|

시장보고서

상품코드

1801828

흡수성 수술용 봉합사 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Absorbable Surgical Sutures Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

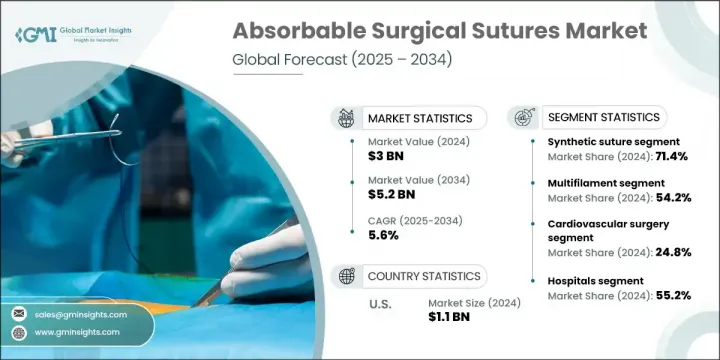

세계의 흡수성 수술용 봉합사 시장은 2024년에 30억 달러로 평가되어 CAGR 5.6%로 성장할 전망이며 2034년에는 52억 달러에 이를 것으로 추정됩니다.

시장 성장은 전 세계적으로 수술 건수의 급증, 만성 질환 발생률 증가, 봉합 기술 발전, 그리고 부인과 수술의 급증에 의해 촉진되고 있습니다. 의료 시스템이 최소 침습적 기술, 빠른 회복 기간, 환자 결과 개선에 더욱 집중함에 따라 흡수성 봉합사에 대한 수요도 증가하고 있습니다. 코팅 및 실 구조 혁신을 포함한 재료와 기술의 지속적인 개선은 전 세계 병원, 수술 센터, 외래 진료 시설에서 사용이 확대되기에 주요 역할을 하고 있습니다.

흡수성 수술용 봉합사는 체내에서 자연적으로 분해되도록 설계되어 수동 제거의 필요성을 없애고 수술 후 관리를 단순화합니다. 항균 특성, 가시 실 구조, 고성능 폴리머 블렌드와 같은 향상된 기능은 감염 위험을 줄이고 치유를 가속화하는 데 기여하고 있습니다. 더 많은 임상 현장에서 이러한 고급 도구를 채택함에 따라 전반적인 효율성과 환자 경험이 개선되어 최근 의료에서 제품의 중요성이 강화되고 있습니다. 환자 편의성과 시술 최적화에 대한 관심이 높아지면서 흡수성 봉합사는 다양한 외과 전문 분야에서 선호되는 선택지로 자리매김하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 30억 달러 |

| 예측 금액 | 52억 달러 |

| CAGR | 5.6% |

합성 봉합사 부문은 신뢰할 수 있는 흡수 특성, 높은 강도 유지력, 낮은 생물학적 반응성을 바탕으로 2024년 71.4%의 점유율을 차지했습니다. 폴리디옥사논(PDO), 폴리락틱산(PLA), 폴리글리콜릭산(PGA)과 같은 소재는 외과의가 분해 시점을 정밀하게 제어할 수 있게 하여 상처 치유의 각 단계에 맞춤형 지원을 가능하게 합니다. 개방형 및 최소 침습 수술 모두에서 활용 가능한 적응성 덕분에 고정밀 환경에서 신뢰할 수 있는 솔루션으로 자리매김하고 있습니다.

병원 부문은 2024년 55.2%의 점유율을 기록했습니다. 이러한 우위는 특히 고성장 국가에서 확대되는 병원 인프라, 증가하는 만성 질환 부담, 수술 기술 접근성 향상과 연관이 있습니다. 의료 시스템이 진화함에 따라 신축 및 기존 병원들은 치료 결과 개선, 합병증 발생률 감소, 최근 수술 기준 충족을 위해 고급 봉합 옵션을 우선적으로 도입하고 있습니다.

