|

시장보고서

상품코드

1822563

자동차용 디지털 트윈 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Digital Twin in Automotive Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

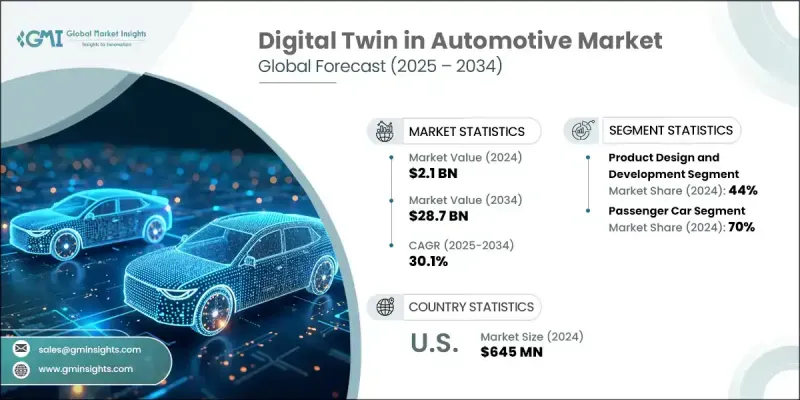

자동차용 디지털 트윈 세계 시장 규모는 2024년에 21억 달러로 평가되었고, CAGR 30.1%로 성장하고, 2034년에는 287억 달러에 달할 것으로 예측되고 있습니다.

이러한 현저한 성장은 자동차 부문 전반에 걸쳐 진행 중인 디지털 변혁에 의해 촉진되고 있습니다. Connected Technology, IoT, IIoT, Industry 4.0의 원칙에 대한 의존도가 높아짐에 따라 기존 자동차가 지능형 데이터 구동 기계로 전환되고 있습니다. 자동차가 기계 하드웨어에서 복잡한 소프트웨어 플랫폼으로 진화함에 따라 디지털 트윈 기술은 센서, 시스템 및 자동차 컴퓨터에서 대규모 데이터를 관리하는 데 사용됩니다. 자동차 제조업체는 이 데이터를 활용하여 AI, 머신러닝, 고도의 애널리틱스를 이용하여 성능 향상, 고장 방지, 예지 보전 실현을 목표로 하고 있습니다. 디지털 트윈은 설계 및 엔지니어링 변경을 시뮬레이션할 뿐만 아니라 업무 효율성 향상, 직원 교육 지도, 생산 합리화에 필수적인 것으로 입증되었습니다. 전기자동차 및 자율 주행 차량 수요가 급증함에 따라 보다 신속한 프로토타이핑 및 실시간 모니터링을 지원하는 가상 복제본의 필요성이 더욱 가속화되고 있습니다. 업계가 지속가능성, 제로 방출 이동성, 스마트 인프라를 추진하면서 디지털 트윈의 도입은 빠르게 진행될 것으로 예측됩니다. 기업은 이러한 고성장 환경에서 경쟁을 유지하기 위해 강력한 투자와 전략적 이니셔티브로 대응하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 21억 달러 |

| 예측 금액 | 287억 달러 |

| CAGR | 30.1% |

이 시장 가운데 제품 설계·개발 분야는 2024년에 44%의 점유율을 차지하고 2025년부터 2034년에 걸쳐 CAGR 29%를 보일 것으로 예측됩니다. 자동차 제조업체는 제조 전에 디지털 트윈 기술을 사용하여 차량 부품을 개발하고 검증합니다. 이를 통해 팀은 프로토타이핑 비용을 절감하고 개발 사이클을 단축하며 EV 배터리, 파워트레인, 차량의 에어로다이나믹스와 같은 복잡한 시스템의 혁신을 가속화할 수 있습니다. 초기 단계에서 복잡한 요소를 시뮬레이션함으로써 보다 신속한 테스트, 정확한 반복, 시장 출시 시간을 단축할 수 있습니다. 이러한 장점으로 OEM은 규제 일정을 앞당기면서 성능과 커스터마이징에 대한 소비자 증가 요구에 부응하고 있습니다.

