|

시장보고서

상품코드

1822554

군용 보호 안경 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Military Protective Eyewear Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

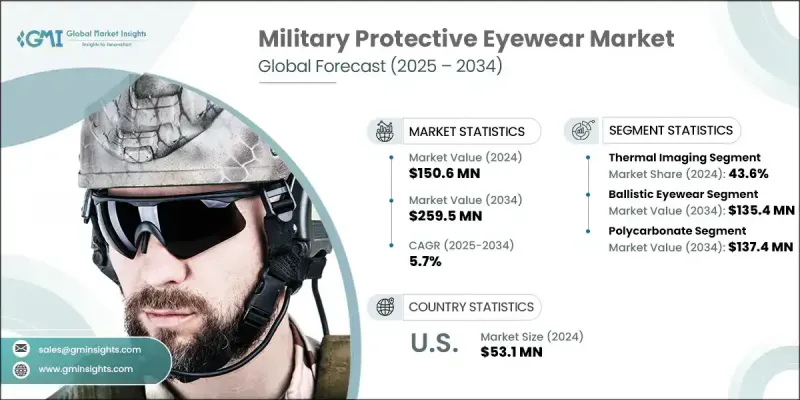

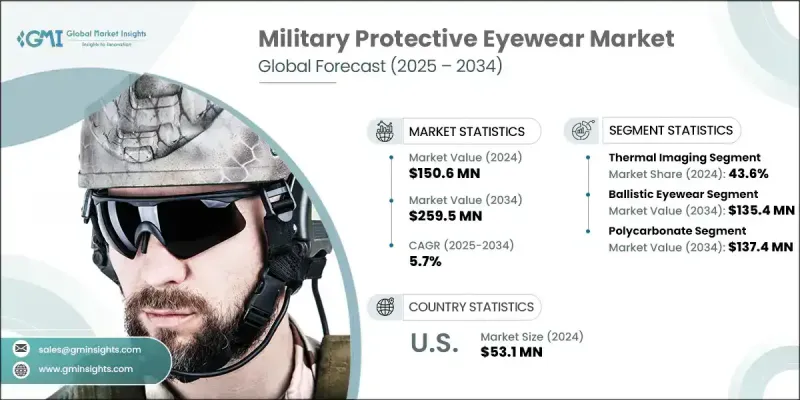

군용 보호 안경 세계 시장은 2024년에 1억 5,060만 달러로 평가되었고 CAGR 5.7%로 성장하여 2034년에는 2억 5,950만 달러에 이를 것으로 예측됩니다.

각국의 군사예산 증가와 전투시스템의 증강현실 등 스마트기술의 통합 증가가 시장 수요를 촉진하는 주요 요인입니다. 군사 조직은 군인의 안전과 작전 준비 태세를 더욱 중요시하고 있으며, 고급 아이웨어에 대한 주목의 고조로 이어지고 있습니다. 조달 형태는 라이프 사이클 비용 효율성, 성능 지속성, 보호 안경 시스템의 지속적인 연구 개발을 선호하는 장기적인 파트너십으로 진화하고 있습니다. 군은 민간기술 개발자와 협력해 특히 차세대 전술광학계의 공동프로그램을 통해 기술 혁신을 추진하고 있습니다. 또한 Additive Manufacturing과 Rapid Prototype 기술에 대한 관심도 높아져 모바일 필드 환경에서의 아이웨어 부품의 온 디맨드 작성이 가능해지고 있습니다. 이러한 진보는 물류 전략을 재구성하고 있으며, 향후 10년까지 특히 특수부대들 사이에서 미래의 작전의 중심이 될 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 1억 5,060만 달러 |

| 예측 금액 | 2억 5,950만 달러 |

| CAGR | 5.7% |

열화상 시스템은 2024년 43.6%의 점유율을 차지했습니다. 야간 임무, 정찰, 목표 추적 등 저조도나 불명료한 조건 하에서의 시인성이 요구되는 작전으로 적외선 광학 기기의 채택이 증가하고 있습니다. 컴포넌트의 소형 경량화가 추진되고 있는 가운데, 개발자는 헬멧이나 AR 대응 헤드 기어와 일체화한 컴팩트한 서멀 모듈의 개발에 임하고 있습니다. 제조업체는 저전력 소비를 유지하고 헤드업 디스플레이와 원활하게 작동하는 경량 열 장치를 혁신하도록 권장됩니다. 이러한 강화된 시스템은 장시간 임무 중에 편안함과 배터리 성능을 저하시키지 않으면서 효율적이고 첨단 기술을 활용한 필드 비전을 필요로 하는 엘리트 전투 부대에게 필수적인 도구가 되고 있습니다.

