|

시장보고서

상품코드

1801855

보석 제조 및 귀금속 가공 장비 시장 기회와 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Jewelry Making and Precious Metals Processing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

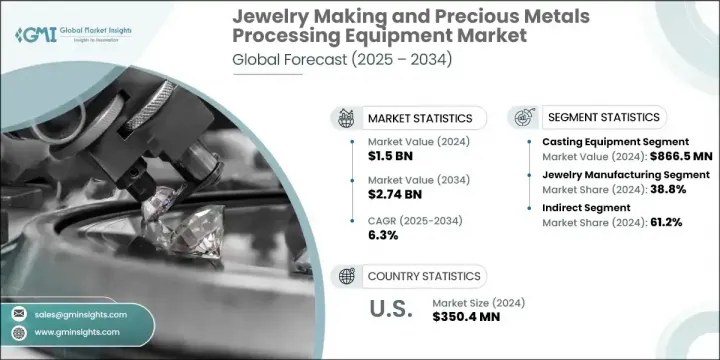

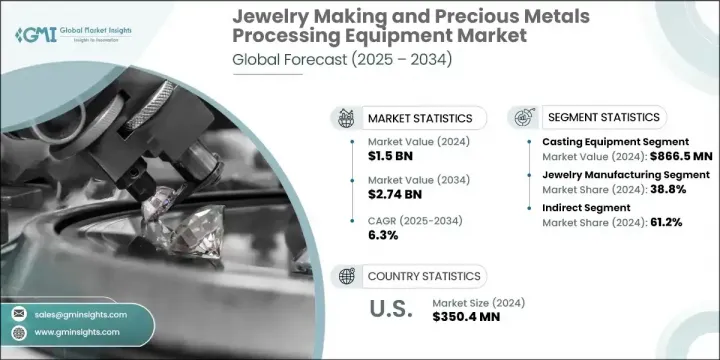

세계의 보석 제조 및 귀금속 가공 장비 시장 규모는 2024년에 15억 달러에 달하고, CAGR 6.3%로 성장할 전망이며 2034년에는 27억 4,000만 달러에 달할 것으로 예측되고 있습니다.

이 시장은 고품질 맞춤형 디자인 보석에 대한 소비자 관심 증가에 힘입어 강력하고 지속적인 성장을 보이고 있습니다. 특히 젊은 층과 선진국 및 신흥국 모두의 부유한 소비자들 사이에서 라이프스타일과 개성을 표현하는 주얼리를 찾는 수요가 강하다. 정밀 제조에 대한 필요성이 증가함에 따라 업계 업체들은 정확성과 확장성을 보장하는 고급 생산 기술을 도입하고 있다.

컴퓨터 지원 설계 소프트웨어, 3D 프린팅 도구, 자동화 시스템은 제조업체가 재료 낭비와 생산 시간을 최소화하면서 정교하고 일관되며 확장 가능한 디자인을 구현하는 데 도움을 주고 있다. 이러한 발전은 인건비 절감에도 상당한 기여를 하고 있다. 아시아태평양 지역은 확립된 인프라, 숙련된 노동력, 증가하는 국내 및 전 세계 수요 덕분에 이 산업의 주요 중심지로 자리매김하고 있습니다. 해당 지역 국가들은 저비용 노동력, 유리한 규제 체계, 보석 구매를 촉진하는 문화적 선호도 등 혜택을 누리며, 이 모든 요소가 결합되어 아시아태평양 지역의 전 세계 시장 영향력을 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 15억 달러 |

| 예측 금액 | 27억 4,000만 달러 |

| CAGR | 6.3% |

주조 장비 부문은 2024년 8억 6,650만 달러를 기록했으며, 2025년부터 2034년까지 연평균 6.7%의 성장률을 보일 것으로 예상됩니다. 이 장비는 대량 생산 적합성, 맞춤형 유연성, 비용 효율성으로 인해 보석 및 귀금속 용도에서 높은 선호도를 보입니다. 정밀 마감에는 레이저 기반 시스템(예: 조각 및 용접 도구) 사용이 증가하고 있지만, 주조 기술은 특히 신흥 시장과 중소 규모 제조업체에서 확장 가능한 생산을 위한 주요 선택지로 남아 있습니다. 그 적응성과 경제적 가치는 해당 분야 전반에 걸친 광범위한 채택을 지속적으로 촉진하고 있습니다.

보석 제조 부문은 2024년 38.8%의 점유율을 기록했으며, 2034년까지 연평균 성장률(CAGR) 6.8%를 보일 것으로 예상됩니다. 귀금속 가공 및 보석 장비 산업 내 주요 용도인 이 부문은 소비자 수요 증가, 디지털 제조 공정 발전, 보석 생산 네트워크의 국제화로 인해 확대되고 있습니다. 산업용 정제나 재활용과 같은 다른 용도와 비교하면, 보석 생산은 더 다양한 도구와 장비를 필요로 하여, 산업의 지속적인 발전과 혁신에서 핵심적인 역할을 하고 있습니다.

