|

시장보고서

상품코드

1833453

브레이크 마찰 제품 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Brake Friction Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

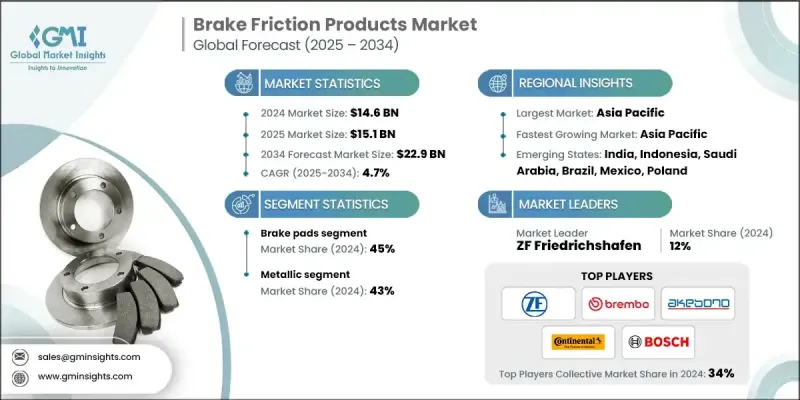

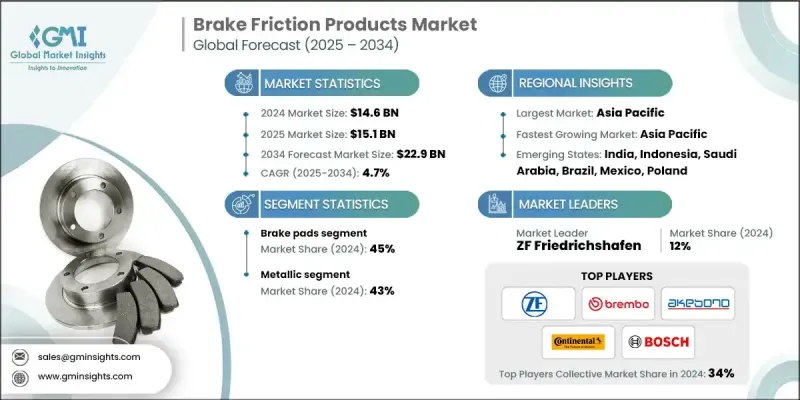

세계의 브레이크 마찰 제품 시장 규모는 2024년에 146억 달러로 평가되었고, CAGR 4.7%로 성장할 전망이며, 2034년에는 229억 달러에 이를 것으로 예측되고 있습니다.

세계 자동차 생산량의 꾸준한 증가는 브레이크 마찰 제품 시장의 주요 촉진요인입니다. 경제 국가가 발전하고 도시화함에 따라, 더 많은 소비자가 이동의 필요를 충족시키기 위해 승용차, 상용 트럭 및 이륜차를 구입하고 있습니다. 이러한 각 차량은 안전을 보장하기 위해 신뢰할 수 있는 브레이크 시스템에 크게 의존하고 있으며, 패드, 라이닝, 슈 등의 브레이크 마찰 제품은 모든 신차에 필수적인 부품이 되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 146억 달러 |

| 예측 금액 | 229억 달러 |

| CAGR | 4.7% |

브레이크 패드 수요 증가

브레이크 패드 분야는 승용차, 상용차, 이륜차에 필수적인 자동차의 안전과 성능에 견인되어 2024년에 큰 수익을 올렸습니다. 제조업체는 소비자 기대의 고조에 대응하기 위해 브레이크 패드의 내구성과 소음 저감 기능의 강화에 주력하고 있습니다. 게다가 세라믹 컴파운드나 세미 메탈릭 컴파운드와 같은 첨단 재료의 채용이 증가하고 있는 것도 이 부문의 성장을 뒷받침하고 있습니다. 지속적인 기술 혁신과 엄격한 안전 규제로 브레이크 패드 분야는 자동차 생산량 증가와 교환 수요에 견인되어 확대를 계속하고 있습니다.

