|

시장보고서

상품코드

1797883

동결건조 주사제 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Lyophilized Injectable Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

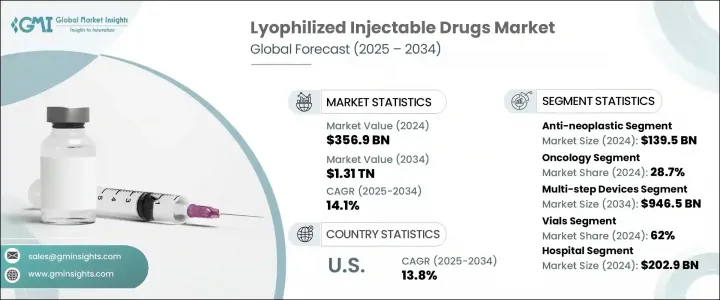

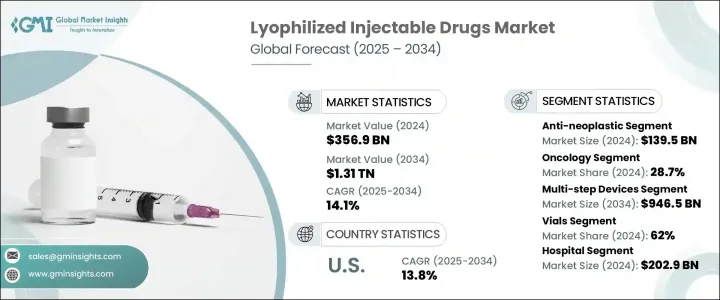

세계의 동결건조 주사제 시장은 2024년에 3,569억 달러로 평가되었고 CAGR 14.1%를 나타내 2034년에는 1조 3,100억 달러에 이를 것으로 추정됩니다.

암과 감염을 포함한 만성 건강 상태 증가로 안정적이고 장기간 작용하는 치료제에 대한 수요가 계속 증가하고 있습니다. 보존 기간의 연장과 약효 개선의 필요성 때문에 동결건조 주사제 제제는 의약품 파이프라인의 중요한 부분이 되고 있습니다. 또한, 세계 규제 승인 증가와 동결건조 공정의 기술적 진보로 시장 침투가 현저하게 높아지고 있습니다. 입원 및 외래 치료 모두에서 생물학적 제제와 주사 요법으로의 전환으로 동결건조 주사제 부문에서는 생산 능력, 물류 인프라 및 임상 응용 분야의 급속한 발전을 볼 수 있습니다.

내구성이 있고 안정성이 높은 제제에 대한 요구가 증가함에 따라, 제약 회사가 확대하는 주사제에 동결 건조를 채택하는 것을 뒷받침하고 있습니다. 콜드체인 유통 강화, 단일 용량 패키징, 재구성 효율 개선 등의 혁신으로 세계 의료 시스템 전반에 걸쳐 제품의 신뢰성이 향상되었습니다. 동결건조된 제형은 안정성과 무균성이 중요한 질병의 치료에서 기세를 늘리고 있습니다. 이러한 약물은 일반적으로 희석제와 혼합한 후에 투여되기 때문에 의료 서비스 제산업체는 투여 정확도를 관리하고 제품의 유용성을 확대할 수 있습니다. 보존기간이 길고 신뢰성이 높은 제제를 입수할 수 있기 때문에 특히 인프라가 제한되어 고도의료에의 액세스가 확대되고 있는 지역에서는 동결건조 의약품이 바람직한 옵션이 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 3,569억 달러 |

| 예측 금액 | 1조 3,100억 달러 |

| CAGR | 14.1% |

2024년, 항악성 종양제 부문은 1,395억 달러의 점유율을 얻었지만, 이는 종양에 특화된 생물학적 제제 및 세포독성 화합물에 대한 수요의 급증을 반영합니다. 동결건조 주사제는 이러한 치료에 특히 적합하며, 오염 및 취급과 관련된 위험을 최소화하면서 안정성 향상과 보존 기간 연장을 실현합니다. 이러한 특성은 정확한 투여량, 무균성, 장기 보존이 필수적인 암 치료에 매우 중요합니다. 규제 당국이 암 영역에서 동결건조 제제를 승인하는 경우가 늘고 있는 점에서 제약회사는 항악성 종양성 주사제, 특히 고가치 제제로 효능과 순도의 일탈의 여지가 제한되는 제제를 중심으로 개발 파이프라인을 우선하고 있습니다.

암 영역은 2024년에 28.7%의 톱 점유율을 차지했습니다. 이 분야의 우위성은 세계의 암 이환율 증가와 장기간 보관 및 수송을 통해 치료효과를 유지하는 안정된 주사요법의 필요성 때문입니다. 세계의 건강 관리 시스템은 보다 견고한 약물 전달 솔루션에 대한 투자를 추진하고 있으며, 동결건조 주사제는 비용 효율적이고 장기적인 솔루션입니다. 의약품 개발 기업은 암 치료에 대한 수요 증가에 대응하기 위해 전달 방법의 개선, 약제 낭비의 삭감, 동결 건조에 의한 제품 수명의 강화에 중점적으로 임하고 있습니다.

