됩니다. 이 바닥재 솔루션은 다용도성과 내구성으로 주목받고 있으며, 특히 습기 취약 지역 및 고인파 지역에서의 성장세를 보이고 있는 백킹, 접착제, 표면 코팅 분야의 화학적 혁신으로 그 장점이 강화되고 있습니다. 카펫과 같은 다른 인기 바닥재 유형은 친환경 건축 기준과 공공 보건 기대에 부응하기 위해 항균 처리 및 저배출 소재 분야에서 고급 진전을 보이고 있습니다.

2024년 미국의 바닥재용 화학제품 시장 점유율은 80%를 차지했으며 7억 1,160만 달러의 매출을 기록했습니다. 미국 바닥재용 화학제품 부문은 활발한 주택 건설, 리모델링 동향, 성능 중심 바닥재 시스템 수요에 힘입어 성장하고 있습니다. 지역별 다양한 기후와 건축 규정을 고려하여 코팅제, 프라이머, 접착제 분야의 혁신은 기후 변화에 강하고 구조물 특성에 맞춘 솔루션에 집중되고 있습니다. 이로 인해 미국은 바닥재용 화학제품 기술 혁신의 핵심 허브로 자리매김했습니다.

전 세계 바닥재용 화학제품 시장의 주요 기업은 Sika AG, BASF SE, The Dow Chemical Company, Henkel AG & Co.KGaA, 3M Company 등입니다. 바닥재용 화학제품 시장의 주요 기업은 VOC 배출량이 적고 내구성이 향상된 고급 제형을 개발하기 위해 R&D에 투자하고 있습니다. 진화하는 규제에 대응하고 지속가능한 제품에 대한 소비자 수요 증가에 대응하기 위해 보다 환경친화적인 화학제품로 이동하고 있습니다. 바닥재 제조업체 및 건설 회사와의 전략적 파트너십은 다양한 시공 요구에 맞는 통합 솔루션을 생성하기 위해 형성됩니다. 각 회사는 고성장 지역에 새로운 제조 시설을 개설하고 유통망을 강화하여 세계적인 발자취를 확대하고 있습니다. 실시간 분석 및 스마트 물류를 포함한 디지털 변환은 비즈니스 효율성을 높입니다. 마케팅 전략은 환경 의식이 높은 구매자와 환경 의식이 높은 소비자의 주목을 받기 위해 환경과 건강을 배려한 바닥재용 화학제품의 이점을 크게 다루고 있습니다.

목차

제1장 조사 방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역 및 국가

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 촉진요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 코스트 내역 분석

- 특허 분석

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산 에너지 효율

- 환경 친화적 인 노력

- 탄소발자국의 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병(M&A)

- 파트너십 및 협업

- 신제품 발매

- 확장계획과 자금조달

제5장 시장 추계 및 예측, 제품 유형별(2021-2034년)

- 주요 동향

- 접착제

- 수성 접착제

- 용매 기반 접착제

- 우레탄 기반 및 습기 경화 접착제

- 분말 접착제

- 핫멜트 접착제

- 실란트

- 실리콘 실란트

- 폴리우레탄 실란트

- 아크릴 실란트

- 부틸 실란트

- 코팅

- 에폭시 코팅

- 폴리우레탄 코팅

- 폴리아스파르트산 코팅

- 아크릴 코팅

- 항균 코팅

- 프라이머 및 표면 처리

- 에폭시 프라이머

- 아크릴 프라이머

- 폴리우레탄 프라이머

- 표면 처리용 화학약품

- 기초재 및 평활화제

- 셀프 벨벳 컴파운드

- 방습 배리어

- 방음 기초

- 바닥 마감제 및 연마제

- 수성 마감

- 용매 기반 마감

- UV 경화 마감

- 유지관리용 폴리쉬

제6장 시장 추계 및 예측, 용도별(2021-2034년)

- 주요 동향

- 경목 바닥

- 라미네이트 바닥재

- 비닐 바닥재

- 카펫 바닥

- 타일 및 석재 바닥재

- 콘크리트 바닥재

- 기타 바닥재

제7장 시장 추계 및 예측, 최종 용도별(2021-2034년)

