|

시장보고서

상품코드

1797782

자동차용 콘덴서 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Automotive Condenser Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

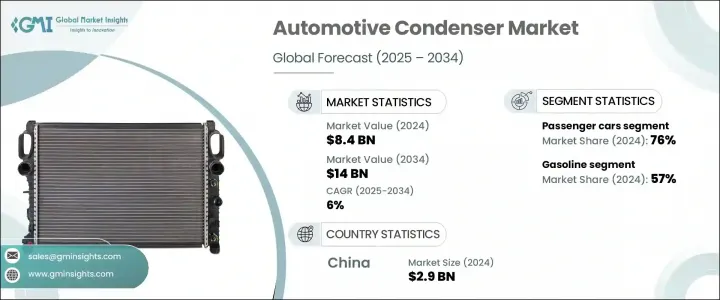

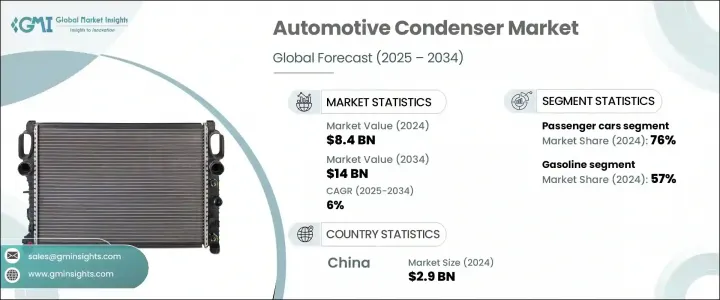

세계의 자동차용 콘덴서 시장 규모는 2024년에 84억 달러로 평가되었고, CAGR 6%를 나타내, 2034년에는 140억 달러에 이를 것으로 예측되고 있습니다.

전기자동차와 차세대 열 관리 시스템으로의 전환이 진행되고 있으며, 자동차용 콘덴서의 개발과 채용에 큰 영향을 미치고 있습니다. 최신 자동차가 보다 컴팩트하고 효율적인 구성 요소를 탑재함에 따라 고급 냉매 흐름, 열 부하 밸런싱 및 전기자동차에 특화된 HVAC 구성에 대한 기술적 숙련의 필요성이 커지고 있습니다. 이 진화는 OEM과 Tier-1 공급업체 모두 새로운 수요에 대응하기 위한 인적 자원 개발과 전문 교육을 우선하도록 촉구하고 있습니다.

자동차 제조업체는 낮은 GWP 냉매 사용, 경량 소재, 하이브리드 및 전기 플랫폼에 맞는 고효율 콘덴서 시스템에 중점을 둡니다. 이 기술적 전환은 특히 열 시스템의 유지 보수, 진단 및 구성 요소 통합에서 역할에 따라 업무별 교육이 필수적입니다. 시장의 성장은 숙련노동력을 창출하기 위한 교육기관과 민간기업과의 협력관계의 강화에 의해서도 지원되고 있습니다. 자동차 플랫폼이 지속적으로 발전함에 따라 기후대를 넘어 제품 효율을 확보하고 최적의 열 성능을 유지하는 것은 전 세계 제조업체들에게 중요한 고려 사항이 되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 84억 달러 |

| 예측 금액 | 140억 달러 |

| CAGR | 6% |

승용차 부문은 2024년에 76%의 점유율을 차지했으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 6.8%를 나타낼 것으로 예측됩니다. 이 부문의 콘덴서는 공간 절약 아키텍처, 연비 및 냉매의 국제 표준 준수를 중시하도록 설계되었습니다. 자동차 제조업체는 자동차 실내 온도 조절과 배터리 온도 조절을 지원하기 위해 고효율의 가벼운 콘덴서 유닛을 통합하여 내연 엔진과 전기자동차 플랫폼을 강화하고 있습니다. 특히 아시아태평양과 유럽에서 생산량이 많아지면서 이 부문의 성장을 가속하는데 중요한 역할을 하고 있습니다.

가솔린 자동차 부문은 2024년에 57%의 점유율을 차지했고, 2025-2034년의 CAGR은 7%를 나타낼 것으로 예측됩니다. 가솔린차가 우위를 유지하고 있는 것은 승용차와 소형 상용차의 양 부문으로 세계적으로 널리 보급되고 있는 것이 큰 요인입니다. 이러한 차량은 신뢰성 높은 냉각 성능과 흐림 방지 성능을 요구하기 때문에 자동차 제조업체는 비용 효율성과 경량성을 유지하면서 우수한 열교환 효율을 실현하는 알루미늄 기반 콘덴서 솔루션을 추진하고 있습니다. 설계 혁신은 열효율을 향상시키고 이 범주의 진화하는 차량 플랫폼의 요구에 대응하는데 여전히 중심적인 역할을 하고 있습니다.

