|

시장보고서

상품코드

1822607

자동차 보안 시스템 시장 : 기회, 성장 촉진요인, 산업 동향 분석과 예측(2025-2034년)Car Security System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

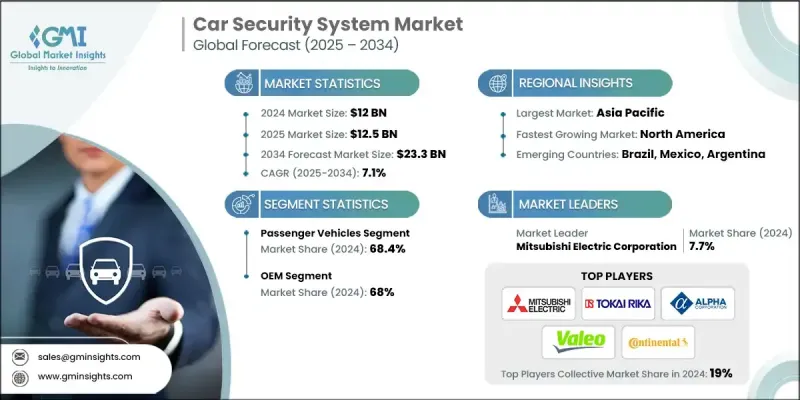

자동차 보안 시스템 세계 시장 규모는 2024년에 120억 달러에 달했고, CAGR 7.1%로 성장하고, 2034년에는 233억 달러에 이를 것으로 예측됩니다.

세계 차량 도난이 증가하고 있는 것이 고급 자동차 보안 시스템 수요 증가의 주요 요인이 되고 있습니다. 도난의 수법이 교묘해지면서, 전통적인 잠금 메커니즘만으로는 더 이상 무단 접근을 막거나 방지하기에 충분하지 않습니다. 따라서 소비자와 자동차 제조업체 모두 GPS 기반 추적 시스템, 엔진 이모빌라이저, 암호화 키리스 엔트리, 실시간 경고 알림 등 강력한 보안 기술을 선호합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 120억 달러 |

| 예측 금액 | 233억 달러 |

| CAGR | 7.1% |

승용차에서의 채택 증가

강화된 안전과 도난 방지 솔루션에 대한 소비자 수요 증가로 승용차 부문은 2024년에 큰 점유율을 차지했습니다. 도시화의 진전과 자동차 소유율의 상승에 따라, 승용차의 소유자는 자산을 보호하기 위해 키리스 엔트리, 이모빌라이저, GPS 추적 등의 고급 보안 기술에 많은 투자를 하고 있습니다. 이 부문의 성장을 뒷받침하는 것은 편의성과 보호의 양립을 요구하는 소비자의 기호이며, 제조업체 각 사는 끊임없는 기술 혁신에 임하고 있습니다.

견인 역할을 하는 OEM

OEM 분야는 신차에 고급 보안 기능을 직접 통합하는 것을 배경으로 2024년에 주목할만한 점유율을 획득했습니다. OEM은 생체인증, 암호화 키포브, 커넥티드 차량 보안 솔루션과 같은 시스템을 제조하는 동안 통합하기 위해 기술 제공업체와의 협력을 더욱 강화하고 있습니다. 이 통합은 차량 안전을 향상시킬 뿐만 아니라 원활한 사용자 경험을 제공하며 자동차 제조업체에게 경쟁 우위를 제공합니다.

지역별 인사이트

유리한 지역으로 상승하는 아시아태평양

아시아태평양의 자동차 보안 시스템 시장은 급속한 도시화, 자동차 판매 증가, 인구 밀집 도시의 범죄율 상승에 힘입어 2024년에는 큰 점유율을 차지합니다. 중국, 인도, 동남아시아 등 시장에서는 자동차 안전에 대한 소비자의 의식이 높아지고 있으며, 고급 보안 솔루션의 채택이 증가하고 있습니다. 또한 스마트시티 구상과 자동차 기술에 대한 투자 증가가 커넥티드 자동차 보안 시스템과 지능형 자동차 보안 시스템에 대한 수요를 촉진하고 있습니다.

자동차 보안 시스템 시장의 주요 기업은 Tesla, Tokai Rika, Mitsubishi Electric, Qualcomm Technologies, ZF Friedrichshafen, ALPHA Corporation, Thales Group, Continental, Stoneridge, Valeo SA 등 입니다.

