|

시장보고서

상품코드

1801861

냉동식품용 식용 포장 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Edible Packaging for Frozen Foods Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

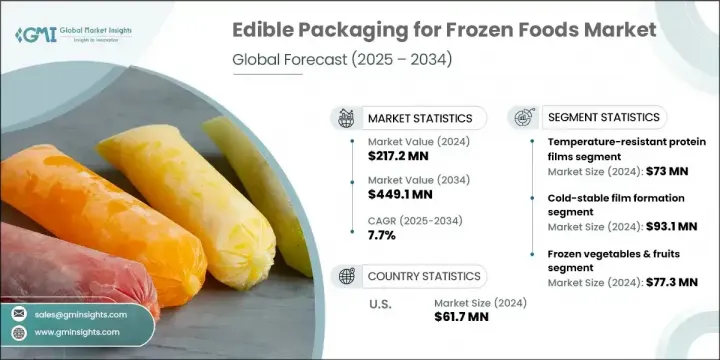

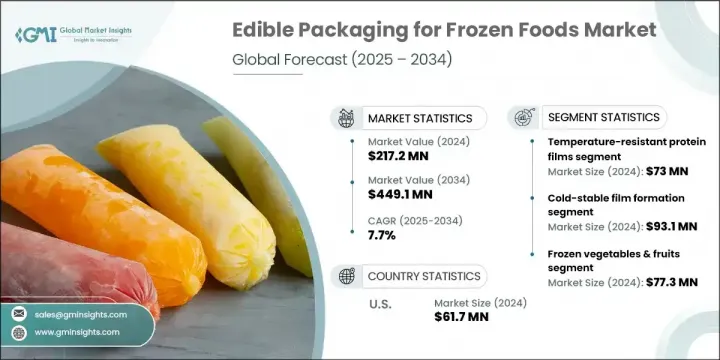

세계의 냉동식품용 식용 포장 시장은 2024년에는 2억 1,720만 달러에 달하고, CAGR 7.7%로 성장할 전망이며 2034년에는 4억 4,910만 달러에 이를 것으로 예측되고 있습니다.

이 성장하는 시장은 특히 개별 급속 동결(IQF) 과일, 채소, 전자레인지용 냉동 식품 및 즉석 가열 식품을 위한 냉동 안정성 및 생분해성 포장재에 대한 수요 증가에 의해 촉진되고 있습니다. 이러한 수요는 북미, 유럽 및 일본, 한국, 호주 등 아시아태평양 일부 지역에서 특히 두드러집니다. 식용 포장 수요는 주로 북미와 유럽의 냉동 과일 및 식물성 식사 판매 증가와 더불어 아시아태평양 일부 지역의 키토산 및 전분 기반 포장재와 같은 더 저렴한 대안의 등장으로 촉진되었습니다.

저렴한 가격과 냉동 안정성 덕분에 다당류 필름이 시장에서 가장 높은 성장률을 보일 것으로 예상됩니다. 또한 콜드체인 최적화 필요성과 식용 코팅에 향료 통합이 프리미엄 제품 부문의 성장을 촉진할 것으로 예상됩니다. 북미와 서유럽에서 사설 브랜드 냉동 식품의 부상은 식용 포장 채택 증가의 또 다른 상당한 요인입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 2억 1,720만 달러 |

| 예측 금액 | 4억 4,910만 달러 |

| CAGR | 7.7% |

다당류 필름 부문은 2034년까지 34.9%의 점유율을 달성할 것으로 예상됩니다. 전분, 알긴산염, 셀룰로오스 등의 원료로 제조된 이 필름은 저렴한 비용, 알레르기 유발 위험 최소화, 냉동 환경에서의 우수한 성능으로 선호됩니다. 또한 유연성을 제공하여 야채, 해산물, 즉석식 등 다양한 냉동 식품에 적합합니다.