탄도 보호 안경 분야는 2034년까지 1억 3,540만 달러에 이릅니다. 이 분야는 활발한 전투지대에서 빠른 위협, 폭풍 파편, 적의 발사체에 노출될 기회가 늘어나기 때문에 더 높은 보급률을 보이고 있습니다. 보다 가벼운 프레임 디자인, 모듈식 맞춤 옵션, 내충격성을 갖춘 업그레이드 렌즈가 제품의 매력에 기여합니다. 최신의 군사·안전 인증 규격에 준거는 세계의 방위군에의 제품 전개를 뒷받침하고 있습니다. MIL-PRF 및 ANSI Z87.1과 같은 표준의 광범위한 도입은 방어 기관 전체에서 가속화되고 있습니다. 이 부문의 기업은 경쟁력을 유지하기 위해 교체 가능한 렌즈 플랫폼 개발에 점점 더 많은 노력을 기울이고 있으며, 다년간의 정부 공급 계약을 얻기 위해 고품질의 충격 컴플라이언스를 추진하고 있습니다.

북미 군용 보호 안경 2024년의 점유율은 42.4%로, 2034년까지의 CAGR은 6.7%를 나타낼 전망입니다. 강력한 국방 지출 문화, 견고한 혁신 생태계 및 보호 복의 조기 기술 도입으로 이 지역은 리더십을 유지하고 있습니다. 국방 현대화 이니셔티브와 진화하는 전장 요구 사항은 레이저 내성, 탄도 등급, AR 통합 안경을 포함한 고급 보호 광학 부품의 조달을 뒷받침하고 있습니다. 이 지역은 전투원의 생존성을 중시하고 있으며, 광범위한 R&D 지원과 함께 다양한 환경 조건 하에서 상황 인식, 실시간 조준, 위협 완화를 강화할 수 있는 차세대 안경의 기초가 구축되고 있습니다.

세계 군용 보호 안경 시장을 형성하는 주요 기업은 Honeywell, Oakley, Wiley X, 3M, Revision Military 등입니다. 군용 보호 안경 시장의 주요 기업은 그 존재감을 확고하게하기 위해 다면적인 전략에 주력하고 있습니다. 연구개발 투자를 우선하고 진화하는 군사작전의 구체적인 요구를 충족시키기 위해 탄도 성능과 광학 성능을 강화한 경량 모듈러 시스템을 설계하고 있습니다. 고가치로 장기적인 방위 계약을 확보하기 위해 정부 조달 프로토콜 및 인증과 연계하는 기업도 있습니다. 기술 파트너와의 전략적 제휴를 통해 AR, 열, HUD 시스템을 안경에 통합하는 것도 가능합니다. 기업은 일관된 납품을 보장하기 위해 공급망 허브와 지역 제조 유닛을 설립하여 고지출 지역에서 입지를 확대하고 있습니다.

목차

제1장 조사 방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역/국가

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계 방위비 증가

- 군사 근대화와 장비 업그레이드

- 증강현실과 스마트 아이웨어 시스템의 통합

- 경량으로 인체공학에 근거한 디자인의 채용

- 법 집행기관 및 준군사 조직으로부터의 조달 증가

- 업계의 잠재적 위험 및 과제

- 고급 보호 안경의 고비용

- 개발도상국의 예산제약

- 시장 기회

- 병사 근대화 프로그램에 통합

- 법 집행 기관과 국토 안보에서의 수요 증가

- 재료과학과 렌즈기술의 진보

- 레이저 및 방사선에 의한 눈 보호에 중점 강화

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신규 기술

- 새로운 비즈니스 모델

- 컴플라이언스 요건

- 국방예산 분석

- 세계의 방위비의 동향

- 지역 방위 예산 배분

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 주요 방위 근대화 프로그램

- 예산 예측(2025-2034)

- 업계의 성장에 미치는 영향

- 국가별 방위 예산

- 공급 체인의 탄력

- 지정학적 분석

- 인재 분석

- 디지털 변혁

- 합병, 인수, 전략적 파트너십의 상황

- 위험 평가 및 관리

- 주요 계약 체결(2021-2024)

