|

시장보고서

상품코드

1801948

지하 고압 케이블 시장 기회와 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Underground High Voltage Cable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

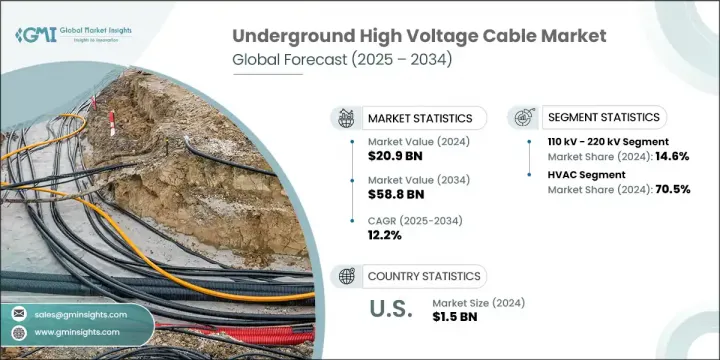

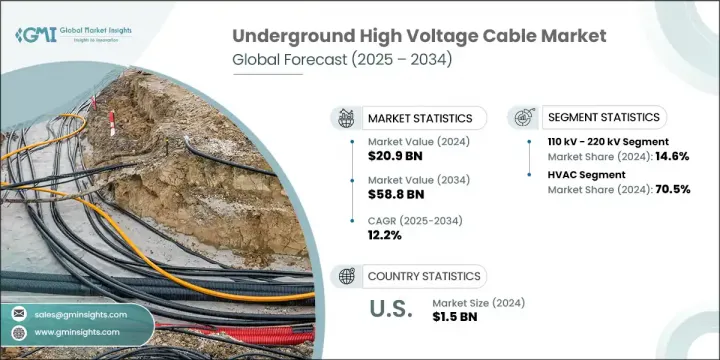

지하 고압 케이블 세계 시장 규모는 2024년에 209억 달러로 평가되었고, CAGR 12.2%로 성장하여 2034년에는 588억 달러에 이를 것으로 추정됩니다.

이러한 강력한 성장은 전 세계 도시화의 가속화에 따른 것으로, 특히 선진국과 빠르게 발전하고 있는 지역에서는 안정적인 송전에 대한 수요가 증가하고 있습니다. 도시 밀도가 높아짐에 따라 공간 효율이 높고 시각적 영향이 적은 지하 케이블 시스템이 선호되고 있습니다. 미관과 안전성이 중시되는 대도시권에서는 전력회사가 가공 송전선을 없애고 지중 송전선을 채택하는 사례가 늘고 있습니다.

이러한 시스템은 신뢰성이 높고, 기상 이변 시 사고 및 정전 위험이 현저히 낮습니다. 정부와 유틸리티 회사들은 스마트시티 개발 계획에 지하 배선을 포함시켜 장기적인 매력도를 더욱 높이고 있습니다. 산불, 허리케인 등 기후 관련 재해가 증가함에 따라 업계는 지하 고압 케이블을 전력망 복원력의 핵심으로 보고 있습니다. 그리드 현대화를 위한 규제 프레임워크와 정부 주도의 인센티브도 일부 지역에서 시장 모멘텀을 강화하는 데 매우 중요한 역할을 하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 209억 달러 |

| 예측 금액 | 588억 달러 |

| CAGR | 12.2% |

110kV-220kV 지하 케이블 부문은 2024년 14.6%의 점유율을 차지할 것으로 예상되며, 2034년까지 연평균 25%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 이 전압 범위는 송전 및 대용량 배전 네트워크에 폭넓게 적용할 수 있어 선호되고 있습니다. 특히 대규모 재생에너지 프로젝트를 송전망에 통합할 때 변전소 간 연결 및 중거리 송전에 필수적인 역할을 합니다. 유틸리티 제공업체는 지역 배전 수요에 효율적으로 대응하기 위해 이 케이블에 대한 의존도를 높이고 있습니다.

고압 교류(HVAC) 케이블 부문은 2024년 70.5%의 최대 점유율을 차지할 것으로 예상되며, 2034년까지 21%의 연평균 복합 성장률(CAGR)을 보일 것으로 전망됩니다. HVAC 시스템은 현재 인프라와의 호환성이 용이하기 때문에 도시 지역 및 중거리 송전에서 지하 케이블 부설의 유력한 선택이 되고 있습니다. 절연 기술과 컴팩트한 케이블 설계의 발전으로 HVAC의 설치 효율이 더욱 향상되어 밀집되고 복잡한 환경에 이상적입니다. 복잡한 컨버터 스테이션이 필요하지 않고 기존 자산과 원활하게 통합할 수 있어 송전망 현대화 프로젝트에 적합한 솔루션입니다.

