|

시장보고서

상품코드

1797780

전동 지게차 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Electric Forklift Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

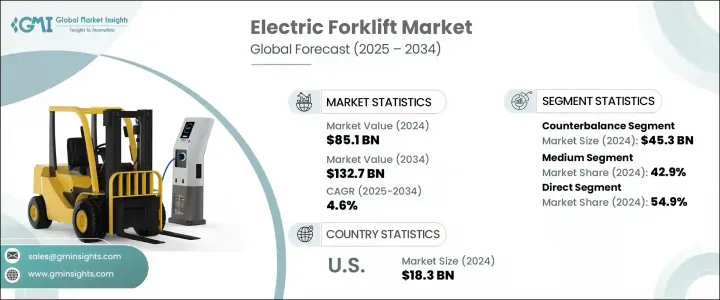

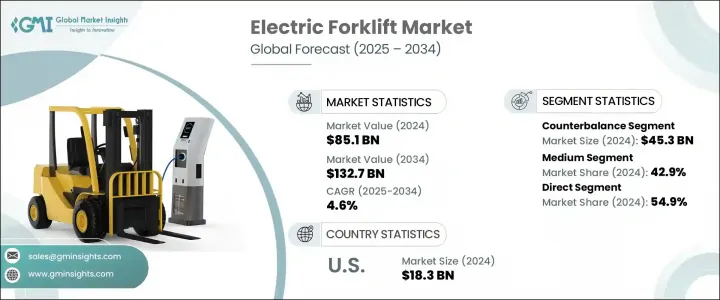

세계의 전동 지게차 시장은 2024년에는 851억 달러로 평가되었고, CAGR 4.6%를 나타내 2034년에는 1,327억 달러에 이를 것으로 추정됩니다.

이 꾸준한 성장의 원동력이 되는 것은 내연기관에서 보다 지속가능한 배터리 구동으로의 전환이 진행되고 있다는 것입니다. 산업계가 보다 깨끗하고 비용 효율적인 자재관리 솔루션을 요구하는 가운데 전동 지게차는 물류, 창고 관리, 제조 및 소매 분야에서 큰 지지를 받고 있습니다. 친환경 운영과 총소유비용 절감에 대한 수요 증가는 배출가스 저감, 소음 저감, 효율 개선을 제공하는 전동 지게차 모델의 채용을 기업에 촉구하고 있습니다. 정부와 규제기관이 보다 엄격한 배출 기준을 추진하고 있는 가운데, 전동 지게차는 많은 선진국과 신흥 경제 국가에서 선호되는 선택이 되고 있습니다.

성장을 가속하는 주요 요인은 배터리 기술의 급속한 진화입니다. 납 배터리는 역사적으로 대부분의 전동 지게차에 전력을 공급해 왔지만, 충전 사이클의 길이와 지속적인 유지 보수에 시달리고 있습니다. 대조적으로, 리튬 이온 배터리는 더 빠른 충전, 더 높은 에너지 밀도 및 최소한의 유지 보수 요구 사항을 제공함으로써 시장을 재구성하고 있습니다. 또한 리튬 이온 배터리는 '기회 충전'에도 대응하고 있어, 오퍼레이터는 단시간의 작업 중단중에 배터리의 수명을 줄이지 않고 배터리의 전력을 보충할 수 있습니다. 이 기능을 사용하면 작업 시간 동안 기계를 더 오랫동안 가동할 수 있어 생산성 향상에 기여할 수 있습니다. 수소 연료전지 기술의 출현도 특히 까다로운 산업 응용 분야에서 주목을 받고 있습니다. 이러한 시스템은 종종 3분 미만의 초고속 연료 공급과 일관된 중단 없는 워크플로우를 가능하게 하는 장시간 작동을 제공합니다. 연료전지는 가동 중지 시간을 최소화해야 하며, 장시간 이동이 일반적인 경우에 실용적인 선택이 되고 있습니다. 일부 제조업체들은 수소 기반 시스템을 활용하여 배터리 구동 장치에 비해 다운타임을 2자리 줄이는 데 성공했습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 851억 달러 |

| 예측 금액 | 1,327억 달러 |

| CAGR | 4.6% |

제품 유형 중 카운터 밸런스 전동 지게차 부문은 2024년에 453억 달러를 창출했고 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 3.5%를 나타낼 것으로 예측됩니다. 이 모델은 세계에서 판매되는 지게차 유닛의 60% 가까이를 차지하고 있으며, 다용도와 간편한 조작성으로 시장의 주력 제품이 되고 있습니다. 이 지게차의 구조에는 무거운 전단 짐을 들어 올릴 때 안정성을 제공하는 후방 카운터 웨이트가 포함되어 있어 대용량 및 고주파 리프팅 환경에 이상적입니다.

중간 용량 전기 지게차 부문은 2024년에 42.9%의 점유율을 차지했으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 5.1%를 나타낼 것으로 예측됩니다. 이러한 모델은 자동차, 제조업, 항만, 물류 거점 등 리프팅 능력과 조종성의 균형이 요구되는 작업에서 선호됩니다. 리튬 이온 배터리의 진보로 에너지 밀도가 200Wh/kg로, 몇년전의 2배 이상으로 높아졌기 때문에 이러한 포크리프트는 현재, 장시간의 시프트에서도 운전할 수 있어 불과 1-2시간으로 재충전할 수 있게 되어 실용성이 더욱 높아지고 있습니다.