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 주요 기업의 경쟁 벤치마킹

- 재무실적의 비교

- 수익

- 이익률

- 연구개발

- 제품 포트폴리오 비교

- 제품 라인업의 넓이

- 기술

- 혁신

- 지리적 존재의 비교

- 세계 실적 분석

- 서비스 네트워크의 범위

- 지역별 시장 침투율

- 경쟁 포지셔닝 매트릭스

- 리더들

- 도전자

- 팔로워

- 틈새 기업

- 전략적 전망 매트릭스

- 재무실적의 비교

- 주요 발전, 2021-2024

- 합병과 인수

- 파트너십 및 협업

- 기술적 진보

- 확대 및 투자 전략

- 지속가능성에 대한 노력

- 디지털 변혁의 대처

- 신규기업/스타트업기업경쟁 구도

제5장 시장 추정 및 예측 : 제품 유형별, 2021-2034

- 주요 동향

- 방탄 안경

- 레이저 보호 안경

- 화학·생물 보호 안경

- 야간 시력 대응 안경

- 표준 보호 안경

- 기타

제6장 시장 추정 및 예측 : 재료별, 2021-2034

- 주요 동향

- 석영

- 폴리카보네이트

- 유리 섬유

- 사파이어

- 기타

제7장 시장 추정 및 예측 : 기술별, 2021-2034

- 주요 동향

- 열화상

- 화상 증강 장치

제8장 시장 추정 및 예측 : 용도별, 2021-2034

- 주요 동향

- 사수 조준경

- 해군 추적기

- 주행 조준경

- 보병 무기 조준경

- 기타

제9장 시장 추정 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계 주요 기업

- 3M

- Honeywell International

- Oakley

- Revision Military

- Wiley X

- 지역별 주요 기업

- 북미

- ESS Eyewear

- Gentex

- Smith Optics

- 유럽

- BAE Systems

- Bolle Safety

- Thales

- 아시아태평양

- Bharat Electronics

- Day Sun Industrial

- Univet Optical Technologies

- 북미

- 틈새 기업/디스 랩터

- Elbit Systems

- Kentek

- Meopta

- NoIR Laser

- Philips Safety Products

- Uvex Safety Group

The Global Military Protective Eyewear Market was valued at USD 150.6 million in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 259.5 million by 2034.

Rising military budgets across nations and increasing integration of smart technologies such as augmented reality into combat systems are key factors driving market demand. Military organizations are placing higher importance on soldier safety and operational readiness, leading to increased focus on advanced eyewear. Procurement patterns are evolving toward long-term partnerships that prioritize lifecycle cost-efficiency, sustained performance, and continuous R&D in protective eyewear systems. Armed forces are collaborating with private tech developers to advance innovations via joint programs, especially for next-gen tactical optics. There's also a rising interest in additive manufacturing and rapid prototyping techniques, enabling on-demand creation of eyewear parts in mobile field environments. These advancements are reshaping logistics strategies and are expected to become central to future operations, particularly among special forces, by the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $150.6 Million |

| Forecast Value | $259.5 Million |

| CAGR | 5.7% |

The thermal imaging systems held a 43.6% share in 2024. The adoption of thermal optics is rising in operations requiring visibility in low-light or obscured conditions, such as night missions, reconnaissance, and target tracking. With a push to reduce the size and weight of components, developers are working on compact thermal modules that integrate with helmets and AR-enabled headgear. Manufacturers are encouraged to innovate lightweight thermal units that maintain low power consumption and work seamlessly with heads-up displays. These enhanced systems are becoming essential tools for elite combat units who require efficient, tech-enabled field vision without compromising comfort or battery performance during extended missions.

The ballistic protective eyewear segment will reach USD 135.4 million by 2034. This segment is witnessing higher uptake due to escalating exposure to high-velocity threats, blast debris, and hostile projectiles in active combat zones. Lighter frame designs, modular fit options, and upgraded lenses with high-impact resistance are all contributing to product appeal. Compliance with updated military and safety certification standards is helping drive product deployment across global defense forces. Widespread implementation of standards like MIL-PRF and ANSI Z87.1+ is accelerating across defense agencies. To retain a competitive edge, companies in this segment are increasingly focused on developing interchangeable lens platforms and working toward high-grade impact compliance to win multi-year government supply contracts.