승용차 부문은 2024년에 70%의 점유율을 차지하고 있으며, 2034년까지의 CAGR은 29%를 나타낼 전망입니다. 자동차 회사는 디지털 트윈을 사용하여 다양한 운전 패턴 및 환경 조건 하에서 EV 배터리의 거동을 평가합니다. 이 접근법은 열 효율, 에너지 밀도 및 배터리 안전과 같은 주요 매개 변수를 최적화하는 데 도움이 됩니다. EV 파워 시스템의 성능과 수명을 향상시킴으로써 디지털 트윈은 배출량 감소에 직접 기여하여 전기 승용차의 보급을 촉진합니다. 지속가능한 운송 솔루션을 위한 세계 추진력 증가는 이 부문에서 디지털 트윈 플랫폼의 활용을 더욱 강화하고 있습니다.

미국 자동차용 디지털 트윈 시장은 2024년에 90%의 점유율을 차지하며 6억 4,500만 달러를 창출했습니다. 미국의 자동차 생태계는 특히 전기자동차와 자율 주행 영역에서 자동차 혁신의 한계를 계속 밀고 있습니다. 기업은 디지털 트윈 환경을 활용하여 컴포넌트를 가상으로 테스트하고 성능을 미세 조정하며 실제 고장을 기다리지 않고 배터리 관리 등의 과제를 해결하고 있습니다. 이러한 솔루션은 신뢰성을 높이면서 제품 개발 기간을 크게 단축합니다. 신속한 설계에서 전개까지의 사이클에 대한 수요 증가는 이 지역 전체 시장 기세를 가속화하는데 중요한 역할을 합니다.

세계 자동차용 디지털 트윈 시장에서 주요 기업으로는 Capgemini, Siemens, General Electric, Microsoft, IBM, Bosch, and Dassault Systemes 등이 있습니다. 이러한 기업들은 자동차 산업을 위한 맞춤형 시뮬레이션 및 모델링 기술의 발전에 크게 기여하고 있습니다. 디지털 트윈 자동차 분야의 선두 기업은 지속적인 혁신, 협업 파트너십, 중점적인 인수를 통해 시장에서의 존재감을 높이고 있습니다. 대부분은 AI와 고급 분석을 자체 플랫폼에 통합하여 예측 진단 및 실시간 모니터링 기능을 제공합니다. 또한 컨셉부터 운영까지 차량 라이프사이클의 다양한 단계에 대응하는 커스터마이징 가능하고 확장 가능한 솔루션을 개발하고 있습니다. 경쟁력을 강화하기 위해 기업은 자동차 제조업체 및 소프트웨어 개발 회사와 전략적 제휴를 맺어 세계 비즈니스 배포에서 디지털 트윈 도구의 도입을 효율화하고 있습니다.

목차

제1장 조사 방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역/국가

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 채택에 있어서의 AI와 자동화의 도입 증가

- 집중형 채용 플랫폼의 요구 증가

- 리모트 워크와 하이브리드 워크의 문화의 확대

- CRM 및 HRIS 시스템과의 통합

- 데이터에 근거한 채택 결정에의 이행

- 업계의 잠재적 위험 및 과제

- 초기 설정과 높은 구독 비용

- 데이터의 프라이버시와 컴플라이언스에 대한 우려

- 레거시 시스템과의 통합 복잡성

- 자동화의 과잉 사용에 의한 후보자의 체험 문제

- 틈새 시장에 대한 맞춤화 제한

- 시장 기회

- AI에 의한 후보자 발굴과 스킬 매칭

- 신흥 시장으로 확대

- 비디오 인터뷰 및 평가 도구와의 통합

- 프리랜서&기그 이코노미의 채택

- 모바일 퍼스트 ATS 도입

- HR테크 생태계 파트너십

- 성장 촉진요인

- 디지털 트윈 기술의 기반과 아키텍처

- 디지털 트윈의 기초와 진화

- 디지털 트윈 유형 : 제품, 프로세스, 성과, 자산, 시스템

- 디지털 스레드와 데이터의 상호 운용성

- 모델 기반 시스템 엔지니어링(MBSE)

