|

시장보고서

상품코드

1801953

주택용 태양광발전 인버터 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Residential Solar PV Inverter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

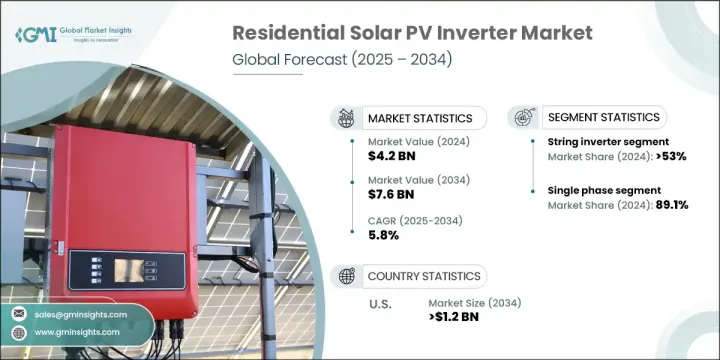

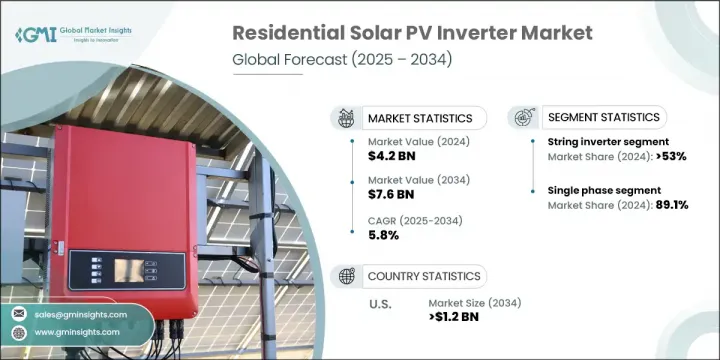

세계의 주택용 태양광발전 인버터 시장 규모는 2024년에 42억 달러에 달했고, CAGR 5.8%를 나타내 2034년에는 76억 달러에 이를 것으로 예측됩니다.

태양에너지 도입의 꾸준한 증가는 보조금, 리베이트, 세제 우대 조치에 의한 재정 지원의 가용성 증가와 함께 패널 및 관련 기술의 가격 하락에 의해 뒷받침되고 있습니다. 기존의 송전망과 관련된 광열비의 상승은 주택 소유자가 대체 에너지를 모색하는 동기부여가 되어 태양광발전 시스템이나 PV 인버터와 같은 지원 제품 수요를 밀어 올리고 있습니다.

이 인버터는 태양전지판의 직류 전류를 주거용 전력망에서 사용되는 교류 전류로 변환하는 데 중요한 역할을 하는 동시에 필수적인 안전 및 모니터링 기능을 갖추고 있습니다. 보다 깨끗한 에너지를 촉진하는 규제 프레임워크과 장기적인 절약을 소개하는 계몽 캠페인이 주택에의 설치를 더욱 뒷받침하고 있습니다. 지속가능성과 에너지의 자립을 목표로 하는 가정의 에너지 수요의 증대에 대응하기 위해, 업계의 리더들은 최첨단의 인버터 기술을 채용하게 되어 왔습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 42억 달러 |

| 예측 금액 | 76억 달러 |

| CAGR | 5.8% |

마이크로 인버터 부문은 패널 레벨 최적화에 의해 부분적인 그늘 설치에서도 성능이 향상되기 때문에 2034년까지의 CAGR은 6%를 나타낼 전망입니다. 설치의 간소화, 저전압 설계, 확장 가능한 아키텍처로 마이크로 인버터는 중소규모 주택에 이상적이며 시장 보급을 촉진합니다.

단상 인버터는 2024년에 89.1%의 점유율을 획득했으며 2034년까지 연평균 복합 성장률(CAGR) 5.6%를 나타낼 것으로 예측됩니다. 이 장치는 컴팩트한 설계, 설치 용이성, 평균 주택 전력 수요에 대한 적합성으로 널리 지원됩니다. 에너지 저장 시스템 및 지능형 에너지 플랫폼과의 통합은 또한 광열비 절감과 이산화탄소 배출량 최소화를 목표로 하는 가정으로부터의 관심 증가를 지원합니다. 솔라 + 축전 솔루션이 보급됨에 따라 최신 스마트 홈 내에서 원활하게 작동하는 단상 인버터에 대한 수요가 계속 증가하고 있습니다.