- 주요 동향

- 주거용

- 단독 주택

- 다세대 주택

- 리모델링 및 개조

- 상업용

- 오피스 빌딩

- 소매 공간

- 호텔

- 의료시설

- 교육기관

- 산업

- 제조 시설

- 창고 및 배송 센터

- 식품 가공 공장

- 의약품 시설

- 화학 처리 공장

제8장 시장 추계 및 예측, 기술별(2021-2034년)

- 주요 동향

- 기존 화학 시스템

- 기존 에폭시 시스템

- 표준 폴리우레탄 배합

- 기존 아크릴 시스템

- 고급 화학 기술

- 나노기술 활용 처방

- 스마트 및 기능적 코팅

- 자기 복구 재료

- 항균 기술

- 지속 가능하고 바이오 시스템

- 바이오 기반 폴리우레탄

- 식물 기반 접착제

- 재활용 컨텐츠 배합

- 낮은 VOC 및 제로 VOC 시스템

- 특수 및 고성능 시스템

- 내약품성 제제

- 내고온 시스템

- 정전기 방지 및 전도성 시스템

- 장식과 미적 시스템

제9장 시장 추계 및 예측, 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 필리핀

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 이집트

제10장 기업 프로파일

- BASF SE

- Sika AG

- Henkel AG & Co. KGaA

- The Dow Chemical Company

- 3M Company

- Sherwin-Williams Company

- Mapei SpA

- HB Fuller Company

- RPM International Inc.

- Arkema Group

The Global Flooring Chemicals Market was valued at USD 4.5 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 7.9 billion by 2034. The market is rapidly evolving due to a shift toward eco-friendly materials and low-emission chemical formulations. As sustainability becomes a core focus, manufacturers are developing advanced flooring solutions with reduced VOC levels and increased bio-based content to meet both environmental regulations and changing consumer expectations. Smart manufacturing techniques and digital tools are being integrated into production to ensure greater process efficiency, quality control, and responsiveness to demand.

Increasing digitalization is enabling real-time monitoring, improved supply chain coordination, and precise targeting of customer needs. The push for high-performance, durable, and sustainable flooring materials is fueling widespread demand across residential, commercial, and industrial construction. Flooring chemicals such as resins, coatings, and adhesives are central to improving floor aesthetics, wear resistance, and functionality under varying environmental loads. The market is benefiting from strong innovation and rapid adoption of flooring systems that combine resilience, easy maintenance, and minimal environmental impact, further reinforcing its global expansion across developed and emerging regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.5 Billion |

| Forecast Value | $7.9 Billion |

| CAGR | 5.9% |

The coatings segment generated USD 1.03 billion in 2024 and is expected to continue growing at 7.2% CAGR through 2034. Coatings, adhesives, and sealants remain critical to floor installation and protection across multiple materials including wood, tile, laminate, and vinyl. With rising awareness around emissions, companies are innovating low-VOC and fast-curing adhesive formulations, boosting demand across both residential and commercial construction. Product advancements in water-based and bio-based adhesives have gained traction for their minimal environmental footprint and adaptability across diverse flooring types.

The vinyl flooring segment is expected to grow at a CAGR of 6.8% from 2025 to 2034. This flooring solution is gaining momentum due to its versatility and resilience, enhanced by chemical innovations in backings, adhesives, and surface coatings that boost performance in moisture-prone and high-traffic areas. Other popular flooring types, like carpet, are seeing advancements in antimicrobial treatments and low-emission materials to align with green building standards and public health expectations.

United States Flooring Chemicals Market held 80% share and generated USD 711.6 million in 2024. The U.S. flooring chemicals sector is thriving on the back of strong housing construction, renovation trends, and demand for performance-based flooring systems. With its diverse climate and varying construction codes across regions, innovation in coatings, primers, and adhesives is focused on climate-resilient and structure-specific solutions. This has positioned the U.S. as a key hub for innovation in flooring chemical technologies.

