|

시장보고서

상품코드

1801944

바이오메디컬 냉장고 및 냉동고 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Biomedical Refrigerators and Freezers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

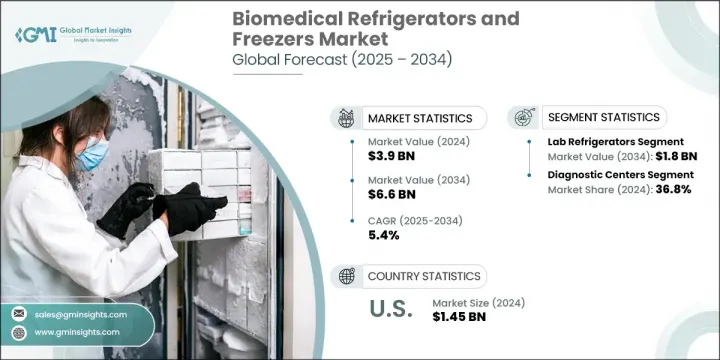

세계 바이오메디컬 냉장고 및 냉동고 시장은 2024년에 39억 달러로 평가되었고, CAGR 5.4%로 성장하여 2034년에는 66억 달러에 이를 것으로 추정됩니다.

시장 개척의 주요 요인은 기술 혁신, 바이오 의약품 개발의 활성화, 장기 이식 증가, 연구 및 임상시험에 대한 정부 자금의 확대 등입니다. 이러한 요인이 함께 선진지역과 개발도상지역 모두에서 왕성한 수요가 창출되고 있습니다. 바이오메디컬 냉장고 및 냉동고는 의료, 제약 및 연구 환경에서 중요한 보관 솔루션입니다. 이 시스템은 의약품, 백신, 생물학적 샘플 및 연구 시약의 무결성과 안정성을 유지하기 위해 정확한 온도 제어를 유지하도록 설계되었습니다.

장기 이식에 대한 세계 수요 증가는 이식 전에 제공된 장기 및 조직을 보존하는 데 도움이 되기 때문에 이러한 시스템의 중요성을 더욱 높일 수 있습니다. 이러한 섬세한 재료의 품질을 보장하는 것은 환자의 결과와 과학 연구의 성공에 직접 영향을 미칩니다. 의료 진보, 특히 생명공학 분야에 대한 관심이 높아짐에 따라, 신뢰할 수 있는 저온 저장 시스템에 대한 필요성이 점점 커지고 있습니다. 바이오 의료용 저온 저장 장치는 실험실, 진단센터, 의료시설에서 규제 준수, 업무 효율성, 제품 안전을 유지하는 데 중요한 역할을 계속하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작금액 | 39억 달러 |

| 예측 금액 | 66억 달러 |

| CAGR | 5.4% |

실험실 냉장고 부문은 2024년에 11억 달러의 매출을 올렸으며, 2034년에는 18억 달러에 이르고, CAGR 5.7%로 성장할 것으로 예측됩니다. 이 부문은 실험실 환경 전체에서 정확한 온도 제어 솔루션에 대한 수요 증가로 이익을 얻고 있습니다. 연구개발의 확대와 의약품 개발 증가는 실험실이 고급 냉동장치를 채택하는 원동력이 되고 있습니다. 일반적으로 2°C와 8°C 사이에서 작동하는 이러한 시스템은 테스트 및 개발 프로세스에 필수적인 시약, 시료, 화학 화합물 등의 온도에 민감한 물질을 안전하게 보관할 수 있는 신뢰할 수 있는 옵션을 제공합니다.

2024년에는 진단센터가 36.8%로 가장 높은 시장 점유율을 차지했습니다. 이러한 시설은 증가하는 진단 검사 및 생물학적 샘플을 처리하기 위해 생물 의학적 저온 보관 장치에 크게 의존합니다. 예방 헬스케어가 주목되고 질병의 조기 발견에 대한 의식이 높아지는 가운데, 신뢰성이 높은 샘플 보관의 필요성이 높아지고 있습니다. 바이오메디컬 냉장 시스템은 검사주기 전반에 걸쳐 시료의 품질을 유지하며 이러한 센터에서 효율성과 진단 정확도를 지원합니다.