미국 지하 고압 케이블 시장은 50.2%의 점유율을 차지하며 2024년 15억 달러 규모 시장을 형성할 것으로 예측됩니다. 미국에서는 전력망 강화 노력, 에너지 전환 정책, 기후 변화와 관련된 재난 발생 빈도 증가 등이 성장의 원동력이 되고 있습니다. 유틸리티는 특히 재해가 잦은 도시 지역에서 인프라의 복원력과 지속적인 전력 공급을 보장하기 위해 지하 케이블 배선에 투자하고 있습니다. 특히, 국가 인프라 구상을 통한 개발 프로그램과 자금 지원은 이러한 개발을 가속화하고 있습니다. 또한, 데이터센터, 전기자동차 네트워크, 재생에너지 등의 분야에서 급속히 증가하는 수요는 지하 고압 솔루션의 추가 개발을 촉진하고 있습니다.

세계 주요 기업으로는 Sumitomo Electric Industries Ltd., Nexans, ZTT, TF Kable, Riyadh Cable, NKT A/S, Brugg Kabel AG, Jeddah Cables, Ducab, Prysmian Group, KEI Industries Limited, alfanar Group, ILJIN ELECTRIC, Hellenic Cable Limited, Universal Cable Limited, Taihan Cable & Solution Co. Prysmian Group,KEI Industries Limited,alfanar Group,ILJIN ELECTRIC,Hellenic Cables,Universal Cable Limited,Taihan Cable &Solution Co.L.L.C., Tratos,LS Cable &Solution Co. Tratos,LS Cable &System Ltd.,FURUKAWA ELECTRIC CO., LTD. 등이 있습니다. 지하 고압 케이블 분야의 주요 기업들은 제품 혁신에 적극적으로 투자하고 있으며, 차세대 송전 요구 사항을 충족시키기 위해 케이블의 효율성, 소형화, 열 성능 향상에 주력하고 있습니다. 많은 기업들이 대규모 송전 프로젝트의 장기 계약을 확보하기 위해 전력회사 및 인프라 개발업체와 전략적 제휴 및 합작투자를 체결하고 있습니다. 제조업체는 또한 리드 타임을 단축하고 각 지역 수요 급증에 효과적으로 대응하기 위해 전 세계 생산 기지를 확장하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 규제 상황

- 업계에 대한 영향요인

- 가격 동향 분석(USD/km)

- 전압별

- 지역별

- 성장 가능성 분석

- Porter의 Five Forces 분석

- 공급 기업의 교섭력

- 바이어의 교섭력

- 신규 진출업체의 위협

- 대체품의 위협

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석 : 지역별

- 북미

- 유럽

- 아시아태평양

- 세계 기타 지역

- 전략적 이니셔티브

- 경쟁 벤치마킹

- 전략적 대시보드

- 혁신과 기술 상황

제5장 시장 규모와 예측 : 전압별, 2021년-2034년

- 주요 동향

- 110kV 미만

- 110kV-220kV

- 220kV 이상

제6장 시장 규모와 예측 : 전류별, 2021년-2034년

- 주요 동향

- HVAC

- HVDC

제7장 시장 규모와 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 아시아태평양

- 중국

- 인도

- 태국

- 인도네시아

- 세계 기타 지역

제8장 기업 개요

- alfanar Group

- Brugg Kabel AG

- Ducab

- FURUKAWA ELECTRIC CO., LTD.

- Hellenic Cables

- ILJIN ELECTRIC

- Jeddah Cables

- KEI Industries Limited

- LS Cable &System Ltd.

- Nexans

- NKT A/S

- Prysmian Group

- Power Plus Cables Co. L.L.C.

- Riyadh Cable

- Southwire Company, LLC

- Sumitomo Electric Industries Ltd.

- Taihan Cable &Solution Co., Ltd.

- TF Kable

- Tratos

- Universal Cable Limited

- ZTT

The Global Underground High Voltage Cable Market was valued at USD 20.9 billion in 2024 and is estimated to grow at a CAGR of 12.2% to reach USD 58.8 billion by 2034. This robust growth is largely attributed to the accelerating rate of urbanization worldwide, which is intensifying the demand for dependable electricity transmission, especially in industrialized and fast-developing regions. As urban density increases, the preference is shifting toward underground cable systems due to their space efficiency and reduced visual impact. In metropolitan areas where aesthetics and safety are vital, utilities are increasingly abandoning overhead lines in favor of underground solutions.

