|

시장보고서

상품코드

1801905

콘크리트 포장 장비 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Concrete Paving Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

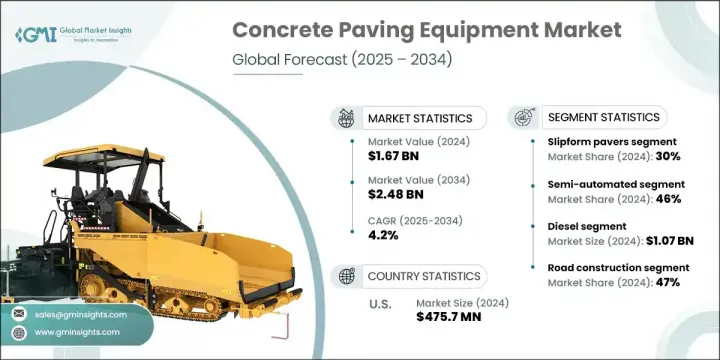

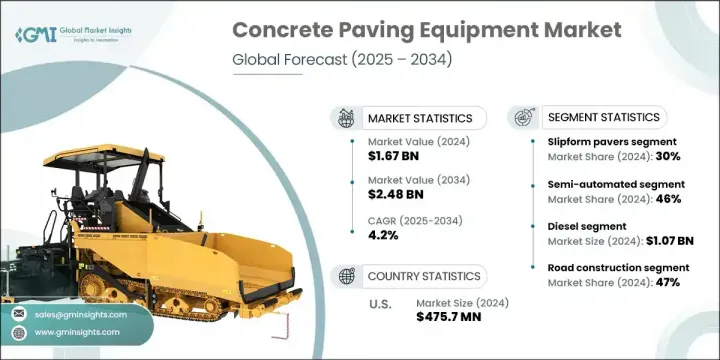

콘크리트 포장 장비 세계 시장 규모는 2024년에 16억 7,000만 달러로 평가되었고, CAGR 4.2%로 성장하여 2034년에는 24억 8,000만 달러에 이를 것으로 예측됩니다.

이러한 꾸준한 증가는 세계 인프라 개발, 특히 도로, 고속도로, 다리 및 공항 건설에 지속적인 기세가 있기 때문입니다. 특히 신흥국에서는 혼잡을 완화하고 경제 확대를 지원하기 위해 정부가 교통 개선을 우선시하고 있습니다. 고정밀 도로 공사와 장기적인 내구성을 중시하게 되어 최신의 포장 설비에 대한 신뢰가 높아지고 있습니다. 콘크리트 포장 시스템도 자동화로의 전환이 급속히 진행되고 있으며, 제조업체는 AI, GPS, 텔레매틱스를 기계에 내장하여 포장 정밀도와 작업 효율을 높이고 있습니다. 머신러닝을 지원하는 예지보전 시스템은 가동 중지 시간을 최소화하고 현장 성능을 최적화함으로써 입지를 다지고 있습니다.

슬립폼 페이버(Slipform Paver) 부문은 2024년에 30%의 점유율을 차지하며, 2034년까지 연평균 복합 성장률(CAGR) 5%로 성장할 것으로 예측됩니다. 이 기계는 사전 설치된 측면 거푸집 없이 연속적인 콘크리트 타설을 수행하므로 대규모 용도에 이상적입니다. 이 시장은 기업이 대규모 인프라 공사에서 속도와 표면 품질 향상을 요구하고 있기 때문에 이러한 고성능 기계에 대한 수요가 높아지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 16억 7,000만 달러 |

| 예측 금액 | 24억 8,000만 달러 |

| CAGR | 4.2% |

2024년 반자동 포장 기계 부문은 46%의 점유율을 기록했으며 2034년까지 4%의 성장이 예상됩니다. 이 기계는 수동 제어와 자동 지침 시스템의 융합을 제공하여 재료의 분배와 마무리를 보다 정확하게 수행합니다. 센서 어시스트 유압 및 GPS 가이드 스티어링과 같은 첨단 기술로 이러한 기계는 보다 효율적이고 비용 효율적이며 성능과 작동 유연성이 균형을 이룹니다.