2024년 냉동 채소 및 과일 부문은 높은 수출량과 수분 보존 및 친환경 브랜딩 강화에 기여하는 식용 코팅의 조기 도입으로 35.6% 점유율을 차지했습니다. 유럽 및 아시아 일부 지역을 포함한 여러 지역에서 유기농 라벨링 규제가 강화되고 냉동 농산물용 플라스틱 포장재 사용이 금지되면서 식용 포장 사용이 더욱 성장세를 보이고 있습니다.

북미의 냉동식품용 식용 포장 시장은 소매업체의 도입 확대, 식용 포장 분야의 혁신적인 스타트업 등장, 지속가능성에 대한 소비자 인식 증가에 힘입어 2024년 33%의 점유율을 기록했습니다. 미국 단독으로 6,170만 달러를 차지했습니다. 또한 지속가능성을 차별화 요소로 내세운 식용 필름을 적용한 자체 브랜드 냉동식품의 부상이 시장 성장을 더욱 촉진했습니다. 그러나 원자재 고가 및 규제 준수 등의 과제가 시장 확장을 저해할 수 있습니다.

세계의 냉동식품용 식용 포장 시장의 주요 진출기업으로는 Ingredion Incorporated, Tate & Lyle PLC, BASF SE, WikiCell Designs Inc., Amcor Plc. 등이 있습니다. 식용 포장 업계 기업들은 시장 지위를 유지하고 확대되기 위해 다양한 전략을 구사해 왔습니다. 여기에는 냉동 식품의 동결 안정성 향상 및 수분 유지력 개선과 같은 제품 성능 향상을 위한 지속적인 소재 혁신이 포함됩니다. 기업들은 또한 지속 가능성에 주력하여 자사 제품이 생분해 가능하고 친환경 솔루션에 대한 소비자 수요에 부합하도록 보장하고 있습니다. 냉동 식품 제조업체와의 전략적 파트너십 및 협력을 통해 기업들은 특히 성장하는 식물성 및 유기농 식품 부문에서 더 다양한 제품군에 식용 포장을 통합할 수 있게 되었습니다.

목차

제1장 조사 방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역/국가

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제와 한계

제2장 주요 요약

제3장 산업 고찰

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 산업에 미치는 영향요인

- 성장 촉진요인

- 산업의 잠재적 리스크 및 과제

- 공급망의 복잡성

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속 가능한 실습

- 폐기물 감축 전략

- 생산의 에너지 효율

- 친환경 활동

- 탄소발자국 고려 사항

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정 및 예측 : 재료별(2025-2034년)

- 주요 동향

- 내열성 단백질 필름

- 다당류 필름

- 지질 기반 코팅

- 복합재료와 하이브리드 재료

제6장 시장 추정 및 예측 : 기술 유형별(2025-2034년)

- 주요 동향

- 냉동 안정성 필름 형성

- 차단성 강화

- 콜드체인 통합

제7장 시장 추정 및 예측 : 용도 유형별(2025-2034년)

- 주요 동향

- 냉동 채소 및 과일

- 냉동고기 및 해산물

- 냉동 즉석식품

- 냉동유제품 및 디저트

제8장 시장 추정 및 예측 : 지역별(2025-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Tate & Lyle PLC

- Kerry Group plc

- Ingredion Incorporated

- Cargill, Incorporated

- Archer-Daniels-Midland Company

- DuPont de Nemours, Inc.

- BASF SE

- Corbion NV

- Roquette Freres

- CP Kelco(JM Huber Corporation)

- FMC Corporation

- Ashland Global Holdings Inc.

- Novamont SpA

- WikiCell Designs Inc.

- MonoSol LLC

The Global Edible Packaging for Frozen Foods Market was valued at USD 217.2 million in 2024 and is estimated to grow at a CAGR of 7.7% to reach USD 449.1 million by 2034. This growing market is driven by an increasing demand for cold-stable, biodegradable packaging, particularly for individually quick frozen (IQF) fruits, vegetables, microwaveable frozen meals, and ready-to-heat meals. This demand is particularly evident in North America, Europe, and select parts of Asia-Pacific, such as Japan, South Korea, and Australia. The demand for edible packaging has been primarily fueled by the sales of frozen fruits and plant-based meals in North America and Europe, alongside more affordable alternatives like chitosan and starch-based packaging in parts of Asia-Pacific.