- 물리-디지털-물리(PDP) 루프

- 실시간 데이터 동기화 및 피드백

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 혁신과 고급 기능

- 시뮬레이션 엔진과 솔버 기술

- IoT 센서 통합 및 데이터 수집

- 엣지 컴퓨팅, 5G, 실시간 디지털 트윈

- AI/ML 모델 관리와 시뮬레이션 자동화

- AR/VR과 몰입형 시각화

- 클라우드, On-Premise, 하이브리드 아키텍처

- API 및 시스템 통합 기능

- 가격 동향 분석

- 코스트 내역 분석

- 특허 분석

- 기술 분야별 특허 포트폴리오 분석

- 특허 출원 동향과 혁신 활동

- 경쟁특허정보

- 지속가능성과 환경 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적인 노력

- 탄소발자국의 고려

- 이용 사례

- 제품 설계 및 가상 프로토타이핑

- 컨셉 설계, 시뮬레이션, 테스트

- 경량화와 재료 최적화

- 충돌 및 충격 시뮬레이션

- 제조업과 스마트 팩토리

- 생산계획과 스케줄링

- 로봇 공학과 자동화의 통합

- 품질 관리 및 실시간 감시

- 공장 레이아웃과 공정 최적화

- 차량 성능과 라이프사이클 관리

- 예지보전과 상태감시

- 보증 분석 및 리콜 관리

- 플릿 관리 및 사용 상황 분석

- OTA 업데이트 및 서비스 중 업그레이드

- 공급망과 물류 최적화

- 공급망의 디지털 트윈과 가시성

- 재고 최적화 및 수요 예측

- 공급업체와의 연계와 리스크 관리

- 물류 네트워크 시뮬레이션

- 고객 경험과 애프터 판매

- 개인화된 차량 구성 및 판매

- 디지털 쇼룸과 VR/AR 비주얼라이제이션

- 커넥티드 서비스와 원격 진단

- 고객 피드백 루프와 제품 개선

- 규제, 보증, 컴플라이언스의 디지털 트윈

- 규정 준수 및 디지털 보고서

- 보증 청구 및 근본 원인 분석

- 안전 인증 및 감사 추적

- 제품 설계 및 가상 프로토타이핑

- 최상의 시나리오

- 제품 수명, 재활용, 순환형 경제

- 해체와 재활용을 위한 디지털 트윈

- 재제조, 재사용, 순환형 공급망

- 규제보고 및 규정 준수

- 수명 주기 평가 및 탄소 영향

- 비즈니스 모델의 혁신과 수익화

- 서비스형 디지털 트윈(DTaaS)