2024년 미국의 전동 지게차 시장 규모는 183억 달러를 기록했고 2034년까지 연평균 복합 성장률(CAGR) 5.3%를 나타낼 것으로 예측됩니다. 이 나라의 리더십은 확립된 제조 인프라, 자동화 주도 운영, 지속가능성을 요구하는 강력한 규제 추진에 기인하고 있습니다. 활황을 보이고 있는 전자상거래와 창고관리분야가 지게차 수요의 급증에 기여하고 있으며, 전동모델은 운전비용과 배출가스 저감을 실현하고 있습니다. 미국은 또한 제조업자와 판매자의 강력한 기반, 광범위한 서비스 네트워크, 숙련 노동력으로부터 혜택을 받고 있으며, 전동 지게차의 혁신과 전개에 있어서 세계적인 리더로 자리매김하고 있습니다.

세계의 전동 지게차 시장을 선도하는 주요 기업으로는 Hyster-Yale Materials Handling, Inc., Toyota Material Handling, Mitsubishi Logisnext Co.Ltd., KION Group AG, Junheinrich AG 등이 있습니다. 경쟁 전략 측면에서 주요 전동 지게차 제조업체는 배터리 기술, 시스템 통합 및 지능형 차량 관리 플랫폼을 강화하기 위한 연구 개발에 적극적으로 투자하고 있습니다. 대부분은 다양한 용도 요구에 맞는 모듈식 배터리 팩과 확장 가능한 에너지 시스템에 주력하고 있습니다. 에너지 기업 및 인프라 제산업체와의 협업은 배터리 충전 및 수소 공급 스테이션의 간소화에 도움이 됩니다. 제조업체는 또한 텔레매틱스 및 원격 진단 기능을 개선하기 위해 노력하고 있으며, 함대 운영자가 성능을 모니터링하고 유지 보수를 계획하며 함대 사용률을 최적화 할 수 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 배터리 기술의 진보

- 환경규제와 지속가능성 목표

- 전자상거래와 창고업의 성장

- 업계의 잠재적 위험 및 과제

- 높은 초기 투자 비용

- 한정된 고내구성

- 기회

- 신흥 시장 진출

- 스마트 창고와의 통합

- 급속 충전 및 교환 가능한 배터리 솔루션 개발

- 성장 촉진요인

- 성장 가능성 분석

- 향후 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 규제 프레임워크

- 규격과 인증

- 환경규제

- 수출입 규제

- 무역 통계

- 주요 수입국

- 주요 수출국

- Porter's Five Forces 분석

- PESTEL 분석

- 소비자 행동 분석

- 구입 패턴

- 선호 분석

- 소비자 행동의 지역차

- 전자상거래가 구매결정에 미치는 영향

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계·예측 : 유형별(2021-2034년)

- 주요 동향

- 카운터 밸런스

- 창고 지게차

- 팔레트 잭 및 스태커

- 리치 트랙

- 기타

제6장 시장 추계·예측 : 용량별(2021-2034년)

- 주요 동향

- 소형(3톤 미만)

- 중형(3-10톤)

- 대형(10톤 이상)

제7장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 공장

- 창고

- 소매점

- 식품 및 제약

- 건설 현장

- 기타

제8장 시장 추계·예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접

- 간접

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 말레이시아

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

제10장 기업 프로파일

- Anhui Heli Co., Ltd.

- Clark Material Handling Company

- Crown Equipment Corporation

- Doosan Industrial Vehicle Co., Ltd.

- EP Equipment Co., Ltd.

- Hangcha Group Co., Ltd.

- Hyster-Yale Materials Handling, Inc.

- Hyundai Material Handling

- Jungheinrich AG

- KION Group AG

- Komatsu Ltd.

- Lonking Holdings Limited

- Mitsubishi Logisnext Co., Ltd.

- Noblelift Intelligent Equipment Co., Ltd.

- Toyota Material Handling

The Global Electric Forklift Market was valued at USD 85.1 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 132.7 billion by 2034. This steady growth is being driven by the ongoing transition from internal combustion engines to more sustainable, battery-powered alternatives. As industries seek cleaner and more cost-efficient material handling solutions, electric forklifts are gaining significant traction across logistics, warehousing, manufacturing, and retail sectors. The growing demand for environmentally friendly operations and lower total cost of ownership is pushing businesses to adopt electric forklift models that offer reduced emissions, less noise, and improved efficiency. With governments and regulatory bodies continuing to push stricter emissions standards, electric forklifts are becoming a preferred choice in many developed and developing economies.

