|

시장보고서

상품코드

1833408

항공 사이버 보안 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Aviation Cybersecurity Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

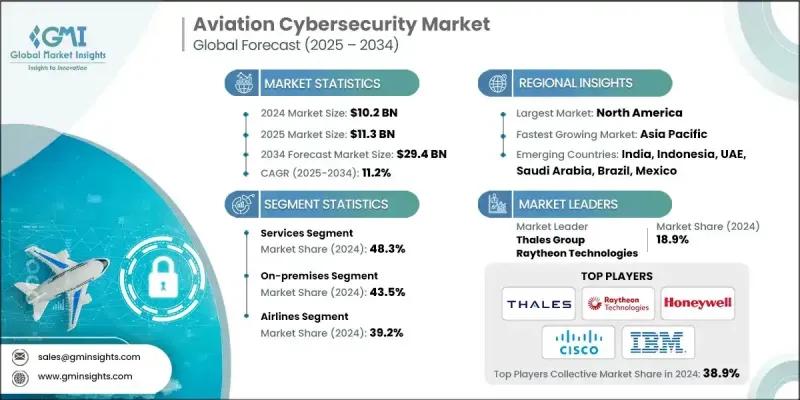

항공 사이버 보안 세계 시장 규모는 2024년에 102억 달러로 평가되었고, CAGR 11.2%로 성장하여 2034년에는 294억 달러에 이를 것으로 예측됩니다.

성장의 원동력은 시스템의 상호연결이 진행됨에 따라 증가하는 사이버 위협입니다. 규제 기관은 엄격한 보안 프로토콜을 요구하고 있으며, 항공기 시스템, 공항, 항공사의 업무는 커넥티드 기술에 대한 의존도가 높아져 새로운 취약점을 드러내고 있습니다. 랜섬웨어 및 악성코드 사고가 급격히 증가함에 따라 항공사는 데이터, 운영 및 승객의 안전을 보호하기 위해 첨단 사이버 보안 툴을 도입해야 합니다. 민간 항공과 항공 교통이 확대됨에 따라 복잡성이 증가하고 공격자의 침입 경로가 증가합니다. 국내 민간 항공 당국부터 국제기구에 이르기까지 규제 준수를 위해서는 암호화, 침입 감지, ID 관리, 지속적인 모니터링이 필요합니다. 서비스 제공업체와 솔루션 개발자는 급변하는 위협 환경 속에서 안전과 컴플라이언스 요구사항을 모두 충족시키기 위해 진화해야 합니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 102억 달러 |

| 예측 금액 | 294억 달러 |

| CAGR | 11.2% |

서비스 분야는 2024년 48.3%의 점유율을 차지할 것으로 예상되며, 위협이 복잡해짐에 따라 전문가 주도형 솔루션에 대한 요구가 증가하면서 우위를 점하고 있습니다. 항공사, 공항, 항공기 OEM, 항공 서비스 제공업체는 24시간 365일 위협 모니터링, 사고 대응, 컴플라이언스 감사, 위험 평가, 사이버 보안 교육 등 관리형 보안 서비스를 제공하는 제3자 공급업체에 대한 의존도가 높아지고 있습니다. 항공 업무의 데이터 통합과 상호연결이 가속화되고 있는 가운데, 이러한 서비스를 아웃소싱함으로써 기업은 고급 위협 인텔리전스에 접근하고, 내부 오버헤드를 줄이고, 빠르게 진화하는 세계 규제에 대응할 수 있습니다.

On-Premise 부문은 2024년 43.5%의 점유율을 차지할 것으로 예상되는데, 이는 많은 항공 관계자들이 보안 운영 및 중요 시스템을 직접 관리하는 것을 선호하기 때문입니다. 대규모 공항, 항공 항법 서비스 제공업체, 항공우주 OEM의 경우, 인프라를 사내에서 관리하면 엔드투엔드 가시성, 맞춤형 설정, 부서별 컴플라이언스 요구사항에 대한 탁월한 대응력을 확보할 수 있습니다. 이러한 사업체들은 종종 독점 시스템, 레거시 장비, 엄격한 기밀 유지 정책에 따라 보호되어야 하는 민감한 승객 데이터 및 국가 안보 데이터를 호스팅하는 경우가 많습니다.

