|

시장보고서

상품코드

1801943

경성 내시경 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Rigid Endoscopes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

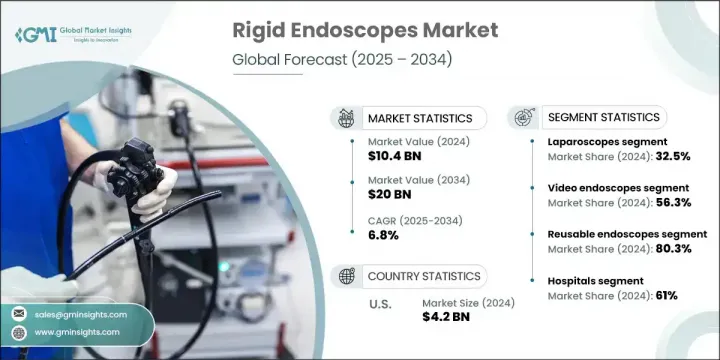

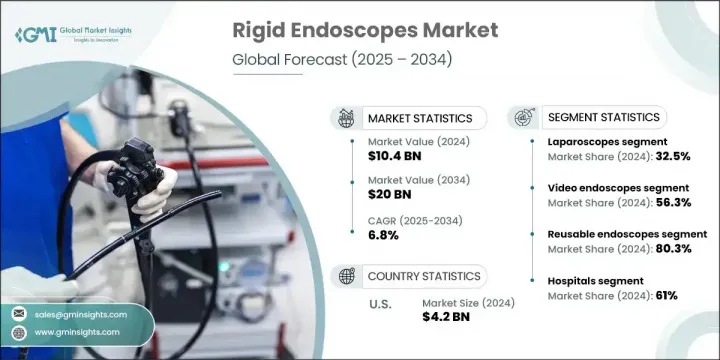

세계 경성 내시경 시장은 2024년에는 104억 달러로 평가되었고, CAGR 6.8%로 성장하여 2034년에는 200억 달러에 이를 것으로 추정됩니다.

시장 확대의 주요 요인은 만성 건강 문제의 발생률 증가와 세계 인구의 고령화입니다. 경성 내시경은 호흡기 합병증, 소화기계 질환, 이비인후과 질환을 포함한 광범위한 질병의 진단과 치료를 돕는 낮은 침습 치료를 시행하는 데 필수적입니다. 이 장치는 선명한 이미지를 제공하며 복강, 관절, 생식기, 방광 등 수술에 널리 적용됩니다. 회복이 빠르고, 합병증이 적고, 입원기간이 짧기 때문에 저침습 기술에 대한 환자의 선호가 높아지고 있는 것이, 수요를 늘리는 데 중요한 역할을 하고 있습니다. 또한, 고화질 이미지와 수술 네비게이션 도구의 진보로 외래 및 입원 치료에서의 채택이 더욱 진행되고 있습니다.

복강경 부문은 2024년에 32.5%의 점유율을 차지했고 담낭 적출, 탈장 수리, 부인과 수술 등 수술 후 통증을 최소화하고 입원 기간을 단축하는 수술 등 인기가 높아지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작금액 | 104억 달러 |

| 예측 금액 | 200억 달러 |

| CAGR | 6.8% |

비디오 내시경의 2024년 점유율은 56.3%로 실시간으로 고화질 이미지를 제공할 수 있다는 점에 힘입어 견인하고 있습니다. 또한 이러한 도구는 수술 중 팀 협업을 촉진하며 수술 부서 전체에서 매우 선호됩니다.

미국의 경성 내시경 시장은 견고한 건강 관리 인프라와 낮은 침습 수술 절차의 광범위한 도입에 힘입어 2024년에는 42억 달러에 달했습니다. 강력한 상환 체제, 노인 인구 증가 및 조기 진단 스크리닝 증가로 인해 지역 수요가 계속 강화되고 있습니다. 수술 건수 증가, 선진적인 화상 기술 혁신, 외래 환자에 의한 수술에 대한 주목이 이 기세를 지속시키고 있습니다. 미국의 주요 제조업체나 의료기술 혁신기업도 내시경의 연구개발 및 자동화에 많은 투자를 하고 있습니다.

