|

시장보고서

상품코드

1797744

채뇨 기기 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Urine Collection Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

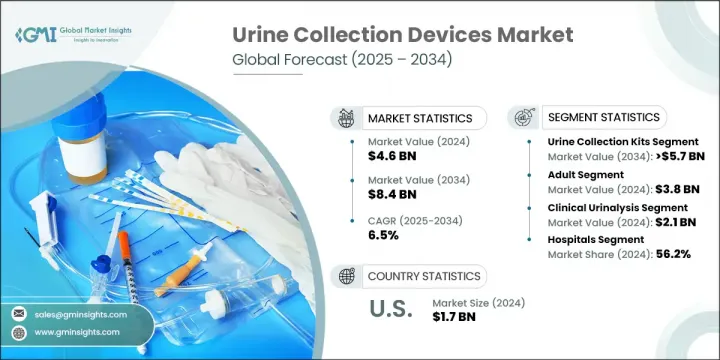

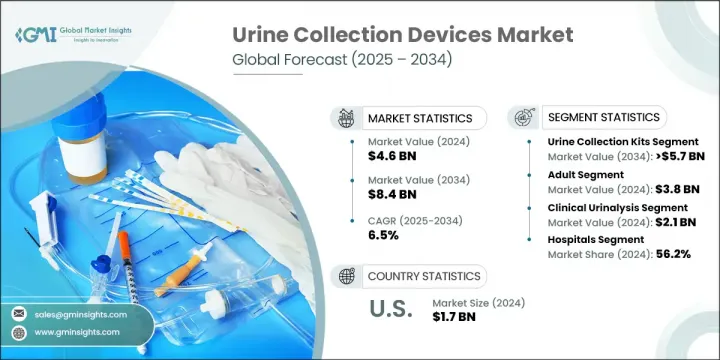

세계의 채뇨 기기 시장은 2024년 46억 달러로 평가되었으며 CAGR 6.5%로 성장해 2034년까지 84억 달러에 이를 것으로 예측됩니다.

시장 확대는 만성 신장병, 요로 감염, 실금을 겪는 고령화 사회의 부담 증가에 강하게 지지되고 있습니다. 재택 헬스케어로의 전환, POC(Point of Care) 진단의 성장, 기기의 기능과 디자인에 있어서의 지속적인 기술 혁신이 계속해서 시장 동향을 형성하고 있습니다. 채뇨 기기는 안전하고 무균이며 정확한 샘플을 채취, 수송 및 보관할 수 있게 함으로써 진단에 중요한 역할을 합니다. 이 도구는 컵과 시료 가방에서 채취 키트 및 운송 용기에 이르기까지 병원, 클리닉, 실험실 및 재택 환경에서 널리 사용됩니다. 특히 만성기 의료 및 대사 진단에서 질병 스크리닝의 빈도가 증가함에 따라 이러한 서비스에 대한 지속적인 수요가 이어지고 있습니다. 의료의 분산화가 현저해지고 환자 중심의 케어 모델이 진화함에 따라 사용하기 쉽고 위생적이고 신뢰할 수 있는 채뇨 시스템에 대한 관심이 높아지고 있습니다. 이러한 시장 역학은 기업이 생산 규모를 확대하면서 샘플 취급과 진단 정확도를 높이는 기술에 투자하는 데 도움이 됩니다.

신장학, 종양학, 내분비학 등의 분야에서 임상시험의 수가 증가하고 있기 때문에 유전체, 단백질체학, 바이오마커 검사에 대응한 고도의 채뇨 솔루션에 대한 수요가 높아지고 있습니다. 연구자들은 운송 및 분석 중에 시료의 무결성을 유지하는 멸균되고 화학적으로 안정한 용기를 점점 더 필요로 합니다. 그 결과 공급업체는 실험실 연구에 맞는 보다 전문적인 키트를 개발하고 보다 광범위한 임상 연구 생태계를 지원합니다. 또한, 이동이 곤란한 환자나 만성질환 환자에 대한 재택의료의 확대에 의해 종래의 임상 현장 이외의 채뇨 용품의 사용이 확대되고 있습니다. 이러한 전환은 휴대성, 안전성, 사용 편의성에 중점을 둔 제품 설계의 진화에 기여합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 46억 달러 |

| 예측 금액 | 84억 달러 |

| CAGR | 6.5% |

채뇨 키트 부문은 2024년에 69.4%의 점유율을 차지했습니다. 이 강한 지위는 주로 가정용 진단 키트에 대한 의존도 증가, 분산 임상시험의 성장, 무균 안전한 시료 취급의 중요성 증가로 인한 것입니다. 이 키트는 임상 시설 외부의 사용자에게도 편의성과 접근성을 제공하여 진단 컴플라이언스 및 관리 연속성을 향상시키는 데 도움이 됩니다. 채뇨 키트의 높은 채용률은 만성 질환 모니터링, 생식 의료, 약물 검사 등의 용도에서 볼 수 있습니다.