A key factor driving growth is the rapid evolution in battery technologies. While lead-acid batteries have historically powered most electric forklifts, they suffer from lengthy charge cycles and ongoing maintenance. In contrast, lithium-ion batteries are reshaping the market by offering faster charging, higher energy density, and minimal maintenance requirements. They also support "opportunity charging," which allows operators to top up battery power during brief operational breaks without diminishing battery life. This feature helps improve productivity by keeping machines operational longer throughout the workday. The emergence of hydrogen fuel cell technology is also gaining attention, especially for demanding industrial applications. These systems offer ultra-fast refueling-often under three minutes-and extended operation times that allow for consistent, uninterrupted workflow. Fuel cells are becoming a practical alternative where downtime needs to be minimized and long shifts are common. Several manufacturers are leveraging hydrogen-based systems to reduce downtime by double-digit percentages compared to battery-powered units.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $85.1 Billion |

| Forecast Value | $132.7 Billion |

| CAGR | 4.6% |

Among the product types, the counterbalance electric forklifts segment generated USD 45.3 billion in 2024 and is expected to grow at a CAGR of 3.5% between 2025 and 2034. These models represent nearly 60% of the total forklift units sold globally and remain the workhorse of the market due to their versatility and straightforward operation. Their construction includes rear counterweights that provide stability when lifting heavy front-end loads, making them ideal for high-capacity, high-frequency lifting environments.

The medium-capacity electric forklifts segment held 42.9% share in 2024 and is forecast to grow at a CAGR of 5.1% from 2025 to 2034. These models are favored in operations that demand a balance between lifting capacity and maneuverability-such as in automotive, manufacturing, ports, and distribution hubs. With lithium-ion battery advancements pushing energy densities as high as 200 Wh/kg-more than double what was available just a few years ago-these forklifts can now operate for extended shifts and recharge in just 1 to 2 hours, further enhancing their practicality.

United States Electric Forklift Market generated USD 18.3 billion in 2024 and is projected to grow at a CAGR of 5.3% through 2034. The country's leadership is attributed to its well-established manufacturing infrastructure, automation-driven operations, and a strong regulatory push for sustainability. The booming e-commerce and warehousing segments are contributing to soaring forklift demand, with electric models offering lower operating costs and emissions. The U.S. also benefits from a strong base of manufacturers and distributors, extensive service networks, and a skilled labor force, positioning it as a global leader in electric forklift innovation and deployment.

Key players leading the Global Electric Forklift Market include Hyster-Yale Materials Handling, Inc., Toyota Material Handling, Mitsubishi Logisnext Co., Ltd., KION Group AG, and Jungheinrich AG. In terms of competitive strategies, major electric forklift manufacturers are aggressively investing in research and development to enhance battery technologies, system integration, and intelligent fleet management platforms. Many are focusing on modular battery packs and scalable energy systems that adapt to diverse application needs. Collaborations with energy companies and infrastructure providers help streamline battery charging and hydrogen refueling stations. Manufacturers are also working to improve telematics and remote diagnostics capabilities, allowing fleet operators to monitor performance, schedule maintenance, and optimize fleet utilization.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021-2034

- 2.2 Key market trends

- 2.2.1 Business trends

- 2.2.2 Regional trends

- 2.2.3 Type trends

- 2.2.4 Capacity trends

- 2.2.5 End use trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Advancements in battery technology

- 3.2.1.2 Environmental regulations & sustainability goals

- 3.2.1.3 Growth of e-commerce and warehousing

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Limited heavy-duty capabilities

- 3.2.3 Opportunities

- 3.2.3.1 Expansion into emerging markets

- 3.2.3.2 Integration with smart warehousing

- 3.2.3.3 Development of fast-charging and swappable battery solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation Landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory framework

- 3.7.1 Standards and certifications

- 3.7.2 Environmental regulations

- 3.7.3 Import export regulations

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Consumer behavior analysis

- 3.11.1 Purchasing patterns

- 3.11.2 Preference analysis

- 3.11.3 Regional variations in consumer behavior

- 3.11.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Counterbalance

- 5.3 Warehouse Forklifts

- 5.3.1 Pallet jacks and stackers

- 5.3.2 Reach trucks

- 5.3.3 Others

Chapter 6 Market Estimates & Forecast, By Capacity, 2021-2034, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Small (under 3 tons)

- 6.3 Medium (3-10 tons)

- 6.4 Heavy (over 10 tons)

Chapter 7 Market Estimates & Forecast, By End use, 2021-2034, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Factories

- 7.3 Warehouses

- 7.4 Retail stores

- 7.5 Food and pharma

- 7.6 Construction sites

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Distribution channel, 2021-2034, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Malaysia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Anhui Heli Co., Ltd.

- 10.2 Clark Material Handling Company

- 10.3 Crown Equipment Corporation

- 10.4 Doosan Industrial Vehicle Co., Ltd.

- 10.5 EP Equipment Co., Ltd.

- 10.6 Hangcha Group Co., Ltd.

- 10.7 Hyster-Yale Materials Handling, Inc.

- 10.8 Hyundai Material Handling

- 10.9 Jungheinrich AG

- 10.10 KION Group AG

- 10.11 Komatsu Ltd.

- 10.12 Lonking Holdings Limited

- 10.13 Mitsubishi Logisnext Co., Ltd.

- 10.14 Noblelift Intelligent Equipment Co., Ltd.

- 10.15 Toyota Material Handling