|

시장보고서

상품코드

1797847

스마트 임플란트 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Smart Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

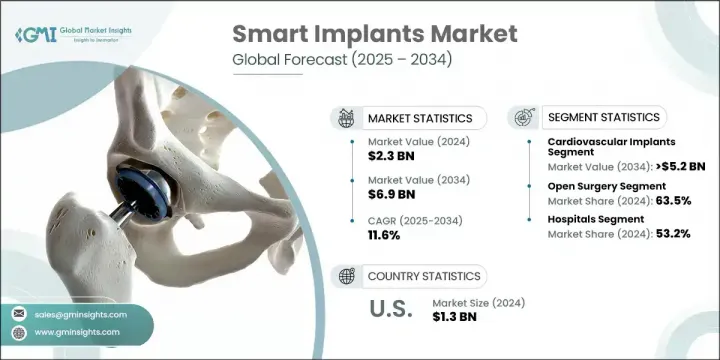

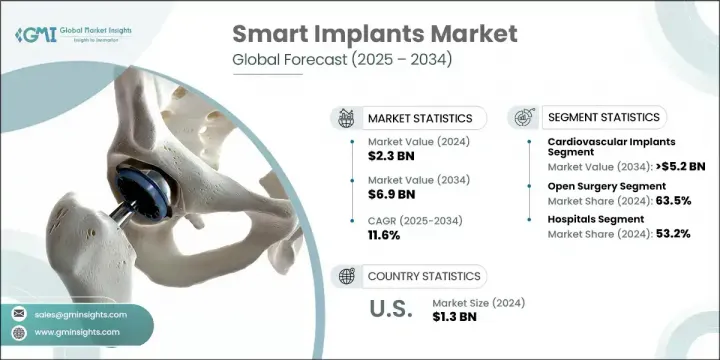

세계의 스마트 임플란트 시장은 2024년에는 23억 달러로 평가되었으며 CAGR 11.6%를 나타내 2034년에는 69억 달러에 이를 것으로 추정됩니다.

이러한 대폭적인 확대는 심혈관 질환 유병률의 상승, 스마트 의료 기술의 급속한 진보, 실시간으로 환자를 모니터링하는 기기에 대한 수요 증가 등이 함께 추진되고 있습니다. 스마트 임플란트는 치료 지원을 제공할 뿐만 아니라 진단 및 치료 최적화를 돕는 실시간 생리학적 데이터를 수집하여 현대 의료에 변혁적인 역할을 합니다. 이러한 기술은 헬스케어 시스템이 개별화된 프로액티브 케어로 이동함에 따라 기세가 증가하고 있습니다. 세계적으로 고령화가 진행됨에 따라 신흥경제국에서는 가처분소득이 증가하고 있기 때문에 시장에서는 다양한 건강상태에 적응할 수 있는 기술적으로 고도의 임플란트에 대한 수요가 꾸준히 증가하고 있습니다. 정형외과 수술의 일관된 증가, 신경 자극 장치 채택 확대, 차세대 임베디드 장치의 연구 개발 활동에 대한 투자 확대도 여러 임상 부문에서 성장을 가속화하고 있습니다.

2024년에는 심혈관 임플란트 부문이 78.1%의 점유율을 차지했습니다. 이러한 이점은 페이싱 시스템, 삽입형 모니터 및 증가하는 심장병 환자의 관리를 목적으로 하는 다른 이식형 장치에 대한 요구가 확산되고 있다는 배경입니다. 이러한 스마트 심장 장치는 치료 및 진단 능력이 지속적으로 향상되고 환자의 건강 상태를 실시간으로 의사에게 파악하고 더욱 치밀한 치료 전략을 촉진하기 위해 보다 높은 비율로 도입되고 있습니다. 만성 심혈관 질환을 앓고 있는 환자가 많은 것이 촉진요인이며, 임플란트 기능의 계속적인 진보에 의해 일상 심장병 진료에 있어서의 임상적 가치가 계속 강화되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 23억 달러 |

| 예측 금액 | 69억 달러 |

| CAGR | 11.6% |

개복 수술 부문은 2024년에 63.5%의 점유율을 차지했으며 앞으로 수년간 안정된 성장을 유지할 것으로 예측됩니다. 이 수술 접근법은 특히 복잡한 심장혈관과 정형외과 수술과 같은 해부학 가시성과 정확성을 향상시키는 것이 중요한 경우에 여전히 바람직한 방법입니다. 개복 수술은 외상 치료 및 낮은 침습 절차에 대한 접근이 제한된 지역에서도 널리 사용됩니다. 정형외과나 신경내과의 외과의사는 특히 복수의 합병증이나 해부학적 과제를 가지는 환자를 치료할 때, 그 신뢰성의 높이로부터 개복 수술을 선호하는 경우가 많습니다.

