|

시장보고서

상품코드

1833413

전투 드론 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Combat Drones Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

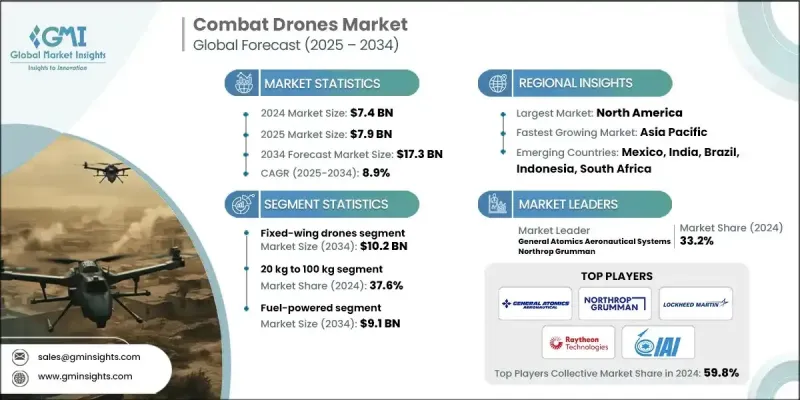

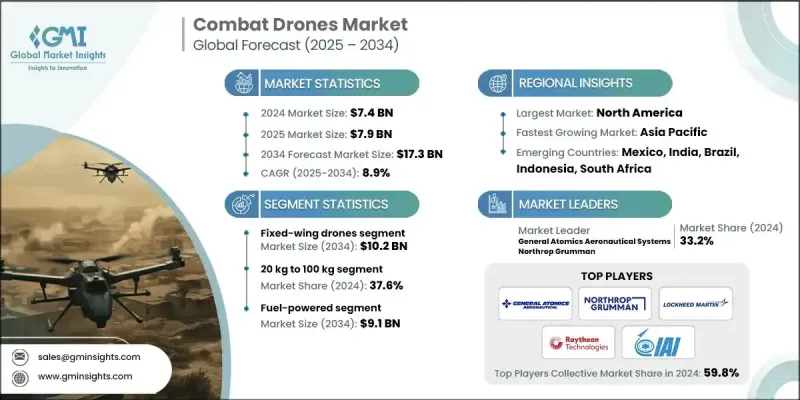

세계의 전투 드론 시장 규모는 2024년 74억 달러에 달했고, CAGR 8.9%를 나타내 2034년에는 173억 달러에 이를 것으로 추정됩니다.

이 급성장의 배경에는 군비의 현대화에 대한 노력, 국방비 증가, 인공지능(AI), 센서, 자율기술의 급속한 진보 등 몇 가지 요인이 있습니다. 신흥경제국가 국방의 근대화를 우선하는 가운데 무인전투항공시스템 개발에도 큰 자원이 할당되고 있습니다. 이러한 노력으로 각국은 선진적인 드론 기술의 혜택을 받으면서 군사대국과의 경쟁력을 유지할 수 있습니다. 스텔스 기술과 저관측 기술을 탑재한 전투 드론이 보급되고 있으며, 군사력이 고도의 방공 시스템에 의한 감지를 회피하면서, 위협이 높은 환경에서 활동할 수 있도록 되어 있습니다. 게다가 연계한 UAV가 보다 효과적으로 적의 방어망에 잠입하여 무력화할 수 있기 때문에 스웜 드론 전술의 이용이 점점 보급되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 74억 달러 |

| 예측 금액 | 173억 달러 |

| CAGR | 8.9% |

고정익 드론 분야는 2034년까지 102억 달러에 달할 것으로 전망됩니다. 고정 날개 드론는 긴 운영 범위, 향상된 페이로드 용량, 장거리 공격 및 모니터링 임무에 대한 적합성으로 인해 특히 선호됩니다. 이 부문의 채용은 북미와 아시아와 같은 지역에서 증가할 것으로 예상되며, 이곳에서는 이미 국경 순찰과 대규모 작전에 사용되고 있습니다. 제조업체는 경쟁력을 유지하기 위해 스텔스 기능을 강화하고 고급 정보, 모니터링 및 정찰(ISR) 페이로드를 통합하는 데 주력해야 합니다.

20kg에서 100kg의 무게 등급 부문은 2024년 37.6%의 점유율을 차지했습니다. 이 무게 범위 내의 드론는 이식성과 합리적인 가격으로 정찰 및 정밀 타격과 같은 전술적 임무에 사용됩니다. 이러한 시스템은 군의 현대화를 위한 비용 효율적인 솔루션을 추구하는 방어 예산이 제한된 국가에 매력적입니다. 개발 업체는 이러한 신흥 국가 시장을 위한 효과적이고 저렴한 컴팩트 한 인공지능 드론 생산에 주력해야합니다.

