|

시장보고서

상품코드

1801797

유제품 및 대두 식품 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Dairy and Soy Food Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

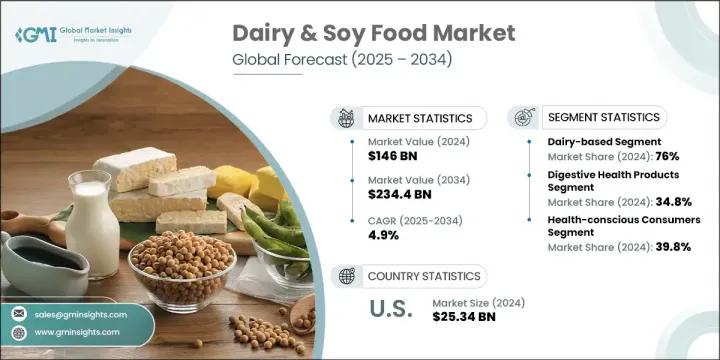

세계의 유제품 및 대두 식품 시장의 2024년 시장 규모는 1,460억 달러에 달하고, CAGR 4.9%로 성장할 전망이며 2034년에는 2,344억 달러에 이를 것으로 추정됩니다.

이 시장은 우유, 요구르트, 치즈와 같은 유제품부터 식물성 음료 및 대두 대체품에 이르기까지 광범위한 제품을 아우릅니다. 이러한 성장의 주요 촉진요인은 소비자들의 건강과 웰빙에 대한 관심 증가입니다. 첨가물을 최소화하고 기능적 이점을 더한 영양가 높은 제품에 대한 수요가 증가하고 있습니다. 유당 불내증이 흔해짐에 따라 많은 소비자들이 전통 유제품과 동일한 맛, 질감, 영양가를 제공하는 식물성 대체품으로 눈을 돌리고 있습니다.

식물성 및 비건 식단의 부상은 이 분야에서 상당한 혁신을 촉발했으며, 기업들은 비건, 플렉시테리언, 환경 의식이 높은 소비자를 대상으로 한 새로운 유형의 요구르트, 식물성 음료, 강화 식품을 포함하도록 포트폴리오를 다각화하고 있습니다. 선진국의 고령화 인구 역시 강화 유제품 및 대두 식품, 특히 뼈 건강, 소화 기능, 전반적인 활력을 지원하기 위해 단백질, 비타민, 프로바이오틱스로 강화된 제품에 대한 수요를 촉진하고 있습니다. 한편, 전자상거래의 급속한 성장은 제품 접근성을 개선하여 브랜드가 더 많은 소비자에게 도달하고 더 다양한 제품을 제공할 수 있게 하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 1,460억 달러 |

| 예측 금액 | 2,344억 달러 |

| CAGR | 4.9% |

2024년 기준 유제품 기반 건강식품 부문이 76%로 최대 점유율을 기록했으며, 2034년까지 5.3%의 성장률을 유지할 것으로 전망됩니다. 장 건강, 면역력, 뼈 강도에 주목하는 건강 의식이 높은 소비자를 대상으로 한 이 제품들은 지방과 당분 함량을 줄이면서 식이 제한이 있는 개인의 접근성을 높이기 위한 혁신을 통해 개발되고 있습니다.

소화 건강 제품 부문은 2024년 시장 점유율 34.8%를 차지했으며, 2034년까지 5.5%의 성장률이 예상됩니다. 이러한 인상적인 성장은 영양적 및 기능적 이점을 동시에 제공하는 제품을 찾는 소비자가 증가함에 따라 장 건강과 면역 체계 강화에 대한 소비자 관심이 높아진 데 주로 기인합니다. 복부 팽만감과 소화불량부터 과민성 대장 증후군(IBS)과 같은 복잡한 질환에 이르기까지 전 세계적으로 소화 건강 문제가 더욱 보편화됨에 따라, 소비자들은 소화 기능 개선과 전반적인 장내 미생물 균형 조화를 촉진하는 식품 및 보충제로 눈을 돌리고 있습니다.

미국의 유제품 및 대두 식품 시장 규모는 2024년에 253억 4,000만 달러에 달했습니다. 안전성을 최우선으로 하는 브랜드에 대한 소비자 신뢰, 영양 성분 표기의 투명성, 편리한 제품 형태 등이 주도하며 2034년까지 연평균 성장률(CAGR) 6.4%로 성장할 전망입니다. 유기농, 글루텐 프리, 식물성 제품의 인기가 높아지면서 미국 시장이 더욱 가속화되고 있습니다.

