|

시장보고서

상품코드

1822548

양조 및 증류 장비 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Brewing and Distillery Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

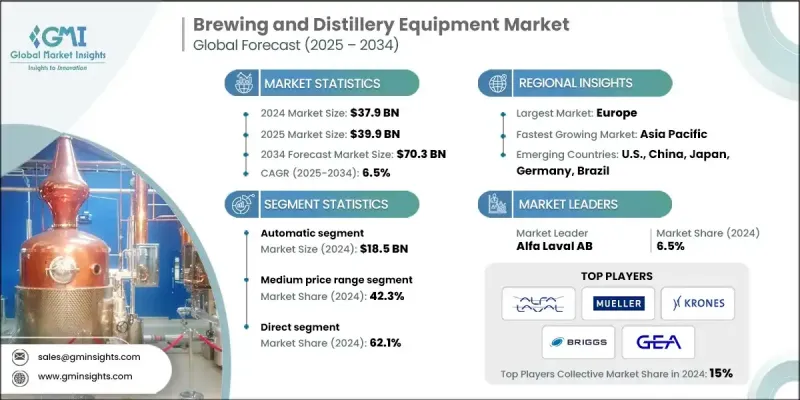

양조 및 증류 장비 세계 시장 규모는 2024년에 379억 달러로 평가되었고, CAGR 6.5%로 성장하여 2034년에는 703억 달러에 이를 것으로 예측되고 있습니다.

크래프트 맥주 양조장의 급성장과 장인 기술이 빛나는 고급 증류주에 대한 세계적인 수요 증가가 양조 및 증류 장비 시장을 견인하는 주된 요인이 되고 있습니다. 소비자가 독특한 맛과 소량 생산 제품을 지속적으로 찾고있는 동안 양조장과 증류소는이 급성장 분야의 요구를 충족시키기 위해 특수 장비에 투자를 추진하고 있습니다.

| 시장 규모 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 379억 달러 |

| 예측 금액 | 703억 달러 |

| CAGR | 6.5% |

자동 장치에 대한 수요 증가

제조업체와 생산자가 효율성, 일관성 및 확장성을 선호하기 위해 자동화 부서는 2024년에 큰 점유율을 차지했습니다. 고급 양조 제어 시스템 및 자동 발효 모니터링과 같은 자동화 기술을 통해 양조장과 증류소는 생산 공정을 크게 향상시킬 수 있습니다. 이러한 자동화로의 전환은 인건비 절감, 생산 능력 향상, 제품 품질 유지 등의 소망에 의해 추진되고 있습니다.

중가격대의 보급 확대

중간 가격대 부문은 2024년에 큰 수익을 올렸습니다. 이 부문은 프리미엄 모델과 같은 높은 가격대가 아니라 신뢰할 수 있고 내구성있는 양조 및 증류 장비를 찾는 기업을 지원합니다. 성장하는 양조장과 증류소에 확장성과 유연성을 갖춘 장비를 제공함으로써 시장 성장이 촉진됩니다.

직접 판매로 견인력 확보

제조업체가 소비자에게 직접 장비를 판매하는 직접 판매 부문은 2024년에 상당한 성장을 이루었습니다. 개인화된 맞춤형 솔루션에 대한 추세가 점점 퍼지고 있습니다. 양조장과 증류소는 자체 생산 공정에 맞는 맞춤형 장비를 선택하여 통합 지원 서비스 및 유지 보수 계획을 제공합니다. 직접 판매를 통해 기업은 최종 사용자와 보다 긴밀한 관계를 구축할 수 있어 고객의 요구 사항을 이해하고 교육 및 지속적인 기술 지원과 같은 구매 후 서비스를 제공할 수 있는 기회를 얻을 수 있습니다.

지역별 인사이트

유리한 지역으로 상승하는 유럽

유럽 양조 및 증류 장비 시장은 2024년도 지속적인 점유율을 유지. 대규모 맥주 제조업체와 공예 맥주 제조업체는 효율성, 지속가능성 및 혁신성에 대한 엄격한 유럽 표준을 충족하는 최첨단 장비를 찾고 있습니다. 또한 유럽에서는 환경 친화적인 생산 공정에 대한 동향이 증가하고 있으며, 많은 기업들이 물 사용량을 줄이고 폐기물을 최소화하는 에너지 효율적인 장비에 주목하고 있습니다.