미국 항공 사이버 보안 2024년 시장 규모는 35억 달러로, 1,000개가 넘는 민간 공항의 존재, 엄격한 사이버 보안 의무화, 커넥티드 항공기 기술 활용 확대에 힘입어 성장하고 있습니다. FAA, TSA, CISA 등 연방 규제 및 산업별 컴플라이언스 프레임워크는 통신 네트워크, 항공 교통 관리 시스템, 승객 정보 데이터베이스를 엄격하게 보호하도록 요구하고 있습니다.

항공 사이버 보안 시장의 주요 기업인 IBM Corporation, Honeywell International Inc. Systems, Thales Group, Leidos, Cisco Systems 등은 전 세계 항공 부문의 보안 아키텍처를 개발, 배포 및 유지하는 데 중요한 역할을 담당하고 있습니다. 항공 사이버 보안 시장의 기업들은 몇 가지 중요한 전략을 추구하고 있습니다. 사이버 공격에 선제적으로 대응하기 위해 AI를 활용한 위협 감지, 아나모리 마이닝, 예측 분석에 투자를 집중하고 있습니다. 규제 기관 및 항공 조직과 파트너십을 맺고 컴플라이언스 프레임워크를 솔루션에 통합하고 있습니다.

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역/국

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 커넥티드 항공기 시스템 도입 확대

- 항공 업계를 노린 사이버 위협 증가

- 엄격한 규제 준수 요건

- 상업 항공과 항공교통 성장

- 항공 업무 AI와 IoT 통합

- 업계의 잠재적 리스크&과제

- 사이버 보안 솔루션 고비용

- 항공 업계 숙련 한 사이버 보안 전문가 부족

- 시장 기회

- 신흥 시장 사이버 보안 서비스 확대

- AI를 활용한 사이버 보안 솔루션 개발

- 클라우드 기반 항공 사이버 보안 플랫폼 수요

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter의 Five Forces 분석

- PESTEL 분석

- 기술 및 혁신 상황

- 현재 기술 동향

- 신기술

- 새로운 비즈니스 모델

- 컴플라이언스 요건

- 국방 예산 분석

- 세계의 방위비 동향

- 지역 방위 예산배분

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 주요 방위 현대화 프로그램

- 예산 예측(2025-2034)

- 업계 성장에 대한 영향

- 국가별 방위 예산

- 공급망 회복탄력성

- 지정학적 분석

- 인재 분석

- 디지털 변혁

- 합병, 인수, 전략적 파트너십 상황

- 리스크 평가와 관리

- 주요 계약 체결(2021-2024)

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 주요 기업-경쟁 벤치마킹

- 재무 실적 비교

- 매출

- 이익률

- 연구개발

- 제품 포트폴리오 비교

- 제품 라인 업 넓이

- 테크놀러지

- 혁신

- 지역 존재감 비교

- 세계 발자국 분석

- 서비스 네트워크 범위

- 지역별 시장 침투율

- 경쟁 포지셔닝 매트릭스

- 리더들

- 과제자들

- 팔로워

- 니치 기업

- 전략적 전망 매트릭스

- 재무 실적 비교

- 주요 발전, 2021-2024

- 인수합병(M&A)

- 파트너십 및 협업

- 기술적 진보

- 확대와 투자 전략

- 디지털 변혁 대처

- 신규 기업/스타트업 기업 경쟁 구도

제5장 시장 추산·예측 : 솔루션별, 2021-2034

- 주요 동향

- 하드웨어

- 소프트웨어

- 서비스

제6장 시장 추산·예측 : 보안 유형별, 2021-2034

- 주요 동향

- 네트워크 보안

- 방화벽

- 침입 감지/방지 시스템(IDS/IPS)

- 가상사설망(VPN)

- 기타

- 용도과 클라우드 보안

- Web 및 모바일 애플리케이션 보안

- 클라우드 보안 플랫폼

- 안전한 소프트웨어 개발

- 기타

- 엔드포인트와 ID 보안

- 엔드포인트 감지와 응답(EDR/XDR)

- 멀웨어 대책/랜섬웨어 대책 툴

- 신원과 액세스 관리

- 기타

- 데이터 보안과 암호화

- 데이터 유출 방지(DLP)

- 데이터베이스 보안

- 암호화와 열쇠 관리

- 기타

- 기타

제7장 시장 추산·예측 : 전개 모드별, 2021-2034

- 주요 동향

- On-Premise

- 클라우드 기반

- 하이브리드

제8장 시장 추산·예측 : 최종 용도별, 2021-2034

- 주요 동향

- 항공사

- 공항 및 지상 오퍼레이터

- 항공 관제 당국

- 항공기 제조업체 및 OEM

- MRO 프로바이더

- 기타

제9장 시장 추산·예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트

제10장 기업 개요

- 세계의 주요 기업

- Airbus

- BAE Systems

- Honeywell International Inc.