북미 시장은 2024년에 47%를 차지하며 이 지역의 선진적인 의약품 사정과 만성 질환 환자의 집중에 지지되었습니다. 이 지역의 이점은 강력한 R&D 능력, 동결건조 주사제의 빈번한 FDA 승인, 병원 및 외래의 광범위한 채용을 지원하는 성숙한 의료 제공 시스템에 기인합니다. 종양학, 자가면역질환 치료제, 생물제제에 대한 지속적인 투자와 보존 기간이 연장된 주사제의 수용 확대는 세계의 동결건조 주사제 시장에서 이 지역의 아성을 지지하고 있습니다.

동결건조 주사제 업계의 기업은 시장에서 리더십을 확보하기 위해 대용량 동결건조장치와 엄격한 세계 규제 기준을 충족하는 최첨단 제조 라인에 대한 투자를 늘리고 있습니다. 많은 기업들은 수탁 제조 서비스를 확대하고, 콜드체인 물류를 개선하고, 다운타임과 제조 비용을 줄이기 위해 자동화를 통합하고 있습니다. 혁신적인 생물학적 화합물에 대한 액세스를 얻고 제품 포트폴리오를 확대하기 위해 전략적 공동 연구 및 라이선스 계약이 일반적으로 사용됩니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성 질환 및 감염증의 만연

- 약물전달 시스템의 기술적 진보

- 생물제제와 복합분자 수요가 증가

- 업계의 잠재적 위험 및 과제

- 높은 생산 비용과 설비 비용

- 규제와 품질 컴플라이언스의 과제

- 시장 기회

- 맞춤형 의료와 정밀의료

- 계약조사제조서비스(CRAMS) 확대

- 성장 촉진요인

- 성장 가능성 분석

- 기술의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 분석

- 파이프라인과 R&D 투자분석

- 특허 정세 분석

- 상위 시장 분석

- 규제 상황

- 향후 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

제5장 시장 추계·예측 : 약제 유형별(2021-2034년)

- 주요 동향

- 감염 방지

- 항종양

- 항응고제

- 호르몬

- 항부정맥제

- 양성자 펌프 억제제

- 마취제

- 기타 약제 유형

제6장 시장 추계·예측 : 적응증별(2021-2034년)

- 주요 동향

- 자가면역질환

- 호흡기 질환

- 위장 장애

- 종양학

- 심혈관 질환

- 감염증

- 호르몬 장애

- 대사 장애

- 생식 건강

- 기타 적응증

제7장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 프리필드 희석액 주사기

- 다단계 디바이스

제8장 시장 추계·예측 : 포장별(2021-2034년)

- 주요 동향

- 바이알

- 카트리지

- 프리필드 디바이스

제9장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 전문 클리닉

- 기타 용도

제10장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 일본

- 중국

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Akums Drugs and Pharmaceuticals

- Aurobindo Pharma

- Bora Pharmaceuticals

- Bristol Myers Squibb

- Cipla

- F. Hoffmann-La Roche

- Fareva

- Fresenius

- Gilead Sciences

- Gufic Group

- Johnson &Johnson

- Meiji Group

- Merck

- Novo Nordisk

- Pfizer

- Sanofi

- Takeda Pharmaceuticals

- Vetter Pharma

- Zydus

The Global Lyophilized Injectable Drugs Market was valued at USD 356.9 billion in 2024 and is estimated to grow at a CAGR of 14.1% to reach USD 1.31 trillion by 2034. Rising incidences of chronic health conditions, including cancer and infectious diseases, continue to escalate demand for stable and long-acting therapeutics. The need for extended shelf life and improved drug efficacy has made freeze-dried injectable formulations an essential part of the pharmaceutical pipeline. Additionally, the increase in global regulatory approvals and technological advancements in lyophilization processes is significantly enhancing market penetration. With a shift toward biologics and injectable therapies in both inpatient and outpatient care, the lyophilized injectables sector is seeing rapid development in manufacturing capabilities, logistics infrastructure, and clinical applications.

The rising need for durable and highly stable drug formulations is pushing pharmaceutical companies to adopt lyophilization for an expanding range of injectable drugs. Innovations such as enhanced cold-chain distribution, single-dose packaging, and improvements in reconstitution efficiency are strengthening product reliability across global healthcare systems. Lyophilized formulations are gaining momentum in the treatment of diseases where stability and sterility are critical. These drugs are typically administered after mixing with a diluent, allowing healthcare providers to manage dosing accuracy and extend product usability. The availability of reliable formulations with longer shelf lives makes lyophilized drugs a preferred choice, particularly in regions with limited infrastructure and growing access to advanced medical care.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $356.9 Billion |

| Forecast Value | $1.31 Trillion |

| CAGR | 14.1% |

In 2024, the anti-neoplastic agents segment captured a USD 139.5 billion share, reflecting the surging demand for oncology-focused biologics and cytotoxic compounds. Lyophilized injectable drugs are particularly well-suited for these treatments, offering improved stability and longer shelf life while minimizing the risks associated with contamination and handling. These properties are critical in cancer care, where precise dosage, sterility, and long-term storage are vital. With regulatory bodies increasingly approving freeze-dried formulations in oncology, pharmaceutical firms are prioritizing development pipelines around anti-neoplastic injectables, particularly those with high-value formulations and limited room for deviation in potency or purity.