2024년 미국의 스마트 임플란트 시장 규모는 13억 달러에 이르렀고, 2034년까지 연평균 복합 성장률(CAGR)은 11.5%를 나타낼 전망입니다. 이 지역의 성장은 견고한 건강 관리 인프라의 존재, 높은 R&D 활동, 외래수술센터(ASC) 및 외래수술센터(ASC)에서 수행되는 수술 건수 증가에 의해 강화되고 있습니다. 환자의 취향이 입원기간 단축과 당일 수술로 이동함에 따라 지능형 임베디드 기기의 채용이 급증하고 있습니다. 게다가 신경질환과 심혈관질환의 유병률이 증가함에 따라 지속적인 모니터링과 표적 치료를 제공하는 첨단 임플란트 기술에 대한 수요가 계속 증가하고 있습니다.

스마트 임플란트 시장 주요 기업으로는 뉴로페이스, 보스턴 사이언티픽, 직접 싱크 서지컬, 짐머 바이오멧, 인텔리전트 임플란트, 비오트로닉, 애봇, 메드트로닉 등이 있습니다. 이러한 기업들은 기술 혁신과 환자 중심 제품 설계를 통해 업계의 방향성 형성에 적극적으로 기여하고 있습니다. 스마트 임플란트 시장에서 사업을 전개하는 기업은 경쟁력을 강화하기 위해 제품 혁신, 임상 검증, 시장 침투에 초점을 맞춘 전략적 이니셔티브를 실시했습니다. 대기업은 실시간 건강 추적을 위해 AI, 무선 통신, 센서 기술을 통합한 디바이스를 설계하기 위한 연구 개발에 많은 투자를 하고 있습니다. 학술기관과 연구기관과의 협력은 특정 질병에 맞는 임플란트의 개발을 가속화하는 데 도움이 됩니다. 지역 실적을 확대하기 위해 각 회사는 전략적 유통 파트너십을 체결하고 주요 지역에서 생산 능력을 확대하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 실시간 건강 모니터링 수요 증가

- 심혈관 질환의 발생률 증가

- 사고나 스포츠로 인한 부상 증가

- 스마트 임플란트의 기술 진보

- 업계의 잠재적 위험 및 과제

- 엄격한 규제 틀

- 임플란트의 고액의 비용

- 시장 기회

- 낮은 침습 수술에 대한 관심 증가

- 에너지 수확과 배터리리스 임플란트의 개발에 주목 증대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 임플란트 유형별 가격 동향

- 향후 시장 동향

- 스마트 임플란트에서 사이버 보안의 역할

- 비교 분석 : 스마트 임플란트와 기존 임플란트

- 소비자 행동 분석

- 상환 시나리오

- Porter's Five Forces 분석

- PESTEL 분석

- 갭 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 세계 기타 지역(RoW)

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계·예측 : 임플란트 유형별(2021-2034년)

- 주요 동향

- 심혈관 임플란트

- 정형외과 임플란트

- 신경 자극 임플란트

제6장 시장 추계·예측 : 수술별(2021-2034년)

- 주요 동향

- 개복 수술

- 최소침습 수술

제7장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 심장 케어 센터

- 외래수술센터(ASC)

- 기타 용도

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Abbott

- Biotronik

- Boston Scientific

- DirectSync Surgical

- Intelligent Implants

- Medtronic

- NeuroPace

- Zimmer Biomet

The Global Smart Implants Market was valued at USD 2.3 billion in 2024 and is estimated to grow at a CAGR of 11.6% to reach USD 6.9 billion by 2034. This significant expansion is being propelled by a combination of rising cardiovascular disease prevalence, rapid advancements in smart medical technology, and increasing demand for devices that offer real-time patient monitoring. Smart implants play a transformative role in modern medicine by not only offering therapeutic support but also collecting real-time physiological data that aids in diagnosis and treatment optimization. These technologies are gaining momentum as healthcare systems shift toward personalized and proactive care. With the global aging population growing and disposable income rising in several developed economies, the market is experiencing a steady increase in demand for technologically advanced implants that can adapt to various health conditions. The consistent increase in orthopedic surgeries, expanding adoption of neurostimulation devices, and growing investment in R&D activities for next-generation implantable devices are also accelerating growth across multiple clinical segments.