2024년 중국의 자동차용 콘덴서 시장 규모는 29억 달러에 달했고, 점유율은 65%를 기록했습니다. 중국의 주도적 지위는 일본의 방대한 자동차 생산 능력, 확립된 공급망 네트워크 및 자동차 전기화의 야심찬 추진에 의해 지원되고 있습니다. 게다가 에너지 절약, 배기 가스 규제, 냉매 대체를 둘러싼 국가의 정책이 국내 자동차 생산에 있어서의 선진적인 열기술의 전개를 가속화하고 있어, 세계의 콘덴서 시장에 있어서의 중국의 아성을 보다 견고하게 하고 있습니다.

자동차용 콘덴서 시장의 상위를 차지하는 기업은 Modine Manufacturing Company, Valeo, 케이힌, Sanden Holdings, Hanon Systems, Denso Corporation, MAHLE 등입니다. 이 선수들은 기술 혁신과 비즈니스 규모를 통해 시장을 형성하고 있습니다. 주요 기업은 자동차용 콘덴서 시장에서 경쟁력을 강화하기 위해 EV 및 하이브리드 플랫폼에 최적화된 고성능 및 경량의 콘덴서 솔루션을 개발하기 위한 연구 개발에 많은 투자를 하고 있습니다. 하논 시스템즈, 케이힌, Modine 등의 제조업체는 최신의 모빌리티 솔루션의 열 수요를 충족하는 컴팩트하고 에너지 효율적인 유닛 설계에 주력하고 있습니다. 자동차 제조업체와의 공동 개발을 통해 플랫폼에 특화된 열 관리 시스템을 공동 개발하는 것은 핵심 전략입니다. 또한 많은 기업들이 세계 생산시설을 확대하고 지역별 공급망을 강화함으로써 보다 신속한 납품과 각 지역의 컴플라이언스를 확보하고 있습니다.

목차

제1장 조사 방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역/국가

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계 자동차 생산 증가

- 차량 에어컨 시스템 수요 증가

- HVAC 시스템의 기술적 진보

- 정부는 EV 인프라와 부품을 지원

- 경량?컴팩트한 콘덴서 설계로의 이행

- 첨단 배터리 열 관리 시스템에 콘덴서 통합

- 업계의 잠재적 위험 및 과제

- 공급망의 혼란

- 엄격한 환경 규제

- 시장 기회

- 상용차에 있어서의 전동화 증가

- 자율주행차에 있어서의 열 솔루션 수요

- 친환경 냉매 대응 콘덴서 기술 개발

- 신흥국의 애프터마켓 수요 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출과 수입

- 코스트 내역 분석

- 특허 분석

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적인 노력

- 탄소발자국의 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획과 자금조달

제5장 시장 추계·예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 세단

- 해치백

- SUV

- 상용차

- 소형

- 중형

- 대형

제6장 시장 추계·예측 : 추진력별(2021-2034년)

- 주요 동향

- 가솔린

- 디젤

- 전기

- PHEV

- HEV

- FCEV

제7장 시장 추계·예측 : 디자인별(2021-2034년)

- 주요 동향

- 서펜타인

- 병렬 흐름

- 튜브 및 핀

제8장 시장 추계·예측 : 재료별(2021-2034년)

- 주요 동향

- 알루미늄

- 구리

제9장 시장 추계·예측 : 판매 채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 인도네시아

- 필리핀

- 태국

- 한국

- 싱가포르

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- AVIC Xinhang

- Calsonic Kansei

- Chaoli Hi-Tech

- Delphi Technologies

- Denso

- Fawer

- Hanon Systems

- Keihin

- Koyorad

- LUZHOU North Chemical Industries

- MAHLE

- Mitsubishi Electric

- Modine Manufacturing Company

- Nissens Automotive A/S

- Pranav Vikas

- Sanden Holdings

- Tata AutoComp Systems

- Transpro

- Valeo

- Zhejiang Yinlun Machinery

The Global Automotive Condenser Market was valued at USD 8.4 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 14 billion by 2034. The ongoing transformation toward electric vehicles and next-generation thermal management systems is significantly influencing the development and adoption of automotive condensers. As modern vehicles incorporate more compact and efficient components, there is a growing need for technical proficiency in advanced refrigerant flow, thermal load balancing, and EV-specific HVAC configurations. This evolution is prompting both OEMs and Tier-1 suppliers to prioritize workforce development and specialized training to align with emerging demands.