시장 상황을 형성하는 주요 기업은 Stryker, Olympus Corporation, Richard Wolf, Karl Storz, Smith &Nephew, 후지 필름, Scholly Fiberoptic, Arthrex, PENTAX Medical, ConMed, B. Braun, Henke-Sass, Wolf, Cook Medical, XI A/S등이 있습니다. 경성 내시경 시장에서 각 사가 채용하고 있는 주요 전략에는 AI 지원 이미징, 인체공학을 기반으로 한 기구 설계, 수술 정밀도를 향상시키는 통합 비디오 시스템 등에 의한 제품 혁신의 추진이 포함됩니다. 제품 포트폴리오를 확대하고 미개척 지역에 진입하기 위해 합병, 전략적 제휴 및 인수가 일반적입니다. 각 회사는 낮은 침습 플랫폼을 강화하고 로봇 내시경 기술을 탐구하기 위해 연구 개발에 많은 투자를하고 있습니다. 또한 많은 기업들이 애프터서비스망을 강화하고 의사의 교육 프로그램에 임하고 있어 보급을 추진하고 있습니다. 수술센터와 의료기관과의 제휴는 조기 임상 도입을 지원하고 시장에의 침투를 세계적으로 높이고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성 질환 증가

- 기술적 진보

- 저침습 수술의 도입 증가

- 건강 의식의 고조와 조기 진단 수요

- 업계의 잠재적 위험 및 과제

- 높은 기기 비용

- 환자의 불쾌감과 절차의 제한 위험

- 시장 기회

- 외래 및 외래수술센터(ASC)의 확장

- 헬스케어 인프라가 정비되고 있는 신흥 시장

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술의 상황

- 현재의 기술 동향

- 신흥기술

- 상환 시나리오

- 가격 분석, 2024

- 장래 시장 동향

- 시장 진출 전략

- 파이프라인 분석

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 밸류체인 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추정 및 예측 : 제품 유형별, 2021년-2034년

- 주요 동향

- 복강경

- 관절경

- 방광경

- 이비인후과 내시경

- 기관지경

- 요관경

- 자궁경

- 기타 제품 유형

제6장 시장 추정 및 예측 : 기술별, 2021년-2034년

- 주요 동향

- 기존 내시경

- 비디오 내시경

- 광섬유 내시경

제7장 시장 추정 및 예측 : 사용성별, 2021년-2034년

- 주요 동향

- 재사용 가능한 내시경

- 일회용 내시경

제8장 시장 추정 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 기타 용도

제9장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Ambu

- Arthrex

- B. Braun

- Boston Scientific

- ConMed

- Cook

- Fujifilm

- Henke-Sass Wolf

- Olympus

- PENTAX Medical

- Richard Wolf

- Scholly Fiberoptic

- Smith &Nephew

- Storz

- Stryker

- XION medical

The Global Rigid Endoscopes Market was valued at USD 10.4 billion in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 20 billion by 2034. Market expansion is largely driven by the rising incidence of chronic health issues and an aging global population. Rigid endoscopes are essential for performing minimally invasive procedures that aid in diagnosing and treating a wide range of conditions, including respiratory complications, digestive system ailments, and ENT disorders. These devices deliver crystal-clear imaging and are widely applied in surgeries involving the abdominal cavity, joints, reproductive system, and urinary bladder. Increasing patient preference for minimally invasive techniques-because of faster recovery, fewer complications, and lower hospitalization times-is playing a vital role in boosting demand. Additionally, ongoing advancements in high-definition imaging and surgical navigation tools further reinforce their adoption in both outpatient and inpatient care.