North America Military Protective Eyewear Market held 42.4% share in 2024 and is expected to grow at a CAGR of 6.7% through 2034. A strong culture of defense spending, robust innovation ecosystems, and early tech adoption in protective gear have allowed the region to maintain leadership. Defense modernization initiatives and evolving battlefield requirements are pushing procurement of advanced protective optics, including laser-resistant, ballistic-grade, and AR-integrated eyewear. The region's focus on warfighter survivability, combined with extensive R&D support, is laying the groundwork for next-gen eyewear capable of enhancing situational awareness, real-time targeting, and threat mitigation under varied environmental conditions.

Key players shaping the Global Military Protective Eyewear Market landscape include Honeywell, Oakley, Wiley X, 3M, and Revision Military. Leading companies in the military protective eyewear market are focusing on multi-faceted strategies to solidify their presence. Prioritizing R&D investment, they are designing lightweight, modular systems with enhanced ballistic and optical capabilities to meet the specific needs of evolving military operations. Several firms are aligning with government procurement protocols and certifications to secure high-value, long-term defense contracts. Strategic collaborations with tech partners are also enabling the integration of AR, thermal, and HUD systems into eyewear. Companies are expanding their footprint in high-spending regions by establishing supply chain hubs and regional manufacturing units to ensure consistent delivery

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Material trends

- 2.2.3 Technology trends

- 2.2.4 End use application trends

- 2.2.5 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global defense expenditures

- 3.2.1.2 Military modernization and equipment upgrades

- 3.2.1.3 Integration of augmented reality and smart eyewear systems

- 3.2.1.4 Adoption of lightweight and ergonomic designs

- 3.2.1.5 Rising procurement from law enforcement and paramilitary forces

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs of advanced protective eyewear

- 3.2.2.2 Budget constraints in developing nations

- 3.2.3 Market opportunities

- 3.2.3.1 Integration into soldier modernization programs

- 3.2.3.2 Growing demand from law enforcement and homeland security

- 3.2.3.3 Advancements in material science and lens technology

- 3.2.3.4 Increased focus on laser and radiation eye protection

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Defense budget analysis

- 3.11 Global defense spending trends

- 3.12 Regional defense budget allocation

- 3.12.1 North America

- 3.12.2 Europe

- 3.12.3 Asia Pacific

- 3.12.4 Middle East and Africa

- 3.12.5 Latin America

- 3.13 Key defense modernization programs

- 3.14 Budget forecast (2025-2034)

- 3.14.1 Impact on industry growth

- 3.14.2 Defense budgets by country

- 3.15 Supply chain resilience

- 3.16 Geopolitical analysis

- 3.17 Workforce analysis

- 3.18 Digital transformation

- 3.19 Mergers, acquisitions, and strategic partnerships landscape

- 3.20 Risk assessment and management

- 3.21 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Ballistic eyewear

- 5.3 Laser protection eyewear

- 5.4 Chemical and biological protection eyewear

- 5.5 Night vision-compatible eyewear

- 5.6 Standard protective eyewear

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Material, 2021 - 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 Quartz

- 6.3 Polycarbonate

- 6.4 Glass Fiber

- 6.5 Sapphire

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Thermal imaging

- 7.3 Image intensifier

Chapter 8 Market Estimates and Forecast, By End Use Application, 2021 - 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 Gunner sights

- 8.3 Naval trackers

- 8.4 Driving sights

- 8.5 Infantry weapon sight

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (Million & Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 3M

- 10.1.2 Honeywell International

- 10.1.3 Oakley

- 10.1.4 Revision Military

- 10.1.5 Wiley X

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 ESS Eyewear

- 10.2.1.2 Gentex

- 10.2.1.3 Smith Optics

- 10.2.2 Europe

- 10.2.2.1 BAE Systems

- 10.2.2.2 Bolle Safety

- 10.2.2.3 Thales

- 10.2.3 APAC

- 10.2.3.1 Bharat Electronics

- 10.2.3.2 Day Sun Industrial

- 10.2.3.3 Univet Optical Technologies

- 10.2.1 North America

- 10.3 Niche Players / Disruptors

- 10.3.1 Elbit Systems

- 10.3.2 Kentek

- 10.3.3 Meopta

- 10.3.4 NoIR Laser

- 10.3.5 Philips Safety Products

- 10.3.6 Uvex Safety Group