|

시장보고서

상품코드

1797858

용접 강철 탱크 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Welded Steel Tanks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

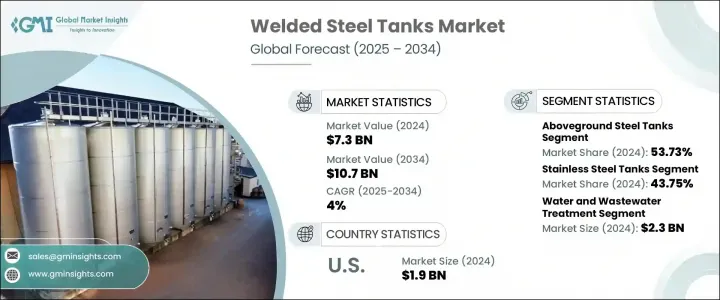

세계의 용접 강철 탱크 시장은 2024년 73억 달러로 평가되었으며 CAGR 4%로 성장해 2034년까지 107억 달러에 이를 것으로 추정됩니다.

기업이 환경 규제 강화와 운영 기준 엄격화에 직면하고 있기 때문에 다양한 산업에서 견고하고 내식성이 높은 저장 솔루션에 대한 수요가 계속 증가하고 있습니다. 용접 강철 탱크는 내구성, 수명, 가혹한 조건에 대한 적응성 때문에 수처리, 화학, 석유, 가스, 농업 등의 분야에서 필수적입니다.

산업계가 보다 지속 가능한 인프라를 목표로 하는 가운데, 재활용 가능하고 유지보수가 용이한 이 탱크는 인기를 모으고 있습니다. 또한 여러 지역에서 산업이 급성장하고 있는 것도 연료, 물, 화학물질의 봉쇄에 사용되는 대용량 저장 탱크 수요를 끌어올리고 있습니다. 또한 자동 용접 시스템, 모듈식 탱크 설계, IoT 통합 등의 기술적 진보로 효율성이 향상되고 운영 중단 시간이 단축되고 이러한 시스템의 비용 효율성이 높아지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 73억 달러 |

| 예측 금액 | 107억 달러 |

| CAGR | 4% |

환경보전과 에너지저장에 대한 관심 증가는 각 산업이 지속가능성과 장기적인 자원관리를 선호하고 있기 때문에 시장 확대를 더욱 강화하고 있습니다. 이산화탄소 배출량을 줄이고 물을 보전하기 위한 정부의 지침을 통해 기업은 환경 친화적인 노력을 지원하는 인프라에 대한 투자를 촉진하고 있으며, 용접 강철 탱크는 안전하고 효율적인 저장을 위한 실행 가능한 솔루션을 제공합니다. 용접 강철 탱크의 탱크는 빗물 저장, 바이오연료 저장, 수소 및 열 에너지 저장과 같은 재생에너지 시스템에 사용되는 경우가 늘고 있습니다.

지상형 용접 강철 탱크는 2024년 53.73%로 가장 큰 시장 점유율을 차지했으며, 2034년까지 CAGR 4.46%로 예상됩니다. 이 탱크는 비용 효율적이고 설치가 빠르며 지하 대체품보다 검사 및 유지 보수가 쉽기 때문에 지원됩니다. 적응성이 높고 설치 비용이 낮기 때문에 소규모부터 대규모 산업까지 폭넓게 이용할 수 있습니다. 지상 탱크는 기동성과 유연성을 갖추고 있으며 빠르게 변화하는 산업 환경에서 매우 가치가 있습니다. 이러한 시스템은 안전과 환경 프로토콜 준수를 보장하면서 필요에 따라 조정, 재배치 및 확장이 가능합니다.

스테인레스 강철 탱크 분야는 2024년 총 매출의 약 43.75%를 차지하며 예측 기간을 통해 CAGR 4.6%를 보일 것으로 예측됩니다. 부식 및 화학 물질에 대한 탁월한 내성으로 알려진 스테인레스 강철 탱크는 위생, 안전 및 강도가 중요한 환경에서 널리 사용됩니다. 이 탱크는 미생물의 번식에 강하고, 살균이 용이하며, 세척에 필요한 시스템의 가동 중지 시간이 최소화되므로 의약품, 식품 가공, 화학 약품 등의 분야에서 선호됩니다. 수명이 길고 유지보수가 필요하지 않기 때문에 총소유비용을 절감할 수 있는 귀중한 투자가 되고 있습니다.