금속 재료 채용 증가

내열성 및 내구성이 우수하기 때문에 2024년에는 금속 부문이 큰 점유율을 차지하고 있습니다. 이 부문은 엄격한 조건 하에서 견고한 브레이킹이 필요한 상용차 및 고성능 자동차에서 특히 선호됩니다. 그러나 업계는 금속 함량을 줄이는 환경 규제와 환경 친화적인 대체품 개발의 필요성과 같은 문제에 직면해 있습니다. 각사는 연구개발에 투자하여 성능과 지속가능성의 균형을 맞추는 저금속 마찰재와 하이브리드 마찰재를 혁신하여 이 분야가 경쟁력을 유지하고 진화하는 규격에 적합하도록 하고 있습니다.

아시아태평양이 추진력이 있는 지역이 될 전망입니다.

아시아태평양의 브레이크 마찰 제품 시장은 중국, 인도, 일본 등 국가에서 자동차 생산 증가와 도시화 확대로 2034년까지 급성장할 것으로 보입니다. 자동차 안전에 대한 소비자 의식 증가와 애프터마켓 분야 확대는 시장 확대를 더욱 뒷받침하고 있습니다. 주요 기업은 현지 제조 기지 설립, OEM과의 전략적 파트너십 구축, 지역 선호 및 규제 요구 사항에 맞는 비용 효율적인 고품질 마찰 제품에 대한 주력을 통해 이 지역의 발판을 강화하고 있습니다.

브레이크 마찰 제품 시장의 주요 기업는 Delphi Technologies, Federal-Mogul, Brembo, Akebono Brake Industry Co., Advics Co., Robert Bosch, Continental, ZF Friedrichshafen, Nisshinbo Holdings, Aisin Seiki Co 입니다.

브레이크 마찰 제품 시장에서 사업을 전개하는 기업은 시장의 지위를 강화하기 위해 기술 혁신, 전략적 파트너십, 지역 확대를 조합하여 전개하고 있습니다. 연구 개발에 중점을 둔 투자를 통해 제조업체는 제품 성능을 향상시키면서 엄격한 환경 및 안전 규정을 충족하는 고급 마찰 제품을 개발하고 있습니다. 주문자 상표 부착 생산 제조업체(OEM)와의 제휴는 장기 공급 계약 확보에 도움이 되며 안정적인 수익원을 확보하고 있습니다.

