|

시장보고서

상품코드

1801874

액체막 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Liquid Membrane Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

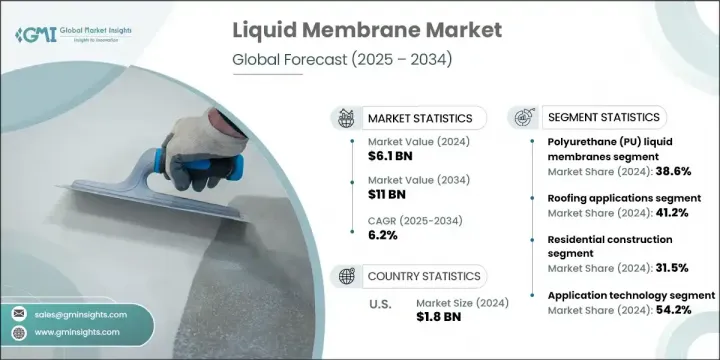

액체막 세계 시장 규모는 2024년에 61억 달러로 평가되었고, CAGR 6.2%로 성장하여 2034년에는 110억 달러에 이를 것으로 예측됩니다.

시장 성장의 주요 요인은 인프라 투자 증가, 건축 요구 사항의 진화, 민관 협력 프로젝트 증가에 기인합니다. 상업용, 주거용, 산업용 구조물 전반에 걸쳐 에너지 효율 의무화 및 방습 규정을 준수하기 위해 액상 멤브레인은 개축 및 신축 프로젝트에서 채택되고 있습니다. 신흥 시장에서는 시트형 멤브레인에 비해 경화가 빠르고 시공이 간편하며 수명이 길어 채택이 증가하고 있습니다. 급속한 도시화, 수직 건축 트렌드, 지속 가능한 건축 인증의 추진도 이 부문에서 폴리우레탄, 아크릴, 시멘트계 배합에 대한 수요를 가속화하고 있습니다.

장기적인 방수 성능과 강력한 내화학성을 제공하는 첨단 액상 멤브레인은 기후가 불안정한 지역의 옥상 데크, 지하실, 노출된 지붕과 같은 까다로운 용도에 점점 더 많이 사용되고 있습니다. 변성 폴리우레탄의 배합은 견고한 접착 특성을 유지하면서 우수한 신장성, 자외선 저항성, 투습성으로 주목받고 있습니다. VOC 함량이 낮은 친환경 아크릴 베이스 멤브레인은 저렴한 가격과 환경 적합성으로 인해 저경사 지붕, 발코니, 금속 구조물에 널리 채택되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 61억 달러 |

| 예측 금액 | 110억 달러 |

| CAGR | 6.2% |

폴리우레탄(PU) 액상 멤브레인 부문은 2024년 전체 매출의 38.6%를 차지했고, 2034년까지 6.8% 이상의 CAGR을 나타낼 것으로 예측됩니다. 탄력성, 자외선 노출에 대한 내구성, 복잡한 건축 설계에 대한 적합성으로 인해 상업용 루핑 및 인프라 프로젝트 모두에 매우 적합합니다. 그 인기는 밀집된 도시 건설지역에서 장수명화를 위해 고성능 방수가 필요한 개보수 공사에서 확대되고 있습니다.

루핑 응용 분야는 2024년 41.2%의 점유율을 차지했으며, 2034년까지 5.6%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 이 부문의 성장은 특히 유럽과 북미 도시 지역의 상업용 건물 및 주택 개보수 투자에 힘입어 성장세를 보이고 있습니다. 액상 멤브레인은 시공의 용이성, 자외선에 대한 내성, 우수한 균열 가교 능력으로 인해 지붕용으로 계속 선호되고 있습니다. 또한, 에너지 절약형 지붕과 태양광 지붕의 설치가 증가하고 있는 것도 전체 지붕재 부문 수요를 뒷받침하고 있습니다.

2024년 미국 액체막 시장 점유율은 82%로 18억 달러에 달했습니다. 이 나라의 우위는 잘 구축된 건설 환경과 방수 및 에너지 절약 건물 외벽에 대한 투자 증가에 기인합니다. 연방 정부의 환경 및 수자원 인프라에 대한 지출은 1,220억 달러를 넘어섰으며, 공공 인프라 개발에서 액상 멤브레인의 역할과 국가 전체의 건물 복구 노력이 더욱 강조되고 있습니다.