미국 용접 강철 탱크 시장은 86.85%의 점유율을 차지했으며 2024년에는 6억 450만 달러를 창출했습니다. 이 이점은 이 나라의 강력한 산업 기반, 성숙한 인프라, 물 관리, 에너지 및 가공 산업에 대한 일관된 투자로 인한 것입니다. 각 기관이 엄격한 안전 및 환경 기준을 부과하는 중, 고품위 용접 강철 탱크의 채용이 확대되고 있습니다. 지역 전반의 시설은 엄격한 규정을 준수하고 화학 물질, 폐수 및 기타 물질을 저장하기 위해 이러한 탱크에 의존합니다. 또한, 노후화된 인프라의 갱신이 진행되고 있기 때문에 내식성이 뛰어나고 커스터마이즈 가능한 용접 탱크는 공공 부문과 민간 부문의 양쪽 모두의 프로젝트에서 선호되는 솔루션이 되고 있습니다.

용접 강철 탱크 시장의 주요 기업으로는 TaTank Connection, Superior Tank Co., Bulldog Steel Products, McDermott (구 CB&I), Pittsburg Tank & Tower Group, BH Tank, United Industries Group (UIG Tanks & Domes), Caldwell Tanks, Tech Fab, Skinner Tank Company, CST Industries, Highland Tank & Manufacturing Company, Lipp GmbH, TF Warren Group (Tarsco), PermianLide 등이 있습니다. 용접 강철 탱크 시장의 주요 기업은 시장의 지위를 강화하기 위해 기술 혁신, 지역 확대 및 사용자 정의에 주력하고 있습니다. 대부분은 자동화, AI를 활용한 품질 점검, 정밀 용접을 통합하여 제조 능력을 업그레이드하고 비용 절감과 내구성 향상을 도모하고 있습니다. 지속가능성은 또 다른 중점분야로 재활용 가능한 소재와 환경에 안전한 코팅을 도입하고 있습니다. 정부 기관 및 산업계 고객과의 파트너십은 기업이 물 관리 및 에너지 분야에서 대규모 계약을 획득하는 데 도움이 됩니다. 업계 고유의 요구에 맞는 탱크 구성을 제공하는 것은 애프터 서비스 및 실시간 모니터링 기술에 대한 투자와 함께 일반적인 전략입니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 산업 확대와 인프라 성장

- 엄격한 환경 규제와 ESG 이니셔티브

- 기술의 진보와 자동화

- 업계의 잠재적 위험 및 과제

- 원재료비의 변동

- 대체 재료의 경쟁

- 기회

- 물 인프라 프로젝트 확대

- 재생에너지 저장 요구

- 성장 촉진요인

- 성장 가능성 분석

- 미래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 유형별

- 규제 상황

- 표준 및 컴플라이언스 요건

- 지역 규제 틀

- 인증기준

- 무역 통계(HS코드-73090090)

- 주요 수입국

- 주요 수출국

- Porter's Five Forces 분석

- PESTLE 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 유형별, 2021-2034년

- 주요 동향

- 지상식 강철 탱크

- 지하식 강철 탱크

- 커스텀 및 모듈러 탱크

제6장 시장 추계 및 예측 : 재료별, 2021-2034년

- 주요 동향

- 탄소강 탱크

- 스테인리스 탱크

- 304 스테인레스 스틸

- 316 스테인레스 스틸

- 합금강 탱크

제7장 시장 추계 및 예측 : 설계별, 2021-2034년

- 주요 동향

- 오픈 탱크

- 클로즈 탱크

제8장 시장 추계 및 예측 : 마무리별, 2021-2034년

- 주요 동향

- 코팅 또는 라이닝된 강철 탱크

- 코팅되지 않은 강철 탱크

제9장 시장 추계 및 예측 : 용량별, 2021-2034년

- 주요 동향

- 0-10,000갤런

- 10,000-20,000갤런

- 20,000-40,000갤런

- 40,000-50,000갤런

- 50,000갤런 이상

제10장 시장 추계 및 예측 : 탱크 형태별, 2021-2034년

- 주요 동향

- 직사각형

- 원통형

제11장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 석유 및 가스 산업

- 화학산업

- 물 및 폐수 처리

- 식품 및 음료 업계

- 제약업계

- 발전

- 펄프 및 종이

- 건설

- 농업

- 기타(광업, 해양 등)

제12장 시장 추계 및 예측 : 유통 채널별, 2021-2034년

- 주요 동향

- 직접

- 간접

제13장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제14장 기업 프로파일

- BH Tank

- Bulldog Steel Products

- Caldwell Tanks

- CST Industries

- Highland Tank & Manufacturing Company

- Lipp GmbH

- McDermott(구 CB&I)

- PermianLide

- Pittsburg Tank & Tower Group

- Skinner Tank Company

- Superior Tank Co.