시장 포지션을 강화하기 위해 자동차 보안 시스템 업계의 기업은 혁신과 전략적 파트너십을 선호합니다. AI를 활용한 침입 감지, 스마트폰과의 연계, 생체인증 입퇴실 관리 등 최첨단 기술을 개발하기 위해 연구개발에 많은 투자를 하고 있습니다. 자동차 제조업체와의 협업은 OEM의 원활한 통합을 가능하게 하고, 시스템의 신뢰성과 고객의 신뢰를 높입니다. 또한 기업은 새로운 고객 기반을 개척하기 위해 인수 및 신흥 시장 진출을 통해 사업 영역을 확대하고 있습니다. 유지 보수 및 원격 모니터링을 포함한 종합적인 애프터 서비스를 제공함으로써 기업은 장기적인 관계를 구축하고 경쟁 구도에서 차별화를 도모 할 수 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 차량 도난과 사이버 범죄 증가

- 커넥티드카와 자율주행차의 성장

- 자동차 사이버 보안에 대한 규제 추진

- 스마트 기능에 대한 소비자 수요

- 업계의 잠재적 위험 및 과제

- 높은 도입 비용

- 기술의 복잡성과 신뢰성 문제

- 시장 기회

- 생체인증 보안 도입

- 스마트 모빌리티와 IoT와의 통합

- 애프터마켓의 성장 가능성

- 블록체인 기반의 키 관리

- 성장 촉진요인

- 성장 가능성 분석

- 특허 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 공급망의 취약성 평가

- Tier-1, Tier-2, Tier-3 공급업체의 위험 분석

- 사이버 보안 공급망 요구 사항

- 컴포넌트 인증 및 검증

- 공급망의 혼란의 영향 분석

- 리스크 경감 전략과 모범 사례

- 공급업체 인증 및 규정 준수 요건

- 기술 채용 및 성숙도 분석

- 제품 카테고리별 기술 성숙도(TRL) 평가

- 지역별·차종별 채택 곡선 분석

- 기술 통합의 복잡성 매트릭스

- 상호 운용성과 표준화의 타임라인

- 혁신 파이프라인과 R&D 투자 분석

- 특허정세와 지적재산 전략 분석

- 기술 진부화 위험 평가

- 비용 편익과 ROI 분석 프레임워크

- 총소유비용(TCO) 모델

- OEM과 애프터마켓의 ROI 분석

- 보험료에 대한 영향의 정량화

- 도난 방지 비용 편익 분석

- 유지 보수 및 수명주기 비용 내역

- 기술 업그레이드 및 마이그레이션 비용

- 소비자의 지불 의사 분석

- 규제 규정 준수 및 표준 분석

- UNECE R155/R156 준거 코스트 분석

- ISO/SAE 21434 구현 요건

- 지역 규제 상황의 비교

- 사이버 보안 관리 시스템(CSMS)의 비용

- 소프트웨어 갱신 관리 시스템(SUMS)의 요건

- 인증 및 감사 프로세스 분석

- 컴플라이언스 타임라인과 벌칙 평가

- 미래의 규제 동향과 영향

- 소비자 행동과 시장 채용 분석

- 소비자의 보안 의식과 인식에 관한 조사

- 구입 결정 요인과 가격 감도

- 인구통계 부문에 의한 기술의 수용

- 지역에 의한 소비자의 기호의 차이

- 도입 장벽과 저항 요인

- 브랜드 신뢰와 보안 인식 분석

- 소비자 교육 및 계발 프로그램

- 최종 사용자 경험과 만족도 분석

- 보험업계의 통합과 파트너십 분석

- 보험료 삭감 모델

- 텔레매틱스와 이용 기반 보험의 통합

- 리스크 평가와 보험 수리상의 영향

- 보험사의 제휴 전략

- 클레임 삭감과 손실 방지 분석

- 데이터 공유 계약 및 개인 정보 보호 고려 사항

- 보험 통합에 관한 규제 요건

- 장래의 보험 업계의 제휴 모델

- 특허 분석

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적인 노력

- 탄소발자국의 고려

- 이용 사례

- 최상의 시나리오

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획과 자금조달

제5장 시장 추정 및 예측 : 차량별, 2021-2034

- 주요 동향

- 승용차

- 상용차

- 전기자동차와 하이브리드 자동차

제6장 시장 추정 및 예측 : 제품별, 2021-2034

- 주요 동향

- 이모빌라이저

- 리모트 키리스 엔트리

- 집중 잠금 시스템

- 자동차 경보

- 기타

제7장 시장 추정 및 예측 : 기술별, 2021-2034

- 주요 동향

- 기본 보안

- 중간 정도 보안

- 고급 보안

- 통합 보안 생태계

제8장 시장 추정 및 예측 : 판매채널별, 2021-2034

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추정 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계 기업

- Continental AG

- Delphi Technologies(BorgWarner)

- Denso Corporation

- Johnson Controls International

- Lear Corporation

- Magna International

- Robert Bosch

- Valeo

- 지역 기업

- Alps Electric

- Mitsubishi Electric

- STRATTEC Security

- Tokai Rika

- TRW Automotive(ZF Friedrichshafen)

- Viper(VOXX International)

- 신규 기업

- NXP Semiconductors NV

- Qualcomm Technologies

- Tesla

- Thales Group

- Upstream Security

- VicOne(Trend Micro)

The Global Car Security System Market was valued at USD 12 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 23.3 billion by 2034.