The oncology segment held the leading share of 28.7% in 2024. Its dominance is driven by the growing global incidence of cancer and the necessity for stable injectable therapies that maintain therapeutic effectiveness through extended storage and transport. Healthcare systems worldwide are investing in more robust drug delivery solutions, and lyophilized injectables provide a cost-effective, long-term answer. Pharmaceutical developers are focusing heavily on refining delivery methods, reducing drug wastage, and enhancing product lifespan through lyophilization to meet the growing demand for cancer treatments.

North America Lyophilized Injectable Drugs Market held 47% in 2024, underpinned by the region's advanced pharmaceutical landscape and high concentration of chronic disease cases. The region's dominance also stems from strong R&D capabilities, frequent FDA approvals for freeze-dried injectables, and a mature healthcare delivery system that supports wide adoption across hospital and ambulatory settings. Continued investment in oncology, autoimmune disease therapies, and biologics, combined with growing acceptance of injectable drugs with extended shelf lives, continues to support the region's stronghold in the global lyophilized injectable drugs market.

Prominent market participants contributing to industry growth include Cipla, Novo Nordisk, Akums Drugs and Pharmaceuticals, Merck, Aurobindo Pharma, Pfizer, Gilead Sciences, Sanofi, Johnson & Johnson, Takeda Pharmaceuticals, Vetter Pharma, Zydus, Meiji Group, Gufic Group, Fareva, Bristol Myers Squibb, Fresenius, F. Hoffmann-La Roche, and Bora Pharmaceuticals. To secure their market leadership, companies in the lyophilized injectable drugs industry are increasingly investing in high-capacity freeze-drying equipment and state-of-the-art manufacturing lines that meet stringent global regulatory standards. Many firms are expanding their contract manufacturing services, improving cold chain logistics, and integrating automation to reduce downtime and production costs. Strategic collaborations and licensing agreements are commonly used to gain access to innovative biologic compounds and expand product portfolios.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Drug type

- 2.2.3 Indication

- 2.2.4 Application

- 2.2.5 Age group

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of chronic and infectious diseases

- 3.2.1.2 Technological advancements in drug delivery systems

- 3.2.1.3 Rising demand for biologics and complex molecules

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production and equipment costs

- 3.2.2.2 Regulatory and quality compliance challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Personalized and precision medicine

- 3.2.3.2 Expansion of contract research and manufacturing services (CRAMS)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing analysis

- 3.6 Pipeline and R&D investment analysis

- 3.7 Patent landscape analysis

- 3.8 Parent market analysis

- 3.9 Regulatory landscape

- 3.9.1 North America

- 3.9.2 Europe

- 3.9.3 Asia Pacific

- 3.9.4 Latin America

- 3.9.5 Middle East and Africa

- 3.10 Future market trends

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Anti-infective

- 5.3 Anti-neoplastic

- 5.4 Anticoagulant

- 5.5 Hormones

- 5.6 Antiarrhythmic

- 5.7 Proton pump inhibitors

- 5.8 Anesthetics

- 5.9 Other drug types

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Autoimmune diseases

- 6.3 Respiratory diseases

- 6.4 Gastrointestinal disorders

- 6.5 Oncology

- 6.6 Cardiovascular diseases

- 6.7 Infectious diseases

- 6.8 Hormonal disorders

- 6.9 Metabolic disorders

- 6.10 Reproductive health

- 6.11 Other indications

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Prefilled diluent syringes

- 7.3 Multi-step devices

Chapter 8 Market Estimates and Forecast, By Packaging, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Vials

- 8.3 Cartridges

- 8.4 Prefilled devices

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Specialty clinics

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Akums Drugs and Pharmaceuticals

- 11.2 Aurobindo Pharma

- 11.3 Bora Pharmaceuticals

- 11.4 Bristol Myers Squibb

- 11.5 Cipla

- 11.6 F. Hoffmann-La Roche

- 11.7 Fareva

- 11.8 Fresenius

- 11.9 Gilead Sciences

- 11.10 Gufic Group

- 11.11 Johnson & Johnson

- 11.12 Meiji Group

- 11.13 Merck

- 11.14 Novo Nordisk

- 11.15 Pfizer

- 11.16 Sanofi

- 11.17 Takeda Pharmaceuticals

- 11.18 Vetter Pharma

- 11.19 Zydus