In 2024, the cardiovascular implants segment held 78.1% share. This dominance is fueled by the widespread need for pacing systems, insertable monitors, and other implantable devices aimed at managing the increasing number of individuals with cardiac conditions. These smart cardiac devices are being deployed at a higher rate as their therapeutic and diagnostic capabilities continue to improve, offering physicians real-time insight into patient health and facilitating more targeted treatment strategies. The large number of patients dealing with chronic cardiovascular disorders is a driving factor, and ongoing advancements in implant functionality continue to strengthen their clinical value in everyday cardiology practice.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $6.9 Billion |

| CAGR | 11.6% |

The open surgery segment held a 63.5% share in 2024 and is projected to maintain steady growth over the coming years. This surgical approach remains the preferred method in cases where enhanced anatomical visibility and precision are critical, especially in complex cardiovascular and orthopedic procedures. Open surgery is also widely used in trauma care and in regions where access to minimally invasive techniques is limited. Surgeons in orthopedic and neurology disciplines often favor open procedures for their reliability, particularly when treating patients with multiple comorbidities or anatomical challenges.

United States Smart Implants Market reached USD 1.3 billion in 2024 and is set to grow at a CAGR of 11.5% through 2034. Growth in this region is fueled by the presence of a robust healthcare infrastructure, high research and development activity, and an increasing volume of surgical procedures conducted in outpatient and ambulatory surgical centers. As patient preference shifts toward shorter hospital stays and same-day surgical interventions, the adoption of intelligent implantable devices is surging. Additionally, the growing prevalence of neurological and cardiovascular conditions continues to increase the demand for advanced implant technologies that offer continuous monitoring and targeted therapy delivery.

Key players in the Smart Implants Market include NeuroPace, Boston Scientific, DirectSync Surgical, Zimmer Biomet, Intelligent Implants, Biotronik, Abbott, and Medtronic. These companies are actively contributing to shaping the direction of the industry through technological innovation and patient-centric product design. Companies operating in the smart implants market are implementing strategic initiatives focused on product innovation, clinical validation, and market penetration to enhance their competitive edge. Leading players are investing heavily in R&D to design devices that integrate AI, wireless communication, and sensor technology for real-time health tracking. Collaborations with academic institutions and research bodies are helping to accelerate the development of implants tailored to specific diseases. To expand their geographic footprint, companies are entering into strategic distribution partnerships and expanding manufacturing capabilities in key regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Implant type trends

- 2.2.3 Surgery trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surging demand for real-time health monitoring

- 3.2.1.2 Growing incidence of cardiovascular disorders

- 3.2.1.3 Rise in number of accidents and sport injuries

- 3.2.1.4 Technological advancements in smart implants

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory framework

- 3.2.2.2 High cost of implants

- 3.2.3 Market opportunities

- 3.2.3.1 Rising preference for minimally invasive surgery

- 3.2.3.2 Growing focus towards development of energy-harvesting and battery-less implants

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends, by implant type

- 3.7 Future market trends

- 3.8 Role of cybersecurity in smart implants

- 3.9 Comparative analysis: Smart vs. conventional implants

- 3.10 Consumer behaviour analysis

- 3.11 Reimbursement scenario

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Rest of the world (RoW)

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Implant Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Cardiovascular implants

- 5.3 Orthopedic implants

- 5.4 Neurostimulation implants

Chapter 6 Market Estimates and Forecast, By Surgery, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Open surgery

- 6.3 Minimally invasive surgery

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Cardiac care centers

- 7.4 Ambulatory surgical centers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 Biotronik

- 9.3 Boston Scientific

- 9.4 DirectSync Surgical

- 9.5 Intelligent Implants

- 9.6 Medtronic

- 9.7 NeuroPace

- 9.8 Zimmer Biomet