Polysaccharide films, due to their affordability and freeze stability, are expected to see the highest growth within the market. Additionally, the need for cold-chain optimization and the integration of flavors into edible coatings is expected to drive growth in premium product categories. The rise of private-label frozen foods in North America and Western Europe is another significant contributor to the increasing adoption of edible packaging.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $217.2 Million |

| Forecast Value | $449.1 Million |

| CAGR | 7.7% |

The polysaccharide films segment will reach 34.9% share by 2034. These films, derived from materials like starch, alginate, and cellulose, are preferred for their low cost, minimal allergen risk, and strong performance in frozen environments. They also offer flexibility, making them suitable for various frozen foods, such as vegetables, seafood, and ready-to-eat meals.

In 2024, the frozen vegetables and fruits segment accounted for 35.6% share driven by their high export volumes and early adoption of edible coatings, which help preserve moisture and enhance eco-friendly branding. The use of edible packaging has gained further momentum due to stricter organic labeling regulations and bans on plastic wraps for frozen produce in various regions, including Europe and parts of Asia.

North America Edible Packaging for Frozen Foods Market held 33% share in 2024, driven by retailer adoption, innovative start-ups in edible packaging, and growing consumer awareness of sustainability. The U.S. alone represented USD 61.7 million. Additionally, the rise of private-label frozen food products featuring edible films as a sustainable differentiation point has fueled further market growth. However, challenges such as the high cost of raw materials and regulatory compliance may slow the market's expansion.

Key players in the Global Edible Packaging for Frozen Foods Market include Ingredion Incorporated, Tate & Lyle PLC, BASF SE, WikiCell Designs Inc., and Amcor Plc. To maintain and expand their market position, companies in the edible packaging sector have employed a variety of strategies. These include ongoing innovation in materials to enhance product performance, such as increasing freeze stability and improving moisture retention for frozen foods. Companies have also focused on sustainability, ensuring their products are biodegradable and aligned with consumer demand for eco-friendly solutions. Strategic partnerships and collaborations with frozen food manufacturers have allowed companies to integrate their edible packaging into a broader range of products, especially in the growing plant-based and organic food sectors.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Technology

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain complexity

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2025 - 2034 (USD Million, Units)

- 5.1 Key trends

- 5.2 Temperature-resistant protein films

- 5.3 Polysaccharide films

- 5.4 Lipid-based coatings

- 5.5 Composite & hybrid materials

Chapter 6 Market Estimates and Forecast, By Technology Type, 2025 - 2034 (USD Million, Units)

- 6.1 Key trends

- 6.2 Cold-stable film formation

- 6.3 Barrier enhancements

- 6.4 Cold chain integration

Chapter 7 Market Estimates and Forecast, By Application type, 2025 - 2034 (USD Million, Units)

- 7.1 Key trends

- 7.2 Frozen vegetables & fruits

- 7.3 Frozen meat & seafood

- 7.4 Frozen ready meals

- 7.5 Frozen dairy & desserts

Chapter 8 Market Estimates and Forecast, By Region, 2025 - 2034 (USD Million, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 Tate & Lyle PLC

- 9.2 Kerry Group plc

- 9.3 Ingredion Incorporated

- 9.4 Cargill, Incorporated

- 9.5 Archer-Daniels-Midland Company

- 9.6 DuPont de Nemours, Inc.

- 9.7 BASF SE

- 9.8 Corbion N.V.

- 9.9 Roquette Freres

- 9.10 CP Kelco (J.M. Huber Corporation)

- 9.11 FMC Corporation

- 9.12 Ashland Global Holdings Inc.

- 9.13 Novamont S.p.A.

- 9.14 WikiCell Designs Inc.

- 9.15 MonoSol LLC