|

시장보고서

상품코드

1801823

척추 로봇 수술 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Spine Robotic Surgery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

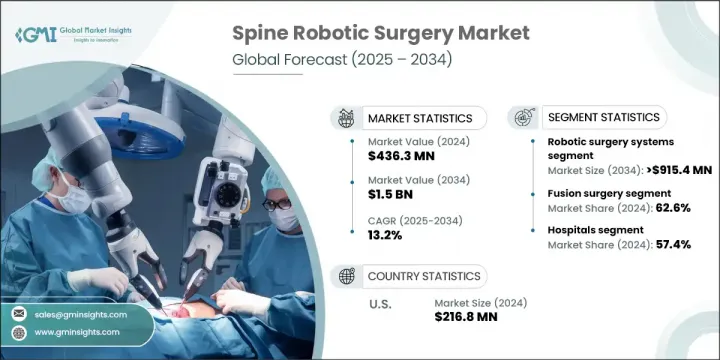

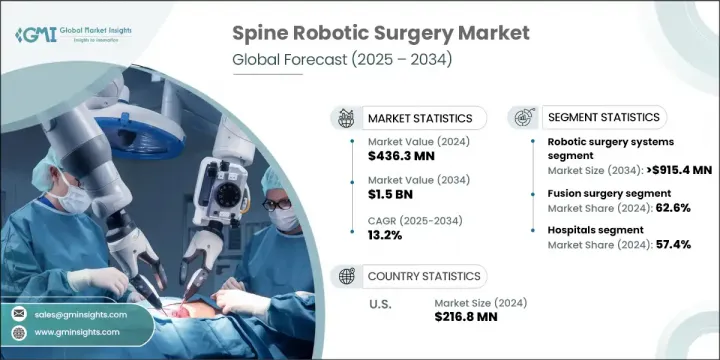

세계의 척추 로봇 수술 시장은 2024년에는 4억 3,630만 달러로 평가되었으며 CAGR 13.2%로 성장할 전망이며 2034년에는 15억 달러에 이를 것으로 추정됩니다.

이러한 상당한 성장은 척추 질환 발생률 증가, 의료 투자 확대, 그리고 전 세계적으로 최소 침습 수술 절차로의 전환에 의해 촉진되고 있습니다. 환자와 의료진 모두 회복 시간을 단축시키면서도 더 안전하고 정확한 시술을 추구함에 따라 고급 수술 옵션에 대한 수요는 지속적으로 증가하고 있습니다. 고령 인구가 증가하고 의료 시스템이 발전함에 따라 로봇 보조 척추 시술에 대한 수요는 다양한 지역에서 확대되고 있습니다.

인공 지능, 내비게이션, 실시간 영상 기술 발전과 결합된 수술용 로봇 기술의 혁신은 이러한 시스템의 신뢰성을 높이고 광범위한 채택을 가능하게 하고 있습니다. 이러한 기술들은 복잡한 척추 수술 중 정밀도를 향상시키고 기존 수술 방법으로는 달성하기 어려웠던 결과를 가능하게 합니다. 진화하는 의료 미래 속에서 로봇 시스템은 척추 수술의 필수 요소로 자리매김하며 안전성과 효율성을 동시에 높이고 있습니다. 병원 및 수술 센터에서의 점유율 증가는 향후 10년간 강력한 시장 성장세를 예고합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 4억 3,630만 달러 |

| 예측 금액 | 15억 달러 |

| CAGR | 13.2% |

척추 로봇 수술은 통제력과 정확성을 제공하여 척추 시술 방식을 획기적으로 개선합니다. 최소 침습적 특성으로 회복 속도를 높이고 합병증 위험을 낮춰 외과 의사와 환자 모두에게 매력적입니다. 로봇 시스템을 활용하면 의료진이 더 작고 정밀한 절개를 수행할 수 있어 주변 조직 손상을 최소화합니다. 이 시스템은 수동으로는 재현하기 어려운 정밀한 조작을 가능하게 하여 수술 오류 가능성을 줄이고 더 나은 결과를 제공합니다. 병원은 회복 시간 단축과 환자 입원 기간 감소로 혜택을 보며, 이는 전체 의료 비용을 낮추고 수술 워크플로우 효율성을 높입니다.

로봇 수술 시스템 부문은 2024년 58.3%의 점유율을 기록했습니다. 전문가들은 이러한 성과에 대한 주요 촉진 요인으로 기술적 발전과 강력한 임상 결과를 지목했습니다. 최근 수술용 로봇은 향상된 영상 기술, AI를 촉진한 계획 수립, 실시간 내비게이션 기능을 탑재하여 외과의가 고도로 복잡한 시술을 용이하게 수행할 수 있도록 보조합니다. 이는 더 정밀한 수술과 재수술 위험 감소로 이어져 많은 의료 기관에서 로봇 플랫폼을 선호하는 선택지로 만듭니다. 또한 로봇 시스템은 최소 침습적 기법을 보조하도록 설계되어 섬세하고 복잡한 작업을 보조하는 고급 도구를 제공합니다. 이러한 정밀성은 수술 품질을 향상시킬 뿐만 아니라 외과의의 자신감도 높여줍니다.

