|

시장보고서

상품코드

1801893

스마트 미터 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Smart Meter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

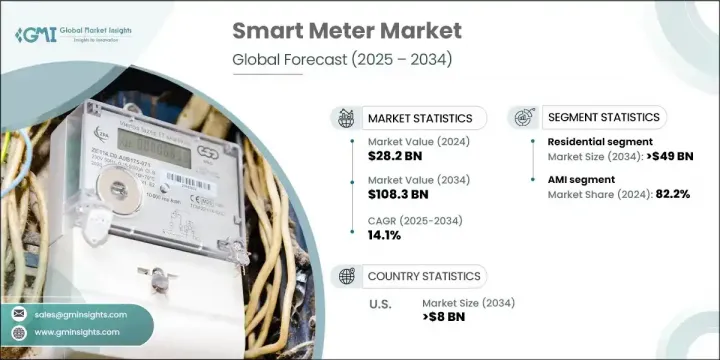

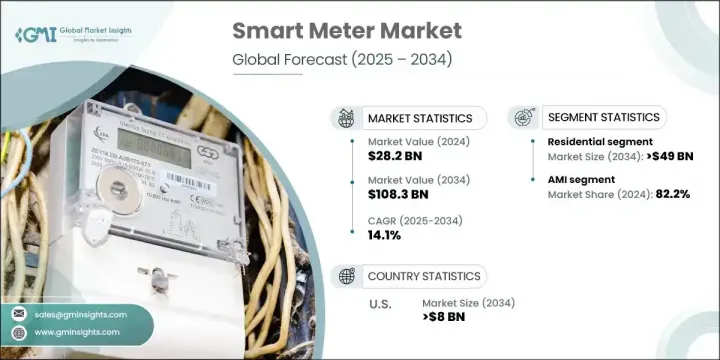

세계의 스마트 미터 시장은 2024년 282억 달러로 평가되었으며 CAGR 14.1%로 성장해 2034년에는 1,083억 달러에 이를 것으로 추정됩니다.

이러한 현저한 성장은 규제 당국의 지원 증가, 계측 기술의 지속적인 혁신, 지속가능한 에너지 사용에 대한 소비자의 관심 증가에 의해 뒷받침되고 있습니다. 디지털화가 진행되고 에너지 사정이 재구성되는 가운데 스마트 미터는 에너지 관리 시스템의 핵심 요소가 되고 있습니다. 이러한 장비는 전력, 가스 및 수도의 소비 데이터를 실시간으로 획득하고 그 정보를 전력 회사에 직접 전송하여 업무 효율성과 청구 정확도를 향상시킵니다.

많은 경제권에서 국가 송전망 업그레이드를 목적으로 한 정부 지원 프로그램으로 스마트 미터는 현대화 전략의 핵심에 자리 잡고 있습니다. 스마트 그리드로의 전환은 신뢰성 향상뿐만 아니라 청정 에너지의 통합과 송전 손실의 최소화로 이어집니다. 이산화탄소 배출량 감소와 에너지 투명성 향상이 보다 중시되는 가운데, 전력회사는 기존의 미터를 양방향 통신과 실시간 분석을 실현하는 지능형 시스템으로 빠르게 교체하고 있습니다. 그리드 최적화, 에너지 절약, 소비자 임파워먼트의 우선순위가 높아짐에 따라 주택, 상업, 산업 분야에서 스마트 미터 시장이 기세를 늘리고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 282억 달러 |

| 예측 금액 | 1,083억 달러 |

| CAGR | 14.1% |

주택 부문은 가정용 에너지 인프라를 현대화하기 위한 광범위한 정부의 이니셔티브에 힘입어 2034년까지 490억 달러에 달할 것으로 예측됩니다. 에너지 효율과 환경 책임에 대한 일반 소비자의 의식이 증가함에 따라 소비자가 스마트 미터 솔루션을 채택하는 데 영향을 미칩니다. 이러한 디지털 미터는 사용자가 실시간 데이터에 액세스할 수 있게 하고 에너지 소비를 보다 적절하게 관리할 수 있게 하며 지속 가능한 생활을 지원하면서 광열비를 절감할 수 있게 합니다. 수요측 관리와 에너지 절약 프로그램이 정착되고 있는 가운데, 주택용 용도 부문은 여전히 성장의 최전선에 있습니다.

