|

시장보고서

상품코드

1801862

보강용 부식 억제제 시장 : 기회, 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Corrosion Inhibitors for Reinforcement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

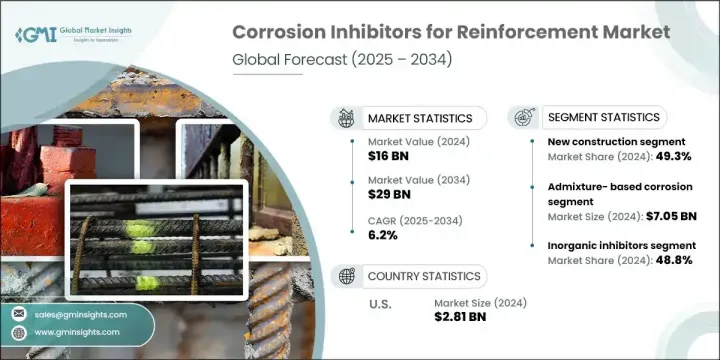

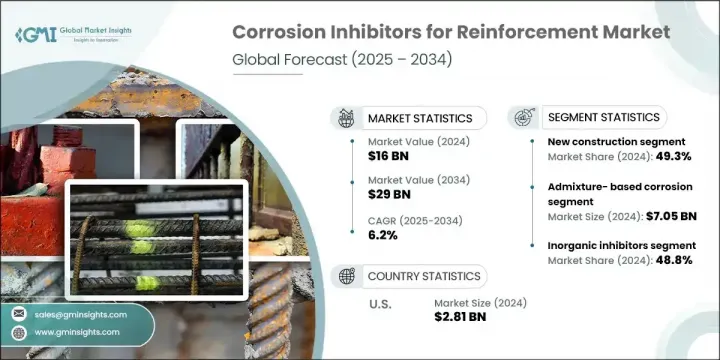

세계의 보강용 부식 억제제 시장은 2024년에는 160억 달러로 평가되어 CAGR 6.2%로 성장할 전망이며 2034년에는 290억 달러에 이를 것으로 추정되고 있습니다.

이 시장은 철근 콘크리트 구조물의 부식을 방지하기 위해 특별히 설계된 표면 도포형 억제제, 혼합제 기반 제형, 이동형 시스템 등 다양한 유형의 솔루션으로 구성됩니다. 시장의 성장은 인프라 개발 증가, 도시화, 내구성 향상 및 보수 빈도 감소를 목표로 한 강화된 규제 요구에 힘입어 촉진되고 있습니다.

더 많은 국가들이 엄격한 건축 규정과 지속가능성 목표를 시행함에 따라, 첨단 억제제를 사용하여 철근 콘크리트 구조물의 수명을 연장할 필요성이 건설 및 토목 공학 분야 전반에 걸쳐 필수적이 되었습니다. 북미, 유럽, 아시아태평양과 같은 지역에서는 내구성이 뛰어나고 오래 지속되는 건축 자재에 대한 수요가 증가하여 부식 방지 기술에 대한 강력한 성장세를 창출하고 있습니다. 환경 친화적이고 지속 가능한 부식 억제제 솔루션으로의 전환은 혁신을 가속화하고 있습니다. 제조사들은 전 세계 환경 규정 준수 목표에 부합하는 새로운 전달 메커니즘과 친환경 화학 물질을 개발 중입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 160억 달러 |

| 예측 금액 | 290억 달러 |

| CAGR | 6.2% |

다양한 제품 유형 중 혼합제 기반 부식 억제제 부문은 2024년 44%의 점유율을 기록했습니다. 이 제품은 콘크리트 혼합물에 쉽게 통합될 수 있고, 특히 신축 구조물에 장기적인 내부 보호 기능을 제공할 수 있다는 점에서 선호됩니다. 또한 유지보수 용도에도 효과적으로 사용됩니다. 반면, 표면 도포형 솔루션은 노후 콘크리트 자산의 복구 및 보존에 널리 사용됩니다.