- 종량 과금제와 구독 모델

- 가치 기반 가격 설정 및 성과 기반 모델

- 디지털 트윈 수익화 및 데이터 라이선싱

- 조직 변경, 인재, 프로세스 변혁

- 변경 관리와 디지털 트윈의 도입

- 노동력의 재교육과 인재 개발

- 디지털 트윈 성숙도 모델과 조직의 준비 상황

- 프로세스 리엔지니어링과 민첩한 변화

- 에코시스템, 표준, 컨소시엄

- 업계 표준 및 레퍼런스 아키텍처

- 디지털 트윈 컨소시엄, ASAM, 기타 얼라이언스

- 오픈소스 vs 독점 솔루션

- 생태계 파트너십과 상호 운용성

- 지속가능성, ESG, 수명주기 평가

- 탄소 실적 분석 및 보고서

- ESG 지표와 규정 준수

- 지속 가능한 디자인과 그린 제조

- 순환형 경제와 자원 최적화

- ROI, 비용 효과, 회수 기간의 분석

- 구현 비용 구조 및 투자 요구 사항

- 운영 및 재무상의 이점

- 전략적 이점과 경쟁 우위

- ROI 프레임워크와 회수 기간 분석

- 미래 시나리오와 혼란 분석

- 자율주행차와 디지털 트윈의 통합

- MaaS, 스마트 시티, V2 X

- 규제의 진화와 정책의 영향

- 기술의 파괴와 산업 변혁

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획과 자금조달

제5장 시장 추정 및 예측 : 전개 모드별, 2021-2034

- 주요 동향

- 클라우드

- On-Premise

- 하이브리드

제6장 시장 추정 및 예측 : 차량별, 2021-2034

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 경작

- 중형

- Heavy-duty

제7장 시장 추정 및 예측 : 기술별, 2021-2034

- 주요 동향

- 시스템 디지털 트윈

- 제품 디지털 트윈

- 프로세스 디지털 트윈

제8장 시장 추정 및 예측 : 용도별, 2021-2034

- 주요 동향

- 제품 설계 및 개발

- 기계 및 장비의 건강 상태 모니터링

- 프로세스 지원 및 서비스

제9장 시장 추정 및 예측 : 최종 용도별, 2021-2034

- 주요 동향

- OEM

- Tier 1 공급업체

- 자동차 소프트웨어 및 기술 기업

- 이동성 서비스 제공업체

- 애프터마켓과 서비스 센터

제10장 시장 추정 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Global Leaders

- Altair

- Ansys

- Autodesk

- Capgemini

- Dassault Systemes

- General Electric

- IBM

- Microsoft

- Oracle

- PTC

- SAP

- Siemens

- Regional Champions

- AVL

- Bentley Systems

- Bosch

- Cognizant

- Hexagon

- KPIT Technologies

- Tata Technologies

- 신규 기업/파괴적 혁신

- Bosch

- General Electric

- Siemens Energy

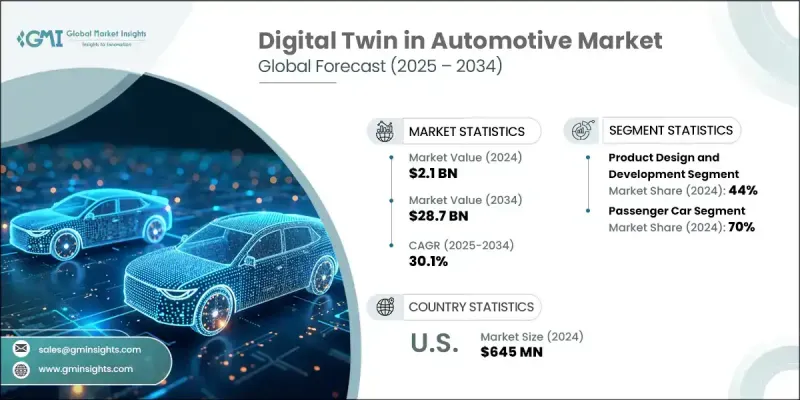

The Global Digital Twin in Automotive Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 30.1% to reach USD 28.7 billion by 2034.

This significant growth is being fueled by the ongoing digital transformation across the automotive sector. Increasing reliance on connected technologies, IoT, IIoT, and Industry 4.0 principles is transforming traditional vehicles into intelligent, data-driven machines. As vehicles evolve from mechanical hardware to complex software platforms, digital twin technology is being used to manage large-scale data from sensors, systems, and onboard computers. Automakers are leveraging this data to improve performance, prevent breakdowns, and enable predictive maintenance using AI, machine learning, and advanced analytics. Digital twins are proving vital not only in simulating design and engineering changes but also in enhancing operational efficiency, guiding workforce training, and streamlining production. The surge in demand for electric and autonomous vehicles is further accelerating the need for virtual replicas that support faster prototyping and real-time monitoring. As the industry pushes toward sustainability, zero-emission mobility, and smart infrastructure, digital twin adoption is expected to rise rapidly. Companies are responding with strong investment and strategic initiatives to remain competitive in this high-growth environment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $28.7 Billion |

| CAGR | 30.1% |

Within this market, the product design and development segment held a 44% share in 2024 and is set to grow at a CAGR of 29% between 2025 and 2034. Automakers are using digital twin technology to develop and validate vehicle components before manufacturing. This allows teams to reduce prototyping costs, shorten development cycles, and speed up innovation for complex systems like EV batteries, powertrains, and vehicle aerodynamics. The simulation of intricate elements at an early stage enables faster testing, accurate iteration, and quicker time-to-market. These benefits are helping OEMs meet growing consumer demands for performance and customization while staying ahead of regulatory timelines.

The passenger car segment held a 70% share in 2024 and is expected to grow at a CAGR of 29% through 2034. Automotive companies are using digital twins to evaluate how EV batteries behave under diverse driving patterns and environmental conditions. This approach helps optimize key parameters such as thermal efficiency, energy density, and battery safety. By improving the performance and lifespan of EV power systems, digital twins contribute directly to reducing emissions and encouraging broader adoption of electric passenger vehicles. The growing global push toward sustainable transport solutions is further intensifying the use of digital twin platforms in this segment.

United States Digital Twin in Automotive Market held a 90% share in 2024, generating USD 645 million. The US automotive ecosystem continues to push the boundaries of vehicle innovation, especially in the electric and autonomous space. Companies are using digital twin environments to test components virtually, fine-tune performance, and address challenges like battery management all without waiting for real-world failures. These solutions are significantly cutting down product development time while increasing dependability. The growing demand for rapid design-to-deployment cycles is playing a critical role in accelerating market momentum across the region.