고도 계측 인프라(AMI)의 2024년 점유율은 82.2%로, 그 폭넓은 기능이 견인하고 있습니다. AMI는 전력 회사와 최종 사용자 간의 실시간 양방향 데이터 통신을 가능하게 하며 에너지 최적화와 송전망의 신뢰성에 필수적입니다. 원격 검침, 동적 가격, 로드 밸런싱, 신속한 고장 감지 등의 기능을 통해 AMI는 에너지 공급업체가 수요 변화에 적극적으로 대응할 수 있도록 합니다. 이 시스템은 스마트 홈 및 소비자 수준의 에너지 대시보드와 쉽게 통합되어 투명성을 높이고 효율적인 에너지 행동을 촉진합니다.

미국 스마트 미터 시장은 2034년까지 80억 달러에 이르고, 산업과 주택 업그레이드가 기여합니다. 미국에서는 에너지 수요 증가와 재생에너지원의 비율 증가에 대응하기 위해 송전망 인프라의 강화가 진행되고 있습니다. 규제 조치는 고급 모니터링 및 관리 도구를 요구하고 있으며 스마트 미터는 중요한 인프라로 자리 잡고 있습니다. 게다가 스마트 미터는 에너지 집약적인 섹터로 채용이 진행되고 있어 업무 효율, 컴플라이언스, 공급의 신뢰성에 한층 더 부가가치를 가져오고 있습니다.

세계의 스마트 미터 시장을 선도하는 유력한 기업으로는 Siemens, Schneider Electric, Itron, Honeywell International, Landis + Gyr 등이 있습니다. 스마트 미터 업계의 주요 기업은 기술 혁신, 전략적 제휴, 지역 확대를 결합하여 시장에서의 포지셔닝을 강화하고 있습니다. R&D 투자는 여전히 중요한 역할을 하고 있으며, 각 회사는 AI, IoT, 클라우드 기반 애널리틱스를 통합한 차세대 미터 개발에 주력하고 있습니다. 또한 대기업은 전력회사나 정부와 파트너십을 맺어 장기적인 전개계약을 획득하고 있습니다. 증가하는 수요에 대응하기 위해 기업은 생산 능력을 확대하고 전략적 지역에서 제조의 현지화를 진행하고 있습니다. 또한 고객 가치와 운영 신뢰성을 높이기 위해 에너지에 대한 통찰력, 원격 진단 및 예측 서비스를 제공하는 소프트웨어 플랫폼을 포함하여 서비스 제공을 강화하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 규제 상황

- 수출입 무역 분석

- 가격 동향 분석 : 지역별

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- PESTEL 분석

- 새로운 기회와 동향

- 디지털화와 IoT의 통합

- 신흥 시장으로의 침투

- 투자분석과 전망

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석 : 지역별

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 전략적 노력

- 경쟁 벤치마킹의 묘사

- 전략 대시보드

- 혁신과 기술의 상황

제5장 시장 규모와 예측 : 용도별, 2021-2034년

- 주요 동향

- 주택용

- 상업용

- 유틸리티

제6장 시장 규모와 예측 : 기술별, 2021-2034년

- 주요 동향

- AMI

- AMR

제7장 시장 규모와 예측 : 제품별, 2021-2034년

- 주요 동향

- 스마트 가스

- 스마트 워터

- 스마트 전기

제8장 시장 규모와 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스웨덴

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 이집트

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

제9장 기업 프로파일

- Apator SA

- ABB

- AEM

- Aclara Technologies LLC

- ARAD Group

- B Meters Metering Solutions

- Badger Meter, Inc.

- Chint Group

- General Electric

- Honeywell International, Inc.

- Itron, Inc.

- Iskraemeco Group

- Kamstrup

- Larsen & Toubro Limited

- Landis Gyr

- Ningbo Water Meter Co., Ltd.

- Osaki Electric Co., Ltd.

- Raychem RPG Private Limited

- Schneider Electric SE

- Siemens

- Sensus

- Sontex SA

- Wasion Group

The Global Smart Meter Market was valued at USD 28.2 billion in 2024 and is estimated to grow at a CAGR of 14.1% to reach USD 108.3 billion by 2034. This remarkable growth is being fueled by rising regulatory support, continued innovation in metering technologies, and growing consumer focus on sustainable energy usage. As digitalization continues to reshape the energy landscape, smart meters are becoming a central component of energy management systems. These devices capture real-time consumption data for electricity, gas, or water, transmitting the information directly to utilities for improved operational efficiency and billing accuracy.

