|

시장보고서

상품코드

1801807

BREEAM 준수 자재 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)BREEAM-Compliant Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

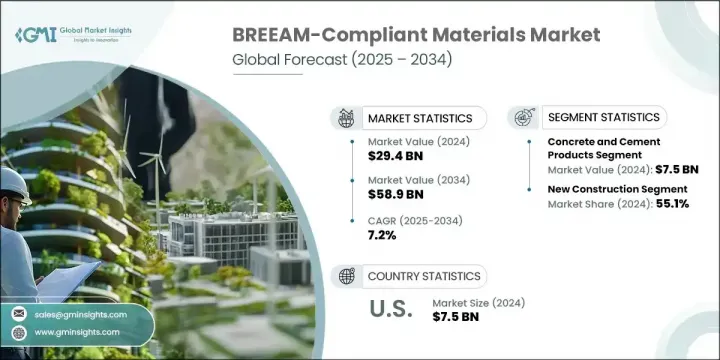

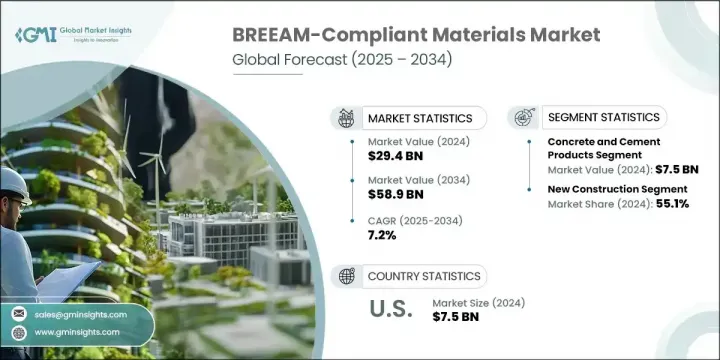

세계의 BREEAM 준수 자재 시장은 2024년에 294억 달러로 평가되었으며 CAGR 7.2%로 성장할 전망이며 2034년까지는 589억 달러에 이를 것으로 추정됩니다.

이러한 자재들은 BREEAM의 지속가능성 요건에 부합하도록 설계되어, 원자재 조달 및 제조부터 수명 종료 시 폐기에 이르기까지 전 생애 주기 동안 환경에 미치는 영향을 최소화합니다. 환경 의식 고조, 규제 의무 강화, 기업의 지속가능성 약속 강화 추세가 이러한 친환경 건설 자재 수요를 상당하게 촉진하고 있습니다. 산업계와 정부가 탄소 발자국 감축을 위해 노력함에 따라 BREEAM 인증 자재는 최근 건축 관행의 필수 요소로 자리매김하고 있습니다.

환경 문제가 심화되면서 기업과 정책 입안자들은 건설 분야에 친환경 솔루션을 도입하기 위해 협력하며, 이러한 지속가능한 대안의 채택을 가속화하고 있습니다. 특히 환경 정책이 엄격하고 친환경 건설에 대한 인센티브가 큰 지역에서 강력한 규제 지원으로 시장이 지속적으로 성장하고 있습니다. 지속 가능한 건설이 동향에서 표준으로 진화함에 따라 BREEAM 준수 자재의 성장세는 빠르게 증가하며 친환경 인프라 구축에서의 역할을 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 294억 달러 |

| 예측 금액 | 589억 달러 |

| CAGR | 7.2% |

콘크리트 및 시멘트 기반 재료는 기초 및 구조 건설에서 핵심적인 역할을 수행하여 2024년 75억 달러의 매출을 기록하며 BREEAM 준수 부문에서 선두를 달렸습니다. 이러한 제품들은 비용 효율성과 신축 구조물 및 친환경 개조 모두에 대한 적응성 덕분에 널리 채택되고 있습니다. 도시화가 확대되고 인프라 프로젝트가 증가함에 따라, 특히 지속 가능한 개발에 주력하는 지역에서 저탄소 대안에 대한 수요가 가속화되고 있습니다. 제조업체들은 진화하는 친환경 건축 기대치를 충족시키기 위해 이러한 재료의 환경 친화적 버전을 점점 더 우선시하고 있습니다.