양조 및 증류 장비 시장의 주요 기업은 Criveller Group, Ziemann Holvrieka, Paul Mueller, Portland Kettle Works, Briggs of Burton, Alfa Laval, Specific Mechanical Systems, JVNW, Krones, Kaspar Schulz, GEA Group, ABE Equipment, Lehui International, Ss Brewtech, and Della Toffola 등이 있습니다.

양조 및 증류 장비 시장의 각 사는 존재감을 높이기 위해 혁신, 전략적 파트너십, 고객 중심 솔루션의 조합에 주력하고 있습니다. 최첨단 자동화 기술에 투자함으로써 기업은 고객의 운영을 간소화하고 생산 효율성을 높입니다. 게다가 많은 기업들은 양조와 증류에 있어 환경 친화적인 관행에 대한 수요 증가에 대응하고 에너지 효율적인 지속 가능한 장비 옵션을 포함한 제품 포트폴리오를 확대하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 알코올 음료 산업의 확대

- 크래프트 맥주와 스피릿 수요 증가

- 기술적 진보

- 업계의 잠재적 위험 및 과제

- 높은 초기 자본 투자액

- 엄격한 규제 및 라이선싱 요건

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신규 기술

- 가격 동향

- 지역별

- 기기별

- 규제 상황

- 표준 및 컴플라이언스 요건

- 지역 규제 틀

- 인증기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추정 및 예측 : 기기종별, 2021-2034

- 주요 동향

- 양조 설비

- 양조장 시스템

- Mash tuns

- Lauter tuns

- Brew kettles

- Whirlpool systems

- 발효 장치

- 발효 탱크

- Bright beer tanks

- 온도 제어 시스템

- 여과 및 정화 시스템

- 포장 장비

- Bottling lines

- 통조림 시스템

- Kegging equipment

- 품질관리 및 시험장치

- 양조장 시스템

- 증류장치

- Pot stills

- Column stills

- 하이브리드 스틸

- 응축기와 열교환기

- 노화 및 성숙 장비

- Blending and proofing systems

- 서포트 기기

- 세정 및 소독 시스템(CIP/SIP)

- 증기발생장치

- 냉각 시스템

- 펌프와 밸브

- 저장 탱크와 용기

제6장 시장 추정 및 예측 : 동작 모드별, 2021-2034

- 주요 동향

- 자동

- 반자동

- 매뉴얼

제7장 시장 추정 및 예측 : 가격별, 2021-2034

- 주요 동향

- 저

- 중

- 고

제8장 시장 추정 및 예측 : 재료별, 2021-2034

- 주요 동향

- 스테인레스 스틸

- 구리

- 기타(알루미늄, 탄소강)

제9장 시장 추정 및 예측 : 최종 용도별, 2021-2034

- 주요 동향

- 크래프트 맥주 양조장

- 상업 양조장

- 크래프트 증류소

- 상업 증류소

- 교육연구기관

- 자가 양조와 증류 애호가

제10장 시장 추정 및 예측 : 유통채널별, 2021-2034

- 주요 동향

- 직접

- 간접적

제11장 시장 추정 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 인도네시아

- 말레이시아

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

제12장 기업 프로파일

- ABE Equipment

- Alfa Laval

- Briggs of Burton

- Criveller Group

- Della Toffola

- GEA Group

- JVNW

- Kaspar Schulz

- Krones

- Lehui International

- Paul Mueller

- Portland Kettle Works

- Specific Mechanical Systems

- Ss Brewtech

- Ziemann Holvrieka

The Global Brewing and Distillery Equipment Market was valued at USD 37.9 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 70.3 billion by 2034.

The rapid growth of craft breweries and the rising global demand for artisanal and premium spirits are major factors driving the brewing and distillery equipment market. As consumers continue to seek unique flavors and small-batch products, breweries and distilleries are investing in specialized equipment to meet the needs of this burgeoning sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $37.9 Billion |

| Forecast Value | $70.3 Billion |

| CAGR | 6.5% |

Rising demand for Automatic Equipment

The automatic segment held a significant share in 2024, as manufacturers and producers prioritize efficiency, consistency, and scalability. With automation technologies, such as advanced brewing control systems and automated fermentation monitoring, breweries and distilleries can significantly enhance production processes. This shift to automation is driven by the desire to reduce labor costs, increase production capacity, and maintain product quality.

Growing Prevalence of Medium Price Range

The medium price range segment generated significant revenue in 2024. This segment caters to businesses that are looking for reliable and durable brewing and distilling equipment without the steep price tag of premium models. Offering equipment that provides scalability and flexibility for growing breweries and distilleries proliferate market growth.