목차

제1장 조사 방법

- 시장의 범위 및 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역 및 국가

- 기본 추정과 계산

- 기준 연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제 및 한계

제2장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 엄격한 안전규제

- 신흥 시장에서 자동차 생산의 성장

- 구리 프리 및 환경 친화적인 소재로의 이행

- 아시아태평양에서의 이륜차 및 플릿 소유 증가

- 업계의 잠재적 위험 및 과제

- 원재료 가격 변동

- 저비용 비조직화 기업과의 경쟁

- 시장 기회

- 차량의 전동화

- 애프터마켓의 디지털화 및 전자상거래

- 선진 시장에서 프리미엄화의 경향

- 전략적 제휴 및 M&A

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 세계

- ISO 26867:2009 시험 규격의 구현

- 환경규제

- 성능 테스트 및 검증 프로토콜

- 품질 보증 및 제조 기준

- 지역

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 세계

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 전기자동차 혁명의 영향 평가

- Brake-by-wire 시스템 개발 및 도입

- 자율주행차의 브레이크 요건

- 제조기술 혁신

- 신흥 기술

- 스마트 머티리얼 및 적응 성능

- AI 및 예지보전의 통합

- 지속 가능한 재료의 혁신 및 개발

- 현재의 기술 동향

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출과 수입

- 비용 내역 분석

- 특허 분석

- 지속가능성 및 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경 친화적인 노력

- 탄소발자국의 고려

- 브레이크 먼지 배출 분석 및 환경에 미치는 영향

- 환경 규제 준수 프레임워크

- 기업의 지속가능성 및 ESG 실적

- 브레이크 성능 분석 및 테스트 인텔리전스

- 현실 세계의 정지 거리 데이터베이스

- 열성능 및 페이드 분석

- 마찰계수의 일관성 분석

- 소음, 진동, 하슈네스(NVH) 인텔리전스

- 브레이크 노이즈의 분석과 경감

- 진동과 저더 성능

- 엄격함 및 편안함의 지표

- 건강과 환경에 미치는 영향에 관한 정보

- 브레이크 더스트 배출량의 정량화

- 노동 안전 보건 분석

- 환경 수명주기 평가

제3장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획 및 자금 조달

- 제조 및 공급망 분석

- 세계의 제조 거점 및 생산 능력의 분석

- 원재료 공급망 및 리스크 평가

- 제조 비용 분석 및 최적화

- 공급망의 탄력성 및 리스크 관리

- 품질 관리 및 성능 검증 프레임워크

- 통계적 공정 제어(SPC) 분석

- 성능 테스트 및 검증 프로토콜

- 고장 모드 영향 해석(FMEA)

제4장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 브레이크 패드

- 브레이크 슈

- 브레이크 라이닝

- 브레이크 드럼

- 브레이크 로터 및 디스크

- 기타

제5장 시장 추계 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 메탈릭

- 세라믹

- 복합

- 기타

제6장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 세단

- SUV

- 해치백

- 상용차

- 소형 상용차(LCV)

- 대형 상용차(HCV)

- 중형 상용차(MCV)

- 이륜차

- 오프로드 차량

제7장 시장 추계 및 예측 : 판매 채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Global companies

- Aisin Seiki Co.

- Akebono Brake Industry Co.

- Brembo

- Continental

- Federal-Mogul

- Miba Friction Group

- Robert Bosch

- Tenneco

- TMD Friction Holdings

- ZF Friedrichshafen

- Regional companies

- Advics Co.

- ATE

- Delphi Technologies

- EBC Brakes

- Ferodo

- Jurid

- MAT Holdings

- Nisshinbo Holdings

- NRS Brakes

- Sangsin Brake

- Wagner Brake

- 신흥 기업

- AI-Powered Brake Analytics Startups

- Drivezy

- Brake Parts

- Fras-le

- Galfer Bike

- Hardron Friction Material

- SGL Carbon SE-Brake Disc Division

- Xinyi Brake Pad Co.

The Global Brake Friction Products Market was valued at USD 14.6 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 22.9 billion by 2034.

The steady rise in global vehicle production is a primary driver in the brake friction products market. As economies develop and urbanize, more consumers are purchasing passenger cars, commercial trucks, and two-wheelers to meet their transportation needs. Each of these vehicles depends heavily on reliable braking systems to ensure safety, making brake friction components like pads, linings, and shoes essential parts in every new vehicle.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.6 Billion |

| Forecast Value | $22.9 Billion |

| CAGR | 4.7% |

Increasing Demand for Brake Pads

The brake pads segment generated substantial revenues in 2024, driven by vehicle safety and performance that makes them indispensable across passenger cars, commercial vehicles, and two-wheelers. Manufacturers are focusing on enhancing the durability and noise reduction capabilities of brake pads to meet rising consumer expectations. Furthermore, the increasing adoption of advanced materials such as ceramic and semi-metallic compounds is fueling growth within this segment. With ongoing innovations and stringent safety regulations, the brake pads segment continues to expand, driven by rising vehicle production and replacement demand.

Rising Adoption of Metallic Material

The metallic segment held a significant share in 2024 owing to its superior heat resistance and durability. This segment is particularly favored in commercial vehicles and high-performance automobiles that require robust braking under demanding conditions. However, industry faces challenges such as environmental regulations pushing for reduced metal content and the need to develop eco-friendlier alternatives. Companies are investing in R&D to innovate low-metallic or hybrid friction materials that balance performance with sustainability, ensuring this segment remains competitive and compliant with evolving standards.