미국 콘크리트 포장 장비 시장은 85%의 점유율을 차지하며, 2024년에는 4억 7,570만달러의 수익을 올렸습니다. 인프라 재생을 지원하는 연방 정부의 강력한 프로그램이 최신 포장 시스템의 채택을 가속화하고 있습니다. 정부의 주요 정책은 자동 머신 가이던스(AMG)와 같은 기술의 통합을 강조합니다. AMG는 위성 기반 포지셔닝을 활용하여 보다 뛰어난 그라디언트 제어, 포장 균일성 및 재료 활용을 실현합니다. 이 나라는 자동화를 선호하고 연방 정부로부터 일관된 자금 지원을 받고 있기 때문에 업계의 최전선에 군림을 계속하고 있습니다.

콘크리트 포장 장비 세계 시장에서 주요 기업은 Gomaco Corporation, Bid-well, Caterpillar, BESSER, Wirtgen Group, Ammann Group, SANY Group 등입니다. 시장에서의 지위를 강화하기 위해, 주요 기업은 기술 혁신, 기술통합, 세계전개에 초점을 맞춘 전략을 조합하여 활용하고 있습니다. 개발 업체는 대규모 포장 프로젝트와 소규모 포장 프로젝트를 모두 지원하는 모듈식, 적응성이 높은 장비를 적극적으로 개발하고 있습니다. 인프라 개발자와의 전략적 제휴는 장기 계약 확보에 도움이 됩니다. 또한 스마트 센서 및 텔레매틱스와 같은 고급 자동화 기능에 투자하여 효율성을 높이고 노동력에 대한 의존도를 줄입니다. 기계 제어 시스템과 AI를 활용한 유지 보수 도구의 지속적인 개선으로 가동률 향상을 실현하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 원재료 공급업체