세계 액체막 시장을 형성하고 있는 주요 기업으로는 BASF SE, Sika AG, Soprema Group, Tremco Incorporated, Carlisle Companies Inc. 등이 있습니다. 액체 멤브레인 시장에서의 입지를 강화하기 위해 주요 기업들은 몇 가지 전략적 이니셔티브를 전개하고 있습니다. 여기에는 특정 기후와 용도에 맞는 제품 라인의 확대, 더 높은 탄성, 자외선 차단, 환경 적합성을 갖춘 첨단 배합의 연구개발에 대한 대규모 투자가 포함됩니다. 인프라 개발자, 계약자, 건축가와의 파트너십을 통해 대규모 프로젝트를 위한 맞춤형 솔루션을 제공합니다. 또한, 많은 기업들이 지속가능성에 중점을 두고 그린빌딩 기준에 부합하는 저VOC 제품 및 재활용 가능한 제품을 개발하고 있습니다. 특히 성장률이 높은 신흥 시장에서의 지역 확대와 스마트 용도 기술의 통합은 더 넓은 시장 침투와 장기적인 고객 충성도를 높이는 데 도움이 되고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 산업 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 산업에 대한 영향요인

- 성장 촉진요인

- 산업 잠재적 리스크와 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter의 Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 유형별

- 향후 시장 동향

- 기술과 혁신 상황

- 현재 기술 동향

- 신기술

- 특허 상황

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 인수합병(M&A)

- 파트너십 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정·예측 : 제품 유형별, 2021-2034년

- 주요 동향

- 폴리우레탄(PU) 액체막

- 단일 성분 PU 시스템

- 이성분 PU 시스템

- 방향족 PU 막

- 지방족 PU 막

- 바이오 기반 PU 막

- 아크릴액막

- 수성 아크릴 시스템

- 용제계 아크릴계

- 순수 아크릴막

- 개질 아크릴막

- 시멘트질액체막

- 연질 시멘트계

- 경질 시멘트계

- 폴리머 개질 시멘트질

- 결정 방수 시스템

- 하이브리드막 및 특수막

- 폴리우레아 시스템

- 실리콘 기반 막

- 비튜멘 개질 시스템

- 기타 특수 배합

제6장 시장 추정·예측 : 용도별, 2021-2034년

- 주요 동향

- 지붕재 용도

- 평지붕 방수

- 경사 지붕 용도

- 녹색 지붕 시스템

- 지붕 개조 및 보수

- 지하 방수

- 지하실 방수

- 기초 방수

- 지하 구조물

- 터널 방수

- 지상 용도

- 발코니 및 테라스 방수

- 욕실과 습윤 장소 방수

- 파사드 및 벽 보호

- 수영장 방수

- 인프라 용도

- 교량 데크 방수

- 주차장 데크 용도

- 수처리 시설

- 산업용 바닥 코팅

- 특수용도

- 해양 및 앞바다 구조물

- 교통 인프라

- 농업 용도

- 광업 및 중공업

제7장 시장 추정·예측 : 최종 이용 산업별, 2021-2034년

- 주요 동향

- 주택 건설

- 신축 주택 건설

- 주택 개조 및 수리

- 집합주택

- 단독주택

- 상업 건설

- 오피스 빌딩

- 소매점 및 쇼핑센터

- 호스피탈리티 및 엔터테인먼트

- 의료시설

- 산업 건설

- 제조 시설

- 창고 및 배송센터

- 화학 및 프로세스 산업

- 식음료 시설

- 인프라 및 유틸리티

- 교통 인프라

- 물 및 폐수 처리

- 에너지 및 발전

- 정부기관 및 공공시설

제8장 시장 추정·예측 : 기술별, 2021-2034년

- 주요 동향

- 응용 기술

- 냉간 응용 시스템

- 온간 응용 시스템

- 스프레이 도포 시스템

- 브러쉬/롤러 도포 시스템

- 경화 기술

- 습기 경화 시스템

- 열 경화 시스템

- UV 경화 시스템

- 화학 경화 시스템

- 퍼포먼스 기술

- 표준 퍼포먼스 시스템

- 고성능 시스템

- 특수 퍼포먼스 시스템

- 스마트 반응형 시스템

제9장 시장 추정·예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 개요

- Sika AG

- BASF SE

- Tremco Incorporated

- Carlisle Companies Inc.