미국의 주택용 태양광발전 인버터 시장은 2024년에 99.3%의 점유율을 차지했으며, 2034년에는 12억 달러에 이를 것으로 예측됩니다. 이 나라의 강력한 기세는 신재생에너지 의무화, 세제우대조치, 넷미터링 프로그램, 전력회사 수준의 리베이트 제공 등의 유리한 정책에 의해 초래되고 있습니다. 이러한 조치는 대규모 주거용 태양광발전 시스템의 설치를 지원합니다. 선진적인 제품 개발에 투자하고 있는 주요 시장 개척 기업의 존재는 신재생에너지로 전환하고 있는 미국 가정의 장기 성장을 더욱 뒷받침하고 있습니다.

주택용 태양광발전 인버터 시장에서 사업을 전개하고 있는 유력 기업은 Sungrow, Solar Edge Technologies, Inc., Siemens, Schneider Electric, Panasonic Corporation, INVERGY, Huawei Technologies Co., Ltd., Hitachi Hi-Rel Power Electronics Private Limited, GoodWeGol Electric, Frontius International GmbH, Fimer Group, Eaton, Enphase Energy, Delta Electronics, Inc., Darfon Electronics Corp., Canadian Solar, Servotech Power Systems 등이 있습니다. 대기업은 스토리지 및 IoT 용도과 호환되는 소형, 고효율, 스마트 인버터에 초점을 맞추고 제품 혁신을 추진함으로써 시장 발판을 굳히고 있습니다. 각 회사는 안전 기능을 강화하고 AI 기반 모니터링을 통합하고 패널 당 에너지 수율을 증가시키기 위해 연구 개발에 적극적으로 투자하고 있습니다. 배터리 제조업체나 스마트 홈 플랫폼과의 협업에 의해 진화하는 주택 에너지 요구에 합치한 부가가치가 높은 제품이 만들어지고 있습니다. 기업은 또한 지역 제조 단위, 유통 파트너십, 디지털 판매 네트워크를 통해 지역 실적을 확대하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 업계 인사이트

- 업계 요약(2021-2034년)

- 비즈니스 동향

- 제품 동향

- 위상 동향

- 지역 동향

제3장 업계 인사이트

- 생태계 분석

- 원자재 및 부품 공급업체

- 인버터 제조업체

- EPC 및 시스템 통합자

- 프로젝트 개발자 및 IPP

- 가격 동향 분석(2021-2034년)

- 제품별

- 지역별

- 비용 구조 분석

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석 : 지역별

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 전략적 대시보드

- 전략적 노력

- 기업 벤치마킹

- 혁신과 기술의 상황

제5장 시장 규모와 예측 : 제품별(2021-2034년)

- 주요 동향

- 문자열

- 마이크로

제6장 시장 규모와 예측 : 위상별(2021-2034년)

- 주요 동향

- 단상

- 삼상

제7장 시장 규모와 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 이탈리아

- 폴란드

- 네덜란드

- 오스트리아

- 영국

- 프랑스

- 아시아태평양

- 중국

- 호주

- 인도

- 일본

- 한국

- 중동 및 아프리카

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 이집트

- 나이지리아

- 라틴아메리카

- 브라질

- 멕시코

- 칠레

제8장 기업 프로파일

- Canadian Solar

- Darfon Electronics Corp.

- Delta Electronics, Inc.

- Enphase Energy

- Eaton

- Fimer Group

- Fronius International GmbH

- General Electric

- Ginlong Technologies

- Goldi Solar

- GoodWe

- Hitachi Hi-Rel Power Electronics Private Limited

- Huawei Technologies Co., Ltd.

- INVERGY

- Panasonic Corporation

- Schneider Electric

- Siemens

- SMA Solar Technology AG

- Servotech Power Systems

- Solar Edge Technologies, Inc.

- Sungrow

The Global Residential Solar PV Inverter Market was valued at USD 4.2 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 7.6 billion by 2034. A steady rise in solar energy adoption is being fueled by declining prices of panels and associated technologies, along with increasing availability of financial support through grants, rebates, and tax incentives. Escalating utility costs tied to conventional power grids are motivating homeowners to explore energy alternatives, pushing up demand for solar-powered systems and supporting products like PV inverters.

These inverters play a critical role in converting direct current from solar panels into alternating current used by residential electrical grids, while also providing essential safety and monitoring features. Regulatory frameworks promoting cleaner energy and awareness campaigns that showcase long-term savings are further encouraging residential installations. Industry leaders are increasingly adopting cutting-edge inverter technologies to meet the growing energy demands of households aiming for sustainability and energy independence.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.2 Billion |

| Forecast Value | $7.6 Billion |

| CAGR | 5.8% |

The micro inverter segment is poised for a CAGR of 6% through 2034, driven by its panel-level optimization, which ensures enhanced performance even in partially shaded installations. The simplified installation, low-voltage design, and scalable architecture make micro inverters ideal for small and mid-size homes, promoting wider market adoption.