세계의 유제품 및 대두 식품 시장의 주요 기업은 Danone SA, Unilever PLC, Lactalis Group, Fontera Co-operative Group, Hain Celestial Group, Inc., Friesland Campina, General Mills, Inc., Dean Foods Company, Arla Foods amba, Silk(Danone), Nestle SA, The Kraft Foods(Danone), Kellogg Company 등이 있습니다. 경쟁이 치열한 유제품 및 대두 식품 부문에서 입지를 공고히 하기 위해 기업들은 다양한 전략을 시행해 왔습니다. 여기에는 저당, 고단백, 무유당 옵션 제공 등 변화하는 소비자 선호도를 충족시키기 위한 지속적인 제품 개량이 포함됩니다. 많은 기업들은 비건 및 플렉시테리언 선택지에 대한 증가하는 수요를 활용하여 식물성 대체품을 포함하도록 제품 라인을 확장했습니다. 파트너십, 인수합병, 생산 공정의 혁신 또한 포트폴리오를 다각화하고 제품 접근성을 개선하기 위한 핵심 전략이었습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 건강 및 웰빙 의식 증대

- 유당 불내증 유병률 증가

- 식물성 식단 채택 및 비건주의 성장

- 단백질 강화 및 영양 개선 수요

- 업계의 잠재적 위험 및 과제

- 기존 유제품 산업과의 경쟁

- 특수 건강 제품의 가격 프리미엄

- 시장 기회

- 신흥 시장의 건강 의식 성장

- 기능성 식품 및 기능성 의약품 통합

- 맞춤형 영양 및 개인화

- 전자상거래 및 소비자 직접 판매 성장

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 카테고리별

- 장래 시장 동향

- 기술과 혁신 미래

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가만 제공)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국의 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 상품 카테고리별(2021-2034년)

- 주요 동향

- 유제품 기반 건강 식품

- 프로바이오틱스 유제품

- 단백질 강화 유제품

- 기능성 유제품

- 콩 기반 식품

- 기존 콩 식품

- 두유와 음료

- 콩 단백질 제품

- 복합 및 하이브리드 제품

- 유제품-콩 혼합 제품

- 멀티 단백질 배합

- 기능성 식품 조합

- 특수 영양 제품

제6장 시장 추계 및 예측 : 건강 효과별(2021-2034년)

- 주요 동향

- 소화 건강 제품

- 프로바이오틱스 및 프리바이오틱스 식품

- 소화효소 강화

- 장 건강 지원 제품

- 뼈와 관절 건강

- 칼슘 강화 제품

- 비타민 D 강화 식품

- 뼈 건강 지원

- 심장 건강 제품

- 콜레스테롤 관리 식품

- 오메가3 강화제품

- 심장 건강용 조제

- 단백질과 근육의 건강

- 고단백제품

- 근육 회복 처방

- 스포츠 영양 통합

- 체중 관리

- 저칼로리, 저지방

- 포만감 강화제품

- 대사 지원 제형

제7장 시장 추계 및 예측 : 소비자 부문별(2021-2034년)

- 주요 동향

- 건강 지향의 소비자

- 식사 제한 부문

- 연령별 부문

- 아동 및 청소년 영양

- 성인 건강과 웰빙

- 고령자 영양과 케어

- 라이프 스타일 기반 부문

- 바쁜 직장인

- 유기농 및 천연 선호

- 프리미엄 및 수제 제품 소비자

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Arla Foods amba

- Danone SA

- Dean Foods Company

- Fonterra Co-operative Group

- FrieslandCampina

- General Mills, Inc.

- Hain Celestial Group, Inc.

- Kellogg Company

- Lactalis Group

- Nestle SA

- Silk(Danone)

- The Kraft Heinz Company

- Unilever PLC

- WhiteWave Foods(Danone)

- Yakult Honsha Co., Ltd.

The Global Dairy & Soy Food Market was valued at USD 146 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 234.4 billion by 2034. This market spans a broad range of products, including dairy items like milk, yogurt, and cheese, as well as plant-based beverages and soy alternatives. A key driver behind this growth is the increasing focus on health and wellness among consumers. There is a growing demand for nutritious products with minimal additives and more functional benefits. As lactose intolerance becomes more common, many consumers are turning to plant-based options that offer the same taste, texture, and nutritional value as traditional dairy products.

The rise of plant-based and vegan diets has sparked significant innovation in this space, with companies diversifying their portfolios to include new types of yogurt, plant-based beverages, and fortified goods aimed at vegans, flexitarians, and environmentally conscious shoppers. The aging population in developed countries is also fueling demand for fortified dairy and soy foods, particularly those enriched with proteins, vitamins, and probiotics to support bone health, digestion, and overall vitality. Meanwhile, the rapid growth of e-commerce is improving product accessibility, allowing brands to reach more consumers and offer a wider variety of products.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $146 Billion |

| Forecast Value | $234.4 Billion |

| CAGR | 4.9% |

In 2024, dairy-based health foods segment held the largest share at 76% and is expected to maintain a growth rate of 5.3% through 2034. These products, which appeal to health-conscious consumers focused on gut health, immunity, and bone strength, are being developed with innovations aimed at reducing fat and sugar content while increasing accessibility for individuals with dietary restrictions.