Across many economies, government-backed programs aimed at upgrading national grids are placing smart meters at the core of their modernization strategies. The transition to smart grids is not only about enhancing reliability but also about integrating clean energy and minimizing transmission losses. With greater emphasis on reducing carbon footprints and improving energy transparency, utility providers are rapidly replacing conventional meters with intelligent systems that deliver two-way communication and real-time analytics. As grid optimization, energy conservation, and consumer empowerment rise in priority, the smart meter market continues to gain momentum across residential, commercial, and industrial sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $28.2 Billion |

| Forecast Value | $108.3 Billion |

| CAGR | 14.1% |

The residential sector is projected to reach USD 49 billion by 2034, supported by widespread government efforts to modernize household energy infrastructure. Increasing public awareness of energy efficiency and environmental responsibility is also influencing consumers to adopt smart metering solutions. These digital meters allow users to access real-time data, offering better control over energy consumption and helping reduce utility bills while supporting sustainable living. With demand-side management and energy-saving programs gaining ground, the residential application segment remains at the forefront of growth.

The advanced metering infrastructure (AMI) held an 82.2% share in 2024, driven by its wide functionality. AMI enables real-time, bidirectional data communication between utility companies and end users, making it essential for energy optimization and grid reliability. Through features such as remote meter reading, dynamic pricing, load balancing, and quick fault detection, AMI allows energy providers to respond proactively to changes in demand. These systems also integrate easily with smart homes and consumer-level energy dashboards, boosting transparency and encouraging efficient energy behaviors.

U.S. Smart Meter Market will reach USD 8 billion by 2034, with contributions coming from industrial and residential upgrades. The country is strengthening its grid infrastructure to handle growing energy demands and a higher share of variable renewable sources. Regulatory actions are pushing for advanced monitoring and management tools, positioning smart meters as critical infrastructure. Additionally, smart meters are seeing adoption in energy-intensive sectors, adding further value to operational efficiency, compliance, and supply reliability.

Prominent players leading the Global Smart Meter Market include Siemens, Schneider Electric, Itron, Honeywell International, and Landis + Gyr. Major companies in the smart meter industry are enhancing their market positioning through a mix of innovation, strategic alliances, and regional expansion. Investments in R&D continue to play a key role, with companies focusing on developing next-generation meters that integrate AI, IoT, and cloud-based analytics. Leading firms are also forming partnerships with utility providers and governments to win long-term deployment contracts. To meet growing demand, businesses are expanding production capabilities and localizing manufacturing in strategic regions. Furthermore, they are strengthening their service offerings by including software platforms that provide energy insights, remote diagnostics, and predictive maintenance to enhance customer value and operational reliability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Import/Export trade analysis

- 3.4 Price trend analysis, by region (USD/Unit)

- 3.5 Industry impact forces

- 3.5.1 Growth drivers

- 3.5.2 Industry pitfalls & challenges

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitutes

- 3.8 PESTEL analysis

- 3.8.1 Political factors

- 3.8.2 Economic factors

- 3.8.3 Social factors

- 3.8.4 Technological factors

- 3.8.5 Legal factors

- 3.8.6 Environmental factors

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Emerging market penetration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking depictions

- 4.5 Strategy dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & '000 Units)

- 5.1 Key trends

- 5.2 Residential

- 5.3 Commercial

- 5.4 Utility

Chapter 6 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million & '000 Units)

- 6.1 Key trends

- 6.2 AMI

- 6.3 AMR

Chapter 7 Market Size and Forecast, By Product, 2021 - 2034 (USD Million & '000 Units)

- 7.1 Key trends

- 7.2 Smart gas

- 7.3 Smart water

- 7.4 Smart electric

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & '000 Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Sweden

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 Saudi Arabia

- 8.5.3 South Africa

- 8.5.4 Egypt

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Mexico

- 8.6.3 Argentina

Chapter 9 Company Profiles

- 9.1 Apator SA

- 9.2 ABB

- 9.3 AEM

- 9.4 Aclara Technologies LLC

- 9.5 ARAD Group

- 9.6 B Meters Metering Solutions

- 9.7 Badger Meter, Inc.

- 9.8 Chint Group

- 9.9 General Electric

- 9.10 Honeywell International, Inc.

- 9.11 Itron, Inc.

- 9.12 Iskraemeco Group

- 9.13 Kamstrup

- 9.14 Larsen & Toubro Limited

- 9.15 Landis + Gyr

- 9.16 Ningbo Water Meter Co., Ltd.

- 9.17 Osaki Electric Co., Ltd.

- 9.18 Raychem RPG Private Limited

- 9.19 Schneider Electric SE

- 9.20 Siemens

- 9.21 Sensus

- 9.22 Sontex SA

- 9.23 Wasion Group