- Tank Connection

- TechFab

- TF Warren Group(Tarsco)

- United Industries Group(UIG Tanks & Domes)

The Global Welded Steel Tank Market was valued at USD 7.3 billion in 2024 and is estimated to grow at a CAGR of 4% to reach USD 10.7 billion by 2034. The demand for robust and corrosion-resistant storage solutions across various industries continues to rise, as companies face increasing environmental regulations and stricter operational standards. Welded steel tanks have become essential in sectors like water treatment, chemicals, oil and gas, and agriculture due to their durability, longevity, and adaptability to harsh conditions.

As industries move toward more sustainable infrastructure, these tanks are gaining popularity for being recyclable and easier to maintain. Rapid industrial growth across several regions is also boosting the demand for high-capacity storage tanks used for fuel, water, and chemical containment. Additionally, technological advancements such as automated welding systems, modular tank designs, and IoT integration are improving efficiency, reducing operational downtime, and making these systems more cost-effective.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.3 Billion |

| Forecast Value | $10.7 Billion |

| CAGR | 4% |

The growing focus on environmental conservation and energy storage is further driving market expansion, as industries across sectors prioritize sustainability and long-term resource management. Government mandates aimed at reducing carbon emissions and conserving water are prompting businesses to invest in infrastructure that supports green initiatives, and welded steel tanks offer a viable solution for safe and efficient storage. These tanks are increasingly being used for rainwater harvesting, biofuel storage, and renewable energy systems, including hydrogen and thermal energy storage applications.

Aboveground welded steel tanks held the largest market share in 2024 at 53.73% and are expected to register a 4.46% CAGR through 2034. These tanks are favored for being cost-effective, quicker to install, and easier to inspect and maintain than underground alternatives. Their adaptability and lower setup costs make them viable across small to large-scale industries. Aboveground tanks offer mobility and flexibility, which are highly valuable in rapidly changing industrial environments. These systems can be adjusted, repositioned, or expanded as needed while ensuring compliance with safety and environmental protocols.

The stainless-steel tanks segment contributed around 43.75% of total revenue in 2024 and is forecasted to grow at a CAGR of 4.6% through the forecast period. Known for their exceptional resistance to corrosion and chemical exposure, stainless steel tanks are extensively used in environments where hygiene, safety, and strength are critical. These tanks are preferred by businesses in sectors like pharmaceuticals, food processing, and chemicals because they resist microbial growth, are easy to sanitize, and require minimal system downtime for cleaning. Their long service life and low maintenance requirements make them a valuable investment with reduced total cost of ownership.

United States Welded Steel Tank Market held an 86.85% share and generated USD 604.5 million in 2024. This dominance stems from the country's strong industrial base, mature infrastructure, and consistent investment in water management, energy, and processing industries. With agencies enforcing strict safety and environmental standards, the adoption of high-grade welded steel tanks is growing. Facilities across the region rely on these tanks to store chemicals, wastewater, and other materials in compliance with rigorous regulations. Additionally, the ongoing replacement of aging infrastructure has made corrosion-resistant and customizable welded tanks a preferred solution in both public and private sector projects.

Key players in the Welded Steel Tank Market include Tank Connection, Superior Tank Co., Bulldog Steel Products, McDermott (formerly CB&I), Pittsburg Tank & Tower Group, BH Tank, United Industries Group (UIG Tanks & Domes), Caldwell Tanks, Tech Fab, Skinner Tank Company, CST Industries, Highland Tank & Manufacturing Company, Lipp GmbH, TF Warren Group (Tarsco), and PermianLide. Leading companies in the welded steel tank market are focusing on innovation, regional expansion, and customization to strengthen their market position. Many are upgrading their manufacturing capabilities by integrating automation, AI-powered quality checks, and precision welding to reduce costs and improve durability. Sustainability is another focus area, with firms introducing recyclable materials and environmentally safe coatings. Partnerships with government bodies and industrial clients are helping companies win large-scale contracts in water management and energy sectors. Offering tailored tank configurations for industry-specific needs has become a common strategy, along with investing in after-sales services and real-time monitoring technologies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.3 Data collection methods