Leading companies in the Global Digital Twin in Automotive Market include Capgemini, Siemens, General Electric, Microsoft, IBM, Bosch, and Dassault Systemes. These players are key contributors to the advancement of simulation and modeling technologies tailored for the automotive landscape. Top companies in the digital twin automotive space are expanding their market presence through continuous innovation, collaborative partnerships, and focused acquisitions. Many are integrating AI and advanced analytics into their platforms to offer predictive diagnostics and real-time monitoring features. Organizations are also developing customizable, scalable solutions that cater to different stages of the vehicle lifecycle from concept to operation. To enhance competitiveness, firms are forming strategic alliances with automakers and software developers to streamline the implementation of digital twin tools across global operations.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Deployment Mode

- 2.2.3 Vehicle

- 2.2.4 Technology

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of AI & automation in recruitment

- 3.2.1.2 Increasing need for centralized recruitment platforms

- 3.2.1.3 Growing remote & hybrid work culture

- 3.2.1.4 Integration with CRM and HRIS systems

- 3.2.1.5 Shift toward data-driven hiring decisions

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial setup and subscription costs

- 3.2.2.2 Data privacy & compliance concerns

- 3.2.2.3 Integration complexity with legacy systems

- 3.2.2.4 Candidate experience issues from automation overuse

- 3.2.2.5 Limited customization for niche industries

- 3.2.3 Market opportunities

- 3.2.3.1 AI-driven candidate sourcing & skill-matching

- 3.2.3.2 Expansion in emerging markets

- 3.2.3.3 Integration with video interviewing & assessment tools

- 3.2.3.4 Freelance & gig economy recruitment

- 3.2.3.5 Mobile-first ATS adoption

- 3.2.3.6 HR tech ecosystem partnerships

- 3.2.1 Growth drivers

- 3.3 Digital Twin Technology Foundation and Architecture

- 3.3.1 Digital Twin Fundamentals and Evolution

- 3.3.2 Types of Digital Twins: Product, Process, Performance, Asset, System

- 3.3.3 Digital Thread and Data Interoperability

- 3.3.4 Model-Based Systems Engineering (MBSE)

- 3.3.5 Physical-Digital-Physical (PDP) Loop

- 3.3.6 Real-Time Data Synchronization and Feedback

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology innovation and advanced features

- 3.8.1 Simulation Engines and Solver Technology

- 3.8.2 IoT Sensor Integration and Data Acquisition

- 3.8.3 Edge Computing, 5G, and Real-Time Digital Twins

- 3.8.4 AI/ML Model Management and Simulation Automation

- 3.8.5 AR/VR and Immersive Visualization

- 3.8.6 Cloud, On-Premises, and Hybrid Architectures

- 3.8.7 API and System Integration Capabilities

- 3.9 Price trend analysis

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.11.1 Patent Portfolio Analysis by Technology Area