These systems offer greater reliability and significantly lower risks of accidents or outages during extreme weather conditions. Governments and utility companies are incorporating underground cabling into smart city development plans, further enhancing its long-term appeal. With the rise in climate-related disruptions, such as wildfires and hurricanes, the industry is seeing underground high voltage cables as a cornerstone of grid resiliency. Regulatory frameworks and government-led incentives for grid modernization are also playing a pivotal role in strengthening market momentum across several regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $20.9 Billion |

| Forecast Value | $58.8 Billion |

| CAGR | 12.2% |

The 110 kV to 220 kV underground cable segment accounted for a 14.6% share in 2024 and is expected to register a CAGR of 25% through 2034. This voltage range is favored due to its broad applicability in transmission and high-capacity distribution networks. It serves essential roles in linking substations and routing power over moderate distances, especially when integrating large-scale renewable energy projects into the grid. Utility providers increasingly rely on these cables to meet regional power distribution demands efficiently.

The high voltage alternating current (HVAC) cables segment held the largest share of 70.5% in 2024 and is forecasted to grow at a CAGR of 21% through 2034. HVAC systems remain the dominant choice for underground cable installations in urban and mid-range transmission due to their easy compatibility with current infrastructure. Advances in insulation technologies and compact cable design have further improved HVAC installation efficiency, making them ideal for dense, complex environments. Their seamless integration with conventional assets-without requiring complex converter stations-makes them a go-to solution for grid modernization projects.

U.S. Underground High Voltage Cable Market held 50.2% share, generating USD 1.5 billion in 2024. Growth in the U.S. is strongly driven by grid reinforcement initiatives, energy transition policies, and the increasing frequency of climate-related disruptions. Utilities are investing in underground cabling to ensure infrastructure resilience and a continuous power supply, particularly in disaster-prone and urban areas. Government programs and funding support, especially from national infrastructure initiatives, are accelerating these developments. In addition, rapid demand growth from sectors like data centers, electric vehicle networks, and renewable energy is encouraging further deployment of underground high voltage solutions.

Prominent players shaping the Global Underground High Voltage Cable Market include Sumitomo Electric Industries Ltd., Nexans, ZTT, TF Kable, Riyadh Cable, NKT A/S, Brugg Kabel AG, Jeddah Cables, Ducab, Prysmian Group, KEI Industries Limited, alfanar Group, ILJIN ELECTRIC, Hellenic Cables, Universal Cable Limited, Taihan Cable & Solution Co., Ltd., Southwire Company, LLC, Power Plus Cables Co. L.L.C., Tratos, LS Cable & System Ltd., and FURUKAWA ELECTRIC CO., LTD. Leading companies in the underground high voltage cable sector are actively investing in product innovation, focusing on improving cable efficiency, compactness, and thermal performance to meet next-generation transmission requirements. Many firms are forming strategic alliances and joint ventures with utility providers and infrastructure developers to secure long-term contracts for large-scale transmission projects. Manufacturers are also scaling up their global production footprints to reduce lead times and respond more effectively to regional demand surges.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.1.1 Business trends

- 2.1.2 Voltage trends

- 2.1.3 Current trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.4 Price trend analysis (USD/km)

- 3.4.1 By voltage

- 3.4.2 By region

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Environmental factors

- 3.7.6 Legal factors

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Rest of World

- 4.3 Strategic initiative

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Voltage, 2021 - 2034 (USD Million, km)

- 5.1 Key trends

- 5.2 < 110 kV

- 5.3 110 kV - 220 kV

- 5.4 > 220 kV

Chapter 6 Market Size and Forecast, By Current, 2021 - 2034 (USD Million, km)

- 6.1 Key trends

- 6.2 HVAC

- 6.3 HVDC

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, km)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Thailand

- 7.4.4 Indonesia

- 7.5 Rest of World

Chapter 8 Company Profiles

- 8.1 alfanar Group

- 8.2 Brugg Kabel AG

- 8.3 Ducab

- 8.4 FURUKAWA ELECTRIC CO., LTD.

- 8.5 Hellenic Cables

- 8.6 ILJIN ELECTRIC

- 8.7 Jeddah Cables

- 8.8 KEI Industries Limited

- 8.9 LS Cable & System Ltd.

- 8.10 Nexans

- 8.11 NKT A/S

- 8.12 Prysmian Group

- 8.13 Power Plus Cables Co. L.L.C.

- 8.14 Riyadh Cable

- 8.15 Southwire Company, LLC

- 8.16 Sumitomo Electric Industries Ltd.

- 8.17 Taihan Cable & Solution Co., Ltd.

- 8.18 TF Kable

- 8.19 Tratos

- 8.20 Universal Cable Limited

- 8.21 ZTT