Automotive manufacturers are shifting focus toward low-GWP refrigerant usage, lightweight materials, and high-efficiency condenser systems tailored for hybrid and electric platforms. This technological transition has made role-based and task-specific training essential, especially in thermal systems maintenance, diagnostics, and component integration. The market's growth is also being supported by increased collaboration between training institutions and the private sector to produce a skilled labor force. As automotive platforms continue to evolve, ensuring product efficiency across climate zones and maintaining optimal thermal performance is becoming a key consideration for global manufacturers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.4 Billion |

| Forecast Value | $14 Billion |

| CAGR | 6% |

The passenger cars segment held a 76% share in 2024 and is expected to grow at a CAGR of 6.8% between 2025 and 2034. Condensers in this segment are being designed with an emphasis on space-saving architecture, fuel economy, and compliance with international standards for refrigerants. Automakers are enhancing both internal combustion engine and electric vehicle platforms by integrating high-efficiency, lightweight condenser units to support cabin climate control and battery temperature regulation. High production volumes, particularly across Asia-Pacific and Europe, are playing a vital role in propelling growth in this segment.

The gasoline-powered vehicles segment held a 57% share in 2024, with growth projected at a CAGR of 7% during 2025-2034. The sustained dominance of gasoline vehicles is largely due to their widespread global presence in both passenger and light commercial segments. As these vehicles demand reliable cooling and defogging performance, automakers are advancing aluminum-based condenser solutions that deliver excellent heat exchange efficiency while remaining cost-effective and lightweight. Design innovation remains central to improving thermal efficiency and meeting evolving vehicle platform needs in this category.

China Automotive Condenser Market generated USD 2.9 billion and held a 65% share in 2024. Its leadership position is supported by the country's vast vehicle manufacturing capacity, established supply chain networks, and ambitious push for vehicle electrification. Additionally, national policies around energy savings, emissions control, and refrigerant substitution are accelerating the deployment of advanced thermal technologies in domestic vehicle production, thereby reinforcing China's stronghold in the global condenser market.

The top-performing companies in the Automotive Condenser Market include Modine Manufacturing Company, Valeo, Keihin, Sanden Holdings, Hanon Systems, Denso Corporation, and MAHLE. These players are shaping the market through technological innovation and operational scale. To reinforce their competitive position in the automotive condenser market, leading companies are heavily investing in R&D to develop high-performance and lightweight condenser solutions optimized for EVs and hybrid platforms. Manufacturers like Hanon Systems, Keihin, and Modine are focused on designing compact and energy-efficient units that meet the thermal demands of modern mobility solutions. Collaboration with automotive OEMs to co-develop platform-specific thermal management systems is a core strategy. Many companies are also expanding global production facilities and enhancing regional supply chains to ensure faster delivery and local compliance.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Propulsion

- 2.2.4 Design

- 2.2.5 Material

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global vehicle production

- 3.2.1.2 Growing demand for vehicle air conditioning system

- 3.2.1.3 Technological advancements in HVAC systems

- 3.2.1.4 Government supports EV infrastructure and components

- 3.2.1.5 Shift towards lightweight, compact condenser designs

- 3.2.1.6 Integration of condensers in advanced battery thermal management systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain disruptions

- 3.2.2.2 Stringent environmental regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Increased vehicle electrification in commercial fleets

- 3.2.3.2 Demand for thermal solutions in autonomous vehicles

- 3.2.3.3 Development of eco-friendly refrigerant-compatible condenser technologies

- 3.2.3.4 Expansion of aftermarket demand in emerging economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Sedans

- 5.2.2 Hatchbacks

- 5.2.3 SUV

- 5.3 Commercial vehicles

- 5.3.1 Light duty

- 5.3.2 Medium duty

- 5.3.3 Heavy duty

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Gasoline

- 6.3 Diesel

- 6.4 Electric

- 6.4.1 PHEV

- 6.4.2 HEV

- 6.4.3 FCEV

Chapter 7 Market Estimates & Forecast, By Design, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Serpentine

- 7.3 Parallel flow

- 7.4 Tube and fin

Chapter 8 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Aluminium

- 8.3 Copper

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Indonesia

- 10.4.6 Philippines

- 10.4.7 Thailand

- 10.4.8 South Korea

- 10.4.9 Singapore

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AVIC Xinhang

- 11.2 Calsonic Kansei

- 11.3 Chaoli Hi-Tech

- 11.4 Delphi Technologies

- 11.5 Denso

- 11.6 Fawer

- 11.7 Hanon Systems

- 11.8 Keihin

- 11.9 Koyorad

- 11.10 LUZHOU North Chemical Industries

- 11.11 MAHLE

- 11.12 Mitsubishi Electric

- 11.13 Modine Manufacturing Company

- 11.14 Nissens Automotive A/S

- 11.15 Pranav Vikas

- 11.16 Sanden Holdings

- 11.17 Tata AutoComp Systems

- 11.18 Transpro

- 11.19 Valeo

- 11.20 Zhejiang Yinlun Machinery