The laparoscopes category held 32.5% share in 2024, fueled by the expanding popularity of procedures like gallbladder removal, hernia repair, and gynecological surgeries that minimize post-operative pain and shorten hospital stays.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.4 Billion |

| Forecast Value | $20 Billion |

| CAGR | 6.8% |

The video endoscopes segment held 56.3% share in 2024, driven by their ability to deliver real-time, high-definition visualization, which enhances surgical precision and clinical documentation. These tools also facilitate team collaboration during operations, making them highly preferred across surgical departments.

U.S. Rigid Endoscopes Market generated USD 4.2 billion in 2024, supported by robust healthcare infrastructure and wide-scale adoption of minimally invasive surgical techniques. Strong reimbursement frameworks, a growing elderly population, and an uptick in early diagnostic screenings continue to bolster regional demand. Rising surgical volumes, advanced imaging innovations, and a focus on outpatient procedures across the country are sustaining this momentum. Leading manufacturers and medtech innovators in the U.S. are also channeling substantial investments into endoscopic R&D and automation.

Top players shaping the Rigid Endoscopes Market landscape include Stryker, Olympus Corporation, Richard Wolf, Karl Storz, Smith & Nephew, Fujifilm, Scholly Fiberoptic, Arthrex, PENTAX Medical, ConMed, B. Braun, Henke-Sass, Wolf, Cook Medical, XION GmbH, Boston Scientific, and Ambu A/S. Key strategies adopted by companies in the rigid endoscopes market include advancing product innovation through AI-assisted imaging, ergonomic instrument design, and integrated video systems to improve surgical precision. Mergers, strategic partnerships, and acquisitions are common to expand product portfolios and enter untapped geographic areas. Players are heavily investing in R&D to enhance minimally invasive platforms and explore robotic endoscopic technologies. Many are also strengthening after-sales service networks and engaging in physician training programs to drive adoption. Collaborations with surgical centers and institutions support early clinical adoption and increase market penetration globally.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Technology trends

- 2.2.3 Usability trends

- 2.2.4 End use trends

- 2.2.5 Region trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of chronic conditions

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rising adoption of minimally invasive surgeries

- 3.2.1.4 Increasing health awareness and demand for early-stage diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High device cost

- 3.2.2.2 Risk of patient discomfort and procedural limitations

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of outpatient and ambulatory surgical centers (ASCs)

- 3.2.3.2 Emerging markets with improving healthcare infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Pricing analysis, 2024

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.7.4 Latin America

- 3.7.5 Middle East and Africa

- 3.8 Future market trends

- 3.9 Go-to-market strategy

- 3.10 Pipeline analysis

- 3.11 Gap analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 Latin America

- 4.3.6 MEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn and Units)

- 5.1 Key trends

- 5.2 Laparoscopes

- 5.3 Arthroscopes

- 5.4 Cystoscopes

- 5.5 ENT endoscopes

- 5.6 Bronchoscopes

- 5.7 Ureteroscopes

- 5.8 Hysteroscopes

- 5.9 Other product types

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Conventional endoscopes

- 6.3 Video endoscopes

- 6.4 Fiber-optic endoscopes

Chapter 7 Market Estimates and Forecast, By Usability, 2021 - 2034 ($ Mn and Units)

- 7.1 Key trends

- 7.2 Reusable endoscopes

- 7.3 Disposable endoscopes

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn and Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Ambu

- 10.2 Arthrex

- 10.3 B. Braun

- 10.4 Boston Scientific

- 10.5 ConMed

- 10.6 Cook

- 10.7 Fujifilm

- 10.8 Henke-Sass Wolf

- 10.9 Olympus

- 10.10 PENTAX Medical

- 10.11 Richard Wolf

- 10.12 Scholly Fiberoptic

- 10.13 Smith & Nephew

- 10.14 Storz

- 10.15 Stryker

- 10.16 XION medical