|

시장보고서

상품코드

1801868

태양광 일체형 건축 자재 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Solar-Integrated Construction Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

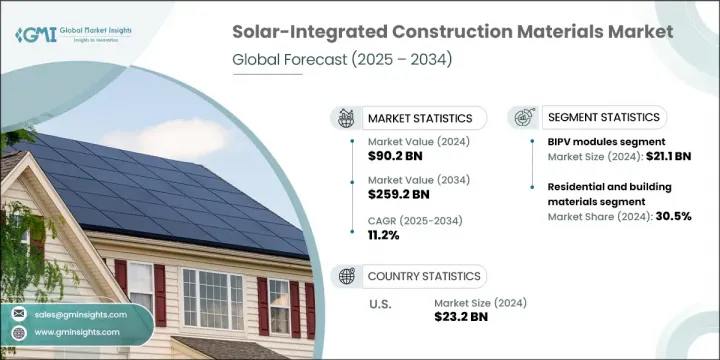

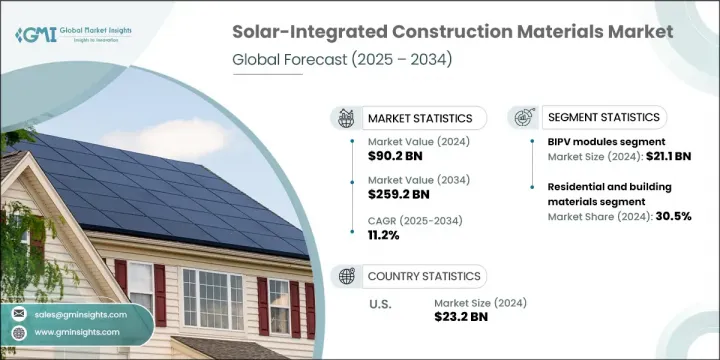

세계의 태양광 일체형 건축 자재 시장 규모는 2024년에는 902억 달러에 달하고, CAGR 11.2%로 성장할 전망이며 2034년에는 2,592억 달러에 달할 것으로 예측되고 있습니다.

태양광 일체형 건축 자재란 태양광 패널(PV)과 같은 태양광 기술이 내장된 건축 제품을 의미합니다. 이러한 자재는 외벽, 지붕, 창문 등 건물의 기능적 구성 요소로 활용되어 재생 에너지를 현장에서 직접 기록할 수 있게 합니다. 이러한 자재를 사용함으로써 건물은 기존 에너지 원에 대한 의존도를 상당한 정도로 줄여 에너지 효율을 향상시킬 수 있습니다.

태양광 일체형 재료에 대한 수요 증가는 정부 정책, 재정적 인센티브, 지속 가능한 발전 및 기후 변화 완화를 위한 전 세계 전환에 의해 촉진되고 있습니다. 또한 에너지 효율적이고 지속 가능한 인프라에 중점을 둔 스마트 시티 개발의 부상은 시장을 더욱 뒷받침하고 있습니다. 전 세계 도시들은 지속 가능성 목표를 달성하기 위해 이러한 기술에 대한 투자를 늘리고 있으며, 이는 해당 부문의 전반적인 성장에 기여하고 있습니다. 기술적 발전과 지원 정책에 주력하는 북미는 가장 빠르게 성장하는 시장입니다. 정책, 혁신, 도시 확장의 복합적 영향이 전 세계 태양광 일체형 건축 자재 시장의 재편을 이끌고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 902억 달러 |

| 예측 금액 | 2,592억 달러 |

| CAGR | 11.2% |

2024년 건물 일체형 태양광(BIPV) 모듈은 211억 달러를 기록하며 시장의 주요 부문으로 자리매김했습니다. BIPV 모듈은 에너지 생산 시스템일 뿐만 아니라 외벽, 지붕, 창문 등 건물 외피의 구조적 요소로도 활용되는 다목적성을 지닙니다. 이러한 다기능성 덕분에 지속가능성 기준을 충족시키면서 건물 미관을 향상시키려는 건축가와 개발자들에게 큰 인기를 끌고 있습니다.

2024년 주거용 및 건축 자재 시장은 전체 시장의 30.5%를 차지했습니다. 에너지 효율적인 주택에 대한 소비자 수요 증가와 탄소 발자국 감축을 목표로 한 정부 인센티브 및 건축 규정이 주거용 건물에 태양광 일체형 자재 채택의 주요 촉진 요인입니다.

2024년 미국의 태양광 일체형 건축 자재 시장은 제조 기술 고급화, 연구개발(R&D) 투자 확대, 친환경 건축 관행 확산에 힘입어 232억 달러 규모로 평가되었습니다. 캐나다 시장 역시 지속가능한 발전과 국가 기후 목표 달성 의지, 친환경 건축 솔루션에 대한 소비자 수요 증가에 의해 촉진되고 있습니다.