- Soprema Group

- GAF Materials Corporation

- Johns Manville Corporation

- Firestone Building Products

- Dow Chemical Company

- Huntsman Corporation

- Pidilite Industries Limited(인도)

- Fosroc International Limited(영국)

- MAPEI S.p.A.(이탈리아)

The Global Liquid Membrane Market was valued at USD 6.1 billion in 2024 and is estimated to grow at a CAGR of 6.2% to reach USD 11 billion by 2034. Growth in the market is largely driven by rising infrastructure investments, evolving architectural requirements, and an increase in public-private partnership projects. Renovation and new construction projects are embracing liquid membranes due to their compliance with energy efficiency mandates and moisture protection codes across commercial, residential, and industrial structures. Emerging markets are seeing increased adoption because of the fast-curing nature, easy application, and extended lifespan of these materials compared to sheet membranes. Rapid urbanization, vertical construction trends, and a push for sustainable building certifications are also accelerating demand for polyurethane, acrylic, and cementitious formulations in this space.

Advanced liquid membranes offering long-term waterproofing performance and strong chemical resistance are seeing increased usage in challenging applications like podium decks, basements, and exposed roofs in regions with volatile climates. Modified polyurethane formulations are gaining attention for their superior elongation, UV resistance, and breathability while maintaining solid adhesion properties. Eco-friendly acrylic-based membranes with low VOC content are being widely adopted for use on low-slope roofs, balconies, and metal structures, due to their affordability and environmental compliance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.1 Billion |

| Forecast Value | $11 Billion |

| CAGR | 6.2% |

The polyurethane (PU) liquid membranes segment held the largest share in 2024, contributing 38.6% of total revenue and are expected to grow at over 6.8% CAGR through 2034. Their elasticity, durability under UV exposure, and compatibility with complex architectural designs have made them highly suitable for both commercial roofing and infrastructure projects. Their popularity is expanding across retrofitting works where high-performance waterproofing is required for extended lifespans in dense urban construction zones.

The roofing applications segment held 41.2% share in 2024 and is forecasted to grow at a CAGR of 5.6% through 2034. Growth in this segment is fueled by investments in commercial and residential building upgrades, particularly across urban regions in Europe and North America. Liquid membranes continue to be favored for roofing due to their ease of application, resistance to UV rays, and superior crack-bridging capabilities. Rising installations of energy-saving roofs and solar-compatible designs are also supporting demand across the roofing segment.

United States Liquid Membrane Market held 82% share contributing USD 1.8 billion in 2024. The country's dominance stems from its well-established construction landscape and growing investments in waterproofing and energy-efficient building envelopes. Robust federal spending on environmental and water infrastructure, which topped USD 122 billion, further underscores the role of liquid membranes in public infrastructure development and building recovery efforts across the nation.

Top companies shaping the Global Liquid Membrane Market include BASF SE, Sika AG, Soprema Group, Tremco Incorporated, and Carlisle Companies Inc. To strengthen their presence in the liquid membrane market, leading companies are deploying several strategic initiatives. These include expanding product lines to meet specific climate and application needs, investing heavily in R&D for advanced formulations with higher elasticity, UV protection, and eco-compliance. Partnerships with infrastructure developers, contractors, and architects are enabling customized solutions for large-scale projects. Many players are also focusing on sustainability, developing low-VOC and recyclable products to align with green building standards. Regional expansion, especially in high-growth emerging markets, and the integration of smart application technologies are helping to drive broader market penetration and long-term customer loyalty.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 End use industry

- 2.2.5 Technology

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing construction industry demand

- 3.2.1.2 Infrastructure development and urbanization

- 3.2.1.3 Increasing focus on building durability

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Raw material price volatility

- 3.2.2.2 Technical application challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Sustainable and bio-based solutions