용도별로는 신축 부문이 2024년에 49.3%의 점유율을 차지했습니다. 콘크리트 혼합 시 억제제를 사용하면 구조적 내구성이 상당하게 향상되고 부식 발생이 지연되어 수명 주기 비용을 최소화하며, 장기적인 관점에서 인프라 품질 기준을 높이기 위한 광범위한 노력과 부합합니다. 이러한 예방적 접근 방식은 최근 건설 관행의 핵심 요소로 자리 잡고 있습니다.

미국의 보강용 부식 억제제 2024년 시장 규모는 28억 1,000만 달러 규모를 기록했습니다. 해당 국가는 선도적 제조업체의 강력한 입지와 제품 성능 향상, 지속가능성, 규제 준수 강화에 주력하는 활발한 연구 활동의 혜택을 누리고 있습니다. 인프라 현대화가 국가적 우선순위로 부상함에 따라 내구성이 뛰어나고 유지보수가 적은 콘크리트 구조물에 대한 수요는 지속적으로 증가하고 있습니다. 고급 억제제 기술은 성능 규정 준수 및 보수 비용 절감을 위해 교통 시스템, 상업용 건물, 민간 인프라, 주거 단지 개발에 걸쳐 점차 확대 적용되고 있습니다.

보강용 부식 억제제 시장에서 사업을 전개하고 있는 주요 기업은 GCP Applied Technologies Inc., BASF SE, Halliburton(생산 화학 부문), Sika AG, Penetron International Ltd., Pidilite Industries Limited, Clariant AG, MAPEI SpA, ChemTreat Inc., Arkema Group, D.Ecob Inc. CV, Evonik Industries AG 등이 있습니다.

보강용 부식 방지제 부문의 기업들은 시장 입지를 강화하기 위해 혁신, 지속 가능성 및 맞춤형 제품 솔루션을 중심으로 한 전략적 계획을 시행하고 있습니다. 친환경적이고 무독성인 제형 개발에 상당한 주력을 기울이고 있으며, 이는 녹색 건축 규정을 준수하고 환경적 영향을 줄이는 데 기여합니다. 기업들은 인프라 수요가 높은 신흥 시장에 진출하여 전 세계 입지가 확대되고 있습니다. 건설 회사 및 연구 개발 기관과의 전략적 협력은 제품 성능과 용도 기술 개선에 도움이 됩니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 산업 고찰

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 산업에 미치는 영향요인

- 성장 촉진요인

- 내구성이 높은 인프라 자재 수요 증가

- 억제제 기술 발전

- 지속 가능한 건설 화학 규제 강화

- 산업의 잠재적 리스크 및 과제

- 콘크리트 배합 설계의 적합성 문제

- 가격 경쟁 시장 비용 감도

- 시장 기회

- 스마트 건설 및 모니터링 시스템 통합

- 환경 친화적이고 지속 가능한 솔루션에 대한 수요 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품 유형별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속 가능한 사례

- 폐기물 감축 전략

- 생산의 에너지 효율

- 친환경 활동

- 탄소발자국 고려 사항

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 혼합제 기반 부식 억제제

- 아질산칼슘 기반 억제제

- 유기혼합제 억제제

- 인산계 혼합제

- 기타 화학혼합제

- 표면 도포형 부식 방지제

- 침투 억제제

- 차단막 형성 억제제

- 2상 억제제

- 이행성 부식 억제제

- 유기 이동 억제제

- 무기 이동 시스템

- 신기술

- 스마트/반응형 억제제

- 나노 강화 시스템

- 생물 기반 억제제

제6장 시장 추정 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 신축 용도

- 콘크리트 혼합 단계 통합

- 시공 전 표면 처리

- 재활 및 수리

- 표면 도포 방법

- 주입과 함침 기술

- 유지보수 및 보호

- 예방 유지 보수 프로그램

- 긴급 수리 용도

제7장 시장 추정 및 예측 : 화학 유형별(2021-2034년)