미국의 보석 제조 및 귀금속 가공 장비 시장은 76.5%의 점유율을 차지해 2024년에는 3억 5,040만 달러를 창출했습니다. 이러한 강력한 입지는 미국의 고급 제조 역량과 명품 보석 브랜드의 확고한 입지 덕분입니다. 미국 제조업체들은 CAD 소프트웨어, 3D 프린팅 시스템, 레이저 기반 도구 등 디지털 기술을 광범위하게 활용하여 작업 흐름을 간소화하고 제품 생산량을 향상시킵니다. 이러한 기술적 엣지는 미국이 고급 보석 제조 분야에서 지속적인 우위를 점하는 데 기여하며, 전체 시장에서 핵심 업체로 자리매김하게 합니다.

세계의 보석 제조 및 귀금속 가공 장비 시장을 형성하는 주요 기업으로는 Durston Tools, UIHM, Orotig, Supermelt, Indutherm, LaserStar Technologies, CDOCAST Machinery, Gesswein, Rio Grande, EnvisionTEC, Gravotech, Schultheiss, Contenti, Pepeto 등이 있습니다. 해당 분야 기업들은 시장 지위를 공고히 하기 위해 제품 혁신, 디지털 설계 역량 확대, 제조 기술 업그레이드에 주력하고 있습니다. 많은 기업들이 설계 정확도를 높이고 생산 일정을 효율화하기 위해 자동화 및 AI 촉진 도구를 통합하고 있습니다. 사용자 친화적 인터페이스와 모듈식 기계에 대한 투자를 통해 기업들은 소규모 장인 작업장에서 대규모 제조업체에 이르기까지 다양한 고객 요구를 충족시킬 수 있습니다. 또한 기업들은 지역 유통업체와의 파트너십 구축 및 신속한 애프터서비스 지원을 통해 전 세계 입지를 확대하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 맞춤 및 고급 보석에 대한 수요 증가

- 가공 장비 기술 발전

- 자동화와 디지털 설계 툴 이용 증가

- 업계의 잠재적 위험 및 과제

- 고급 장비의 높은 비용

- 귀금속 가격 변동

- 기회

- 보석 제조의 3D 프린팅 출현

- 지속가능하고 윤리적인 보석 수요 증가

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 기술과 혁신의 상황

- 규제 환경

- 밸류체인 분석

- 원재료 공급업체 및 부품 제조업체

- 장비 제조업체 및 OEM

- 유통 채널과 판매 네트워크

- 최종 용도 부문 및 용도

- 애프터 서비스 제공업체

- 가격 동향

- 지역별

- 장비유형별

- 규제 상황

- 표준 및 규정 준수 요건

- 지역 규제 틀

- 인증기준 무역 통계

- 주요 수입국

- 주요 수출국

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추정 및 예측 : 장비 유형별(2021-2034년)

- 주요 동향

- 주조 장비

- 용해 및 정제 장비

- 스탬핑 및 성형 장비

- 레이저 장비

- 연마 및 마감 장비

- 전기 도금 장비

- 기타

제6장 시장 추정 및 예측 : 금속 유형별(2021-2034년)

- 주요 동향

- 금 가공 장비

- 은 가공 장비

- 백금족 금속 장비

- 기타

제7장 시장 추정 및 예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 보석 제조

- 귀금속 정제

- 손목시계 제조

- 기타

제8장 시장 추정 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접 판매

- 간접 판매

제9장 시장 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제10장 기업 프로파일

- CDOCAST Machinery

- Contenti

- Durston Tools

- EnvisionTEC

- Gesswein

- Gravotech

- Indutherm

- LaserStar Technologies

- Orotig

- Pepetools

- Rio Grande

- Schultheiss

- Superbmelt

- UIHM

The Global Jewelry Making and Precious Metals Processing Equipment Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 2.74 billion by 2034. This market is witnessing strong and sustained growth, primarily driven by increasing consumer interest in high-quality, custom-designed jewelry. The demand is especially strong among younger demographics and affluent consumers in both established and emerging economies who seek pieces that express their lifestyle and individuality. As the need for precision manufacturing rises, industry players are embracing advanced production technologies that ensure accuracy and scalability.

