|

시장보고서

상품코드

1833625

노천 채굴 장비 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Surface Mining Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

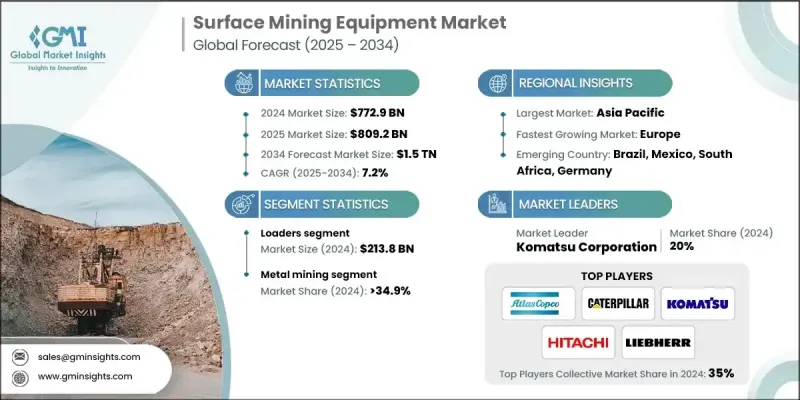

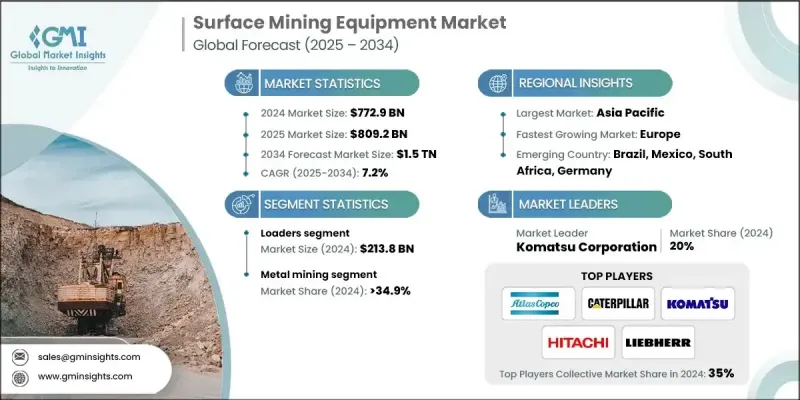

세계의 노천 채굴 장비 시장은 2024년에는 7,729억 달러로 평가되었고, CAGR 7.2%로 성장할 전망이며, 2034년에는 1조 5,000억 달러에 이를 것으로 추정됩니다.

성장의 원동력이 되는 것은 건설, 일렉트로닉스, 자동차를 포함한 주요 최종 이용 산업에서 광물 및 금속 수요 증가입니다. 이러한 분야는 원재료에 크게 의존하기 때문에 광업 사업은 생산량을 높이고 운영 신뢰성을 높이며 공정을 간소화하기 위해 기술적으로 고급 장비에 대한 투자가 증가하고 있습니다. 기업은 효율성을 높이고 인적 위험을 줄이며, 가동 중지 시간을 최소화하기 위해 자동화 및 디지털 플랫폼을 채굴 작업에 빠르게 통합하고 있습니다. 실시간 모니터링 시스템과 AI 기반 분석을 갖춘 지능형 기계는 운영자가 생산성과 자원 배분을 관리하는 방식을 변화시키고 있습니다. 중앙 집중식 제어 시스템을 통해 정보를 기반으로 의사 결정을 내리는 능력은 채굴 작업을 가속화하고 안전하고 비용 효율성을 향상시킵니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 7,729억 달러 |

| 예측 금액 | 1조 5,000억 달러 |

| CAGR | 7.2% |

이 시장에서는 지속 가능하고 환경 친화적인 관행으로의 전환도 볼 수 있습니다. 엄격한 규제가 마련된 가운데 제조업체는 배출 가스를 줄이기 위해 하이브리드 및 전기 구동 광산 기계를 도입하고 있습니다. 보다 깨끗한 엔진 기술, 바이오연료에 대한 대응, 에너지 절약 설계가 표준이되고 있습니다. 또한 절수 시스템 및 방진 솔루션도 도입되어 운영이 환경 벤치마크를 충족하는 데 도움이 됩니다. LiDAR 및 레이더 기반 충돌 방지를 포함한 고급 안전 시스템은 현장의 안전성을 높이고 원격 조작 기계는 운영자가 현장 이외의 장소에서 안전하게 작업할 수 있게 하여 현장의 위험을 낮추고 있습니다.

