|

시장보고서

상품코드

1801882

복막 투석 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Peritoneal Dialysis Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

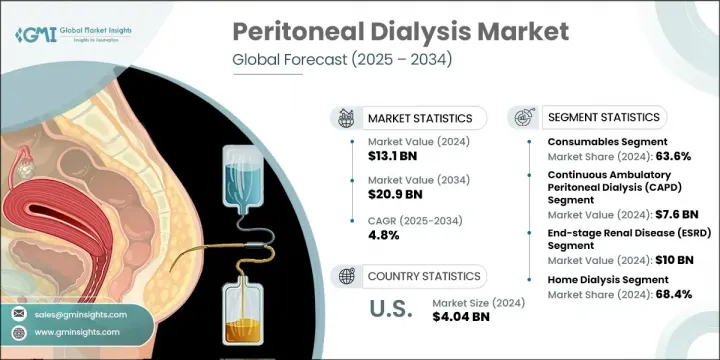

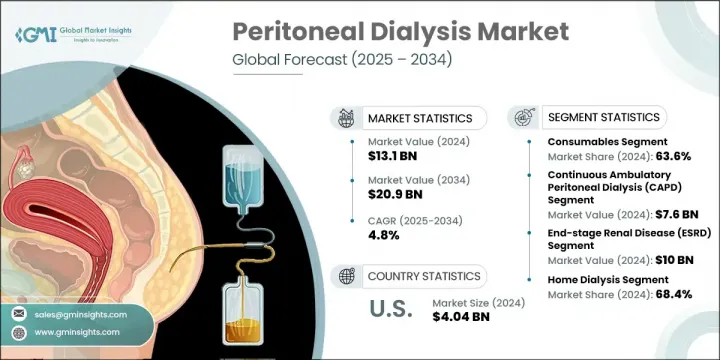

복막 투석 세계 시장 규모는 2024년에 131억 달러로 평가되었고, CAGR4.8%로 성장하여 2034년까지는 209억 달러에 이를 것으로 예측됩니다.

신장 관련 질환의 발병률 증가, 재택 투석 솔루션의 도입 증가, 투석 치료를 지원하는 유리한 상환 제도 등을 주요 요인으로 꼽을 수 있습니다. 또한, 기존 혈액투석보다 비용 효율성이 높고, 신장 기증자 부족 현상이 지속되고 있는 점도 시장 수요를 더욱 증가시키고 있습니다. 복막투석은 말기신부전(ESRD)이나 급성신장질환을 앓고 있는 환자들의 생명유지 요법으로, 신장이 기능을 상실했을 때 노폐물과 과도한 수분을 효과적으로 제거할 수 있습니다. 재택 환자 관리 치료로의 전환이 증가함에 따라 업계 상황을 계속 형성하고 있습니다. 또한, 인구 고령화와 만성신장병 환자 증가는 전 세계 PD 솔루션의 보급에 크게 기여하고 있습니다.

2024년 소모품 부문의 점유율은 63.6%였습니다. 이는 ESRD 환자 증가와 투석액, PD 카테터, 기타 관련 소모품 등 PD에 필수적인 부품에 대한 수요 증가에 기인한 것으로 분석됩니다. 재택 치료로의 전환이 이러한 추세에 큰 영향을 미치고 있으며, 환자가 혼자서 정기적인 투석을 하기 위해서는 이러한 제품의 안정적인 공급이 필요하기 때문입니다. 환자의 소모품에 대한 의존도 증가는 만성 신부전과 급성 신부전, 특히 노인 인구 증가로 인해 만성 신부전 및 급성 신부전 유병률 증가로 인해 더욱 두드러지고 있습니다. 이러한 인구통계학적 변화로 인해 신뢰성이 높고 가정에서 사용할 수 있는 투석액에 대한 수요가 지속적으로 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 131억 달러 |

| 예측 금액 | 209억 달러 |

| CAGR | 4.8% |

지속적 외래 투석(CAPD) 분야는 2024년 76억 달러의 매출을 기록할 것으로 예상되며, 2025년부터 2034년까지 연평균 4.6%의 성장률을 보일 것으로 예측됩니다. CAPD는 자동 투석기에 대한 접근이 제한된 지역에서는 여전히 선호되는 선택입니다. 이 방법은 환자가 기계에 의존하지 않고 하루에 여러 번 수동으로 투석을 할 수 있으며, 저렴한 가격, 사용 편의성, 정상적인 일상 생활을 유지할 수 있는 유연성을 제공합니다. 투석 센터에 대한 의존도를 낮추면서 환자가 자신의 치료에 대한 통제력을 높일 수 있다는 점에서 인기가 높아지고 있습니다.

