|

시장보고서

상품코드

1797795

수륙양용기 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Amphibious Aircraft Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

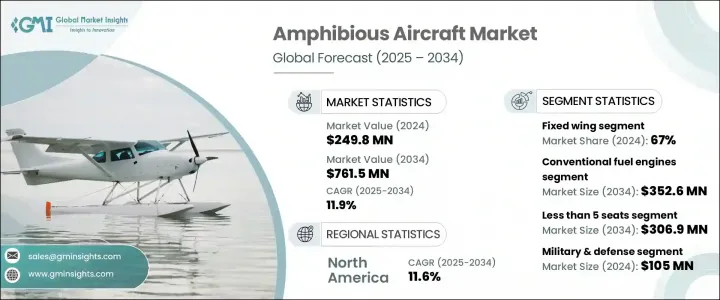

세계의 수륙양용기 시장은 2024년 2억 4,980만 달러로 평가되었으며 CAGR 11.9%를 나타내 2034년에는 7억 6,150만 달러에 이를 것으로 추정됩니다.

이 강력한 성장 궤도는 유연한 항공기 임대 모델에 대한 관심 증가와 원격지의 해안 지역에서 다목적 항공 운송에 대한 수요 증가가 주요 요인이되었습니다. 항공기 운항 회사는 자본 효율과 운항 효율을 최적화하는 것을 목표로 하므로, 임대 수륙양용기는 항공기의 구성을 쉽게 조정할 수 있어 감시와 물류에서 관광 및 긴급 서비스에 이르기까지 변화하는 임무 프로파일에 신속하게 대응할 수 있습니다.

수요를 뒷받침하는 중요한 요소는 임대가 제공하는 유연성의 향상입니다. 대규모의 선행 투자를 피함으로써 영리사업자와 전문사업자 모두 보다 새롭고 선진적인 항공기를 이용할 수 있는 반면 보유체를 실시간으로 확장하는 옵션도 유지할 수 있습니다. 이 접근법은 인도적 임무, 해외 물류 및 격리 된 지역의 지역 연결과 같은 변화하는 상황에 대한 적응성이 필요한 업무에 특히 유용합니다. 또한 해양 관광과 레크리에이션 항공 여행의 인기가 높아지고 있는 것도 기존 시장과 신흥 시장 모두에서 수륙양용기의 전개 확대에 기여하고 있습니다. 이러한 항공기는 착수가 전통적인 활주로를 대체하는 유일한 실행 가능한 옵션인 경우가 많아지면서 비용 효율적이고 시간을 절약할 수 있는 솔루션으로 간주되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 2억 4,980만 달러 |

| 예측 금액 | 7억 6,150만 달러 |

| CAGR | 11.9% |

항공기 유형별로 고정익기는 2024년 67% 점유율로 시장을 선도했습니다. 고정익 비행기 수륙양용기는 장거리 성능, 더 큰 페이로드 용량, 연료 효율로 계속 인기를 얻고 있습니다. 이러한 항공기는 일반적으로 장거리를 커버해야 하는 임무에 선호됩니다. 내식성 소재, 최신의 어비오닉스, STOL 능력의 향상 등의 기술적 강화에 의해 고정익 플랫폼은 다양한 용도에 있어서 보다 신뢰성이 높아지고 있습니다. 특히 열악한 환경조건 하에서 다용도 운용이 가능하기 때문에 민간부문과 정부부문 모두에서 지속적인 수요가 확보되고 있습니다.

추진력 유형에 따라 시장은 하이브리드 전기 추진, 전통적인 연료 엔진, 완전 전기 추진 시스템으로 분류됩니다. 전통적인 연료 엔진은 추진력의 주류를 차지하고 있으며, 이 부문은 2034년까지 3억 5,260만 달러에 달할 것으로 예측됩니다. 이러한 엔진은 높은 내구성, 항속 거리 연장, 중요한 임무에서 안정적인 성능을 필요로 하는 운영자에게 여전히 선호되는 옵션입니다. 그 신뢰성과 강력한 출력으로 방위, 소방, 장거리 운송에 이상적인 엔진이 되어, 하이브리드나 전기 기술이 초기 단계부터 시장에 도입되기 시작하고 있습니다.