The digestive health products segment captured a significant 34.8% share of the market in 2024, with an anticipated growth rate of 5.5% through to 2034. This impressive expansion is largely driven by an increasing consumer focus on gut health and immune system enhancement, as more individuals seek products that offer both nutritional and functional benefits. As digestive health issues become more prevalent globally, from bloating and indigestion to more complex conditions like IBS, consumers are turning to foods and supplements that promote better digestion and overall gut flora balance.

United States Dairy and Soy Food Market generated USD 25.34 billion in 2024. The country's market is expected to grow at a CAGR of 6.4% by 2034, driven by consumer trust in brands that prioritize safety, transparency in nutritional labeling, and convenient product formats. The increasing popularity of organic, gluten-free, and plant-based products has further propelled the U.S. market forward.

Leading companies in the Global Dairy and Soy Food Market include Danone S.A., Unilever PLC, Lactalis Group, Fonterra Co-operative Group, Hain Celestial Group, Inc., FrieslandCampina, General Mills, Inc., Dean Foods Company, Arla Foods amba, Silk (Danone), Nestle S.A., The Kraft Heinz Company, Yakult Honsha Co., Ltd., WhiteWave Foods (Danone), and Kellogg Company. To solidify their position in the competitive dairy and soy food sector, companies have implemented various strategies. These include continuous product reformulations to meet evolving consumer preferences, such as offering lower sugar, high-protein, and lactose-free options. Many companies have expanded their product lines to include plant-based alternatives, tapping into the growing demand for vegan and flexitarian choices. Partnerships, acquisitions, and innovation in production processes have also been key strategies to diversify portfolios and improve product accessibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product category

- 2.2.3 Health benefit

- 2.2.4 Consumer segment

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing health and wellness consciousness

- 3.2.1.2 Rising prevalence of lactose intolerance

- 3.2.1.3 Plant-based diet adoption and veganism growth

- 3.2.1.4 Protein enrichment and nutritional enhancement demands

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Traditional dairy industry competition

- 3.2.2.2 Price premium for specialty health products

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging market health awareness growth

- 3.2.3.2 Functional food and nutraceutical integration

- 3.2.3.3 Personalized nutrition and customization

- 3.2.3.4 E-commerce and direct-to-consumer growth

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product category

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Category, 2021-2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Dairy-based health foods

- 5.2.1 Probiotic dairy products

- 5.2.2 Protein-enriched dairy

- 5.2.3 Functional dairy products

- 5.3 Soy-based food products

- 5.3.1 Traditional soy foods

- 5.3.2 Soy milk and beverages

- 5.3.3 Soy protein products

- 5.4 Combination and hybrid products

- 5.4.1 Dairy-soy blend products

- 5.4.2 Multi-protein formulations

- 5.4.3 Functional food combinations

- 5.4.4 Specialty nutritional products

Chapter 6 Market Estimates and Forecast, By Health Benefit, 2021-2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Digestive health products

- 6.2.1 Probiotic and prebiotic foods

- 6.2.2 Digestive enzyme enhanced

- 6.2.3 Gut health support products

- 6.3 Bone and joint health

- 6.3.1 Calcium-enriched products

- 6.3.2 Vitamin D fortified foods

- 6.3.3 Bone health support formulations

- 6.4 Heart health products

- 6.4.1 Cholesterol management foods

- 6.4.2 Omega-3 enhanced products

- 6.4.3 Heart-healthy formulations

- 6.5 Protein and muscle health

- 6.5.1 High-protein products

- 6.5.2 Muscle recovery formulations

- 6.5.3 Sports nutrition integration

- 6.6 Weight management

- 6.6.1 Low-calorie and reduced-fat

- 6.6.2 Satiety-enhancing products

- 6.6.3 Metabolic support formulations

Chapter 7 Market Estimates and Forecast, By Consumer Segment, 2021-2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Health-conscious consumers

- 7.3 Dietary restriction segments

- 7.4 Age-based segments

- 7.4.1 Children and adolescent nutrition

- 7.4.2 Adult health and wellness

- 7.4.3 Senior nutrition and care

- 7.5 Lifestyle-based segments

- 7.5.1 Busy professional

- 7.5.2 Organic and natural preference

- 7.5.3 Premium and artisanal consumers

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Arla Foods amba

- 9.2 Danone S.A.

- 9.3 Dean Foods Company

- 9.4 Fonterra Co-operative Group

- 9.5 FrieslandCampina

- 9.6 General Mills, Inc.

- 9.7 Hain Celestial Group, Inc.

- 9.8 Kellogg Company

- 9.9 Lactalis Group

- 9.10 Nestle S.A.

- 9.11 Silk (Danone)

- 9.12 The Kraft Heinz Company

- 9.13 Unilever PLC

- 9.14 WhiteWave Foods (Danone)

- 9.15 Yakult Honsha Co., Ltd.

(주말 및 공휴일 제외)