- 3.2.3.2 Smart membrane technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyurethane (PU) liquid membranes

- 5.2.1 Single component PU systems

- 5.2.2 Two-component PU systems

- 5.2.3 Aromatic PU membranes

- 5.2.4 Aliphatic PU membranes

- 5.2.5 Bio-based PU membranes

- 5.3 Acrylic liquid membranes

- 5.3.1 Water-based acrylic systems

- 5.3.2 Solvent-based acrylic systems

- 5.3.3 Pure acrylic membranes

- 5.3.4 Modified acrylic membranes

- 5.4 Cementitious liquid membranes

- 5.4.1 Flexible cementitious systems

- 5.4.2 Rigid cementitious systems

- 5.4.3 Polymer-modified cementitious

- 5.4.4 Crystalline waterproofing systems

- 5.5 Hybrid and specialty membranes

- 5.5.1 Polyurea systems

- 5.5.2 Silicone-based membranes

- 5.5.3 Bitumen-modified systems

- 5.5.4 Other specialty formulations

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Roofing applications

- 6.2.1 Flat roof waterproofing

- 6.2.2 Pitched roof applications

- 6.2.3 Green roof systems

- 6.2.4 Roof renovation and repair

- 6.3 Below-grade waterproofing

- 6.3.1 Basement waterproofing

- 6.3.2 Foundation waterproofing

- 6.3.3 Underground structures

- 6.3.4 Tunnel waterproofing

- 6.4 Above-grade applications

- 6.4.1 Balcony and terrace waterproofing

- 6.4.2 Bathroom and wet area waterproofing

- 6.4.3 Facade and wall protection

- 6.4.4 Swimming pool waterproofing

- 6.5 Infrastructure applications

- 6.5.1 Bridge deck waterproofing

- 6.5.2 Parking deck applications

- 6.5.3 Water treatment facilities

- 6.5.4 Industrial floor coatings

- 6.6 Specialty applications

- 6.6.1 Marine and offshore structures

- 6.6.2 Transportation infrastructure

- 6.6.3 Agricultural applications

- 6.6.4 Mining and heavy industry

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Residential Construction

- 7.2.1 New Residential Construction

- 7.2.2 Residential Renovation and Repair

- 7.2.3 Multi-family Housing

- 7.2.4 Single-family Housing

- 7.3 Commercial Construction

- 7.3.1 Office Buildings

- 7.3.2 Retail and Shopping Centers

- 7.3.3 Hospitality and Entertainment

- 7.3.4 Healthcare Facilities

- 7.4 Industrial Construction

- 7.4.1 Manufacturing Facilities

- 7.4.2 Warehouses and Distribution Centers

- 7.4.3 Chemical and Process Industries

- 7.4.4 Food and Beverage Facilities

- 7.5 Infrastructure and Public Works

- 7.5.1 Transportation Infrastructure

- 7.5.2 Water and Wastewater Treatment

- 7.5.3 Energy and Power Generation

- 7.5.4 Government and Public Buildings

Chapter 8 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Application Technology

- 8.2.1 Cold Applied Systems

- 8.2.2 Hot Applied Systems

- 8.2.3 Spray Applied Systems

- 8.2.4 Brush/Roller Applied Systems

- 8.3 Curing Technology

- 8.3.1 Moisture Curing Systems

- 8.3.2 Heat Curing Systems

- 8.3.3 UV Curing Systems

- 8.3.4 Chemical Curing Systems

- 8.4 Performance Technology

- 8.4.1 Standard Performance Systems

- 8.4.2 High-Performance Systems

- 8.4.3 Specialty Performance Systems

- 8.4.4 Smart and Responsive Systems

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Sika AG

- 10.2 BASF SE

- 10.3 Tremco Incorporated

- 10.4 Carlisle Companies Inc.

- 10.5 Soprema Group

- 10.6 GAF Materials Corporation

- 10.7 Johns Manville Corporation

- 10.8 Firestone Building Products

- 10.9 Dow Chemical Company

- 10.10 Huntsman Corporation

- 10.11 Pidilite Industries Limited (India)

- 10.12 Fosroc International Limited (UK)

- 10.13 MAPEI S.p.A. (Italy)