Direct Sales to Gain Traction

The direct segment held sizeable growth in 2024, where manufacturers sell their equipment directly to consumers. The trend towards personalized and tailored solutions is becoming increasingly prevalent. Breweries and distilleries are opting for bespoke equipment that matches their unique production processes and offer integrated support services and maintenance plans. Direct sales allow companies to form closer relationships with end use, providing them with the opportunity to understand customer requirements and offer post-purchase services such as training and ongoing technical support.

Regional Insights

Europe to Emerge as a Lucrative Region

Europe brewing and distillery equipment market held a sustainable share in 2024. Large-scale and craft brewers seek state-of-the-art equipment that meets rigorous European standards for efficiency, sustainability, and innovation. Europe is also witnessing a growing trend towards eco-friendly production processes, with many companies focusing on energy-efficient equipment that reduces water usage and minimizes waste.

Major players in the brewing and distillery equipment market are Criveller Group, Ziemann Holvrieka, Paul Mueller, Portland Kettle Works, Briggs of Burton, Alfa Laval, Specific Mechanical Systems, JVNW, Krones, Kaspar Schulz, GEA Group, ABE Equipment, Lehui International, Ss Brewtech, and Della Toffola.

To strengthen their presence, companies in the brewing and distillery equipment market are focusing on a combination of innovation, strategic partnerships, and customer-centric solutions. By investing in cutting-edge automation technologies, firms are enabling their customers to streamline operations and boost production efficiency. Additionally, many companies are expanding their product portfolios to include energy-efficient and sustainable equipment options, responding to the growing demand for eco-friendly practices in brewing and distillation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Mode of operation

- 2.2.4 Price

- 2.2.5 Material

- 2.2.6 End Use

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of alcoholic beverage industry

- 3.2.1.2 Rising demand for craft beer and spirits

- 3.2.1.3 Technological advancements

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital investment

- 3.2.2.2 Stringent regulatory and licensing requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2021 - 2034, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Brewing equipment

- 5.2.1 Brewhouse systems

- 5.2.1.1 Mash tuns

- 5.2.1.2 Lauter tuns

- 5.2.1.3 Brew kettles

- 5.2.1.4 Whirlpool systems

- 5.2.2 Fermentation equipment

- 5.2.2.1 Fermentation tanks

- 5.2.2.2 Bright beer tanks

- 5.2.2.3 Temperature control systems

- 5.2.3 Filtration and clarification systems

- 5.2.4 Packaging equipment

- 5.2.4.1 Bottling lines

- 5.2.4.2 Canning systems

- 5.2.4.3 Kegging equipment

- 5.2.5 Quality control and testing equipment

- 5.2.1 Brewhouse systems

- 5.3 Distillation equipment

- 5.3.1 Pot stills

- 5.3.2 Column stills

- 5.3.3 Hybrid stills

- 5.3.4 Condensers and heat exchangers

- 5.3.5 Aging and maturation equipment

- 5.3.6 Blending and proofing systems

- 5.4 Supporting equipment

- 5.4.1 Cleaning and sanitization systems (CIP/SIP)

- 5.4.2 Steam generation equipment

- 5.4.3 Cooling systems

- 5.4.4 Pumps and valves

- 5.4.5 Storage tanks and vessels

Chapter 6 Market Estimates & Forecast, By Mode of Operation, 2021 - 2034, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Automatic

- 6.3 Semi-automatic

- 6.4 Manual

Chapter 7 Market Estimates & Forecast, By Price, 2021 - 2034, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By Material, 2021 - 2034, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Stainless steel

- 8.3 Copper

- 8.4 Others (aluminum, carbon steel)

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Craft breweries

- 9.3 Commercial breweries

- 9.4 Craft distilleries

- 9.5 Commercial distilleries

- 9.6 Educational and research institutions

- 9.7 Home brewing and distilling enthusiasts

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Indonesia

- 11.4.7 Malaysia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 ABE Equipment

- 12.2 Alfa Laval

- 12.3 Briggs of Burton

- 12.4 Criveller Group

- 12.5 Della Toffola

- 12.6 GEA Group

- 12.7 JVNW

- 12.8 Kaspar Schulz

- 12.9 Krones

- 12.10 Lehui International

- 12.11 Paul Mueller

- 12.12 Portland Kettle Works

- 12.13 Specific Mechanical Systems

- 12.14 Ss Brewtech

- 12.15 Ziemann Holvrieka

(주말 및 공휴일 제외)