2024년에는 로더 부문이 2,138억 달러를 창출하여 노천 채굴 활동에 중요한 역할을 유지했습니다. 운반, 적재, 비축 등의 작업을 처리하는 범용성이 있기 때문에 모든 규모의 채광 작업에 필수적입니다. 연비 효율의 향상과 다양한 지형에 대응하는 견고한 성능은 특히 기업이 가혹한 조건 하에서 성능을 발휘하는 신뢰성이 높은 기기를 요구하는 가운데 그 인기를 견인하고 있습니다.

금속 광업 분야는 철, 알루미늄, 구리, 금 등의 금속 수요 증가에 힘입어 2024년 34.9%의 점유율을 획득했습니다. 전자, 건축, 운송과 같은 분야의 소비 증가는 채광 프로젝트의 확대를 촉진하고 있습니다. 노천 채굴은 높은 채굴 능력과 비용 우위성으로 인해 여전히 선호되는 방법이며 기업이 경비를 관리하면서 사업을 확대하는 데 도움이 됩니다.

미국의 노천 채굴 장비 시장은 2024년에 76%의 점유율을 차지하며, 지역 성장에 크게 기여했습니다. 첨단 기술의 급속한 도입과 디지털 도구 및 자동화에 대한 의존도가 높아짐에 따라 미국의 채굴 작업은 더욱 효율적이고 안전합니다. 지원 법률, 세제 우대 조치, 상품 가격 상승이 시설 업그레이드 및 신규 구매를 뒷받침합니다. 지속가능성을 중시하는 정부의 정책과 기술 혁신의 장려책도 환경친화적인 최신 기기 수요를 뒷받침하고 있습니다.

세계의 노천 채굴 장비 시장을 형성하는 주요 기업은 BHP Billiton, Metso, Barrick Gold, Komatsu, Liebherr, Rio Tinto, Anglo American, Hitachi Construction Machinery, Freeport-McMoRan, Sandvik, Atlas Copco, J.C. Bamford Excavators, Vale, Boart Longyear, Caterpillar, 및 Volvo 등이 있습니다. 시장 경쟁력을 강화하기 위해 대기업은 기술 혁신, 전략적 파트너십 및 지속가능성을 선호합니다. 많은 기업들이 세계 배출 목표를 충족시키기 위해 전기 및 하이브리드 기계로 제품 라인을 확대하고 있습니다. 자동화, AI 통합 및 디지털 모니터링 도구에 대한 투자를 통해 각 회사는 효율성과 예지 보전 기능을 강화한 지능형 장비를 제공할 수 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 산업계에서의 금속 수요 증가

- 신흥 국가에서의 도시화 진전

- 유리한 정부 규제

- 업계의 잠재적 위험 및 과제

- 높은 초기 비용

- 보다 엄격한 환경 규제

- 기회

- 자동화와 스마트 제조의 도입

- 신흥 시장으로 확대

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 제품 유형별

- 규제 상황

- 표준 및 컴플라이언스 요건

- 지역 규제 틀

- 인증기준

- 무역 통계

- 주요 수입국

- 주요 수출국

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 로더

- 굴삭기

- 파쇄, 분쇄, 체 분리 장치

- 드릴 및 브레이커

- 댐퍼

- 삽

- 모터 그레이더

- 기타

제6장 시장 추계 및 예측 : 방법별(2021-2034년)

- 주요 동향

- 스트립 채굴

- 점점 밭 채굴

- 노천 채굴

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 석탄 채굴

- 금속 채굴

- 광물 채굴

- 기타(보크사이트 채굴)

제8장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접 판매

- 간접 판매

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

제10장 기업 프로파일

- Anglo American

- Atlas Copco

- Barrick Gold

- BHP Billiton

- Boart Longyear

- Caterpillar

- Freeport-McMoRan

- Hitachi Construction Machinery

- JC Bamford Excavators

- Komatsu

- Liebherr

- Metso

- Rio Tinto

- Sandvik

- Vale

- Volvo

The Global Surface Mining Equipment Market was valued at USD 772.9 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 1.5 trillion by 2034.