2024년 척추 융합 수술 부문은 62.6%의 점유율을 기록하며 척추 치료 분야에서 지속적인 인기를 반영했습니다. 특히 고령화 인구와 생활습관 요인으로 척추 관련 문제가 증가함에 따라 척추 융합은 여전히 가장 빈번하게 시행되는 시술 중 하나입니다. 로봇 보조 융합 수술은 향상된 정밀도, 낮은 합병증 발생률, 낮은 재수술률을 제공하며, 이러한 요소들이 해당 분야의 우위를 점하는 데 기여하고 있습니다. 로봇 기술의 통합은 이러한 시술을 정교화하여 만성 척추 질환을 앓는 환자에게 더 안전하고 예측 가능한 치료를 가능하게 했습니다.

미국의 척추 로봇 수술 2024년 시장 규모는 2억 1,680만 달러를 기록했습니다. 이 지역의 우위는 고급화된 병원 시스템, 혁신 기술의 신속한 도입, 연구 개발에 대한 증가하는 투자에 힘입었습니다. 미국은 확립된 인프라와 보험 적용 미래, 그리고 척추 질환으로 고통받는 대규모 환자 집단 덕분에 강력한 성장을 보이고 있습니다. 이러한 요인들로 인해 북미는 로봇 척추 수술 분야의 혁신 허브이자 상업적 리더로 자리매김하며, 전 세계 시장 진출을 확대하려는 업체들의 관심을 끌고 있습니다.

세계의 척추 로봇 수술 시장에 영향을 미치는 주요 기업으로는 존슨 엔드 존슨, 짐머 바이오멧, 지멘스 헤르티니어스, 메드트로닉, 인터이티브 서지컬 오퍼레이션스, 스트라이커, 브레인랩, Curexo, 오르소픽스 메디컬, R2 서지컬, B 브라운 연구 개발에 대한 지속적인 투자와 제품 혁신에 대한 주력은 척수 수술 기술의 미래를 형성하고 있습니다. 강력한 시장 입지를 구축하기 위해 척추 로봇 수술 분야의 선도 기업들은 지속적인 혁신과 전략적 파트너십에 주력하고 있습니다. 정밀도가 향상된 시스템을 제공하기 위해 인공지능 통합, 향후 내비게이션 도구, 고급 영상 기술에 막대한 투자를 진행 중입니다. 다수는 전 세계 시장에서 규제 승인을 더 빠르게 획득하기 위해 임상 시험 파이프라인을 확대되고 있습니다. 병원 및 학술 기관과의 협력을 통해 교육 및 시연 시설을 제공함으로써 로봇 플랫폼 도입을 가속화하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 척추질환 유병률 증가

- 기술 발전

- 최소 침습 수술 급증

- 의료비 증가

- 업계의 잠재적 위험 및 과제

- 로봇 디바이스의 복잡성

- 엄격한 규제 요건

- 시장 기회

- 신흥 경제 국가의 성장 잠재력

- 제품 개발을 위한 R&D에 대한 지속적인 투자

- 성장 촉진요인

- 성장 가능성

- 성장 가능성 분석

- 상환 시나리오

- 규제 상황

- 미국

- 유럽

- 기술과 혁신 미래

- 현재의 기술 동향

- 신흥기술

- 장래 시장 동향

- 신제품 개발의 정세

- 시작 시나리오

- 가격 분석(2024년)

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 로봇 수술 시스템

- 완전 로봇 시스템

- 로봇 암 보조 시스템

- 수술 내비게이션 시스템

- 전자 항법 시스템

- 광학 항법 시스템

- 하이브리드 내비게이션 시스템

- 소프트웨어 솔루션

- 액세서리와 소모품

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 융합 수술

- 비융합 수술

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 기타 최종 용도

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- B Braun

- Brainlab

- CUREXO

- Globus Medical

- Intuitive Surgical Operations

- Johnson &Johnson

- Medtronic

- Orthofix Medical

- R2 Surgical

- Siemens Healthineers

- Stryker

- Zimmer Biomet

The Global Spine Robotic Surgery Market was valued at USD 436.3 million in 2024 and is estimated to grow at a CAGR of 13.2% to reach USD 1.5 billion by 2034. This substantial growth is largely driven by the rising incidence of spinal disorders, increased healthcare investment, and a global shift toward minimally invasive surgical procedures. The need for advanced surgical options continues to grow as patients and providers alike seek safer, more accurate procedures that also reduce recovery time. As the aging population increases and healthcare systems evolve, the demand for robot-assisted spinal procedures is expanding across various regions.