- IBM Corporation

- Thales Group

- 지역별 주요 기업

- 북미

- Cisco Systems

- Lockheed Martin

- Northrop Grumman

- Raytheon Technologies

- Leidos

- Optiv Security

- Aviation SecOps

- 유럽

- Rohde &Schwarz

- SITA

- The Boeing Company

- Cyviation

- Darktrace

- 아시아태평양

- Wattlecorp Cybersecurity Labs LLP

- 북미

- 니치 기업-/디스럽터

- Darktrace

- Dionach

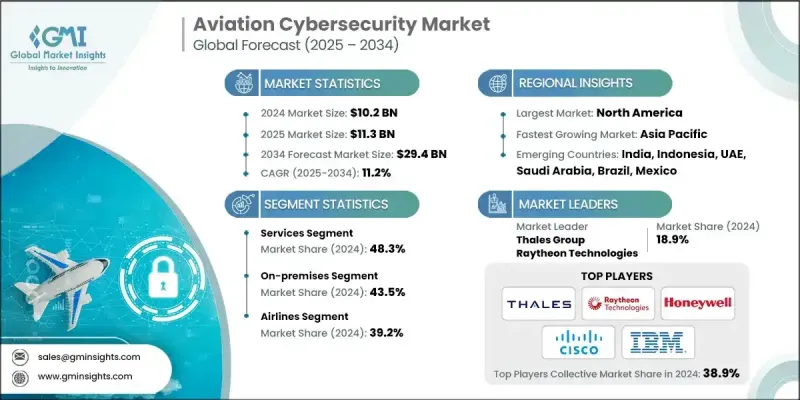

The Global Aviation Cybersecurity Market was valued at USD 10.2 billion in 2024 and is estimated to grow at a CAGR of 11.2% to reach USD 29.4 billion by 2034.

The growth is driven by the growing cyber threats as its systems become more interconnected. Regulatory bodies demand strict security protocols; aircraft systems, airports, and airline operations are increasingly relying on connected technologies that expose new vulnerabilities. Ransomware and malware incidents grow dramatically, pushing operators to adopt sophisticated cybersecurity tools to protect data, operations, and passenger safety. As commercial aviation and air traffic expand, complexity rises, creating more entry points for attackers. Regulatory compliance from domestic civil aviation authorities to international organizations requires encryption, intrusion detection, identity management, and continuous monitoring. Service providers and solution developers must evolve to meet both safety and compliance demands in a fast-changing threat landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.2 billion |

| Forecast Value | $29.4 billion |

| CAGR | 11.2% |

The services segment held a 48.3% share in 2024, dominating due to the rising need for expert-driven solutions amid the growing complexity of threats. Airlines, airports, aircraft OEMs, and aviation service providers increasingly rely on third-party vendors to handle managed security services, including 24/7 threat monitoring, incident response, compliance audits, risk assessments, and cybersecurity training. With aviation operations becoming more data-intensive and interconnected, outsourcing these services allows organizations to access advanced threat intelligence, reduce internal overhead, and stay aligned with rapidly evolving global regulations.

The on-premises segment held a 43.5% share in 2024 as many aviation players prefer to retain full control over security operations and critical systems. For large airports, air navigation service providers, and aerospace OEMs, managing infrastructure internally helps ensure end-to-end visibility, custom configuration, and better responsiveness to sector-specific compliance requirements. These entities often host proprietary systems, legacy equipment, and sensitive passenger or national security data that must be protected under strict confidentiality policies.

U.S. Aviation Cybersecurity Market was valued at USD 3.5 billion in 2024, underpinned by the presence of over a thousand commercial airports, stringent cybersecurity mandates, and the expanding use of connected aircraft technologies. Federal regulations and industry-specific compliance frameworks set by authorities such as the FAA, TSA, and CISA mandate rigorous protection of communication networks, air traffic management systems, and passenger information databases.