Asia Pacific to Emerge as a Propelling Region

Asia Pacific brake friction products market will witness rapid growth through 2034, driven by escalating vehicle production and expanding urbanization across countries like China, India, and Japan. Increasing consumer awareness regarding vehicle safety and the growing aftermarket segment are further propelling market expansion. Key players are strengthening their foothold in this region by establishing local manufacturing units, forming strategic partnerships with OEMs, and focusing on cost-effective, high-quality friction materials tailored to regional preferences and regulatory requirements.

Major players in the brake friction products market are Delphi Technologies, Federal-Mogul, Brembo, Akebono Brake Industry Co., Advics Co., Robert Bosch, Continental, ZF Friedrichshafen, Nisshinbo Holdings, Aisin Seiki Co.

Companies operating in the brake friction products market are deploying a combination of innovation, strategic partnerships, and regional expansion to bolster their market position. Heavy investments in R&D allow manufacturers to develop advanced friction materials that meet stringent environmental and safety regulations while enhancing product performance. Collaborations with original equipment manufacturers (OEMs) help secure long-term supply contracts, ensuring steady revenue streams.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Industry Insights

- 2.1 Industry ecosystem analysis

- 2.1.1 Supplier landscape

- 2.1.2 Profit margin

- 2.1.3 Cost structure

- 2.1.4 Value addition at each stage

- 2.1.5 Factor affecting the value chain

- 2.1.6 Disruptions

- 2.2 Industry impact forces

- 2.2.1 Growth drivers

- 2.2.1.1 Stringent safety regulations

- 2.2.1.2 Vehicle production growth in emerging markets

- 2.2.1.3 Shift toward copper-free & eco-friendly materials

- 2.2.1.4 Rising two-wheeler and fleet ownership in APAC

- 2.2.2 Industry pitfalls and challenges

- 2.2.2.1 Raw material price volatility

- 2.2.2.2 Competition from low-cost unorganized players

- 2.2.3 Market opportunities

- 2.2.3.1 Electrification of vehicles

- 2.2.3.2 Aftermarket digitization & e-commerce

- 2.2.3.3 Premiumization trend in developed markets

- 2.2.3.4 Strategic collaborations & M&A

- 2.2.1 Growth drivers

- 2.3 Growth potential analysis

- 2.4 Regulatory landscape

- 2.4.1 Global

- 2.4.1.1 ISO 26867:2009 Testing Standards Implementation

- 2.4.1.2 Environmental Regulations

- 2.4.1.3 Performance Testing and Validation Protocols

- 2.4.1.4 Quality Assurance and Manufacturing Standards

- 2.4.2 Regional

- 2.4.2.1 North America

- 2.4.2.2 Europe

- 2.4.2.3 Asia Pacific

- 2.4.2.4 Latin America

- 2.4.2.5 Middle East & Africa

- 2.4.1 Global

- 2.5 Porter’s analysis

- 2.6 PESTEL analysis

- 2.7 Technology and innovation landscape

- 2.7.1 Current technological trends

- 2.7.1.1 Electric vehicle revolution impact assessment

- 2.7.1.2 Brake-by-wire systems development and adoption

- 2.7.1.3 Autonomous vehicle braking requirements

- 2.7.1.4 Manufacturing technology innovation

- 2.7.2 Emerging technologies

- 2.7.2.1 Smart materials and adaptive performance

- 2.7.2.2 AI and predictive maintenance integration

- 2.7.2.3 Sustainable material innovation and development

- 2.7.1 Current technological trends

- 2.8 Price trends

- 2.8.1 By region

- 2.8.2 By product

- 2.9 Production statistics

- 2.9.1 Production hubs

- 2.9.2 Consumption hubs

- 2.9.3 Export and import

- 2.10 Cost breakdown analysis

- 2.11 Patent analysis

- 2.12 Sustainability and environmental aspects