임상뇨 검사 응용 분야는 2024년에 21억 달러를 창출하고 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 6.1%를 보일 것으로 예측됩니다. 소변 검사는 요로 결석과 당뇨병에서 신장 질환 및 대사성 질환에 이르기까지 광범위한 질병을 확인하기 위한 최전선 진단 도구로 지속되기 때문에 이 부문은 시장을 선도하고 있습니다. 병원과 진단센터는 주요 최종 사용자이며 정확한 검사 결과를 유지하기 위해 화학적으로 안정적이고 오염에 강한 기기에 의존합니다. 정기적 인 건강 진단과 만성 질환 진단이 증가함에 따라 소변 검사는 예방 및 급성기 의료의 핵심으로 확고한 지위를 구축하고 있습니다.

유럽 채뇨 기기 시장은 2024년 13억 달러에 달했습니다. 이 지역은 고도로 발달한 헬스케어 인프라와 비침습적 검사법의 광범위한 채용이 장점. 1인당 의료비가 높고 광범위한 공공 스크리닝 프로그램이 병원과 재택 모두에서 소변 검사 수요를 가속화하고 있습니다. 서유럽와 스칸디나비아 국가에서는 노인 집단의 만성 비뇨기 질환 관리에 중점을 두었기 때문에 특히 높은 사용률을 보여줍니다.

세계 채뇨 기기 시장에 진출하는 주요 기업은 BioTouch, QIAGEN, Ardo Medical, Thermo Fisher Scientific, Roche, Abbott, POLYMED, Aspen Surgical, Cardinal Health, HENSO, Convatec, Becton, Dickinson and Company, Labcorp (Litholink), MEDLINE, ANGIPLAST 등이 있습니다. 채뇨 기기 시장에서 경쟁하는 기업은 제품 혁신, 전략적 파트너십 및 세계 전개를 활용하여 발판을 굳히고 있습니다. 핵심은 최신 임상 및 홈케어 워크플로우에 따른 사용자 중심의 무균 일회용 키트의 개발입니다. 많은 기업들이 진화하는 진단 기준을 충족하기 위해 변조 방지 및 샘플 저장 기능을 갖춘 스마트 패키징 솔루션에 투자하고 있습니다. 의료 제공자나 검사실과의 공동 개발에 의해 특정의 검사 용도에 맞춘 목적 주도형 제품의 공동 개발이 가능하게 되었습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성 신장병(CKD) 유병률 증가

- 고령화 인구 증가

- 비침습성 진단 툴 수요 증가

- 채뇨 기기의 기술 진보

- 업계의 잠재적 위험 및 과제

- 오염이나 샘플 취급 에러의 위험

- 시장 기회

- 소변을 이용한 액체 생검과 유전체 검사의 이용 증가

- 소아가 다루기 쉽고 스마트한 개발 채뇨 기기

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 분석, 2024

- 갭 분석

- Porter's Five Forces 분석

- PESTLE 분석

- 미래 시장 동향

- 밸류체인 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 유형의 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품 유형별, 2021-2034년

- 주요 동향

- 소변 채취 키트

- 소변 샘플 가방

- 소변컵 및 용기

제6장 시장 추계 및 예측 : 환자별, 2021-2034년

- 주요 동향

- 성인

- 소아

제7장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 임상뇨 검사

- 요로 감염(UTI)

- 신장 질환

- 기타 임상 소변 검사

- 약물 검사

- 임신 검사

- 임상조사 및 조사

제8장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 병원

- 진단 실험실

- 재택 케어 환경

- 기타 용도

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Abbott

- ANGIPLAST

- Ardo Medical

- Aspen Surgical

- Becton, Dickinson and Company

- BioTouch

- Cardinal Health

- convatec

- HENSO

- Labcorp(Litholink)

- MEDLINE

- POLYMED

- QIAGEN

- Roche

- Thermo Fisher Scientific

The Global Urine Collection Devices Market was valued at USD 4.6 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 8.4 billion by 2034. Market expansion is strongly supported by the rising burden of chronic kidney diseases, urinary tract infections, and an aging population dealing with incontinence. The shift toward home-based healthcare, together with the growth in point-of-care diagnostics and ongoing innovation in device functionality and design, continues to shape market trends. Urine collection devices play a crucial role in diagnostics by enabling safe, sterile, and accurate sample gathering, transportation, and storage. These tools-ranging from cups and specimen bags to collection kits and transport containers-are extensively used across hospitals, clinics, laboratories, and at-home settings. The increased frequency of disease screening, particularly in chronic care and metabolic diagnostics, is driving sustained demand for these services. As decentralized healthcare becomes more prominent and patient-centric care models evolve, there is significant interest in user-friendly, hygienic, and reliable urine collection systems. These market dynamics are helping companies scale production while investing in technology that enhances sample handling and diagnostic precision.