미국의 전투 드론 시장은 견실한 방어 예산, 드론의 광범위한 이용, 차세대 무인 전투기(UCAV)의 개발에 있어서의 지속적인 기술 혁신이 원동력이 되고, 2024년 시장 규모는 28억 달러가 되었습니다. 미국은 또한 드론의 군 기술과 AI 주도의 자율성에 있어서도 선두 주자입니다. 이 시장 진출기업들은 미국의 국방 근대화 이니셔티브와 보조를 맞추어 현재와 미래의 군사 전략 모두에 통합할 수 있는 확장 가능한 드론 시스템에 주력해야 합니다.

전투 드론 시장의 주요 기업으로는 Northrop Grumman, General Atomics Aeronautical Systems, Israel Aerospace Industries(IAI), Raytheon Technologies, Elbit Systems, Leonardo, Boeing, AeroVironment, Airbus 등의 기업이 포함됩니다. 이들 기업은 최첨단 드론 기술 개발의 최전선에 서서 군사 작전에서 드론 시스템 수요 증가에 대응하고 있습니다. 각 회사 시장 전략은 혁신적인 AI, 자율 및 스텔스 기능을 제품에 통합하는 데 중점을 둡니다. 각 회사는 또한 진화하는 방어 요구를 선점하기 위해 연구 개발에 많은 투자를 하고 있으며, 국가 방위의 우선순위에 맞추기 위해 정부 기관과의 전략적 파트너십을 키우고 있습니다.

목차

제1장 조사 방법

- 시장 범위 및 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 출처

- 세계

- 지역/국가

- 기준 추정치 및 계산

- 기준 연도 계산

- 시장 추정 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제 및 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 군사력의 근대화와 국방비 증가

- AI, 센서, 자율기술의 급속한 기술 진보

- 안보상의 정세와 지정학적 불안정성 증가

- 규제의 전환과 수출의 자유화

- 전략적 제휴와 공급망 확대

- 업계의 잠재적 위험 및 과제

- 높은 개발 및 조달비

- 엄격한 규제와 수출관리의 제한

- 시장 기회

- 인공지능과 머신러닝의 통합

- 군집 드론의 능력 확장

- 하이브리드 기술과 스텔스 기술의 채용 확대

- 신흥 방위 시장으로의 수출 가능성

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신 상황

- 현재의 기술 동향

- 신흥기술

- 새로운 비즈니스 모델

- 컴플라이언스 요건

- 국방예산 분석

- 세계의 방위비의 동향

- 지역 방위 예산 배분

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 주요 방위 근대화 프로그램

- 예산 예측(2025-2034년)

- 업계의 성장에 미치는 영향

- 국가별 방위 예산

- 공급망 회복탄력성

- 지정학적 분석

- 인재 분석

- 디지털 변혁

- 합병, 인수, 전략적 파트너십의 상황

- 위험 평가 및 관리

- 주요 계약 체결(2021-2024년)

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 주요 기업의 경쟁 벤치마킹

- 재무실적의 비교

- 수익

- 이익률

- 연구개발

- 제품 포트폴리오 비교

- 제품 라인업의 넓이

- 기술

- 혁신

- 지리적 입지 비교

- 글로벌 입지 분석

- 서비스 네트워크의 범위

- 지역별 시장 침투율

- 경쟁 포지셔닝 매트릭스

- 리더 기업

- 챌린저 기업

- 팔로워 기업

- 니치 플레이어

- 전략적 전망 매트릭스

- 재무실적의 비교

- 주요 발전(2021-2024년)

- 합병과 인수

- 파트너십 및 협업

- 기술적 진보

- 확대 및 투자 전략

- 디지털 변혁의 대처

- 신흥기업/스타트업 기업 경쟁 구도

제5장 시장 추계·예측 : 드론 유형별(2021-2034년)

- 주요 동향

- 고정익 드론

- 회전익 드론

- 단일 로터

- 다중 로터

- 하이브리드 드론

제6장 시장 추계·예측 : 탑재량별(2021-2034년)

- 주요 동향

- 최대 2kg

- 2kg-19kg

- 20kg-100kg

- 100kg 이상

제7장 시장 추계·예측 : 동력원별(2021-2034년)

- 주요 동향

- 배터리 구동

- 하이브리드 구동

- 연료 구동

제8장 시장 추계·예측 : 기술별(2021-2034년)