수륙양용기 시장은 용도별로 군사 및 방위, 상업, 정부·공공 부문으로 나눌 수 있습니다. 군사 및 방위 분야는 2024년 1억500만 달러를 차지했습니다. 방위 조직의 임무에 특화된 항공기 플랫폼에 대한 지속적인 투자는 전략적 전략에서 수륙양용기의 중요성을 뒷받침합니다. 이 항공기는 해상 정찰, 전술 운송, 해안 감시에 중요한 역할을 합니다. 정찰, 야간 작전, 레이더 통합이 점점 중시되고 있는 가운데, 최신의 수륙 양용 플랫폼은 특히 해안선이나 섬 영토가 퍼지는 지역에서 군사력의 진화하는 요구에 맞추어 조정되고 있습니다.

지역별로는 북미가 수륙양용기 시장에서 압도적인 지위를 차지하고 있으며, 2024년에는 세계 점유율의 35.1%를 차지했으며 예측기간을 통해 CAGR 11.6%를 나타낼 것으로 전망됩니다. 이 지역에서 수륙 양용 기계가 널리 사용되는 배경에는 전략적 및 상업적 요구 사항이 모두 있습니다. 북미의 광대한 해안선, 섬, 원격지 지역사회는 육상과 수상 조건 하에서 운용 가능한 항공기에 대한 강한 수요를 창출하고 있습니다. 자금과 제도적 지원을 이용할 수 있게 됨으로써, 여러 부문에 걸친 수륙 양용 플릿의 근대화가 더욱 가속화되고 있습니다.

북미 내에서는 미국이 시장을 선도하고 있으며 2024년에는 7,720만 달러의 평가액을 기록했습니다. 이 나라에서는 수륙양용기가 장거리 감시, 신속한 전개, 군수 지원에 널리 사용되고 있습니다. 해상 운송 가능한 항공 자산에 대한 정부의 강력한 백업은 이러한 플랫폼의 전략적 중요성을 돋보이게 합니다. 이 분야에 대한 투자는 해상 환경에서 항공 즉각성 확보에 대한 헌신 증가를 반영합니다.

경쟁 구도를 형성하는 주요 기업은 ICON Aircraft, De Havilland Canada, Equator Aircraft, AVIC, AeroVolga, Hynaero, Glasair Aviation, Atol Aviation, Dornier Seawings 등입니다. 이 공개 회사는 차세대 항공기 모델 개발에 적극적으로 참여하고 있으며 성능, 안전성, 적응성을 높이고 군사, 상업 및 공공 서비스 용도의 다양한 고객 기반을 지원합니다.

목차

제1장 조사 방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역/국가

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 항공기 임대의 도입이 확대되고, 함대의 확대와 운용의 유연성 증대

- 해양 관광과 레크리에이션 활동의 확대

- 재난 구호이나 인도 지원 활동에서의 이용 증가

- 해군과 해안 경비대의 함대의 근대화

- 신흥국에 의한 방위 조달 투자 증가

- 업계의 잠재적 위험 및 과제

- 고액의 취득비용과 운영비용

- 복잡한 인증 및 규제 승인

- 시장 기회

- 하이브리드·전기자동차의 개발 수륙양용기

- 시마 섬 나라와 원격지 연안 지역의 미개척 수요

- 응급 의료 서비스(EMS)에서 수륙 양용 기계의 통합

- 민간 전세 및 관광 사업자의 참가 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 가격 전략

- 새로운 비즈니스 모델

- 컴플라이언스 요건

- 국방예산 분석

- 세계의 방위비의 동향

- 지역 방위 예산 배분

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 주요 방위 근대화 프로그램

- 예산 예측(2025-2034년)

- 업계의 성장에 미치는 영향

- 국가별 방위 예산

- 지속가능성에 대한 노력

- 공급 체인의 탄력

- 지정학적 분석

- 인재 분석

- 디지털 변혁

- 합병, 인수, 전략적 제휴의 상황

- 위험 평가 및 관리

- 주요 계약 체결(2021-2024년)

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 주요 기업의 경쟁 벤치마킹

- 재무실적의 비교

- 수익

- 이익률

- 연구개발

- 제품 포트폴리오 비교

- 제품 라인업의 넓이

- 기술

- 파괴적 혁신

- 지리적 존재의 비교

- 세계 실적 분석

- 서비스 네트워크의 범위

- 지역별 시장 침투율

- 경쟁 포지셔닝 매트릭스

- 리더들

- 과제자들

- 팔로워

- 틈새 기업

- 전략적 전망 매트릭스

- 재무실적의 비교

- 주요 발전(2021-2024년)