- 2.12.1 Sustainable practices

- 2.12.2 Waste reduction strategies

- 2.12.3 Energy efficiency in production

- 2.12.4 Eco-friendly initiatives

- 2.12.5 Carbon footprint considerations

- 2.12.6 Brake dust emission analysis and environmental impact

- 2.12.7 Environmental regulation compliance framework

- 2.12.8 Corporate sustainability and ESG performance

- 2.13 Brake performance analytics and testing intelligence

- 2.13.1 Real-world stopping distance database

- 2.13.2 Thermal performance and fade analysis

- 2.13.3 Friction coefficient consistency analytics

- 2.14 Noise, vibration, and harshness (NVH) intelligence

- 2.14.1 Brake noise analysis and mitigation

- 2.14.2 Vibration and judder performance

- 2.14.3 Harshness and comfort metrics

- 2.15 Health and environmental impact intelligence

- 2.15.1 Brake dust emission quantification

- 2.15.2 Occupational health and safety analysis

- 2.15.3 Environmental lifecycle assessment

Chapter 3 Competitive Landscape, 2024

- 3.1 Introduction

- 3.2 Company market share analysis

- 3.2.1 North America

- 3.2.2 Europe

- 3.2.3 Asia Pacific

- 3.2.4 LATAM

- 3.2.5 MEA

- 3.3 Competitive analysis of major market players

- 3.4 Competitive positioning matrix

- 3.5 Strategic outlook matrix

- 3.6 Key developments

- 3.6.1 Mergers & acquisitions

- 3.6.2 Partnerships & collaborations

- 3.6.3 New product launches

- 3.6.4 Expansion plans and funding

- 3.7 Manufacturing and supply chain analysis

- 3.7.1 Global manufacturing footprint and capacity analysis

- 3.7.2 Raw material supply chain and risk assessment

- 3.7.3 Manufacturing cost analysis and optimization

- 3.7.4 Supply chain resilience and risk management

- 3.8 Quality control and performance validation framework

- 3.8.1 Statistical process control (SPC) analytics

- 3.8.2 Performance testing and validation protocols

- 3.8.3 Failure mode and effects analysis (FMEA)

Chapter 4 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn, Units)

- 4.1 Key trends

- 4.2 Brake pads

- 4.3 Brake shoes

- 4.4 Brake linings

- 4.5 Brake drums

- 4.6 Brake rotors/discs

- 4.7 Others

Chapter 5 Market Estimates & Forecast, By Material, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Metallic

- 5.3 Ceramic

- 5.4 Composite

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedan

- 6.2.2 SUVs

- 6.2.3 Hatchback

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCVs)

- 6.3.2 Heavy commercial vehicles (HCVs)

- 6.3.3 Medium commercial vehicles (MCVs)

- 6.4 Two-wheelers

- 6.5 Off-highway vehicles

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Original equipment manufacturer (OEM)

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Nordics

- 8.3.7 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global companies

- 9.1.1 Aisin Seiki Co.

- 9.1.2 Akebono Brake Industry Co.

- 9.1.3 Brembo

- 9.1.4 Continental

- 9.1.5 Federal-Mogul

- 9.1.6 Miba Friction Group

- 9.1.7 Robert Bosch

- 9.1.8 Tenneco

- 9.1.9 TMD Friction Holdings

- 9.1.10 ZF Friedrichshafen

- 9.2 Regional companies

- 9.2.1 Advics Co.

- 9.2.2 ATE

- 9.2.3 Delphi Technologies

- 9.2.4 EBC Brakes

- 9.2.5 Ferodo

- 9.2.6 Jurid

- 9.2.7 MAT Holdings

- 9.2.8 Nisshinbo Holdings

- 9.2.9 NRS Brakes

- 9.2.10 Sangsin Brake

- 9.2.11 Wagner Brake

- 9.3 Emerging players

- 9.3.1 AI-Powered Brake Analytics Startups

- 9.3.2 Drivezy

- 9.3.3 Brake Parts

- 9.3.4 Fras-le

- 9.3.5 Galfer Bike

- 9.3.6 Hardron Friction Material

- 9.3.7 SGL Carbon SE - Brake Disc Division

- 9.3.8 Xinyi Brake Pad Co.