Leading companies in the Global Flooring Chemicals Market include Sika AG, BASF SE, The Dow Chemical Company, Henkel AG & Co. KGaA, and 3M Company. Major players in the flooring chemicals market are investing in R&D to develop advanced formulations with lower VOC emissions and improved durability. They are shifting toward greener chemistries to comply with evolving regulations and to meet rising consumer demand for sustainable products. Strategic partnerships with flooring material manufacturers and construction firms are being formed to create integrated solutions tailored to diverse installation needs. Companies are expanding their global footprints by opening new manufacturing facilities in high-growth regions and strengthening distribution networks. Digital transformation, including real-time analytics and smart logistics, is enhancing operational efficiency. Marketing strategies now focus heavily on the environmental and health benefits of eco-conscious flooring chemicals to capture the attention of both commercial buyers and environmentally aware consumers.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Applications

- 2.2.4 End use

- 2.2.5 Technology

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 ($Bn, Kilo tons)

- 5.1 Key trends

- 5.2 Adhesives

- 5.2.1 Water-based adhesives

- 5.2.2 Solvent-based adhesives

- 5.2.3 Urethane-based/moisture-cure adhesives

- 5.2.4 Powder adhesives

- 5.2.5 Hot-melt adhesives

- 5.3 Sealants

- 5.3.1 Silicone sealants

- 5.3.2 Polyurethane sealants

- 5.3.3 Acrylic sealants

- 5.3.4 Butyl sealants

- 5.4 Coatings

- 5.4.1 Epoxy coatings

- 5.4.2 Polyurethane coatings

- 5.4.3 Polyaspartic coatings

- 5.4.4 Acrylic coatings

- 5.4.5 Antimicrobial coatings

- 5.5 Primers and surface preparation

- 5.5.1 Epoxy primers

- 5.5.2 Acrylic primers

- 5.5.3 Polyurethane primers

- 5.5.4 Surface preparation chemicals

- 5.6 Underlayments and smoothing compounds

- 5.6.1 Self-leveling compounds

- 5.6.2 Moisture barriers

- 5.6.3 Sound dampening underlayments

- 5.7 Floor finishes and polishes

- 5.7.1 Water-based finishes

- 5.7.2 Solvent-based finishes

- 5.7.3 UV-cured finishes

- 5.7.4 Maintenance polishes

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Kilo tons)

- 6.1 Key trends

- 6.2 Hardwood flooring

- 6.3 Laminate flooring

- 6.4 Vinyl flooring

- 6.5 Carpet flooring

- 6.6 Tile and stone flooring

- 6.7 Concrete flooring

- 6.8 Other flooring types

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Kilo tons)

- 7.1 Key trends

- 7.2 Residential

- 7.2.1 Single-family homes

- 7.2.2 Multi-family residential

- 7.2.3 Renovation and remodeling

- 7.3 Commercial

- 7.3.1 Office buildings

- 7.3.2 Retail spaces

- 7.3.3 Hospitality

- 7.3.4 Healthcare facilities

- 7.3.5 Educational institutions

- 7.4 Industrial

- 7.4.1 Manufacturing facilities

- 7.4.2 Warehouses and distribution centers

- 7.4.3 Food processing plants

- 7.4.4 Pharmaceutical facilities

- 7.4.5 Chemical processing plants

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Kilo tons)

- 8.1 Key trends

- 8.2 Conventional chemical systems

- 8.2.1 Traditional epoxy systems

- 8.2.2 Standard polyurethane formulations

- 8.2.3 Conventional acrylic systems

- 8.3 Advanced chemical technologies

- 8.3.1 Nanotechnology-enhanced formulations

- 8.3.2 Smart and functional coatings

- 8.3.3 Self-healing materials

- 8.3.4 Antimicrobial technologies

- 8.4 Sustainable and bio-based systems

- 8.4.1 Bio-based polyurethanes

- 8.4.2 Plant-based adhesives

- 8.4.3 Recycled content formulations

- 8.4.4 Low-voc and zero-voc systems

- 8.5 Specialty and high-performance systems

- 8.5.1 Chemical-resistant formulations

- 8.5.2 High-temperature resistant systems

- 8.5.3 Anti-static and conductive systems

- 8.5.4 Decorative and aesthetic systems

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Kilo tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 France

- 9.3.3 Italy

- 9.3.4 Spain

- 9.3.5 Russia

- 9.3.6 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Philippines

- 9.4.7 Vietnam

- 9.4.8 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Egypt

Chapter 10 Company Profiles

- 10.1 BASF SE

- 10.2 Sika AG

- 10.3 Henkel AG & Co. KGaA

- 10.4 The Dow Chemical Company

- 10.5 3M Company

- 10.6 Sherwin-Williams Company

- 10.7 Mapei S.p.A.

- 10.8 H.B. Fuller Company

- 10.9 RPM International Inc.

- 10.10 Arkema Group