- 합병과 인수

- 파트너십 및 협업

- 기술적 진보

- 확대 및 투자 전략

- 지속가능성에 대한 노력

- 디지털 변혁의 대처

- 신흥기업/스타트업기업경쟁 구도

제5장 시장 추계·예측 : 기종별(2021-2034년)

- 주요 동향

- 고정익

- 회전익

제6장 시장 추계·예측 : 추진 유형별(2021-2034년)

- 주요 동향

- 기존 연료 엔진

- 터보프롭

- 피스톤

- 하이브리드 전기 추진

- 완전 전기 추진

제7장 시장 추계·예측 : 좌석 수별(2021-2034년)

- 주요 동향

- 5석 미만

- 5-10석

- 10석 이상

제8장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 군사 및 방위

- 감시 및 순찰

- 수색 및 구조

- 수륙 양용 공격 및 수송

- 상업용

- 여객 운송

- 화물 및 물류

- 관광

- 정부 및 공공 부문

- 재해 구호

- 소방

- 해양법 집행

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- AeroVolga

- Atol Aviation

- AVIC

- De Havilland Canada

- Dornier Seawings

- Equator Aircraft

- Glasair Aviation

- Hynaero

- Icon Aircraft

- Jekta Switzerland

- Legend Aircraft

- Lisa Airplanes

- Maule Air

- Osprey Aircraft

- ShinMaywa Industries

- Textron

- TL Ultralight

- Vickers Aircraft

The Global Amphibious Aircraft Market was valued at USD 249.8 million in 2024 and is estimated to grow at a CAGR of 11.9% to reach USD 761.5 million by 2034. This strong growth trajectory is largely driven by increasing interest in flexible aircraft leasing models and the rising demand for versatile air transportation in remote coastal areas. As fleet operators aim to optimize both capital and operational efficiency, leasing amphibious aircraft allows for easy adjustments in fleet composition, enabling a rapid response to shifting mission profiles, from surveillance and logistics to tourism and emergency services.

A key factor fueling demand is the enhanced flexibility that leasing provides. By avoiding large upfront investments, both commercial and specialized operators can access newer, more advanced aircraft while retaining the option to scale their fleet in real time. This approach is especially useful for operations that require adaptability in changing conditions, such as humanitarian missions, offshore logistics, or regional connectivity in isolated areas. Additionally, the growing popularity of marine tourism and recreational air travel has contributed to greater deployment of amphibious aircraft in both established and emerging markets. These aircraft are increasingly seen as a cost-effective and time-saving solution in regions where water landings are often the only viable alternative to conventional airstrips.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $249.8 Million |

| Forecast Value | $761.5 Million |

| CAGR | 11.9% |

When segmented by aircraft type, the fixed-wing category leads the market with a 67% share in 2024. Fixed-wing amphibious aircraft continue to gain traction due to their long-range capabilities, larger payload capacity, and fuel efficiency. These aircraft are typically preferred for missions requiring extended coverage over large distances. Technological enhancements such as corrosion-resistant materials, updated avionics, and improved STOL capabilities have made fixed-wing platforms more reliable for diverse applications. Their operational versatility, especially in adverse environmental conditions, ensures continued demand across both civilian and government sectors.

Based on propulsion type, the market is categorized into hybrid-electric propulsion, conventional fuel engines, and fully electric propulsion systems. Conventional fuel engines dominate the propulsion landscape, with the segment projected to reach USD 352.6 million by 2034. These engines remain the preferred choice for operators requiring high endurance, extended operational range, and consistent performance in critical missions. Their reliability and strong power output make them ideal for defense, firefighting, and long-distance transport roles, even as hybrid and electric technologies begin to enter the market in early-stage deployments.

By application, the amphibious aircraft market is divided into military & defense, commercial, and government & public sector. The military & defense segment accounted for USD 105 million in 2024. Continued investments in mission-specific aircraft platforms by defense organizations underscore the relevance of amphibious aircraft in strategic operations. These aircraft play a crucial role in maritime reconnaissance, tactical transport, and coastal monitoring. With increasing emphasis on surveillance, night-time operations, and radar integration, modern amphibious platforms are being tailored to meet the evolving needs of military forces, particularly in regions with extended coastlines and island territories.