미국 복막투석 시장은 2024년 40억 4,000만 달러 규모로 2025년부터 2034년까지 연평균 3.5% 성장할 것으로 예측됩니다. PD가 국내에서 받아들여지고 있는 이유는 치료의 유연성, 재택투여, 삶의 질 향상 등 환자 중심의 장점이 있기 때문입니다. 의료 서비스 제공업체들은 특히 의료 시스템이 가치 기반 치료 모델을 채택함에 따라 센터 기반 혈액 투석에 대한 효과적인 대안으로 PD를 권장하고 있습니다. 이러한 증가 추세는 재택투석을 선택하는 환자에 대한 인식이 높아지고 교육 프로그램이 강화되면서 더욱 가속화되고 있습니다.

세계 복막투석 시장을 적극적으로 형성하고 있는 상위권 기업으로는 Terumo, Vantive(Baxter), Diaverum(M42), BD, B. Braun, Davita Kidney Care, Polymed, Utah Medical Products, Vivance, Fresenius Medical Care, medCOMP, Mozarc Medical 등이 있습니다. Vivance, Fresenius Medical Care, medCOMP, Mozarc Medical 등이 있습니다. 시장 지위를 확보하고 경쟁력을 강화하기 위해 복막투석 분야의 기업들은 몇 가지 전략적 이니셔티브를 적극적으로 추진하고 있습니다.

여기에는 보다 진보된 사용자 친화적인 가정용 투석 솔루션으로 제품 포트폴리오를 확장하고, 서비스 제공 네트워크를 강화하기 위해 의료 서비스 제공업체와의 파트너십을 강화하는 등의 노력이 포함됩니다. 많은 기업들이 효율성과 안전성을 높인 차세대 투석기를 개발하기 위해 연구개발에 많은 투자를 하고 있습니다. 또한, 전략적 M&A는 지리적 범위를 넓히고 전문적 역량을 통합하는 데 활용되고 있습니다. 또한, 특히 개발도상국에서 환자들의 도입과 순응도를 높이기 위한 교육 프로그램 및 인식 개선 캠페인도 시작되었습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크와 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술 상황

- 역사적 타임라인과 업계 진화

- 상환 시나리오

- 상환 정책이 시장 성장에 미치는 영향

- 지역별 가격 분석, 2024년

- 투석 장비/사이클러

- 복막 투석 용액/투석액

- 서비스

- 갭 분석

- 소비자 행동 분석

- 역학 전망

- Porter의 Five Forces 분석

- PESTEL 분석

- 향후 시장 동향

- 밸류체인 분석

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 세계 기타 지역(RoW)

- 지역별

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 인수합병(M&A)

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추산·예측 : 카테고리별, 2021년-2034년

- 주요 동향

- 투석 장비/사이클러

- 소모품

- 복막 투석 용액/투석액

- Dextrose

- Icodextrin

- Amino Acid

- 카테터

- 액세스 제품

- 기타 소모품

- 복막 투석 용액/투석액

- 서비스

- 만성 투석

- 급성 투석

- 소모품

제6장 시장 추산·예측 : 유형별, 2021년-2034년

- 주요 동향

- 지속 보행 복막 투석(CAPD)

- 자동 복막 투석(APD)

제7장 시장 추산·예측 : 병상별, 2021년-2034년

- 주요 동향

- 말기 신장 질환(ESRD)

- 급성 신장 장애(AKI)

- 기타 조건

제8장 시장 추산·예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 재택 투석

- 센터내 투석

제9장 시장 추산·예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 개요

- 세계 기업-

- B. Braun

- BD

- Davita Kidney Care

- Diaverum(M42)

- Fresenius Medical Care

- medCOMP

- Mozarc Medical

- Polymed

- Terumo Corporation

- Utah Medical Products

- Vantive(Baxter)

- Vivance

- 지역 기업-

- Apollo Dialysis

- Mitra Industries

- Newsol Technologies

- Northwest Kidney Centers

The Global Peritoneal Dialysis Market was valued at USD 13.1 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 20.9 billion by 2034. Key drivers fueling this expansion include the rising incidence of kidney-related conditions, increasing adoption of home-based dialysis solutions, and favorable reimbursement structures supporting dialysis treatment. Additionally, cost efficiency over traditional hemodialysis, combined with a persistent shortfall in kidney donors, further bolsters market demand. Peritoneal dialysis, a life-sustaining therapy for individuals facing end-stage renal disease (ESRD) and acute kidney injury, allows for the effective removal of waste and excess fluid when the kidneys lose function. A growing shift toward patient-managed care at home continues to shape the industry landscape. Moreover, the aging population and a growing number of patients affected by chronic kidney issues are contributing heavily to the uptake of PD solutions globally.