미국의 흡수성 수술용 봉합사 시장 규모는 2024년에 11억 달러에 달했습니다. 만성 질환 증가와 고급 수술 치료 수요가 지속적으로 수요를 끌어올리고 있습니다. 매년 시행되는 심혈관, 종양학 및 일반 수술 건수가 증가함에 따라 자연 흡수를 통해 빠른 회복 촉진, 감염 위험 감소, 환자 불편 최소화를 제공하는 봉합사로의 강력한 전환이 이루어지고 있습니다.

세계의 흡수성 수술용 봉합사 시장을 독점하고 있는 주요 기업으로는 Demetech, Corza Medical, Futura Surgicare, B. Braun, Medtronic, Unisur, Vitrex Medical Group, Healthium Medtech, Genesis MedTech, Vital Sutures, Advanced Medical Solutions, Lotus Surgicals, Inte & Johnson, CONMED 등이 있습니다. 흡수성 수술용 봉합사 시장 기업들은 생체재료 설계 및 항균 기술 혁신을 통해 입지를 강화하고 있습니다. 기업들은 인장 강도 향상, 제어된 분해 속도, 최소 침습적 기술과의 호환성을 갖춘 봉합사 개발을 위한 연구 개발에 주력하고 있습니다. 인수합병 및 전략적 협력을 통해 제품 포트폴리오와 전 세계 시장 진출이 확대되기를 기대하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성질환 유병률 증가

- 전 세계적으로 증가하는 수술 절차

- 봉합 재료 진보

- 부인과 수술 증가

- 업계의 잠재적 위험 및 과제

- 수속에 드는 비용이 높아

- 엄격한 규제 틀

- 시장 기회

- 저침습 수술 수요 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술 발전

- 현재의 기술 동향

- 신흥기술

- 공급망 분석

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 천연 봉합사

- 합성 봉합사

- 비크릴

- 폴리디옥사논 봉합사(PDS)

- 폴리그레카프론 봉합사(모노크릴)

제6장 시장 추계 및 예측 : 구조별(2021-2034년)

- 주요 동향

- 모노 필라멘트

- 멀티 필라멘트

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 심장혈관 수술

- 부인과 수술

- 정형외과

- 안과 수술

- 신경외과

- 기타 수술 용도

제8장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 전문 클리닉

- 외래수술센터(ASC)

- 기타 용도

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Advanced Medical Solutions

- B. Braun

- Corza Medical

- CONMED

- Demetech

- Futura Surgicare

- Genesis MedTech

- Healthium Medtech

- Integra Lifesciences

- Johnson &Johnson

- Medtronic

- Lotus Surgicals

- Unisur

- Vital Sutures

- Vitrex Medical Group

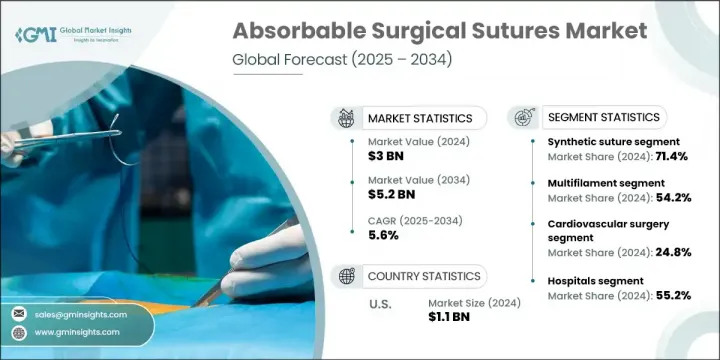

The Global Absorbable Surgical Sutures Market was valued at USD 3 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 5.2 billion by 2034. Market growth is being driven by a sharp rise in the number of surgical procedures worldwide, increasing incidences of chronic illnesses, advancements in suture technology, and a surge in gynecological surgeries. The demand for absorbable sutures is also growing as healthcare systems focus more on minimally invasive techniques, faster recovery timelines, and improved patient outcomes. Continuous improvements in materials and technologies, including innovations in coatings and thread structures, are playing a major role in expanding usage across hospitals, surgical centers, and outpatient facilities globally.