- 3.11.2 Patent Filing Trends and Innovation Activity

- 3.11.3 Competitive Patent Intelligence

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon Footprint Considerations

- 3.13 Use cases

- 3.13.1 Product Design and Virtual Prototyping

- 3.13.1.1 Concept Design, Simulation, and Testing

- 3.13.1.2 Lightweighting and Material Optimization

- 3.13.1.3 Crash and Impact Simulation

- 3.13.2 Manufacturing and Smart Factory

- 3.13.2.1 Production Planning and Scheduling

- 3.13.2.2 Robotics and Automation Integration

- 3.13.2.3 Quality Control and Real-Time Monitoring

- 3.13.2.4 Factory Layout and Process Optimization

- 3.13.3 Vehicle Performance and Lifecycle Management

- 3.13.3.1 Predictive Maintenance and Condition Monitoring

- 3.13.3.2 Warranty Analytics and Recall Management

- 3.13.3.3 Fleet Management and Usage Analytics

- 3.13.3.4 OTA Updates and In-Service Upgrades

- 3.13.4 Supply Chain and Logistics Optimization

- 3.13.4.1 Supply Chain Digital Twin and Visibility

- 3.13.4.2 Inventory Optimization and Demand Forecasting

- 3.13.4.3 Supplier Collaboration and Risk Management

- 3.13.4.4 Logistics Network Simulation

- 3.13.5 Customer Experience and Aftersales

- 3.13.5.1 Personalized Vehicle Configuration and Sales

- 3.13.5.2 Digital Showroom and VR/AR Visualization

- 3.13.5.3 Connected Services and Remote Diagnostics

- 3.13.5.4 Customer Feedback Loop and Product Improvement

- 3.13.6 Regulatory, Warranty, and Compliance Digital Twins

- 3.13.6.1 Regulatory Compliance and Digital Reporting

- 3.13.6.2 Warranty Claims and Root Cause Analysis

- 3.13.6.3 Safety Certification and Audit Trail

- 3.13.1 Product Design and Virtual Prototyping

- 3.14 Best-case scenario

- 3.15 End-of-Life, Recycling, and Circular Economy

- 3.15.1 Digital Twin for Dismantling and Recycling

- 3.15.2 Remanufacturing, Reuse, and Circular Supply Chains

- 3.15.3 Regulatory Reporting and Compliance

- 3.15.4 Lifecycle Assessment and Carbon Impact

- 3.16 Business Model Innovation & Monetization

- 3.16.1 Digital Twin as a Service (DTaaS)

- 3.16.2 Pay-per-Use and Subscription Models

- 3.16.3 Value-Based Pricing and Outcome-Based Models

- 3.16.4 Digital Twin Monetization and Data Licensing

- 3.17 Organizational Change, Workforce, and Process Transformation

- 3.17.1 Change Management and Digital Twin Adoption

- 3.17.2 Workforce Reskilling and Talent Development

- 3.17.3 Digital Twin Maturity Models and Organizational Readiness

- 3.17.4 Process Reengineering and Agile Transformation

- 3.18 Ecosystem, Standards, and Consortia

- 3.18.1 Industry Standards and Reference Architectures

- 3.18.2 Digital Twin Consortium, ASAM, and Other Alliances

- 3.18.3 Open Source vs Proprietary Solutions

- 3.18.4 Ecosystem Partnerships and Interoperability

- 3.19 Sustainability, ESG, and Lifecycle Assessment

- 3.19.1 Carbon Footprint Analytics and Reporting

- 3.19.2 ESG Metrics and Compliance

- 3.19.3 Sustainable Design and Green Manufacturing

- 3.19.4 Circular Economy and Resource Optimization

- 3.20 ROI, Cost-Benefit, and Payback Analysis

- 3.20.1 Implementation Cost Structure and Investment Requirements

- 3.20.2 Operational and Financial Benefits

- 3.20.3 Strategic Benefits and Competitive Advantage

- 3.20.4 ROI Frameworks and Payback Period Analysis

- 3.21 Future Scenarios and Disruption Analysis

- 3.21.1 Autonomous Vehicles and Digital Twin Integration

- 3.21.2. MaaS, Smart Cities, and V2 X

- 3.21.3 Regulatory Evolution and Policy Impact

- 3.21.4 Technology Disruption and Industry Transformation

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Deployment Mode, 2021-2034 ($Bn)

- 5.1 Key trends

- 5.2 Cloud

- 5.3 On-premises

- 5.4 Hybrid

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021-2034 ($Bn)

- 6.1 Key trends

- 6.2 Passenger car

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicle

- 6.3.1 Light duty

- 6.3.2 Medium-duty

- 6.3.3 Heavy-duty

Chapter 7 Market Estimates & Forecast, By Technology, 2021-2034 ($Bn)

- 7.1 Key trends

- 7.2 System digital twin

- 7.3 Product digital twin

- 7.4 Process digital twin

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 ($Bn)

- 8.1 Key trends

- 8.2 Product design and development

- 8.3 Machine and equipment health monitoring

- 8.4 Process support and service

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2034 ($Bn)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Tier 1 suppliers

- 9.4 Automotive software and technology companies

- 9.5 Mobility service providers

- 9.6 Aftermarket and service centers

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Leaders

- 11.1.1 Altair

- 11.1.2 Ansys

- 11.1.3 Autodesk

- 11.1.4 Capgemini

- 11.1.5 Dassault Systemes

- 11.1.6 General Electric

- 11.1.7 IBM

- 11.1.8 Microsoft

- 11.1.9 Oracle

- 11.1.10 PTC

- 11.1.11 SAP

- 11.1.12 Siemens

- 11.2 Regional Champions

- 11.2.1 AVL

- 11.2.2 Bentley Systems

- 11.2.3 Bosch

- 11.2.4 Cognizant

- 11.2.5 Hexagon

- 11.2.6 KPIT Technologies

- 11.2.7 Tata Technologies

- 11.3 Emerging Players / Disruptors

- 11.3.1 Bosch

- 11.3.2 General Electric

- 11.3.3 Siemens Energy