세계의 태양광 일체형 건축 자재 시장의 주요 기업으로는 Trina Solar, JA Solar, Panasonic Corporation, AGC Inc., Tesla, JinkoSolar, First Solar, Mitrex Solar, SunPower Corporation, Saule Technologies, Onyx Solar, Sisecam Group, Guardian Glass, LONGi 등이 있습니다. 기업들은 태양광 일체형 건축 자재 시장에서의 입지를 강화하기 위해 다양한 전략적 접근 방식을 채택하고 있습니다. 여기에는 제품 성능 향상 및 혁신적인 태양광 기술을 건축 자재에 통합하기 위한 고급 연구 개발 투자 등이 포함됩니다. 또한 기업들은 건설사 및 개발사와의 전략적 제휴를 통해 시장 진출이 확대되고, 신규 건축 프로젝트에 태양광 솔루션을 통합하고 있습니다. 더불어 기업들은 지속 가능한 관행에 주력하여 자재가 에너지 효율적이고 환경 친화적인 건축 솔루션에 대한 증가하는 수요를 충족하도록 보장하고 있습니다. 정부 기관과의 협력 강화 및 신흥 친환경 건축 기준에 부합하는 제품 포트폴리오 구축 역시 핵심 전략으로 작용하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 산업 고찰

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 산업에 미치는 영향요인

- 성장 촉진요인

- 산업의 잠재적 리스크 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 장래 시장 동향

- 특허 상황

- 무역 통계(HS코드)(주: 무역 통계는 주요 국가만 제공)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속 가능한 사례

- 폐기물 감축 전략

- 생산의 에너지 효율

- 친환경 활동

- 탄소발자국 고려 사항

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정 및 예측 : 제품별(2021-2034년)

- 주요 동향

- BIPV 모듈

- 결정질 실리콘 BIPV 모듈

- 박막 BIPV 모듈

- 페로브스카이트 BIPV 모듈

- 태양광 유리

- 투명 태양광 유리

- 반투명 태양광 유리

- 컬러 태양광 유리

- 태양광 타일과 싱글

- 세라믹 태양광 타일

- 폴리머 태양광 타일

- 일체형 태양 싱글

- 태양광 외벽

- 커튼월 태양광 발전 시스템

- 환기 태양광 외벽

- 이중 벽 태양광 외벽

- 태양광 채광창 및 캐노피

- 투명 태양광 채광

- 반투명 태양광 채광

- 태양 클래딩 시스템

- 기타

- 태양광 단열재

- 태양광막 시스템

- 연질 태양광 필름

제6장 시장 추정 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 주거용

- 단독주택

- 집합 건물

- 주택 리모델링

- 상업용

- 오피스 빌딩

- 소매점과 쇼핑센터

- 호텔과 접객

- 교육기관

- 의료 시설

- 산업용

- 제조 시설

- 창고와 배송 센터

- 산업용 리모델링

- 시설용

- 정부청사

- 종교 시설

- 문화 및 레크리에이션 시설

- 인프라용

- 교통 허브

- 주차장 구조물

- 교량-터널 통합

제7장 시장 추정 및 예측 : 기술별(2021-2034년)

- 주요 동향

- 결정 실리콘 기술

- 단결정 실리콘

- 다결정 실리콘

- 박막 기술

- 비정질 실리콘(a-Si)

- 카드뮴 텔룰라이드(CdTe)

- 구리 인듐 갈륨 셀레늄(CIGS)

- 페로브스카이트 기술

- 납 기반 페로브스카이트

- 무연 페로브스카이트

- 페로브스카이트-실리콘 탠덤

- 유기 태양전지(OPV)

- 저분자 OPV

- 폴리머 OPV

- 하이브리드 기술

- 페로브스카이트 유기 하이브리드

- 실리콘-페로브스카이트 탠덤

- 신흥기술

- 양자점 태양전지

- 색소 증감 태양전지

제8장 시장 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- AGC Inc

- Canadian Solar

- First Solar

- Guardian Glass

- JA Solar

- JinkoSolar

- LONGi

- Mitrex Solar

- Onyx Solar

- Panasonic Corporation

- Saule Technologies

- Sisecam Group

- SunPower Corporation

- Tesla

- Trina Solar

The Global Solar-Integrated Construction Materials Market was valued at USD 90.2 billion in 2024 and is estimated to grow at a CAGR of 11.2% to reach USD 259.2 billion by 2034. Solar-integrated construction materials refer to building products that are embedded with solar technologies, such as photovoltaic (PV) panels. These materials serve as functional components of buildings, including facades, roofing, and windows, enabling the on-site generation of renewable energy. By using such materials, buildings can significantly reduce their reliance on conventional energy sources, improving energy efficiency.

The growing demand for solar-integrated materials is driven by government policies, financial incentives, and a global shift towards sustainable development and climate change mitigation. Additionally, the rise of smart city development, with an emphasis on energy-efficient, sustainable infrastructure, is further supporting the market. Cities worldwide are increasingly investing in such technologies to meet their sustainability targets, contributing to the overall growth of the sector. North America, with its focus on technological advancements and supportive policies, is the fastest-growing market. The combined forces of policy, innovation, and urban expansion are reshaping the global market for solar-integrated construction materials.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $90.2 Billion |

| Forecast Value | $259.2 Billion |

| CAGR | 11.2% |

In 2024, building-integrated photovoltaic (BIPV) modules generated USD 21.1 billion, representing a key segment of the market. BIPV modules are versatile, serving not only as energy-generating systems but also as structural elements for building envelopes, such as facades, roofs, and windows. This multi-functionality makes them highly popular with architects and developers seeking to meet sustainability standards while enhancing building aesthetics.