- 주요 동향

- 원격 조종 드론

- 반자율 드론

- 완전 자율 드론

제9장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 치명적 전투 드론

- 스텔스 드론

- 로이팅 무기 드론

- 표적 드론

- 기타

제10장 시장 추계·예측 : 발사 방식별(2021-2034년)

- 주요 동향

- 수직 이착륙(VTOL)

- 자동 이착륙(ATOL)

- 캐터필드 발사 드론

- 수동 발사 드론

제11장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 군사 작전

- 전략적 감시

- 전술적 전투

- 정찰 임무

- 훈련 및 시뮬레이션

- 전투 훈련

- 사격 훈련

- 국경 및 해양 안보

- 연안 감시

- 국경 순찰

- 대테러 및 법 집행

- 도시 감시

- 전술적 개입

제12장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제13장 기업 프로파일

- 세계 주요 기업

- Northrop Grumman Corporation

- Raytheon Technologies Corporation(RTX)

- Lockheed Martin Corporation

- 지역별 주요 기업

- 북미

- General Atomics Aeronautical Systems, Inc.

- AeroVironment, Inc.

- The Boeing Company(Insitu, Inc.)

- 유럽

- Airbus SE

- Leonardo SpA

- BAE Systems plc

- 아시아태평양

- Israel Aerospace Industries Ltd.(IAI)

- Turkish Aerospace Industries, Inc.(TAI)

- Safran SA

- 북미

- 니치 플레이어/디스럽터

- Elbit Systems Ltd.

- QinetiQ Group plc

- Kratos Defense &Security Solutions, Inc.

- Anduril Industries, Inc.

- Textron Inc.

- Thales Group

- Griffon Aerospace

- Sistemas de Control Remoto(SCR)

The Global Combat Drones Market was valued at USD 7.4 billion in 2024 and is estimated to grow at a CAGR of 8.9% to reach USD 17.3 billion by 2034.

This surge is driven by several factors, including modernization efforts in military forces, increased defense spending, and rapid advancements in artificial intelligence (AI), sensors, and autonomous technologies. As emerging economies prioritize defense modernization, significant resources are being allocated for the development of unmanned combat aerial systems. These efforts allow nations to stay competitive with major military powers while benefiting from advanced drone technologies. Combat drones equipped with stealth and low-observable technologies are gaining traction, enabling military forces to operate in high-threat environments while evading detection by sophisticated air defense systems. Additionally, the use of swarm drone tactics is becoming increasingly popular, as coordinated UAVs can infiltrate and neutralize enemy defenses more effectively.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.4 Billion |

| Forecast Value | $17.3 Billion |

| CAGR | 8.9% |

The fixed-wing drone segment is expected to reach USD 10.2 billion by 2034. Fixed-wing drones are particularly favored due to their longer operational range, enhanced payload capacity, and suitability for long-range strike and surveillance missions. The segment's adoption is expected to rise in regions like North America and Asia, where they are already used for border patrols and mass operations. Manufacturers must focus on enhancing stealth features and incorporating advanced intelligence, surveillance, and reconnaissance (ISR) payloads to remain competitive.

The 20 kg to 100 kg weight class segment held a 37.6% share in 2024. Drones within this weight range are increasingly used for tactical missions such as reconnaissance and precision strikes due to their portability and affordability. These systems are attractive to nations with limited defense budgets seeking cost-effective solutions for modernizing their armed forces. Manufacturers will need to focus on producing compact, AI-powered drones that are both effective and affordable for these developing markets.

United States Combat Drones Market generated USD 2.8 billion in 2024, driven by a robust defense budget, extensive use of drones, and ongoing innovation in the development of next-generation unmanned combat aerial vehicles (UCAVs). The U.S. also remains a leader in swarm technology and AI-driven autonomy in drones. Companies entering the market must align with U.S. defense modernization efforts, focusing on scalable drone systems that can integrate into both current and future military strategies.

Key players in the combat drones market include companies like Northrop Grumman, General Atomics Aeronautical Systems, Israel Aerospace Industries (IAI), Raytheon Technologies, Elbit Systems, Leonardo, Boeing, AeroVironment, and Airbus. These companies are at the forefront of developing cutting-edge drone technologies and meeting the growing demand for unmanned aerial systems in military operations. Their market strategies focus on incorporating innovative AI, autonomous capabilities, and stealth features into their products. Companies also invest heavily in R&D to stay ahead of evolving defense needs while fostering strategic partnerships with government agencies to align with national defense priorities.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Drone type trends