Computer-aided design software, 3D printing tools, and automated systems are helping manufacturers deliver detailed, consistent, and scalable designs while minimizing material waste and production time. These advancements are also contributing to significant reductions in labor costs. The Asia-Pacific region remains the dominant hub for this industry, thanks to its established infrastructure, skilled labor force, and growing domestic and global demand. Countries across the region benefit from low-cost labor, favorable regulatory frameworks, and cultural preferences that promote jewelry purchases, which collectively strengthen APAC's influence on the global market landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.74 Billion |

| CAGR | 6.3% |

The casting equipment segment generated USD 866.5 million in 2024 and is forecasted to grow at a CAGR of 6.7% between 2025 and 2034. This equipment is highly favored in jewelry and precious metal applications due to its suitability for mass production, flexibility in customization, and cost efficiency. While laser-based systems like engraving and welding tools are increasingly used for precision finishing, casting technology remains the go-to for scalable production, particularly in emerging markets and among small to mid-sized manufacturers. Its adaptability and economic value continue to drive its widespread adoption across the sector.

The jewelry manufacturing segment accounted for a 38.8% share in 2024 and is expected to register a CAGR of 6.8% through 2034. As the leading application within the precious metals processing and jewelry equipment industry, this segment is expanding due to rising consumer demand, advancements in digital manufacturing processes, and the internationalization of jewelry production networks. Compared to other applications like industrial refining or recycling, jewelry production requires a greater variety of tools and equipment, giving it a central role in the industry's continued development and innovation.

U.S. Jewelry Making and Precious Metals Processing Equipment Market held a 76.5% share and generated USD 350.4 million in 2024. This strong position can be attributed to the country's advanced manufacturing capabilities and well-established presence of luxury jewelry brands. American manufacturers widely utilize digital technologies such as CAD software, 3D printing systems, and laser-based tools to streamline workflows and enhance product output. This technological edge supports the country's continued dominance in the high-end jewelry manufacturing space, making it a critical player in the overall market.

Key companies shaping the Global Jewelry Making and Precious Metals Processing Equipment Market include Durston Tools, UIHM, Orotig, Supermelt, Indutherm, LaserStar Technologies, CDOCAST Machinery, Gesswein, Rio Grande, EnvisionTEC, Gravotech, Schultheiss, Contenti, and Pepetools. To reinforce their market position, companies in this sector are focusing on product innovation, expanding digital design capabilities, and upgrading manufacturing technologies. Many are integrating automation and AI-driven tools to enhance design accuracy and streamline production timelines. Investing in user-friendly interfaces and modular machines allows businesses to serve a wide range of customer needs-from small artisan workshops to large-scale manufacturers. Firms are also increasing their global presence by establishing partnerships with regional distributors and offering responsive after-sales support.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.3 Data collection methods

- 1.4 Data mining sources

- 1.4.1 Global

- 1.4.2 Regional/Country

- 1.5 Base estimates and calculations

- 1.5.1 Base year calculation

- 1.5.2 Key trends for market estimation

- 1.6 Primary research and validation

- 1.6.1 Primary sources

- 1.7 Forecast model

- 1.8 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Metal type

- 2.2.4 End use Industry

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for custom and luxury jewelry

- 3.2.1.2 Technological advancements in processing equipment

- 3.2.1.3 Growing use of automation and digital design tools

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of advanced equipment

- 3.2.2.2 Volatility in precious metal prices

- 3.2.3 Opportunities

- 3.2.3.1 Emergence of 3d printing in jewelry manufacturing

- 3.2.3.2 Increasing demand for sustainable and ethical jewelry

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.6 Regulatory environment

- 3.7 Value Chain Analysis

- 3.7.1 Raw material suppliers and component manufacturers

- 3.7.2 Equipment manufacturers and OEMs

- 3.7.3 Distribution channels and sales networks

- 3.7.4 End use segments and applications

- 3.7.5 After-sales service providers

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By equipment type

- 3.9 Regulatory landscape

- 3.9.1 standards and compliance requirements

- 3.9.2 Regional regulatory frameworks

- 3.10 Certification standards Trade statistics

- 3.10.1 Major importing countries

- 3.10.2 Major exporting countries

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Casting equipment

- 5.2.1 Melting and refining equipment

- 5.2.2 Stamping and forming equipment

- 5.3 Laser equipment

- 5.3.1 Polishing and finishing equipment

- 5.3.2 Electroplating equipment

- 5.3.3 Other equipment

Chapter 6 Market Estimates & Forecast, By Metal Type, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Gold processing equipment

- 6.3 Silver processing equipment

- 6.4 Platinum group metals equipment

- 6.5 Other precious metals equipment

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Jewelry manufacturing

- 7.3 Precious metals refining

- 7.4 Watch manufacturing

- 7.5 Other industries

Chapter 8 Market Estimates & Forecast, By Distribution Channel 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 CDOCAST Machinery

- 10.2 Contenti

- 10.3 Durston Tools

- 10.4 EnvisionTEC

- 10.5 Gesswein

- 10.6 Gravotech

- 10.7 Indutherm

- 10.8 LaserStar Technologies

- 10.9 Orotig

- 10.10 Pepetools

- 10.11 Rio Grande

- 10.12 Schultheiss

- 10.13 Superbmelt

- 10.14 UIHM