신규 건설 프로젝트 부문은 2024년 55.1%의 점유율을 차지하며 최대 용도 부문으로 부상했습니다. 높은 환경 성능 기준을 충족하는 프로젝트 증가로 신축 건물이 시장 성장의 핵심 촉진 요인이 되었습니다. 그럼에도 개발사와 소유주가 기존 건물을 최신 에너지 효율 기준으로 업그레이드하려는 움직임에 따라 리모델링 및 리노베이션 수요도 증가하고 있습니다. 특히 상업용 부동산 분야에서 인테리어 및 내부 용도도 증가세에 있는데, 이는 디자인 전문가들이 호텔, 소매점, 사무실 환경에 지속 가능한 솔루션을 모색하기 때문입니다.

미국의 BREEAM 준수 자재 시장은 2024년에 75억 달러를 창출하고 지속 가능한 건설에 대한 강력한 관심과 친환경 재료 사용을 장려하는 규제 체계 덕분에 주요 업체로 자리매김했습니다. 친환경 건축 관행의 우선순위가 높아짐에 따라 상업, 주거, 기관 프로젝트 전반에서 BREEAM 인증 제품 채택이 증가하고 있습니다. 캐나다 역시 적극적인 정부 정책과 학술 기관 및 건설 산업 간의 협력 노력 덕분에 가속화된 성장을 목격하고 있으며, 이는 주요 부문 전반에 걸쳐 지속가능성을 더욱 촉진하고 있습니다.

세계의 BREEAM 준수 자재 시장을 형성하는 유명한 기업으로는 EcoCocon, Kingspan, Holcim, Owens Corning, Amorim Cork, Saint-Gobain, Concrete Centre, BRE Global Ltd. 등이 있습니다. 이들 기업은 지속가능성 기준을 설정하고 혁신적인 건설 자재를 공급하는 데 핵심적인 역할을 하고 있습니다. 선도 기업들은 BREEAM 준수 재료 시장에서의 입지를 강화하기 위해 탄소 배출량 저감, 에너지 효율 증대, 재활용성 개선에 초점을 맞춘 제품 혁신에 상당한 투자를 하고 있습니다. 많은 기업들이 기존 제품 라인을 재설계하여 BREEAM 기준을 충족하거나 초과하도록 하고 있으며, 구조용 및 인테리어 용도용으로 맞춤화된 새로운 친환경 솔루션을 도입하고 있습니다. 지속가능성 인증 기관과의 파트너십 및 건설 가치 사슬 내 전략적 협력은 브랜드가 신뢰와 가시성을 확보하는 데 도움이 되고 있습니다. 기업들은 또한 디지털 플랫폼을 활용해 고객에게 BREEAM 준수 제품의 이점을 알리는 동시에 증가하는 수요를 충족시키기 위해 제조 역량을 확대되고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크 및 도전과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 미래

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 소재별

- 장래 시장 동향

- 기술과 혁신 미래

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)

(참고 : 무역 통계는 주요 국가에서만 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국의 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 자재별(2021-2034년)