Innovations in surgical robotics-combined with developments in artificial intelligence, navigation, and real-time imaging-are making these systems more reliable and widely adopted. These technologies are improving precision during complex spine procedures and enabling outcomes that traditional surgical methods struggle to achieve. In this evolving medical landscape, robotic systems are becoming an essential component of spinal surgery, enhancing both safety and efficiency. Their growing presence in hospitals and surgical centers signals a strong market trajectory through the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $436.3 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 13.2% |

Spine robotic surgery offers a level of control and accuracy that dramatically improves the way spinal procedures are performed. Its minimally invasive nature supports faster healing and lowers complication risks, which appeals to both surgeons and patients. By using robotic systems, clinicians can make smaller, more precise incisions, which helps minimize trauma to surrounding tissue. These systems enable fine-tuned maneuvers that are difficult to replicate manually, reducing the potential for surgical error and delivering better results. Hospitals benefit from reduced recovery times and shorter patient stays, which in turn lowers overall healthcare costs and increases efficiency in surgical workflows.

The robotic surgery systems segment held a 58.3% share in 2024. Experts pointed to technological advancement and strong clinical outcomes as key drivers for this performance. Modern surgical robotics are equipped with enhanced imaging, AI-driven planning, and real-time navigation, helping surgeons perform highly complex procedures with ease. This translates into more precise surgeries and less risk of revision, making robotic platforms a preferred choice in many facilities. Additionally, robotic systems are built to support minimally invasive techniques, offering advanced tools that assist with delicate and intricate tasks. This precision not only improves surgical quality but also boosts surgeon confidence.

The fusion surgery segment accounted for a 62.6% share in 2024, reflecting its continued popularity in spinal treatment. Spinal fusion remains one of the most frequently performed procedures, particularly as spine-related issues become more common with aging populations and lifestyle factors. Robotic-assisted fusion surgeries offer heightened precision, fewer complications, and lower revision rates, all of which contribute to their dominance in this space. The integration of robotics has helped refine these procedures, making them safer and more predictable for patients dealing with chronic spine conditions.

United States Spine Robotic Surgery Market generated USD 216.8 million in 2024. The region's dominance is fueled by advanced hospital systems, quick adoption of innovative technologies, and increasing investments in research and development. The US shows strong growth due to its established infrastructure and reimbursement landscape, alongside a large patient population affected by spine disorders. These factors make North America an innovation hub and commercial leader in robotic spine surgery, drawing interest from companies aiming to expand their global footprint.

Major players influencing the Global Spine Robotic Surgery Market include Johnson & Johnson, Zimmer Biomet, Siemens Healthineers, Medtronic, Intuitive Surgical Operations, Stryker, Brainlab, CUREXO, Orthofix Medical, R2 Surgical, B Braun, Globus Medical, and others. Their continued R&D investments and focus on product innovation are shaping the future of spinal surgery technologies. To build a strong market presence, leading companies in the spine robotic surgery space are focusing on continual innovation and strategic partnerships. They're investing heavily in AI integration, next-gen navigation tools, and advanced imaging capabilities to offer precision-enhanced systems. Many are expanding their clinical trial pipelines to gain regulatory approvals faster across global markets. Collaborations with hospitals and academic institutions are helping accelerate the adoption of robotic platforms by providing training and demonstration facilities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of spinal disorders

- 3.2.1.2 Technological advancements

- 3.2.1.3 Surge in minimally invasive surgical procedures

- 3.2.1.4 Increased healthcare spending

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complexity of robotic devices

- 3.2.2.2 Stringent regulatory requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Growth potential in developing economies

- 3.2.3.2 Continued investment in research and development for product development

- 3.2.1 Growth drivers

- 3.3 Growth potential

- 3.4 Growth potential analysis

- 3.5 Reimbursement scenario

- 3.6 Regulatory landscape

- 3.6.1 U.S.

- 3.6.2 Europe

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Future market trends

- 3.9 New product development landscape

- 3.10 Start-up scenario

- 3.11 Pricing analysis, 2024

- 3.12 Gap analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Robotic surgery systems

- 5.2.1 Fully robotic systems

- 5.2.2 Robotic arm-assisted systems

- 5.3 Surgical navigation systems

- 5.3.1 Electromagnetic navigation systems

- 5.3.2 Optical navigation systems

- 5.3.3 Hybrid navigation systems

- 5.4 Software solutions

- 5.5 Accessories and consumables

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Fusion surgery

- 6.3 Non-fusion surgery

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 B Braun

- 9.2 Brainlab

- 9.3 CUREXO

- 9.4 Globus Medical

- 9.5 Intuitive Surgical Operations

- 9.6 Johnson & Johnson

- 9.7 Medtronic

- 9.8 Orthofix Medical

- 9.9 R2 Surgical

- 9.10 Siemens Healthineers

- 9.11 Stryker

- 9.12 Zimmer Biomet