The growing incidence of vehicle theft worldwide is a major driver behind the increased demand for advanced car security systems. As theft methods become more sophisticated, traditional locking mechanisms are no longer sufficient to deter or prevent unauthorized access. This has prompted both consumers and automakers to prioritize robust security technologies such as GPS-based tracking systems, engine immobilizers, encrypted keyless entry, and real-time alert notifications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12 Billion |

| Forecast Value | $23.3 Billion |

| CAGR | 7.1% |

Rising Adoption in Passenger Vehicles

The passenger vehicle segment held a substantial share in 2024, driven by rising consumer demand for enhanced safety and anti-theft solutions. With increasing urbanization and higher vehicle ownership, owners of passenger cars are investing heavily in advanced security technologies such as keyless entry, immobilizers, and GPS tracking to safeguard their assets. This segment's growth is supported by consumer preferences for convenience combined with protection, pushing manufacturers to innovate continually.

OEM to Gain Traction

The OEM segment generated a notable share in 2024, backed by integrating advanced security features directly into new vehicles. OEMs are increasingly collaborating with technology providers to embed systems like biometric authentication, encrypted key fobs, and connected vehicle security solutions during manufacturing. This integration not only enhances vehicle safety but also offers seamless user experiences, giving automakers a competitive advantage.

Regional Insight

Asia Pacific to Emerge as a Lucrative Region

Asia Pacific car security system market held a sizeable share in 2024, supported by rapid urbanization, increasing vehicle sales, and rising crime rates in densely populated cities. Markets such as China, India, and Southeast Asia are witnessing heightened consumer awareness about vehicle safety, which is translating into increased adoption of sophisticated security solutions. Furthermore, growing investments in smart city initiatives and automotive technology are fueling demand for connected and intelligent car security systems.

Major players in the car security system market are Tesla, Tokai Rika, Mitsubishi Electric, Qualcomm Technologies, ZF Friedrichshafen, ALPHA Corporation, Thales Group, Continental, Stoneridge, and Valeo S.A.

To strengthen their market position, companies in the car security system industry are prioritizing innovation and strategic partnerships. They are investing heavily in R&D to develop cutting-edge technologies like AI-powered intrusion detection, smartphone integration, and biometric access control. Collaborations with automakers enable seamless OEM integration, enhancing system reliability and customer trust. Additionally, firms are expanding their footprint through acquisitions and entering emerging markets to tap into new customer bases. Providing comprehensive after-sales services, including maintenance and remote monitoring, also helps companies build long-term relationships and differentiate themselves in a competitive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.1.3 Base estimates and calculations

- 1.1.4 Base year calculation

- 1.1.5 Key trends for market estimates

- 1.1.6 GMI proprietary AI system

- 1.1.6.1 AI-Powered research enhancement

- 1.1.6.2 Source consistency protocol

- 1.1.6.3 AI accuracy metrics

- 1.2 Forecast model

- 1.3 Primary research and validation

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario Analysis Framework

- 1.4 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Secondary

- 1.5.1.1 Paid Sources

- 1.5.1.2 Public Sources

- 1.5.1.3 Sources, by region

- 1.5.1 Secondary

- 1.6 Research Trail & Confidence Scoring

- 1.6.1 Research Trail Components:

- 1.6.2 Scoring Components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment Model

- 2.2.4 Organization Size

- 2.2.5 Solution

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising vehicle theft & cybercrime

- 3.2.1.2 Growth in connected & autonomous vehicles

- 3.2.1.3 Regulatory push for automotive cybersecurity

- 3.2.1.4 Consumer demand for smart features

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation costs

- 3.2.2.2 Technology complexity & reliability issues

- 3.2.3 Market opportunities

- 3.2.3.1 Biometric security adoption

- 3.2.3.2 Integration with smart mobility & IoT

- 3.2.3.3 Aftermarket growth potential

- 3.2.3.4 Blockchain-based key management

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Patent analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Supply Chain Vulnerability Assessment