- 부품 공급업체

- Tier 1 OEM

- 딜러/유통업체

- 애프터마켓 서비스

- 최종 용도

- 비용 구조

- 이익률

- 각 단계에서의 부가가치

- 공급망에 영향을 미치는 요인

- 방해요소

- 공급자의 상황

- 영향요인

- 성장 촉진요인

- 도시화와 인프라 정비의 개발

- 현대의 포장 기계의 진보의 향상

- 도로의 안전성과 내구성에 대한 중점 증가

- 신흥 시장의 경제 확대

- 업계의 잠재적 위험 및 과제

- 숙련 노동자의 부족

- 원재료 가격 변동

- 시장 기회

- 렌탈 및 리스 서비스

- 스마트 및 자율 포장 기술

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 생산 통계

- 생산과 소비의 중심지

- 수출입 분석

- 무역 흐름 패턴

- 기술과 혁신의 상황

- 현재의 기술

- 스트링리스 포장 기술의 우위성

- 지능형 제어 시스템의 진화

- 신흥기술

- 인공지능(AI)과 머신러닝(ML)의 통합

- 사물인터넷(IoT)과 연결혁명

- 스마트 재료와 콘크리트의 혁신

- 전동화와 대체 파워트레인

- 디지털 트윈과 빌딩 정보 모델링

- 혁신 생태계와 파트너십

- 기술 파트너십 전략

- 혁신 가속 메커니즘

- 현재의 기술

- 특허 분석

- 규제 상황

- 북미

- 규제 프레임 워크의 아키텍처

- 컴플라이언스 비용의 영향

- 유럽

- EU 규제의 조화

- 기술 통합 요건

- 아시아태평양

- 중국의 규제 진화

- 지역 조화 노력

- 라틴아메리카

- 중동 및 아프리카

- 북미

- 가격 동향

- 과거의 가격 추이

- 주요 지역의 가격 동향

- 북미의 가격 패턴

- 아시아태평양의 비용 우위성

- 유럽 프리미엄 시장에서의 포지셔닝

- 가격 탄력성과 감도 분석

- 가격요인분석

- 미래의 가격 예측

- 비용 분석

- 비용 내역 분석

- 주요 시사점

- 미래 시장의 진화

- 지속가능성 주도 시장변혁

- 스마트건설 생태계 진화

- 성능 기반 사양 혁명

- 신속한 배송 필요성

- 시나리오 계획과 전략적 대응

- 무역 흐름 분석

- HS 코드 분류 프레임워크

- 주요 기기의 분류

- 제품 및 재료 분류

- 세계 무역 흐름 패턴

- 건설 업계의 무역개요

- 콘크리트 포장 장비 무역 흐름

- 항만과 물류의 분석

- 관세 및 무역정책 분석

- 미국의 무역 정책의 틀

- 국제무역규제

- HS 코드 분류 프레임워크

- 지속가능성 분석

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적 노력

- 탄소발자국 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획과 자금조달

제5장 시장 추정 및 예측 : 제품별, 2021년-2034년

- 주요 동향

- 슬립 폼 포장재

- 롤러 포장 기계

- 콘크리트 스프레더

- 배치 포장 기계

제6장 시장 추정 및 예측 : 기술별, 2021년-2034년

- 주요 동향

- 매뉴얼

- 반자동

- 완전 자동화

제7장 시장 추정 및 예측 : 전원별, 2021년-2034년

- 주요 동향

- 디젤

- 전기

- 하이브리드

제8장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 주택 건설

- 도로 건설

- 상업 건설

- 기타

제9장 시장 추정 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 정부기관

- 건설회사

- 렌탈회사

제10장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 세계기업

- Caterpillar

- CMI Roadbuilding

- Dynapac

- Fayat Group

- Gomaco Corporation

- JCB

- Komatsu

- Liebherr

- SANY Group

- Terex Corporation(Bid-Well)

- Volvo CE

- Wirtgen Group

- XCMG Group

- 지역 기업

- BESSER

- Guntert &Zimmerman

- HEM Paving Equipment

- Power Curbers Companies

- SCHWING Stetter

- 신흥기업

- Aimix Group

- Curb Fox

The Global Concrete Paving Equipment Market was valued at USD 1.67 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 2.48 billion by 2034. This steady rise is attributed to ongoing momentum in global infrastructure development, particularly across the construction of roads, highways, bridges, and airports. A surge in urbanization is fueling infrastructure investments, especially in emerging economies, where governments are prioritizing transportation upgrades to reduce congestion and support economic expansion. The increased focus on high-precision roadwork and long-term durability has created greater reliance on modern paving equipment. Concrete paving systems are also seeing a rapid shift toward automation, with manufacturers integrating AI, GPS, and telematics into machines to enhance paving precision and operational efficiency. Predictive maintenance systems, supported by machine learning, are gaining ground by minimizing downtime and optimizing field performance.

The slipform pavers segment held a 30% share in 2024 and is projected to grow at a CAGR of 5% through 2034. These machines deliver continuous concrete placement without requiring pre-installed side forms, making them ideal for large-scale applications. The market is experiencing rising demand for such high-performance machinery as companies look to enhance speed and surface quality across major infrastructure jobs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.67 Billion |

| Forecast Value | $2.48 Billion |

| CAGR | 4.2% |

In 2024, the semi-automated paving machines segment captured a 46% share and is expected to grow at 4% through 2034. These machines offer a blend of manual control with automated guidance systems that ensure material is distributed and finished more accurately. Advanced technologies like sensor-assisted hydraulics and GPS-guided steering make these units more efficient and cost-effective, balancing performance with operational flexibility.

United States Concrete Paving Equipment Market held an 85% share and generated USD 475.7 million in 2024. The strong presence of federal programs supporting infrastructure revitalization continues to accelerate the adoption of modern paving systems. Key government policies are emphasizing the integration of technologies like Automatic Machine Guidance (AMG), which leverages satellite-based positioning for better grade control, paving uniformity, and material utilization. The country's preference for automation and consistent federal funding has kept it at the forefront of industry.

The leading players in the Global Concrete Paving Equipment Market include Gomaco Corporation, Bid-well, Caterpillar, BESSER, Wirtgen Group, Ammann Group, and SANY Group. To strengthen their market position, key companies are leveraging a combination of strategies that focus on innovation, technology integration, and global expansion. Manufacturers are actively developing modular and adaptable equipment that supports both large- and small-scale paving projects. Strategic collaborations with infrastructure developers are helping them secure long-term contracts. They are also investing in advanced automation features like smart sensors and telematics to increase efficiency and reduce labor dependency. Continuous improvements in machine control systems and AI-driven maintenance tools are enabling better uptime.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Data mining sources

- 1.2.1 Global

- 1.2.2 Regional/Country

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Type

- 2.2.4 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Tier 1 OEMs

- 3.1.1.4 Dealers/distributors

- 3.1.1.5 Aftermarket services

- 3.1.1.6 End use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing urbanization and infrastructure development

- 3.2.1.2 Raising advancements in modern paving machines

- 3.2.1.3 Increasing focus on road safety and durability

- 3.2.1.4 Economic expansion in emerging markets

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Skilled Labor Shortage

- 3.2.2.2 Volatility in Raw Material Prices

- 3.2.3 Market opportunities

- 3.2.3.1 Rental & leasing services

- 3.2.3.2 Smart & autonomous paving technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Production statistics