- 1.4 Data mining sources

- 1.4.1 Global

- 1.4.2 Regional/Country

- 1.5 Base estimates and calculations

- 1.5.1 Base year calculation

- 1.5.2 Key trends for market estimation

- 1.6 Primary research and validation

- 1.6.1 Primary sources

- 1.7 Forecast model

- 1.8 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Material

- 2.2.4 Design

- 2.2.5 Finishing

- 2.2.6 Capacity

- 2.2.7 Tank Shape

- 2.2.8 End use

- 2.2.9 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.4 Critical success factors for market players

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Industrial expansion and infrastructure growth

- 3.2.1.2 Stringent environmental regulations and ESG initiatives

- 3.2.1.3 Technological advancements and automation

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Volatile raw material costs

- 3.2.2.2 Competition of alternative materials

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of water infrastructure projects

- 3.2.3.2 Renewable energy storage needs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation Landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS code - 73090090)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Mn) (Thousand Units)

- 5.1 Key trends

- 5.2 Aboveground steel tanks

- 5.3 Underground steel tanks

- 5.4 Custom/modular tanks

Chapter 6 Market Estimates & Forecast, By Material, 2021 - 2034 ($Mn) (Thousand Units)

- 6.1 Key trends

- 6.2 Carbon steel tanks

- 6.3 Stainless steel tanks

- 6.3.1 304 stainless steels

- 6.3.2 316 stainless steels

- 6.4 Alloy steel tanks

Chapter 7 Market Estimates & Forecast, By Design, 2021 - 2034 ($Mn) (Thousand Units)

- 7.1 Key trends

- 7.2 Open tanks

- 7.3 Close tanks

Chapter 8 Market Estimates & Forecast, By Finishing, 2021 - 2034 ($Mn) (Thousand Units)

- 8.1 Key trends

- 8.2 Coated or lined steel tanks

- 8.3 Uncoated steel tanks

Chapter 9 Market Estimates & Forecast, By Capacity, 2021 - 2034 ($Mn) (Thousand Units)

- 9.1 Key trends

- 9.2 0-10,000 gallons

- 9.3 10,000-20,000 gallons

- 9.4 20,000-40,000 gallons

- 9.5 40,000-50,000 gallons

- 9.6 Above 50,000 gallons

Chapter 10 Market Estimates & Forecast, By Tank Shape, 2021 - 2034 ($Mn) (Thousand Units)

- 10.1 Key trends

- 10.2 Rectangular

- 10.3 Cylindrical

Chapter 11 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn) (Thousand Units)

- 11.1 Key trends

- 11.2 Oil & gas industry

- 11.3 Chemical industry

- 11.4 Water and wastewater treatment

- 11.5 Food & beverage industry

- 11.6 Pharmaceutical industry

- 11.7 Power generation

- 11.8 Pulp & Paper

- 11.9 Construction

- 11.10 Agriculture

- 11.11 Others (Mining, Marine, etc.)

Chapter 12 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Mn) (Thousand Units)

- 12.1 Key trends

- 12.2 Direct

- 12.3 Indirect

Chapter 13 Market Estimates & Forecast, By Region, 2021 - 2034 ($ Bn, Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 U.S.

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 UK

- 13.3.2 Germany

- 13.3.3 France

- 13.3.4 Italy

- 13.3.5 Spain

- 13.3.6 Russia

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 Australia

- 13.4.5 South Korea

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.6 MEA

- 13.6.1 UAE

- 13.6.2 South Africa

- 13.6.3 Saudi Arabia

Chapter 14 Company Profiles

- 14.1 BH Tank

- 14.2 Bulldog Steel Products

- 14.3 Caldwell Tanks

- 14.4 CST Industries

- 14.5 Highland Tank & Manufacturing Company

- 14.6 Lipp GmbH

- 14.7 McDermott (formerly CB&I)

- 14.8 PermianLide

- 14.9 Pittsburg Tank & Tower Group

- 14.10 Skinner Tank Company

- 14.11 Superior Tank Co.

- 14.12 Tank Connection

- 14.13 TechFab

- 14.14 TF Warren Group (Tarsco)

- 14.15 United Industries Group (UIG Tanks & Domes)