Absorbable surgical sutures are designed to naturally break down within the body, removing the need for manual removal and simplifying postoperative care. Enhanced features such as antimicrobial properties, barbed thread structures, and high-performance polymer blends are helping reduce infection risks and accelerate healing. As more clinical practices adopt these advanced tools, the overall efficiency and patient experience improve, reinforcing the product's relevance in modern healthcare. Increasing focus on patient comfort and procedure optimization is positioning absorbable sutures as a preferred choice across multiple surgical specialties.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 5.6% |

The synthetic sutures segment held 71.4% share in 2024, supported by their reliable absorption profiles, high strength retention, and reduced biological reactivity. Materials like polydioxanone (PDO), polylactic acid (PLA), and polyglycolic acid (PGA) offer surgeons precise control over degradation timelines, allowing tailored support during each phase of wound healing. Their adaptability in both open and minimally invasive procedures makes them a trusted solution in high-precision environments.

The hospitals segment held a 55.2% share in 2024. This dominance is linked to expanding hospital infrastructure, especially in high-growth countries, alongside rising chronic disease burdens and enhanced access to surgical technologies. As healthcare systems evolve, newly built and existing hospitals are prioritizing advanced suturing options to improve outcomes, reduce complication rates, and meet modern surgical standards.

United States Absorbable Surgical Sutures Market generated USD 1.1 billion in 2024. Rising chronic conditions and the need for advanced surgical care continue to elevate demand. With a growing number of cardiovascular, oncological, and general surgeries performed annually, there's a strong shift toward sutures that promote faster recovery, lower infection risks, and minimize patient discomfort through natural absorption.

Key players dominating the Global Absorbable Surgical Sutures Market include Demetech, Corza Medical, Futura Surgicare, B. Braun, Medtronic, Unisur, Vitrex Medical Group, Healthium Medtech, Genesis MedTech, Vital Sutures, Advanced Medical Solutions, Lotus Surgicals, Integra Lifesciences, Johnson & Johnson, and CONMED. Companies operating in the absorbable surgical sutures market are strengthening their positions through innovation in biomaterial design and antimicrobial technologies. Firms are focusing on R&D to develop sutures with enhanced tensile strength, controlled degradation rates, and compatibility with minimally invasive techniques. Mergers, acquisitions, and strategic collaborations are being pursued to expand product portfolios and global reach.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Material trends

- 2.2.3 Structure trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Rising surgical procedures worldwide

- 3.2.1.3 Advancements in suture materials

- 3.2.1.4 Increasing number of gynecological procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of procedures

- 3.2.2.2 Stringent regulatory framework

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for minimally invasive surgeries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Natural suture

- 5.3 Synthetic suture

- 5.3.1 Vicryl

- 5.3.2 Polydioxanone suture (PDS)

- 5.3.3 Poliglecaprone suture (Monocryl)

Chapter 6 Market Estimates and Forecast, By Structure, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Monofilament

- 6.3 Multifilament

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Cardiovascular surgery

- 7.3 Gynaecology surgery

- 7.4 Orthopaedic surgery

- 7.5 Ophthalmic surgery

- 7.6 Neurological surgery

- 7.7 Other surgical applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Specialty clinics

- 8.4 Ambulatory surgical centres

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Advanced Medical Solutions

- 10.2 B. Braun

- 10.3 Corza Medical

- 10.4 CONMED

- 10.5 Demetech

- 10.6 Futura Surgicare

- 10.7 Genesis MedTech

- 10.8 Healthium Medtech

- 10.9 Integra Lifesciences

- 10.10 Johnson & Johnson

- 10.11 Medtronic

- 10.12 Lotus Surgicals

- 10.13 Unisur

- 10.14 Vital Sutures

- 10.15 Vitrex Medical Group