Residential and building materials made up 30.5% of the market in 2024. Increased consumer demand for energy-efficient homes, along with government incentives and building codes aimed at reducing carbon footprints, are key drivers behind the adoption of solar-integrated materials in residential buildings.

In 2024, the U.S. market for solar-integrated construction materials was valued at USD 23.2 billion, fueled by advancements in manufacturing, research and development (R&D), and a growing push towards green building practices. In Canada, the market is driven by a commitment to sustainable development and the country's climate goals, alongside rising consumer demand for eco-friendly building solutions.

Leading players in the Global Solar-Integrated Construction Materials Market include Trina Solar, JA Solar, Panasonic Corporation, AGC Inc., Tesla, JinkoSolar, First Solar, Mitrex Solar, SunPower Corporation, Saule Technologies, Onyx Solar, Sisecam Group, Guardian Glass, and LONGi. To strengthen their position in the solar-integrated construction materials market, companies are adopting various strategic approaches. These include investing in advanced research and development to enhance product performance and integrate innovative solar technologies into construction materials. Companies are also forming strategic partnerships with construction firms and developers to expand their reach and integrate solar solutions into new building projects. Additionally, firms are focusing on sustainable practices, ensuring their materials meet growing demand for energy-efficient and environmentally friendly building solutions. Increasing collaborations with government bodies and aligning product offerings with emerging green building standards have also been essential strategies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Application trends

- 2.2.3 Technology trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Future market trends

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 BIPV modules

- 5.2.1 Crystalline silicon BIPV modules

- 5.2.2 Thin-film BIPV modules

- 5.2.3 Perovskite BIPV modules

- 5.3 Solar glass

- 5.3.1 Transparent solar glass

- 5.3.2 Semi-transparent solar glass

- 5.3.3 Colored solar glass

- 5.4 Solar tiles and shingles

- 5.4.1 Ceramic solar tiles

- 5.4.2 Polymer solar tiles

- 5.4.3 Integrated solar shingles

- 5.5 Solar facades

- 5.5.1 Curtain wall solar systems

- 5.5.2 Ventilated solar facades

- 5.5.3 Double-skin solar facades

- 5.6 Solar skylights and canopies

- 5.6.1 Transparent solar skylights

- 5.6.2 Semi-transparent solar canopies

- 5.7 Solar cladding systems

- 5.8 Others

- 5.8.1 Solar insulation materials

- 5.8.2 Solar membrane systems

- 5.8.3 Flexible solar films

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Residential applications

- 6.2.1 Single-family homes

- 6.2.2 Multi-family residential buildings

- 6.2.3 Residential retrofits

- 6.3 Commercial applications

- 6.3.1 Office buildings

- 6.3.2 Retail and shopping centers

- 6.3.3 Hotels and hospitality

- 6.3.4 Educational institutions

- 6.4 Healthcare facilities

- 6.5 Industrial applications

- 6.5.1 Manufacturing facilities

- 6.5.2 Warehouses and distribution centers

- 6.5.3 Industrial retrofits

- 6.6 Institutional applications

- 6.6.1 Government buildings

- 6.6.2 Religious buildings

- 6.6.3 Cultural and recreational facilities

- 6.7 Infrastructure applications

- 6.7.1 Transportation hubs

- 6.7.2 Parking structures

- 6.7.3 Bridge and tunnel integration

Chapter 7 Market Estimates and Forecast, By Technology, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Crystalline silicon technology

- 7.2.1 Monocrystalline silicon

- 7.2.2 Polycrystalline silicon

- 7.3 Thin-film technology

- 7.3.1 Amorphous silicon (a-Si)

- 7.3.2 Cadmium telluride (CdTe)

- 7.3.3 Copper indium gallium selenide (CIGS)

- 7.4 Perovskite technology

- 7.4.1 Lead-based perovskites

- 7.4.2 Lead-free perovskites

- 7.4.3 Perovskite-silicon tandems

- 7.5 Organic photovoltaics (OPV)

- 7.5.1 Small molecule OPV

- 7.5.2 Polymer OPV

- 7.6 Hybrid technologies

- 7.6.1 Perovskite-organic hybrids

- 7.6.2 Silicon-perovskite tandems

- 7.7 Emerging technologies

- 7.7.1 Quantum dot solar cells

- 7.7.2 Dye-sensitized solar cells

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 AGC Inc

- 9.2 Canadian Solar

- 9.3 First Solar

- 9.4 Guardian Glass

- 9.5 JA Solar

- 9.6 JinkoSolar

- 9.7 LONGi

- 9.8 Mitrex Solar

- 9.9 Onyx Solar

- 9.10 Panasonic Corporation

- 9.11 Saule Technologies

- 9.12 Sisecam Group

- 9.13 SunPower Corporation

- 9.14 Tesla

- 9.15 Trina Solar