- 주요 동향

- 무기 억제제

- 아질산염 기반 시스템

- 인산 기반 화합물

- 규산염 기반 억제제

- 유기 억제제

- 아미노 알코올 기반 시스템

- 아민카르복실산 억제제

- 유기산 유도체

- 하이브리드와 첨단 시스템

- 유기-무기 복합체

- 나노 강화 제제

- 스마트 방출 시스템

제8장 시장 추정 및 예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 인프라 및 교통

- 교량과 고속도로 구조물

- 터널과 지하건설

- 해양과 항만 시설

- 공항 인프라

- 주택건설

- 고층 빌딩

- 주택개발

- 리모델링 프로젝트

- 상업 및 산업용

- 오피스 빌딩과 복합 시설

- 산업시설

- 창고와 배송 센터

- 특수 용도

- 석유 및 가스 시설

- 발전소

- 수처리 인프라

- 화학 처리 공장

제9장 시장 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Arkema Group

- BASF SE

- ChemTreat Inc.

- CEMEX SAB de CV

- Clariant AG

- Dow Inc.

- Ecolab Inc.(Nalco Water)

- Evonik Industries AG

- GCP Applied Technologies Inc

- Halliburton(Production Chemicals Division)

- MAPEI SpA

- Penetron International Ltd.

- Pidilite Industries Limited

- Sika AG

The Global Corrosion Inhibitors for Reinforcement Market was valued at USD 16 billion in 2024 and is estimated to grow at a CAGR of 6.2% to reach USD 29 billion by 2034. This market includes various types of solutions such as surface-applied inhibitors, admixture-based formulations, and migrating systems specifically designed to prevent corrosion in reinforced concrete structures. Market growth is fueled by increasing infrastructure development, urbanization, and heightened regulatory demands aimed at boosting durability and reducing repair frequency.

As more countries implement stricter building codes and sustainability goals, the need to extend the life of reinforced concrete structures using advanced inhibitors has become essential across the construction and civil engineering sectors. In regions like North America, Europe, and Asia-Pacific, there's a rising demand for durable and long-lasting building materials, creating strong momentum for corrosion prevention technologies. The shift toward environmentally safe, sustainable corrosion inhibitor solutions is accelerating innovation. Manufacturers are developing newer delivery mechanisms and green chemistries that align with global eco-compliance goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16 Billion |

| Forecast Value | $29 Billion |

| CAGR | 6.2% |

Among the different product types, the admixture-based corrosion inhibitors segment held a 44% share in 2024. These are favored for their ease of integration into concrete mixes and their ability to provide long-term internal protection, particularly for newly built structures. They are also used effectively in maintenance applications. In contrast, surface-applied solutions are widely used for rehabilitating and preserving older concrete assets.

In terms of application, the new construction segment held a 49.3% share in 2024. The use of inhibitors during concrete mixing significantly improves structural resilience and delays the onset of corrosion, minimizing lifecycle costs and aligning with broader efforts to raise infrastructure quality standards over extended timelines. This preventative approach is becoming a critical part of modern construction practices.

U.S. Corrosion Inhibitors for Reinforcement Market generated USD 2.81 billion in 2024. The country benefits from a strong presence of leading manufacturers and robust research efforts focused on improving product performance, sustainability, and regulatory alignment. As infrastructure modernization gains national priority, the demand for durable, low-maintenance concrete structures continues to rise. Advanced inhibitor technologies are being increasingly adopted across transportation systems, commercial buildings, civil infrastructure, and residential developments to comply with performance mandates and lower repair expenditures.

Key companies operating in the Corrosion Inhibitors for Reinforcement Market include GCP Applied Technologies Inc., BASF SE, Halliburton (Production Chemicals Division), Sika AG, Penetron International Ltd., Pidilite Industries Limited, Clariant AG, MAPEI S.p.A., ChemTreat Inc., Arkema Group, Ecolab Inc. (Nalco Water), Dow Inc., CEMEX S.A.B. de C.V., and Evonik Industries AG.