The rising number of clinical investigations in fields such as nephrology, oncology, and endocrinology is pushing demand for advanced urine collection solutions that are compatible with genomic, proteomic, and biomarker testing. Researchers increasingly require sterile, chemically stable containers that preserve sample integrity during transport and analysis. As a result, suppliers are developing more specialized kits tailored to lab research, supporting the wider clinical research ecosystem. Additionally, the expansion of home-based care for patients with limited mobility or chronic illness is promoting broader use of urine collection products outside traditional clinical settings. This transition is contributing to an evolving product design landscape focused on portability, safety, and ease of use.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.6 Billion |

| Forecast Value | $8.4 Billion |

| CAGR | 6.5% |

The urine collection kits segment held a 69.4% share in 2024. This strong position is primarily due to the increasing reliance on at-home diagnostic kits, growth in decentralized clinical trials, and the rising importance of sterile and secure specimen handling. These kits offer convenience and accessibility to users outside of clinical facilities, helping improve diagnostic compliance and continuity of care. High adoption of urine collection kits is seen in applications like chronic disease monitoring, reproductive health, and drug testing.

The clinical urinalysis application segment generated USD 2.1 billion in 2024 and is projected to grow at a CAGR of 6.1% during 2025-2034. This segment leads the market because urine testing remains a frontline diagnostic tool in identifying a wide range of disorders, from UTIs and diabetes to kidney and metabolic conditions. Hospitals and diagnostic centers are the main end users, relying on chemically stable, contamination-resistant devices to maintain accurate laboratory results. The growing volume of regular health screenings and chronic condition diagnostics has solidified urinalysis as a cornerstone in preventative and acute care.

Europe Urine Collection Devices Market reached USD 1.3 billion in 2024. The region benefits from a highly developed healthcare infrastructure and widespread adoption of non-invasive testing methods. High per capita health expenditure and broad public screening programs are helping accelerate demand for urine testing in both hospitals and home-based settings. Countries in Western Europe and Scandinavia show particularly high usage due to increased focus on managing chronic urological conditions in elderly populations.

Major players operating in the Global Urine Collection Devices Market include BioTouch, QIAGEN, Ardo Medical, Thermo Fisher Scientific, Roche, Abbott, POLYMED, Aspen Surgical, Cardinal Health, HENSO, Convatec, Becton, Dickinson and Company, Labcorp (Litholink), MEDLINE, and ANGIPLAST. Companies competing in the urine collection devices market are leveraging product innovation, strategic partnerships, and global expansion to strengthen their foothold. A core focus lies in developing user-centric, sterile, and disposable kits that align with modern clinical and home care workflows. Many firms are investing in smart packaging solutions with tamper-evidence and sample-preservation features to meet evolving diagnostic standards. Collaborations with healthcare providers and laboratories are enabling co-development of purpose-driven products tailored to specific testing applications.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Patient trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic kidney diseases (CKD)

- 3.2.1.2 Growing geriatric population

- 3.2.1.3 Rising demand for non-invasive diagnostic tools

- 3.2.1.4 Technological advancements in urine collection devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of contamination and sample handling errors

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing use of urine-based liquid biopsy and genomic testing

- 3.2.3.2 Development of pediatric-friendly and smart urine collection devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2024

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

- 3.11 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 Latin America

- 4.3.6 MEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Urine collection kits

- 5.3 Urine specimen bags

- 5.4 Urine cups and containers

Chapter 6 Market Estimates and Forecast, By Patient, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Adult

- 6.3 Pediatric

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Clinical urinalysis

- 7.2.1 Urinary tract infections (UTI)

- 7.2.2 Kidney disorders

- 7.2.3 Other clinical urinalysis

- 7.3 Drug screening

- 7.4 Pregnancy testing

- 7.5 Clinical research and studies

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Diagnostic laboratories

- 8.4 Home care settings

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott

- 10.2 ANGIPLAST

- 10.3 Ardo Medical

- 10.4 Aspen Surgical

- 10.5 Becton, Dickinson and Company

- 10.6 BioTouch

- 10.7 Cardinal Health

- 10.8 convatec

- 10.9 HENSO

- 10.10 Labcorp (Litholink)

- 10.11 MEDLINE

- 10.12 POLYMED

- 10.13 QIAGEN

- 10.14 Roche

- 10.15 Thermo Fisher Scientific