Regionally, North America commands a dominant position in the amphibious aircraft market, accounting for 35.1% of the global share in 2024 and anticipated to grow at a CAGR of 11.6% through the forecast period. The widespread use of amphibious aircraft in this region stems from both strategic and commercial requirements. North America's extensive coastline, island clusters, and remote communities have created strong demand for aircraft capable of operating in both land and water conditions. The availability of funding and institutional support has further accelerated the modernization of amphibious fleets across multiple sectors.

Within North America, the United States leads the market, recording a valuation of USD 77.2 million in 2024. Amphibious aircraft are widely used in the country for long-range surveillance, rapid deployment, and logistics support. Strong government backing for sea-capable aviation assets highlights the strategic importance of these platforms. Investments in this sector reflect a growing commitment to ensuring aerial readiness in maritime environments.

Key players shaping the competitive landscape of the amphibious aircraft market include ICON Aircraft, De Havilland Canada, Equator Aircraft, AVIC, AeroVolga, Hynaero, Glasair Aviation, Atol Aviation, and Dornier Seawings. These companies are actively engaged in the development of next-generation aircraft models, enhancing performance, safety, and adaptability to cater to a diverse customer base across military, commercial, and public service applications.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Aircraft type trends

- 2.2.2 Propulsion type trends

- 2.2.3 Seating capacity trends

- 2.2.4 Application trends

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of aircraft leasing to support fleet expansion and operational flexibility

- 3.2.1.2 Expansion of marine tourism and recreational activities

- 3.2.1.3 Increased use in disaster relief and humanitarian missions

- 3.2.1.4 Modernization of naval and coast guard fleets

- 3.2.1.5 Rising investments in defense procurement by emerging economies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High acquisition and operational costs

- 3.2.2.2 Complex certification and regulatory approvals

- 3.2.3 Market opportunities

- 3.2.3.1 Development of hybrid and electric amphibious aircraft

- 3.2.3.2 Untapped demand in island nations and remote coastal regions

- 3.2.3.3 Integration of amphibious aircraft in emergency medical services (EMS)

- 3.2.3.4 Growing participation of private charter and tourism operators

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Defense budget analysis

- 3.13 Global defense spending trends

- 3.14 Regional defense budget allocation

- 3.14.1 North America

- 3.14.2 Europe

- 3.14.3 Asia Pacific

- 3.14.4 Middle East and Africa

- 3.14.5 Latin America

- 3.15 Key defense modernization programs

- 3.16 Budget forecast (2025-2034)

- 3.16.1 Impact on industry growth

- 3.16.2 Defense budgets by country

- 3.17 Sustainability initiatives

- 3.18 Supply chain resilience

- 3.19 Geopolitical analysis

- 3.20 Workforce analysis

- 3.21 Digital transformation

- 3.22 Mergers, acquisitions, and strategic partnerships landscape

- 3.23 Risk assessment and management

- 3.24 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Aircraft Type, 2021 - 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Fixed wing

- 5.3 Rotary wing

Chapter 6 Market Estimates and Forecast, By Propulsion Type, 2021 - 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 Conventional fuel engines

- 6.3 Turboprop

- 6.4 Piston

- 6.5 Hybrid-electric propulsion

- 6.6 Fully electric propulsion

Chapter 7 Market Estimates and Forecast, By Seating Capacity, 2021 - 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Less than 5 seats

- 7.3 5-10 seats

- 7.4 More than 10 seats

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 Military & defense

- 8.2.1 Surveillance & patrol

- 8.2.2 Search & rescue

- 8.2.3 Amphibious assault & transport

- 8.3 Commercial

- 8.3.1 Passenger transport

- 8.3.2 Cargo & logistics

- 8.3.3 Tourism

- 8.4 Government & public sector

- 8.4.1 Disaster relief

- 8.4.2 Firefighting

- 8.4.3 Maritime law enforcement

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AeroVolga

- 10.2 Atol Aviation

- 10.3 AVIC

- 10.4 De Havilland Canada

- 10.5 Dornier Seawings

- 10.6 Equator Aircraft

- 10.7 Glasair Aviation

- 10.8 Hynaero

- 10.9 Icon Aircraft

- 10.10 Jekta Switzerland

- 10.11 Legend Aircraft

- 10.12 Lisa Airplanes

- 10.13 Maule Air

- 10.14 Osprey Aircraft

- 10.15 ShinMaywa Industries

- 10.16 Textron

- 10.17 TL Ultralight

- 10.18 Vickers Aircraft