Major firms in the Aviation Cybersecurity Market, such as IBM Corporation, Honeywell International Inc., Airbus, Lockheed Martin, Northrop Grumman, Raytheon Technologies, BAE Systems, Thales Group, Leidos, and Cisco Systems, play significant roles in developing, deploying, and maintaining secure architecture across the aviation sector globally. Companies in the Aviation Cybersecurity Market are pursuing several key strategies. They emphasize investment in AI-powered threat detection, anomaly mining, and predictive analytics to stay ahead of cyberattacks. They forge partnerships with regulatory bodies and aviation organizations to ensure compliance frameworks are built into their solutions.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Solution trends

- 2.2.2 Security type trends

- 2.2.3 Deployment mode trends

- 2.2.4 End Use trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of connected aircraft systems

- 3.2.1.2 Rising cyber threats targeting aviation

- 3.2.1.3 Stringent regulatory compliance requirements

- 3.2.1.4 Growth in commercial aviation and air traffic

- 3.2.1.5 Integration of AI and IoT in aviation operations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of cybersecurity solutions

- 3.2.2.2 Lack of skilled cybersecurity professionals in aviation

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of cybersecurity services in emerging markets

- 3.2.3.2 Development of AI-driven cybersecurity solutions

- 3.2.3.3 Demand for cloud-based aviation cybersecurity platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Defense budget analysis

- 3.11 Global defense spending trends

- 3.12 Regional defense budget allocation

- 3.12.1 North America

- 3.12.2 Europe

- 3.12.3 Asia Pacific

- 3.12.4 Middle East and Africa

- 3.12.5 Latin America

- 3.13 Key defense modernization programs

- 3.14 Budget forecast (2025-2034)

- 3.14.1 Impact on Industry Growth

- 3.14.2 Defense Budgets by Country

- 3.15 Supply chain resilience

- 3.16 Geopolitical analysis

- 3.17 Workforce analysis

- 3.18 Digital transformation

- 3.19 Mergers, acquisitions, and strategic partnerships landscape

- 3.20 Risk assessment and management

- 3.21 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Solution, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates and Forecast, By Security Type, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Network security

- 6.2.1 Firewalls

- 6.2.2 Intrusion Detection/Prevention Systems (IDS/IPS)

- 6.2.3 Virtual Private Networks (VPNs)

- 6.2.4 Others

- 6.3 Application & cloud security

- 6.3.1 Web & mobile application security

- 6.3.2 Cloud security platforms

- 6.3.3 Secure software development

- 6.3.4 Others

- 6.4 Endpoint & identity security

- 6.4.1 Endpoint detection & response (EDR/XDR)

- 6.4.2 Anti-malware / Anti-ransomware Tools

- 6.4.3 Identity & access management

- 6.4.4 Others

- 6.5 Data Security & encryption

- 6.5.1 Data loss prevention (DLP)

- 6.5.2 Database security

- 6.5.3 Encryption & key management

- 6.5.4 Others

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Deployment Mode, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 On-premises

- 7.3 Cloud-based

- 7.4 Hybrid

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Airlines

- 8.3 Airports & ground operators

- 8.4 Air traffic control authorities

- 8.5 Aircraft manufacturers & OEMs

- 8.6 MRO providers

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Airbus

- 10.1.2 BAE Systems

- 10.1.3 Honeywell International Inc.

- 10.1.4 IBM Corporation

- 10.1.5 Thales Group

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 Cisco Systems

- 10.2.1.2 Lockheed Martin

- 10.2.1.3 Northrop Grumman

- 10.2.1.4 Raytheon Technologies

- 10.2.1.5 Leidos

- 10.2.1.6 Optiv Security

- 10.2.1.7 Aviation SecOps

- 10.2.2 Europe

- 10.2.2.1 Rohde & Schwarz

- 10.2.2.2 SITA

- 10.2.2.3 The Boeing Company

- 10.2.2.4 Cyviation

- 10.2.2.5 Darktrace

- 10.2.3 Asia Pacific

- 10.2.3.1 Wattlecorp Cybersecurity Labs LLP

- 10.2.1 North America

- 10.3 Niche Players / Disruptors

- 10.3.1 Darktrace

- 10.3.2 Dionach