미국의 바이오메디컬 냉장고 및 냉동고 시장 규모는 2024년에 14억 5,000만 달러에 달했습니다. 생명 과학 투자 확대, 제약 및 생명 공학 생산 시설 확대, 규제 당국의 품질 관리 요구 사항 엄격화 등 여러 요인이 이러한 성장을 가속화하고 있습니다. 맞춤형 의료, 백신 연구, 유전체학 등의 분야에서의 활동이 활발해지고 있는 것이 최첨단의 연구 기기에 대한 수요를 뒷받침하고 있습니다. 이는 전국의 연구개발기관과 상업건강환경에서 고성능 냉동시스템의 필요성에 크게 기여하고 있습니다.

바이오메디컬 냉장고 및 냉동고 세계 시장을 견인하는 주요 기업은 NuAire, PFC Corporation, BINDER, Aegis Scientific, Eppendorf, Lab Research Products, Thermo Fisher Scientific, Azbil Corporation, Stirling Ultracold, Helmer Scientific, So-Low Environment Systems, Powers Scientific, Migali Scientific 등이 있습니다. 바이오메디컬 냉장고 및 냉동고 시장의 주요 제조업체는 제품 혁신, 세계 전개, 첨단 온도 제어 기술을 선호하고 시장에서의 입지를 강화하고 있습니다. 각 회사는 에너지 효율적이고 환경 친화적이며 원격 모니터링 및 온도 추적을 제공하는 IoT 호환 냉동 장치를 개발하기 위해 연구 개발에 많은 투자를 하고 있습니다. 세계 전개를 강화하기 위해, 주요 기업은 유통망을 확대하고, 의료 제공자나 연구 기관과 전략적 파트너십을 맺고 있습니다. 또한 자동화 및 AI를 활용하여 장비 성능을 향상시키고 다운타임을 최소화하며 규제 준수 요건을 충족하는 기업도 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 조사활동과 임상시험에 대한 정부의 지원 증가

- 바이오메디컬 냉장고 및 냉동고에 있어서의 기술의 진보

- 고령 인구 증가

- 바이오의약품과 장기이식 수요 증가

- 업계의 잠재적 위험 및 과제

- 합리적인 가격으로 재생 기기를 제공하는 현지 기업이 다수 존재

- 냉장고나 냉동고에서 방출되는 하이드로플루오로카본은 환경에 유해한 영향을 미칩니다.

- 바이오메디컬 냉장고 및 냉동고의 고액의 구입 비용, 유지 보수 비용, 에너지 비용

- 시장 기회

- 신흥 시장으로 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술적 진보

- 현재의 기술 동향

- 신흥기술

- 공급망과 유통분석

- 가격 분석, 2024

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추정 및 예측 : 제품별, 2021년-2034년

- 주요 동향

- 플라즈마 냉동고

- 혈액은행 냉장고

- 실험실 냉장고

- 실험실 냉동고

- 초저온 냉동고

- 급속 냉동고

제6장 시장 추정 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 혈액은행

- 약국

- 병원

- 연구실

- 진단센터

- 기타 용도

제7장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제8장 기업 프로파일

- Aegis Scientific

- Azbil Corporation

- B Medical Systems

- BINDER

- Eppendorf

- Follett Products

- Helmer Scientific

- Lab Research Products

- Migali Scientific

- NuAire

- PHC Corporation

- Powers Scientific

- So-Low Environmental Equipment

- Stirling Ultracold

- Thermo Fisher Scientific

The Global Biomedical Refrigerators and Freezers Market was valued at USD 3.9 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 6.6 billion by 2034. Market growth is primarily fueled by technological innovations, rising biopharmaceutical development, increasing organ transplant activity, and expanded government funding for research and clinical trials. These drivers are collectively creating robust demand across both advanced and developing regions. Biomedical refrigerators and freezers are critical storage solutions in healthcare, pharmaceutical, and research environments. These systems are engineered to maintain precise temperature control to preserve the integrity and stability of medications, vaccines, biological samples, and lab reagents.