- 3.8.1 Tier-1, Tier-2, Tier-3 supplier risk analysis

- 3.8.2 Cybersecurity supply chain requirements

- 3.8.3 Component authentication and validation

- 3.8.4 Supply chain disruption impact analysis

- 3.8.5 Risk mitigation strategies and best practices

- 3.8.6 Supplier certification and compliance requirements

- 3.9 Technology Adoption and Maturity Analysis

- 3.9.1 Technology readiness level (TRL) assessment by product category

- 3.9.2 Adoption curve analysis by region and vehicle segment

- 3.9.3 Technology integration complexity matrix

- 3.9.4 Interoperability and standardization timeline

- 3.9.5 Innovation pipeline and R&D investment analysis

- 3.9.6 Patent landscape and ip strategy analysis

- 3.9.7 Technology obsolescence risk assessment

- 3.10 Cost-Benefit and ROI Analysis Framework

- 3.10.1 Total cost of ownership (TCO) models

- 3.10.2 ROI analysis for OEMs vs. aftermarket

- 3.10.3 Insurance premium impact quantification

- 3.10.4 Theft prevention cost-benefit analysis

- 3.10.5 Maintenance and lifecycle cost breakdown

- 3.10.6 Technology upgrade and migration costs

- 3.10.7 Consumer willingness-to-pay analysis

- 3.11 Regulatory Compliance and Standards Analysis

- 3.11.1 UNECE R155/R156 compliance cost analysis

- 3.11.2 ISO/SAE 21434 implementation requirements

- 3.11.3 Regional regulatory landscape comparison

- 3.11.4 Cybersecurity management system (CSMS) costs

- 3.11.5 Software update management system (SUMS) requirements

- 3.11.6 Certification and audit process analysis

- 3.11.7 Compliance timeline and penalty assessment

- 3.11.8 Future regulatory trends and impact

- 3.12 Consumer Behavior and Market Adoption Analysis

- 3.12.1 Consumer security awareness and perception studies

- 3.12.2 Purchase decision factors and price sensitivity

- 3.12.3 Technology acceptance by demographic segments

- 3.12.4 Regional consumer preference variations

- 3.12.5 Adoption barriers and resistance factors

- 3.12.6 Brand trust and security perception analysis

- 3.12.7 Consumer education and awareness programs

- 3.12.8 End Use experience and satisfaction analysis

- 3.13 Insurance Industry Integration and Partnership Analysis

- 3.13.1 Insurance premium reduction models

- 3.13.2 Telematics and usage-based insurance integration

- 3.13.3 Risk assessment and actuarial impact

- 3.13.4 Insurance company partnership strategies

- 3.13.5 Claims reduction and loss prevention analysis

- 3.13.6 Data sharing agreements and privacy considerations

- 3.13.7 Regulatory requirements for insurance integration

- 3.13.8 Future insurance industry collaboration models

- 3.14 Patent analysis

- 3.15 Sustainability and environmental aspects

- 3.15.1 Sustainable practices

- 3.15.2 Waste reduction strategies

- 3.15.3 Energy efficiency in production

- 3.15.4 Eco-friendly Initiatives

- 3.15.5 Carbon footprint considerations

- 3.16 Use cases

- 3.17 Best-case scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.3 Commercial vehicles

- 5.4 Electric & hybrid vehicles

Chapter 6 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Immobilizer

- 6.3 Remote keyless entry

- 6.4 Central locking system

- 6.5 Car alarm

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Basic security

- 7.3 Intermediate security

- 7.4 Advanced security

- 7.5 Integrated security ecosystems

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1. Global Players

- 10.1.1 Continental AG

- 10.1.2 Delphi Technologies (BorgWarner)

- 10.1.3 Denso Corporation

- 10.1.4 Johnson Controls International

- 10.1.5 Lear Corporation

- 10.1.6 Magna International

- 10.1.7 Robert Bosch

- 10.1.8 Valeo

- 10.2 Regional Players

- 10.2.1 Alps Electric

- 10.2.2 Mitsubishi Electric

- 10.2.3 STRATTEC Security

- 10.2.4 Tokai Rika

- 10.2.5 TRW Automotive (ZF Friedrichshafen)

- 10.2.6 Viper (VOXX International)

- 10.3 Emerging Players

- 10.3.1 NXP Semiconductors N.V.

- 10.3.2 Qualcomm Technologies

- 10.3.3 Tesla

- 10.3.4 Thales Group

- 10.3.5 Upstream Security

- 10.3.6 VicOne (Trend Micro)