- 2.2.2 Payload capacity trends

- 2.2.3 Power source trends

- 2.2.4 Technology trends

- 2.2.5 Application trends

- 2.2.6 Launching mode trends

- 2.2.7 End use application trends

- 2.2.8 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Force modernization and rising defense spending

- 3.2.1.2 Rapid technological advancements in AI, sensors, and autonomy

- 3.2.1.3 Escalating security threat landscape and geopolitical instability

- 3.2.1.4 Regulatory shifts and export liberalization

- 3.2.1.5 Strategic alliances and supply-chain expansion

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and procurement costs

- 3.2.2.2 Stringent regulatory and export control restrictions

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of artificial intelligence and machine learning

- 3.2.3.2 Expansion of swarm drone capabilities

- 3.2.3.3 Growing adoption of hybrid and stealth technologies

- 3.2.3.4 Export potential to emerging defense markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Defense budget analysis

- 3.11 Global defense spending trends

- 3.12 Regional defense budget allocation

- 3.12.1 North America

- 3.12.2 Europe

- 3.12.3 Asia Pacific

- 3.12.4 Middle East and Africa

- 3.12.5 Latin America

- 3.13 Key defense modernization programs

- 3.14 Budget forecast (2025-2034)

- 3.14.1 Impact on industry growth

- 3.14.2 Defense budgets by country

- 3.15 Supply chain resilience

- 3.16 Geopolitical analysis

- 3.17 Workforce analysis

- 3.18 Digital transformation

- 3.19 Mergers, acquisitions, and strategic partnerships landscape

- 3.20 Risk assessment and management

- 3.21 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Drone Type, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Fixed-wing drones

- 5.3 Rotary-wing drones

- 5.3.1 Single-rotor

- 5.3.2 Multi-rotor

- 5.4 Hybrid drones

Chapter 6 Market Estimates and Forecast, By Payload Capacity, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Up to 2 kg

- 6.3 2 kg to 19 kg

- 6.4 20 kg to 100 kg

- 6.5 Above 100 kg

Chapter 7 Market Estimates and Forecast, By Power Source, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Battery-powered

- 7.3 Hybrid-powered

- 7.4 Fuel-powered

Chapter 8 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Remotely operated drones

- 8.3 Semi-autonomous drones

- 8.4 Fully autonomous drones

Chapter 9 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 Lethal combat drones

- 9.3 Stealth drones

- 9.4 Loitering munition drones

- 9.5 Target drones

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By Launching Mode, 2021 - 2034 (USD Million & Units)

- 10.1 Key trends

- 10.2 Vertical take-off and landing (VTOL)

- 10.3 Automatic take-off and landing (ATOL)

- 10.4 Catapult-launched drones

- 10.5 Hand-launched drones

Chapter 11 Market Estimates and Forecast, By End Use Application, 2021 - 2034 (USD Million & Units)

- 11.1 Key trends

- 11.2 Military operations

- 11.2.1 Strategic surveillance

- 11.2.2 Tactical combat

- 11.2.3 Reconnaissance missions

- 11.3 Training & simulation

- 11.3.1 Combat training

- 11.3.2 Target practice

- 11.4 Border & maritime security

- 11.4.1 Coastal surveillance

- 11.4.2 Border patrol

- 11.5 Counter-terrorism & law enforcement

- 11.5.1 Urban surveillance

- 11.5.2 Tactical interventions

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global Key Players

- 13.1.1 Northrop Grumman Corporation

- 13.1.2 Raytheon Technologies Corporation (RTX)

- 13.1.3 Lockheed Martin Corporation

- 13.2 Regional Key Players

- 13.2.1 North America

- 13.2.1.1 General Atomics Aeronautical Systems, Inc.

- 13.2.1.2 AeroVironment, Inc.

- 13.2.1.3 The Boeing Company (Insitu, Inc.)

- 13.2.2 Europe

- 13.2.2.1 Airbus SE

- 13.2.2.2 Leonardo S.p.A.

- 13.2.2.3 BAE Systems plc

- 13.2.3 APAC

- 13.2.3.1 Israel Aerospace Industries Ltd. (IAI)

- 13.2.3.2 Turkish Aerospace Industries, Inc. (TAI)

- 13.2.3.3 Safran SA

- 13.2.1 North America

- 13.3 Niche Players / Disruptors

- 13.3.1 Elbit Systems Ltd.

- 13.3.2 QinetiQ Group plc

- 13.3.3 Kratos Defense & Security Solutions, Inc.

- 13.3.4 Anduril Industries, Inc.

- 13.3.5 Textron Inc.

- 13.3.6 Thales Group

- 13.3.7 Griffon Aerospace

- 13.3.8 Sistemas de Control Remoto (SCR)