The growth is fueled by rising demand for minerals and metals across major end-use industries, including construction, electronics, and automotive. As these sectors rely heavily on raw materials, mining operations are increasingly investing in technologically advanced equipment to boost output, improve operational reliability, and streamline processes. Companies are rapidly integrating automation and digital platforms into their mining operations to enhance efficiency, reduce human risk, and minimize downtime. Intelligent machinery equipped with real-time monitoring systems and AI-based analytics is transforming how operators manage productivity and resource allocation. The ability to make informed decisions through centralized control systems is making mining operations faster, safer, and more cost-effective.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $772.9 Billion |

| Forecast Value | $1.5 Trillion |

| CAGR | 7.2% |

The market is also seeing a shift toward sustainable and eco-conscious practices. With strict regulations in place, manufacturers are introducing hybrid and electric-powered mining machinery to reduce emissions. Cleaner engine technologies, biofuel compatibility, and energy-saving designs are becoming standard. Additionally, water conservation systems and dust control solutions are being implemented to help operations meet environmental benchmarks. Advanced safety systems, including LiDAR- and radar-based collision prevention, are enhancing site safety while remote-controlled machines allow operators to work safely from off-site locations, lowering on-site risk.

In 2024, the loaders segment generated USD 213.8 billion, maintaining a vital role in surface mining activities. Their versatility in handling tasks such as transporting, loading, and stockpiling makes them indispensable for mining operations of all scales. Enhanced fuel efficiency and rugged performance across varied terrains continue to drive their popularity, especially as companies seek reliable equipment that performs under harsh conditions.

The metal mining segment captured a 34.9% share in 2024, supported by heightened demand for metals like iron, aluminum, copper, and gold. Increased consumption from sectors like electronics, building, and transportation is driving expansion in mining projects. Surface mining remains a preferred method due to its higher extraction capacity and cost advantages, which are helping companies scale operations while managing expenses.

United States Surface Mining Equipment Market held a 76% share in 2024, contributing significantly to regional growth. With the rapid adoption of advanced technologies and increasing reliance on digital tools and automation, mining operations in the U.S. are becoming more efficient and safer. Supportive legislation, tax benefits, and higher commodity prices are encouraging upgrades and new equipment purchases. Sustainability-focused government policies and innovation incentives are also helping fuel demand for modern, environmentally friendly equipment.

Key companies shaping the Global Surface Mining Equipment Market include BHP Billiton, Metso, Barrick Gold, Komatsu, Liebherr, Rio Tinto, Anglo American, Hitachi Construction Machinery, Freeport-McMoRan, Sandvik, Atlas Copco, J.C. Bamford Excavators, Vale, Boart Longyear, Caterpillar, and Volvo. To reinforce their competitive position in the surface mining equipment market, leading players are prioritizing innovation, strategic partnerships, and sustainability. Many are expanding their product lines with electric and hybrid machinery to align with global emission targets. Investment in automation, AI integration, and digital monitoring tools is enabling companies to offer intelligent equipment with enhanced efficiency and predictive maintenance capabilities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type trends

- 2.2.3 Method trends

- 2.2.4 Application trends

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for metals in industries

- 3.2.1.2 Increasing urbanization in developing countries

- 3.2.1.3 Favorable government regulations

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial cost

- 3.2.2.2 Stricter environmental regulations

- 3.2.3 Opportunities

- 3.2.3.1 Adoption of automation and smart manufacturing

- 3.2.3.2 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Loaders

- 5.3 Excavators

- 5.4 Crushing, pulverizing and screen equipment

- 5.5 Drills & breakers

- 5.6 Dumper

- 5.7 Shovels

- 5.8 Motor graders

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Method, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Strip mining

- 6.3 Terrace mining

- 6.4 Open-pit mining

Chapter 7 Market Estimates and Forecast, By Application 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Coal mining

- 7.3 Metal mining

- 7.4 Mineral mining

- 7.5 Other (bauxite mining)

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Anglo American

- 10.2 Atlas Copco

- 10.3 Barrick Gold

- 10.4 BHP Billiton

- 10.5 Boart Longyear

- 10.6 Caterpillar

- 10.7 Freeport-McMoRan

- 10.8 Hitachi Construction Machinery

- 10.9 J.C. Bamford Excavators

- 10.10 Komatsu

- 10.11 Liebherr

- 10.12 Metso

- 10.13 Rio Tinto

- 10.14 Sandvik

- 10.15 Vale

- 10.16 Volvo