The single-phase inverters captured 89.1% share in 2024 and is projected to grow at a CAGR of 5.6% through 2034. These units are widely favored due to their compact design, ease of installation, and compatibility with average residential power demands. Their integration with energy storage systems and intelligent energy platforms also supports growing interest from households looking to reduce utility bills and minimize their carbon footprint. As solar-plus-storage solutions gain traction, the demand for single-phase inverters that seamlessly operate within modern smart homes continues to rise.

United States Residential Solar PV Inverter Market held a 99.3% share in 2024 and is anticipated to reach USD 1.2 billion by 2034. The country's strong momentum is driven by favorable policies such as renewable energy mandates, tax incentives, net metering programs, and utility-level rebate offerings. These measures are encouraging the installation of residential solar systems at scale. The presence of major market players investing in advanced product development further supports long-term growth across US households transitioning toward renewable power solutions.

Prominent companies operating in the Residential Solar PV Inverter Market include Sungrow, Solar Edge Technologies, Inc., Siemens, Schneider Electric, Panasonic Corporation, INVERGY, Huawei Technologies Co., Ltd., Hitachi Hi-Rel Power Electronics Private Limited, GoodWe, Goldi Solar, Ginlong Technologies, General Electric, Fronius International GmbH, Fimer Group, Eaton, Enphase Energy, Delta Electronics, Inc., Darfon Electronics Corp., Canadian Solar, and Servotech Power Systems. Leading players are strengthening their market foothold by advancing product innovation, focusing on compact, high-efficiency, and smart inverters compatible with storage and IoT applications. Firms are actively investing in R&D to enhance safety features, integrate AI-based monitoring, and increase energy yield per panel. Collaborations with battery manufacturers and smart home platforms are creating value-added offerings that align with evolving residential energy needs. Companies are also expanding their geographic footprint through regional manufacturing units, distribution partnerships, and digital sales networks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market Definitions

Chapter 2 Industry Insights

- 2.1 Industry synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Product trends

- 2.4 Phase trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw materials & component suppliers

- 3.1.2 Inverter manufacturers

- 3.1.3 EPC & system integrators

- 3.1.4 Project developers & IPPs

- 3.2 Price trend analysis, 2021-2034

- 3.2.1 By product

- 3.2.2 By region

- 3.3 Cost structure analysis

- 3.4 Regulatory landscape

- 3.5 Industry impact forces

- 3.5.1 Growth drivers

- 3.5.2 Industry pitfalls & challenges

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitutes

- 3.8 PESTEL analysis

- 3.8.1 Political factors

- 3.8.2 Economic factors

- 3.8.3 Social factors

- 3.8.4 Technological factors

- 3.8.5 Legal factors

- 3.8.6 Environmental factors

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Product, 2021 - 2034 (USD Billion & MW)

- 5.1 Key trends

- 5.2 String

- 5.3 Micro

Chapter 6 Market Size and Forecast, By Phase, 2021 - 2034 (USD Billion & MW)

- 6.1 Key trends

- 6.2 Single phase

- 6.3 Three phase

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion & MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Italy

- 7.3.3 Poland

- 7.3.4 Netherlands

- 7.3.5 Austria

- 7.3.6 UK

- 7.3.7 France

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Israel

- 7.5.2 Saudi Arabia

- 7.5.3 UAE

- 7.5.4 South Africa

- 7.5.5 Egypt

- 7.5.6 Nigeria

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Mexico

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 Canadian Solar

- 8.2 Darfon Electronics Corp.

- 8.3 Delta Electronics, Inc.

- 8.4 Enphase Energy

- 8.5 Eaton

- 8.6 Fimer Group

- 8.7 Fronius International GmbH

- 8.8 General Electric

- 8.9 Ginlong Technologies

- 8.10 Goldi Solar

- 8.11 GoodWe

- 8.12 Hitachi Hi-Rel Power Electronics Private Limited

- 8.13 Huawei Technologies Co., Ltd.

- 8.14 INVERGY

- 8.15 Panasonic Corporation

- 8.16 Schneider Electric

- 8.17 Siemens

- 8.18 SMA Solar Technology AG

- 8.19 Servotech Power Systems

- 8.20 Solar Edge Technologies, Inc.

- 8.21 Sungrow