The rise in global demand for organ transplants further amplifies the importance of these systems, as they help preserve donated organs and tissues prior to transplantation. Ensuring the quality of these sensitive materials directly affects patient outcomes and scientific research success. With more focus on medical advancements, especially in biotechnological sectors, the need for reliable cold storage systems is becoming more pronounced. Biomedical cold storage equipment continues to serve as a vital link in maintaining regulatory compliance, operational efficiency, and product safety in labs, diagnostic centers, and medical facilities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.9 Billion |

| Forecast Value | $6.6 Billion |

| CAGR | 5.4% |

The lab refrigerators segment generated USD 1.1 billion in 2024 and is forecasted to hit USD 1.8 billion by 2034, growing at a CAGR of 5.7%. This segment benefits from the increasing demand for precise temperature-controlled solutions across laboratory environments. Expansion in research activity and increased pharmaceutical product development are driving laboratories to adopt advanced refrigeration units. These systems, which typically operate between 2°C and 8°C, offer a dependable option for safely storing temperature-sensitive materials such as reagents, samples, and chemical compounds critical to testing and development processes.

In 2024 the diagnostic centers held the highest market share at 36.8%. These facilities heavily rely on biomedical cold storage equipment to handle the growing volume of diagnostic tests and biological samples. With preventive healthcare gaining more attention and awareness rising around early disease detection, the need for reliable sample storage has grown. Biomedical refrigeration systems ensure that sample quality is maintained throughout the testing cycle, supporting efficiency and diagnostic accuracy within these centers.

United States Biomedical Refrigerators and Freezers Market generated 1.45 billion in 2024. Several factors are accelerating this growth, including greater investments in life sciences, expansion of pharmaceutical and biotech production facilities, and stricter quality control requirements from regulatory bodies. Increasing activity in areas like personalized medicine, vaccine research, and genomics is fueling the demand for state-of-the-art lab equipment. This is significantly contributing to the need for high-performance refrigeration systems in R&D institutions and commercial healthcare settings across the country.

Key players driving the Global Biomedical Refrigerators and Freezers Market include NuAire, PHC Corporation, BINDER, Aegis Scientific, Eppendorf, Lab Research Products, Thermo Fisher Scientific, Azbil Corporation, Stirling Ultracold, Helmer Scientific, So-Low Environmental Equipment, Follett Products, B Medical Systems, Powers Scientific, and Migali Scientific. Leading manufacturers in the biomedical refrigerators and freezers market are prioritizing product innovation, global expansion, and advanced temperature control technology to strengthen their market positions. Companies are heavily investing in R&D to develop energy-efficient, eco-friendly, and IoT-enabled refrigeration units that provide remote monitoring and temperature tracking. To enhance global footprint, key players are expanding distribution networks and forming strategic partnerships with healthcare providers and research institutions. Some companies are also leveraging automation and AI to improve device performance, minimize downtime, and meet regulatory compliance requirements.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising government support for research activities and clinical trials

- 3.2.1.2 Technological advancements in biomedical refrigerators and freezers

- 3.2.1.3 Increasing geriatric population base

- 3.2.1.4 Increasing demand for biopharmaceuticals and organ transplantation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Presence of large number of local players providing affordable refurbished equipment

- 3.2.2.2 Release of hydrofluorocarbons from refrigerators and freezers have deleterious impact on environment

- 3.2.2.3 High purchase costs, maintenance costs and energy costs of biomedical refrigerators and freezers

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain and distribution analysis

- 3.7 Pricing analysis, 2024

- 3.8 Future market trends

- 3.9 Gap analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Plasma freezers

- 5.3 Blood bank refrigerators

- 5.4 Lab refrigerators

- 5.5 Lab freezers

- 5.6 Ultra-low temperature freezers

- 5.7 Shock freezers

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Blood banks

- 6.3 Pharmacies

- 6.4 Hospitals

- 6.5 Research labs

- 6.6 Diagnostic centers

- 6.7 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Aegis Scientific

- 8.2 Azbil Corporation

- 8.3 B Medical Systems

- 8.4 BINDER

- 8.5 Eppendorf

- 8.6 Follett Products

- 8.7 Helmer Scientific

- 8.8 Lab Research Products

- 8.9 Migali Scientific

- 8.10 NuAire

- 8.11 PHC Corporation

- 8.12 Powers Scientific

- 8.13 So-Low Environmental Equipment

- 8.14 Stirling Ultracold

- 8.15 Thermo Fisher Scientific