|

시장보고서

상품코드

1833619

수소 파이프라인 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2035년)Hydrogen Pipeline Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2035 |

||||||

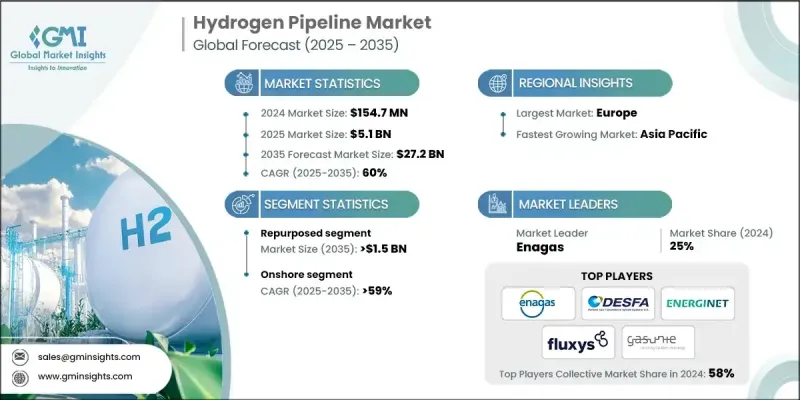

세계의 수소 파이프라인 시장은 2024년에는 1억 5,470만 달러로 평가되었고, 2025년 51억 달러에서 2035년에는 272억 달러까지 성장할 전망이며, CAGR 60%로 성장할 것으로 예측됩니다.

세계의 정부와 산업계가 인터넷 제로 방출의 목표를 내걸고 있으며, 특히 철강, 화학, 중수송 등 배출 감축이 곤란한 분야를 중심으로 중요한 탈탄소화 수단으로서 클린 수소에 대한 대규모 투자를 추진하고 있습니다. 이러한 이유로 파이프라인을 포함한 신뢰할 수 있는 수소 수송 인프라에 대한 수요가 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2035년 |

| 시장 규모 | 1억 5,470만 달러 |

| 예측 금액 | 272억 달러 |

| CAGR | 60% |

재사용 분야 수요 증가

사업자가 인프라 배치를 가속화하기 위해 비용 효율적인 솔루션을 요구하고 있기 때문에 재사용 분야가 2024년에 큰 점유율을 차지했습니다. 처음부터 새로운 파이프라인을 건설하는 대신 기존 천연가스 파이프라인을 수소 운송용으로 전환함으로써 자본 지출을 줄이고 개발 기간을 단축하는 접근 방식을 취하고 있습니다. 이 방법은 레거시 가스 네트워크가 개발되는 지역에서 특히 매력적이며 현재 화석 기반 시스템과 미래의 녹색 에너지 분배 사이의 실용적인 교량이 될 것입니다.

온쇼어 수요 증가

온쇼어 부문은 오프쇼어 인프라에 비해 물류면에서 유리하며 설치 비용이 낮고 규제 당국의 승인이 용이하기 때문에 2024년에 큰 수익을 올렸습니다. 온쇼어 파이프라인은 전해 플랜트와 같은 생산 기지와 산업 사용자, 수소 공급 스테이션, 수출 터미널을 연결하는 데 필수적입니다. 이 분야는 산업 지역을 가로지르는 지역의 수소 허브와 회랑을 가능하게 하기 위해 특히 중요합니다.

유리한 지역으로 상승하는 유럽

유럽 수소 파이프라인 시장은 야심찬 기후 목표, 협력적인 인프라 계획, EU 수소 전략을 통한 강력한 규제 지원에 힘입어 2024년에 큰 점유율을 차지했습니다. 독일, 네덜란드, 스페인 등 주요 국가들은 국경을 넘어 생산과 소비의 거점을 연결하는 국경을 넘는 파이프라인 네트워크에 많은 투자를 하고 있습니다. 또한, 이업종간의 협력, 정부로부터의 자금 지원, 유럽 수소 백본 등의 구상하에 가스 네트워크의 재이용도 성장에 기여하고 있습니다.

수소 파이프라인 시장의 주요 기업은 Denys, Terega, ENERGINET, Siemens Energy, GRTgaz, REN, Fluxys, Bonatti, Tekfen, The ROSEN Group, Spiecapag, Corinth Pipeworks, TENARIS, DESFA, Snam, ONTRAS Gastransport, Enagas, Gasunie, EUROPIPE, GAZ-SYSTEM입니다.

진화하는 수소 파이프라인 시장에서의 지위를 강화하기 위해 각 회사는 기술 혁신, 전략적 파트너십 및 법규제 조정을 결합하여 추구하고 있습니다. 수소 안전 문제를 해결하고 향후 기준을 충족하기 위해 많은 기업들이 첨단 파이프라인 재료 및 모니터링 시스템에 투자하고 있습니다. 신재생에너지 개발 기업 및 산업용 수소 유저와의 협력으로 수직 통합형 밸류체인이 실현되어 수요가 보장되고 있습니다. 게다가 기업은 정책 입안자와 적극적으로 참여하여 규제 체계를 형성하여 보다 부드러운 프로젝트 승인과 자금 조달 자격을 확보하고 있습니다. 특히 유럽과 아시아의 지리적 다양화도 중요한 전략으로, 고성장 시장 진입 및 지역 간 프로젝트 리스크의 균형을 가능하게 합니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 에코시스템

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 비용 구조 분석

- 잠재적인 파이프라인 프로젝트

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 지역별 기업의 시장 점유율

- 북미

- 유럽

- 아시아태평양

- 전략적 대시보드

- 전략적 노력

- 기업 벤치마킹

- 혁신 및 기술의 상황

제5장 시장 규모 및 예측 : 유형별(2021-2035년)