In 2024, the consumables segment held a 63.6% share. This dominance is largely attributed to a higher volume of ESRD cases and increasing demand for essential PD components such as dialysate solutions, PD catheters, and other related consumables. The shift toward home-based therapies has significantly influenced this trend, as patients require a steady supply of these products to conduct regular sessions independently. This growing patient reliance on consumables is magnified by the rising prevalence of both chronic and acute kidney failures, particularly within the elderly population. These demographic changes continue to push demand for dependable, home-compatible dialysis solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.1 Billion |

| Forecast Value | $20.9 Billion |

| CAGR | 4.8% |

The continuous ambulatory peritoneal dialysis (CAPD) segment generated USD 7.6 billion in 2024 and is forecasted to grow at a 4.6% CAGR during 2025-2034. CAPD remains a preferred choice in regions where access to automated dialysis equipment is limited. This approach enables patients to perform manual exchanges multiple times a day without relying on machines, offering affordability, ease of use, and the flexibility to maintain normal routines. Its growing popularity stems from its ability to empower patients with greater control over their treatment while reducing dependence on dialysis centers.

United States Peritoneal Dialysis Market was valued at USD 4.04 billion in 2024 and is expected to grow at a 3.5% CAGR from 2025 through 2034. The rising acceptance of PD in the country is due to its patient-centric benefits, including treatment flexibility, at-home administration, and improved quality of life. Healthcare providers are increasingly recommending PD as a viable alternative to center-based hemodialysis, especially as the healthcare system embraces value-based care models. This upward trend is further fueled by growing awareness and better training programs for patients opting for home dialysis.

The top-tier companies actively shaping the Global Peritoneal Dialysis Market are Terumo Corporation, Vantive (Baxter), Diaverum (M42), BD, B. Braun, Davita Kidney Care, Polymed, Utah Medical Products, Vivance, Fresenius Medical Care, medCOMP, and Mozarc Medical. To secure their market positions and enhance competitiveness, companies operating in the peritoneal dialysis sector are actively pursuing several strategic initiatives.

These include expanding their product portfolios with more advanced and user-friendly dialysis solutions tailored for home use, as well as forming partnerships with healthcare providers to strengthen service delivery networks. Many firms are investing heavily in R&D to develop next-generation PD devices with improved efficiency and safety profiles. Additionally, strategic mergers and acquisitions are being used to widen geographic reach and integrate specialized capabilities. Training programs and awareness campaigns are also being launched to boost patient adoption and adherence, particularly in developing regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Category trends

- 2.2.3 Type trends

- 2.2.4 Disease condition trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising number of end stage renal diseases (ESRD) patients

- 3.2.1.2 Shortage of donor kidneys

- 3.2.1.3 Cost advantages over hemodialysis

- 3.2.1.4 Favourable reimbursement scenario for dialysis treatment

- 3.2.1.5 Growing prevalence of diabetes and hypertension

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complications in the treatment

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in home dialysis adoption

- 3.2.3.2 Increasing demand in emerging countries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.6 Historical timeline and industry evolution

- 3.7 Reimbursement scenario

- 3.7.1 Impact of reimbursement policies on market growth

- 3.8 Pricing analysis by region, 2024

- 3.8.1 Dialysis machines/cyclers

- 3.8.2 Peritoneal dialysis solution/Dialysate

- 3.8.3 Services

- 3.9 Gap analysis

- 3.10 Consumer behaviour analysis

- 3.11 Epidemiology outlook

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Future market trends

- 3.15 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 By Region

- 4.3.1.1 North America

- 4.3.1.2 Europe

- 4.3.1.3 Asia Pacific

- 4.3.1.4 Rest of the world (RoW)

- 4.3.1 By Region

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Category, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Dialysis machines/Cyclers

- 5.2.1 Consumables

- 5.2.1.1 Peritoneal dialysis solution/Dialysate

- 5.2.1.1.1 Dextrose

- 5.2.1.1.2 Icodextrin

- 5.2.1.1.3 Amino Acid

- 5.2.1.2 Catheters

- 5.2.1.3 Access products

- 5.2.1.4 Other consumables

- 5.2.1.1 Peritoneal dialysis solution/Dialysate

- 5.2.2 Services

- 5.2.2.1 Chronic dialysis

- 5.2.2.2 Acute dialysis

- 5.2.1 Consumables

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Continuous ambulatory peritoneal dialysis (CAPD)

- 6.3 Automated peritoneal dialysis (APD)

Chapter 7 Market Estimates and Forecast, By Disease Condition, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 End-stage renal disease (ESRD)

- 7.3 Acute kidney injury (AKI)

- 7.4 Other conditions

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Home dialysis

- 8.3 In-center dialysis

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 B. Braun

- 10.1.2 BD

- 10.1.3 Davita Kidney Care

- 10.1.4 Diaverum (M42)

- 10.1.5 Fresenius Medical Care

- 10.1.6 medCOMP

- 10.1.7 Mozarc Medical

- 10.1.8 Polymed

- 10.1.9 Terumo Corporation

- 10.1.10 Utah Medical Products

- 10.1.11 Vantive (Baxter)

- 10.1.12 Vivance

- 10.2 Regional players

- 10.2.1 Apollo Dialysis

- 10.2.2 Mitra Industries

- 10.2.3 Newsol Technologies

- 10.2.4 Northwest Kidney Centers