- 주요 동향

- 콘크리트 시멘트 제품

- 레디믹스 콘크리트

- 프리캐스트 콘크리트 요소

- 시멘트 대체품과 혼합

- 철강 및 금속 제품

- 구조용 강철

- 철근

- 금속 클래딩과 지붕

- 재활용 금속 함유 제품

- 단열재

- 목재 섬유 단열재

- 코르크 기반 단열재

- 대마 및 바이오 단열재

- 재활용 소재를 사용 단열재

- 목재 및 목재 제품

- 인증된 지속 가능한 목재

- 공학 목재 제품

- 재생목재 및 재활용목재

- 대나무와 대체 목재

- 바닥재 및 마감재

- 지속 가능한 바닥재 솔루션

- 낮은 VOC 페인트 및 코팅

- 재활용 컨텐츠 타일과 표면

- 바이오 기반의 마감재

- 지붕재 및 외벽재

- 녹색 지붕 시스템

- 고성능 유리

- 지속 가능한 외장재

- 방수 장벽 시스템

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 신축

- 상업

- 주거

- 산업

- 인프라 프로젝트

- 리모델링 및 개조

- 역사적 건축물 수복

- 에너지 효율 향상

- 지속 가능한 리노베이션 프로젝트

- 건물의 성능 향상

- 인테리어 및 실내 용도

- 사무실 시설

- 소매 공간

- 의료

- 교육

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 상업용 부동산

- 오피스 빌딩

- 소매점과 쇼핑센터

- 호텔과 접객

- 복합 개발

- 주택 부문

- 단독 주택

- 집합 주택

- 저렴한 주택 프로젝트

- 고급 주택 개발

- 공공시설

- 의료시설

- 교육기관

- 정부청사

- 문화 및 커뮤니티 센터

- 산업과 인프라

- 제조 시설

- 창고와 배송 센터

- 교통 인프라

- 유틸리티 및 에너지 프로젝트

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Amorim Cork

- BRE Global Ltd

- Concrete Centre

- EcoCocon

- Holcim

- Kingspan

- Owens Corning

- Saint-Gobain

The Global BREEAM-Compliant Materials Market was valued at USD 29.4 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 58.9 billion by 2034. These materials are designed to align with BREEAM's sustainability requirements, ensuring minimal environmental impact throughout their lifecycle-from sourcing and manufacturing to end-of-life disposal. Growing environmental awareness, increased regulatory obligations, and the push toward stronger corporate sustainability commitments are significantly fueling demand for these eco-conscious construction products. As industries and governments strive to reduce their carbon footprints, BREEAM-certified materials are becoming an essential component in modern building practices.

With environmental challenges intensifying, companies and policymakers are working in unison to implement green solutions in construction, accelerating the adoption of these sustainable alternatives. The market is seeing continuous growth due to strong regulatory support, especially in regions where environmental policies are more rigorous and green construction is heavily incentivized. As sustainable construction evolves from a trend into a standard, the momentum behind BREEAM-compliant materials continues to grow rapidly, reinforcing their role in creating eco-friendly infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $29.4 Billion |

| Forecast Value | $58.9 Billion |

| CAGR | 7.2% |

The concrete and cement-based materials generated USD 7.5 billion in 2024, leading the BREEAM-compliant segment due to their pivotal role in foundational and structural construction. These products are widely adopted thanks to their cost-efficiency and adaptability in both newly built structures and eco-focused retrofits. As urbanization expands and infrastructure projects increase, especially in regions focused on sustainable development, demand for low-carbon alternatives is gaining pace. Manufacturers are increasingly prioritizing environmentally responsible versions of these materials to meet evolving green building expectations.

The new construction projects segment held 55.1% share in 2024, emerging as the top application segment. The rise in projects committed to meeting high environmental performance standards has made new builds a central driver of market growth. Nonetheless, retrofitting and refurbishing older buildings are gaining traction as developers and owners look to upgrade outdated structures in line with current energy efficiency benchmarks. Fit outs and interior applications are also on the rise, particularly in the commercial real estate space, as design professionals seek sustainable solutions for hospitality, retail, and office environments.

U.S. BREEAM-Compliant Materials Market generated USD 7.5 billion in 2024, positioning itself as a major player due to a strong focus on sustainable construction and regulatory frameworks that encourage the use of green materials. The increasing prioritization of eco-friendly building practices is boosting the adoption of BREEAM-certified products across commercial, residential, and institutional projects. Canada is also witnessing accelerated growth thanks to proactive governmental policies and collaborative efforts between academic institutions and the construction industry, further promoting sustainability across key sectors.