- 3.6.1 Production and consumption hubs

- 3.6.2 Export and import analysis

- 3.6.3 Trade flow patterns

- 3.7 Technology & innovation landscape

- 3.7.1 Current technologies

- 3.7.1.1 Stringless paving technology dominance

- 3.7.1.2 Intelligent control systems evolution

- 3.7.2 Emerging technologies

- 3.7.2.1 Artificial intelligence (AI) and machine learning (ML) integration

- 3.7.2.2 Internet of Things (IoT) and connectivity revolution

- 3.7.2.3 Smart materials and concrete innovation

- 3.7.2.4 Electrification and alternative powertrains

- 3.7.2.5 Digital twin and building information modeling

- 3.7.3 Innovation ecosystem and partnerships

- 3.7.3.1 Technology partnership strategy

- 3.7.3.2 Innovation acceleration mechanisms

- 3.7.1 Current technologies

- 3.8 Patent analysis

- 3.9 Regulatory landscape

- 3.9.1 North America

- 3.9.1.1 Regulatory framework architecture

- 3.9.1.2 Compliance cost implications

- 3.9.2 Europe

- 3.9.2.1 EU Regulatory Harmonization

- 3.9.2.2 Technology integration requirements

- 3.9.3 Asia Pacific

- 3.9.3.1 China's regulatory evolution

- 3.9.3.2 Regional harmonization efforts

- 3.9.4 Latin America

- 3.9.5 Middle East & Africa

- 3.9.1 North America

- 3.10 Price trends

- 3.10.1 Historical price trajectory

- 3.10.2 Major regions price dynamics

- 3.10.2.1 North American pricing patterns

- 3.10.2.2 Asia-Pacific cost advantages

- 3.10.2.3 European premium positioning

- 3.10.3 Price elasticity and sensitivity analysis

- 3.10.4 Price driver analysis

- 3.10.5 Future price projection

- 3.11 Cost breakdown analysis

- 3.11.1 Analysis of the cost breakdown

- 3.11.2 Key takeaways

- 3.12 Future market evolution

- 3.12.1 Sustainability-driven market transformation

- 3.12.2 Smart construction ecosystem evolution

- 3.12.3 Performance-based specification revolution

- 3.12.4 Accelerated delivery imperatives

- 3.12.5 Scenario planning and strategic responses

- 3.13 Trade flow analysis

- 3.13.1 HS code classification framework

- 3.13.1.1 Primary equipment classifications

- 3.13.1.2 Product and material classifications

- 3.13.2 Global trade flow patterns.

- 3.13.2.1 Construction industry trade overview

- 3.13.2.2 Concrete paving equipment trade flows

- 3.13.2.3 Port and logistics analysis

- 3.13.3 Tariff and trade policy analysis.

- 3.13.3.1 U.S. trade policy framework.

- 3.13.3.2 International trade regulations

- 3.13.1 HS code classification framework

- 3.14 Sustainability analysis

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly initiatives

- 3.14.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Slipform pavers

- 5.3 Roller pavers

- 5.4 Concrete spreaders

- 5.5 Batch pavers

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automated

- 6.4 Fully automated

Chapter 7 Market Estimates & Forecast, By Power Source, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Diesel

- 7.3 Electric

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Residential construction

- 8.3 Road construction

- 8.4 Commercial construction

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Government agencies

- 9.3 Construction companies

- 9.4 Rental companies

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 North America

- 10.1.1 U.S.

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Caterpillar

- 11.1.2 CMI Roadbuilding

- 11.1.3 Dynapac

- 11.1.4 Fayat Group

- 11.1.5 Gomaco Corporation

- 11.1.6 JCB

- 11.1.7 Komatsu

- 11.1.8 Liebherr

- 11.1.9 SANY Group

- 11.1.10 Terex Corporation (Bid-Well)

- 11.1.11 Volvo CE

- 11.1.12 Wirtgen Group

- 11.1.13 XCMG Group

- 11.2 Regional Players

- 11.2.1 BESSER

- 11.2.2 Guntert & Zimmerman

- 11.2.3 HEM Paving Equipment

- 11.2.4 Power Curbers Companies

- 11.2.5 SCHWING Stetter

- 11.3 Emerging Players

- 11.3.1 Aimix Group

- 11.3.2 Curb Fox