- 주요 동향

- 온쇼어

- 오프쇼어

제6장 시장 규모 및 예측 : 분류별(2021-2035년)

- 주요 동향

- 신규

- 재사용

제7장 시장 규모 및 예측 : 지역별(2021-2035년)

- 주요 동향

- 북미

- 유럽

- 아시아태평양

- 세계 기타 지역

제8장 기업 프로파일

- Bonatti

- Corinth Pipeworks

- DESFA

- Denys

- Enagas SA

- Energinet

- EUROPIPE

- Fluxys

- Gasunie

- GAZ-SYSTEM

- GRTgaz

- ONTRAS Gastransport GmbH

- REN

- Siemens Energy

- Spiecapag

- Snam

- Tekfen

- Tenaris

- Terega

- The ROSEN Group

The global hydrogen pipeline market was estimated at USD 154.7 million in 2024 and is expected to grow from USD 5.1 billion in 2025 to USD 27.2 billion by 2035, at a CAGR of 60%.

Governments and industries worldwide are committing to net-zero emissions targets, driving massive investments in clean hydrogen as a key decarbonization tool-especially for hard-to-abate sectors like steel, chemicals, and heavy transport. This fuels demand for reliable hydrogen transport infrastructure, including pipelines.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2035 |

| Start Value | $154.7 Million |

| Forecast Value | $27.2 Billion |

| CAGR | 60% |

Rising Demand for the Repurposed Sector

The repurposed segment held a significant share in 2024, as operators look for cost-effective solutions to accelerate infrastructure deployment. Instead of building new lines from scratch, companies are converting existing natural gas pipelines to carry hydrogen an approach that reduces capital expenditure and shortens development timelines. This method is particularly appealing in regions with extensive legacy gas networks, offering a practical bridge between current fossil-based systems and future green energy distribution.

Increasing Demand for Onshore

The onshore segment generated significant revenues in 2024, owing to its logistical advantages, lower installation costs, and easier regulatory approvals compared to offshore infrastructure. Onshore pipelines are essential for connecting production sites, such as electrolysis plants, with industrial users, hydrogen refueling stations, and export terminals. This segment is especially critical for enabling regional hydrogen hubs and corridors across industrial zones.

Europe to Emerge as a Lucrative Region

Europe hydrogen pipeline market held a sizeable share in 2024, fueled by ambitious climate goals, coordinated infrastructure plans, and strong regulatory support through the EU Hydrogen Strategy. Major countries like Germany, the Netherlands, and Spain are investing heavily in transnational pipeline networks to connect production and consumption hubs across borders. The growth is also benefiting from cross-industry collaborations, government funding, and repurposing gas networks under initiatives like the European Hydrogen Backbone.

Major players in the hydrogen pipeline market are Denys, Terega, ENERGINET, Siemens Energy, GRTgaz, REN, Fluxys, Bonatti, Tekfen, The ROSEN Group, Spiecapag, Corinth Pipeworks, TENARIS, DESFA, Snam, ONTRAS Gastransport, Enagas, Gasunie, EUROPIPE, and GAZ-SYSTEM.

To strengthen their position in the evolving hydrogen pipeline market, companies are pursuing a combination of technological innovation, strategic partnerships, and regulatory alignment. Many are investing in advanced pipeline materials and monitoring systems to address hydrogen's safety challenges and meet future standards. Collaborations with renewable energy developers and industrial hydrogen users are enabling vertically integrated value chains and guaranteed demand. In addition, firms are actively engaging with policymakers to shape regulatory frameworks, ensuring smoother project approvals and eligibility for funding. Geographic diversification, particularly in Europe and Asia, is another key strategy, allowing companies to tap into high-growth markets and balance project risk across regions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.1.3 Base estimates and calculations

- 1.1.4 Base year calculation

- 1.1.5 Key trends for market estimates

- 1.2 Forecast model

- 1.3 Primary research & validation

- 1.3.1 Primary sources

- 1.4 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2035

- 2.2 Business trends

- 2.3 Type trends

- 2.4 Classification trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Cost structure analysis

- 3.5 Potential Pipeline Projects

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitutes

- 3.8 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Type, 2021 - 2035 (USD Million, Km)

- 5.1 Key trends

- 5.2 Onshore

- 5.3 Offshore

Chapter 6 Market Size and Forecast, By Classification, 2021 - 2035 (USD Million, Km)

- 6.1 Key trends

- 6.2 New

- 6.3 Repurposed

Chapter 7 Market Size and Forecast, By Region, 2021 - 2035 (USD Million, Km)

- 7.1 Key trends

- 7.2 North America

- 7.3 Europe

- 7.4 Asia Pacific

- 7.5 Rest of World

Chapter 8 Company Profiles

- 8.1 Bonatti

- 8.2 Corinth Pipeworks

- 8.3 DESFA

- 8.4 Denys

- 8.5 Enagas S.A.

- 8.6 Energinet

- 8.7 EUROPIPE

- 8.8 Fluxys

- 8.9 Gasunie

- 8.10 GAZ-SYSTEM

- 8.11 GRTgaz

- 8.12 ONTRAS Gastransport GmbH

- 8.13 REN

- 8.14 Siemens Energy

- 8.15 Spiecapag

- 8.16 Snam

- 8.17 Tekfen

- 8.18 Tenaris

- 8.19 Terega

- 8.20 The ROSEN Group