Prominent players shaping the Global BREEAM-Compliant Materials Market include EcoCocon, Kingspan, Holcim, Owens Corning, Amorim Cork, Saint-Gobain, Concrete Centre, and BRE Global Ltd. These companies are instrumental in setting sustainability benchmarks and delivering innovative construction materials. To enhance their presence in the BREEAM-compliant materials market, leading companies are investing significantly in product innovation focused on lowering carbon emissions, boosting energy efficiency, and improving recyclability. Many are reengineering existing product lines to meet or exceed BREEAM standards and are introducing new eco-conscious solutions tailored to both structural and interior applications. Partnerships with sustainability certifying bodies and strategic collaborations within the construction value chain are helping brands secure trust and visibility. Companies are also leveraging digital platforms to educate customers on the benefits of BREEAM-compliant products while expanding manufacturing capabilities to meet growing demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Material trends

- 2.2.2 Application trends

- 2.2.3 End use sector trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By material

- 3.9 Future market trends

- 3.10 Technology and Innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent Landscape

- 3.12 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Concrete and Cement Products

- 5.2.1 Ready-Mix Concrete

- 5.2.2 Precast Concrete Elements

- 5.2.3 Cement Alternatives and Blends

- 5.3 Steel and Metal Products

- 5.3.1 Structural Steel

- 5.3.2 Reinforcing Steel

- 5.3.3 Metal Cladding and Roofing

- 5.3.4 Recycled Metal Content Products

- 5.4 Insulation Materials

- 5.4.1 Wood Fiber Insulation

- 5.4.2 Cork-based Insulation

- 5.4.3 Hemp and Bio-based Insulation

- 5.4.4 Recycled Content Insulation

- 5.5 Timber and Wood Products

- 5.5.1 Certified Sustainable Timber

- 5.5.2 Engineered Wood Products

- 5.5.3 Reclaimed and Recycled Wood

- 5.5.4 Bamboo and Alternative Wood Materials

- 5.6 Flooring and Finishing Materials

- 5.6.1 Sustainable Flooring Solutions

- 5.6.2 Low-VOC Paints and Coatings

- 5.6.3 Recycled Content Tiles and Surfaces

- 5.6.4 Bio-based Finishing Materials

- 5.7 Roofing and Envelope Materials

- 5.7.1 Green Roofing Systems

- 5.7.2 High-Performance Glazing

- 5.7.3 Sustainable Cladding Materials

- 5.7.4 Weather Barrier Systems

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 New construction

- 6.2.1 Commercial buildings

- 6.2.2 Residential buildings

- 6.2.3 Industrial facilities

- 6.2.4 Infrastructure projects

- 6.3 Refurbishment and retrofit

- 6.3.1 Heritage building restoration

- 6.3.2 Energy efficiency upgrades

- 6.3.3 Sustainable renovation projects

- 6.3.4 Building performance improvements

- 6.4 Fit-out and interior applications

- 6.4.1 Office fit-outs

- 6.4.2 Retail spaces

- 6.4.3 Healthcare facilities

- 6.4.4 Educational buildings

Chapter 7 Market Estimates and Forecast, By End Use Sector, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Commercial real estate

- 7.2.1 Office buildings

- 7.2.2 Retail and shopping centers

- 7.2.3 Hotels and hospitality

- 7.2.4 Mixed-use developments

- 7.3 Residential sector

- 7.3.1 Single-family homes

- 7.3.2 Multi-family housing

- 7.3.3 Affordable housing projects

- 7.3.4 Luxury residential developments

- 7.4 Institutional buildings

- 7.4.1 Healthcare facilities

- 7.4.2 Educational institutions

- 7.4.3 Government buildings

- 7.4.4 Cultural and community centers

- 7.5 Industrial and infrastructure

- 7.5.1 Manufacturing facilities

- 7.5.2 Warehouses and distribution centers

- 7.5.3 Transportation infrastructure

- 7.5.4 Utilities and energy projects

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Amorim Cork

- 9.2 BRE Global Ltd

- 9.3 Concrete Centre

- 9.4 EcoCocon

- 9.5 Holcim

- 9.6 Kingspan

- 9.7 Owens Corning

- 9.8 Saint-Gobain