To enhance market presence, companies in the corrosion inhibitors for reinforcement segment are implementing strategic initiatives centered around innovation, sustainability, and tailored product solutions. A significant focus is placed on developing eco-friendly, non-toxic formulations that comply with green building regulations and reduce environmental impact. Businesses are expanding their global footprint by entering emerging markets with high infrastructure demand. Strategic collaborations with construction firms and R&D institutes help improve product performance and application techniques.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Application method

- 2.2.3 Chemistry type

- 2.2.4 End use industry

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for long-lasting infrastructure materials

- 3.2.1.2 Technological advancements in inhibitor formulations

- 3.2.1.3 Regulatory push for sustainable construction chemicals

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Compatibility issues with concrete mix designs

- 3.2.2.2 Cost sensitivity in price-competitive markets

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with smart construction and monitoring systems

- 3.2.3.2 Rising demand for eco-friendly and sustainable solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Admixture-based corrosion inhibitors

- 5.2.1 Calcium nitrite-based inhibitors

- 5.2.2 Organic admixture inhibitors

- 5.2.3 Phosphate-based admixtures

- 5.2.4 Other chemical admixtures

- 5.3 Surface-applied corrosion inhibitors

- 5.3.1 Penetrating inhibitors

- 5.3.2 Barrier-forming inhibitors

- 5.3.3 Dual-phase inhibitors

- 5.4 Migrating corrosion inhibitors

- 5.4.1 Organic migrating inhibitors

- 5.4.2 Inorganic migrating systems

- 5.5 Emerging technologies

- 5.5.1 Smart/responsive inhibitors

- 5.5.2 Nano-enhanced systems

- 5.5.3 Bio-based inhibitors

Chapter 6 Market Estimates and Forecast, By Application Method, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 New construction applications

- 6.2.1 Concrete mixing stage integration

- 6.2.2 Pre-construction surface treatment

- 6.3 Rehabilitation and repair

- 6.3.1 Surface application methods

- 6.3.2 Injection and impregnation techniques

- 6.4 Maintenance and protection

- 6.4.1 Preventive maintenance programs

- 6.4.2 Emergency repair applications

Chapter 7 Market Estimates and Forecast, By Chemistry Type, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Inorganic inhibitors

- 7.2.1 Nitrite-based systems

- 7.2.2 Phosphate-based compounds

- 7.2.3 Silicate-based inhibitors

- 7.3 Organic inhibitors

- 7.3.1 Aminoalcohol-based systems

- 7.3.2 Amine carboxylate inhibitors

- 7.3.3 Organic acid derivatives

- 7.4 Hybrid and advanced systems

- 7.4.1 Organic-inorganic combinations

- 7.4.2 Nano-enhanced formulations

- 7.4.3 Smart release systems

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Infrastructure and transportation

- 8.2.1 Bridge and highway structures

- 8.2.2 Tunnels and underground construction

- 8.2.3 Marine and port facilities

- 8.2.4 Airport infrastructure

- 8.3 Residential construction

- 8.3.1 High-rise buildings

- 8.3.2 Housing developments

- 8.3.3 Renovation projects

- 8.4 Commercial and industrial

- 8.4.1 Office buildings and complexes

- 8.4.2 Industrial facilities

- 8.4.3 Warehouses and distribution centers

- 8.5 Specialty applications

- 8.5.1 Oil and gas facilities

- 8.5.2 Power generation plants

- 8.5.3 Water treatment infrastructure

- 8.5.4 Chemical processing plants

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Arkema Group

- 10.2 BASF SE

- 10.3 ChemTreat Inc.

- 10.4 CEMEX S.A.B. de C.V.

- 10.5 Clariant AG

- 10.6 Dow Inc.

- 10.7 Ecolab Inc. (Nalco Water)

- 10.8 Evonik Industries AG

- 10.9 GCP Applied Technologies Inc

- 10.10 Halliburton (Production Chemicals Division)

- 10.11 MAPEI S.p.A

- 10.12 Penetron International Ltd.

- 10.13 Pidilite Industries Limited

- 10.14 Sika AG