|

시장보고서

상품코드

1833635

자동차용 전기 진공 펌프 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Automotive Electric Vacuum Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

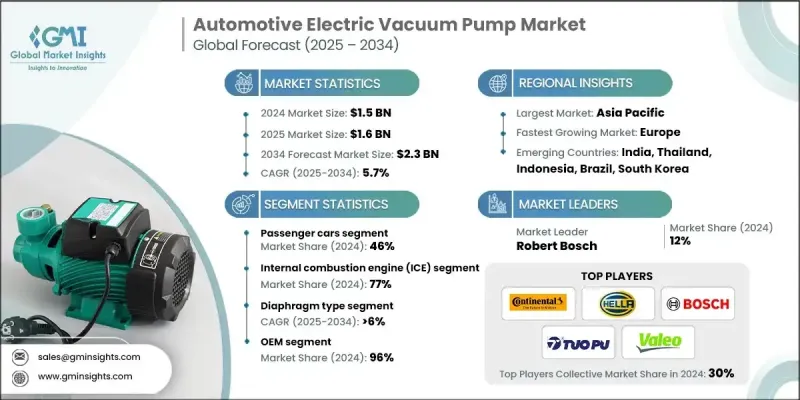

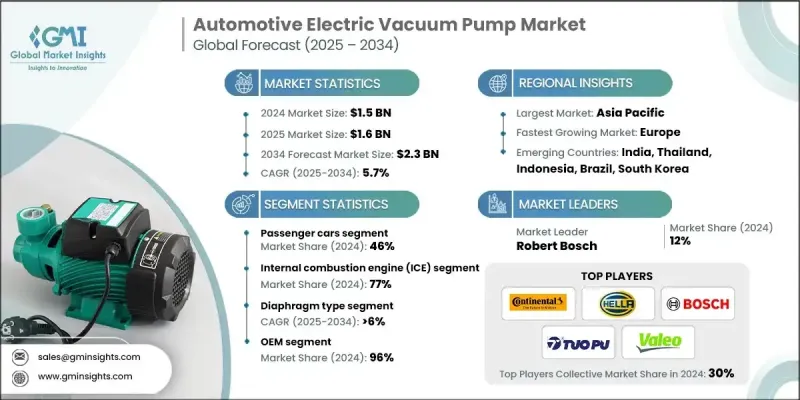

세계의 자동차용 전기 진공 펌프 시장 규모는 2024년에 15억 달러로 평가되었고, CAGR 5.7%로 성장할 전망이며, 2034년에는 23억 달러에 이를 것으로 예측되고 있습니다.

이 시장은 자동차 제조업체가 차량 효율을 높이고 진화하는 배기 가스 규정을 준수하며 파워트레인의 전기화를 지원하는 데 중요한 역할을 합니다. OEM은 특히 엔진 기반 진공원이 없는 하이브리드 자동차 및 전기자동차에서 중요한 차량 시스템에 일관된 독립적인 진공원을 제공하기 때문에 EVP에 대한 의존도를 높이고 있습니다. 환경 친화적인 이동성으로의 전환과 에너지 효율성 및 안전성을 양립시킨 차량에 대한 소비자의 선호도는 최신 차량으로의 EVP 통합을 가속화하고 있습니다. 이산화탄소 배출량 감소에 중점을 둔 정부의 엄격한 규제가 수요를 더욱 촉진하고 있습니다. 제조업체가 지속가능성 목표와 비즈니스 효율성을 달성하기 위해 노력하는 동안 EVP는 회생 브레이크, 스타트 스톱 시스템 및 ECU 구동 차량 역학과 같은 고급 기능을 지원하도록 설계되었습니다. 팬데믹 후 자동차 산업의 회복과 함께 신뢰성이 높고 배출 가스를 줄이는 기술에 대한 요구는 세계 주요 자동차 시장에서 전기 진공 펌프의 혁신과 채택을 모두 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 15억 달러 |

| 예측 금액 | 23억 달러 |

| CAGR | 5.7% |

승용차 부문이 46%의 점유율을 차지했으며, 2025-2034년 CAGR은 7%로 성장이 예측됩니다. 승용차는 SUV, 해치백, 콤팩트 자동차 등 다양한 차량 카테고리에 광범위하게 배치되어 EVP의 주요 용도 분야로 계속되고 있습니다. 이러한 펌프는 안정적인 브레이크 성능을 보장하고 차량 전체의 안전성을 향상시키며, 특히 전기자동차 및 하이브리드 차량에서는 기존의 엔진 진공 소스가 없는 경우의 진공 요구를 지원합니다. 자동차 제조업체가 EVP를 선호하고 사용하는 것은 임베디드가 간단하고 비용 효율적이기 때문에 대규모 재설계 없이 차량 효율을 향상시키는 실용적인 솔루션입니다.

2024년 내연기관(ICE) 부문의 점유율은 77%로, 2034년까지 CAGR 4.5%로 성장할 것으로 보입니다. 전동화가 기세를 늘리고 있다고는 해도, 내연 기관차는 특히 신흥 경제국에서 계속해서 세계의 차량을 지배하고 있습니다. 배출가스와 연비규제가 세계적으로 강화되고 있는 가운데 내연기관차 제조업체는 엔진에 대한 의존도를 낮추고 운전 효율을 향상시키기 위해 EVP 도입을 가속화하고 있습니다. 이러한 시스템은 유휴 시, 발진 및 정지 사이클, 정체 시의 브레이크 및 부스터 기능과 보조기 시스템의 성능을 높이는 데 있어서 중요한 역할을 하고 있습니다.

아시아태평양 시장의 자동차용 전기 진공 펌프 2024년 점유율은 54%로, 이는 자동차의 전동화가 가속되고 있으며, 중국, 일본, 한국 등 주요 국가에서 배기가스 규제가 점점 엄격해지고 있는 것이 요인입니다. 이 지역에서는 EV와 하이브리드의 도입이 급속히 진행되고 있으며, 자동차 제조업체는 현재 및 향후 규제 기준에 맞는 에너지 효율적인 부품을 통합해야 한다고 촉구되고 있습니다. 그 결과 EVP는 최신 자동차 아키텍처의 중요한 부분이 되었습니다. 아시아태평양의 견조한 자동차 생산 능력, 유리한 정책 틀, 전동 이동성 혁신에 대한 투자 증가로 아시아태평양은 자동차 기술 진보의 거점으로 자리매김하고 있습니다.

세계의 자동차용 전기 진공 펌프 시장을 형성하는 주요 기업으로는 Valeo, Youngshin Precision, Continental, Aisin, Tuopu, Robert Bosch, ZF Friedrichshafen, Rheinmetall Automotive, Magna International, Hella 등이 있습니다. 자동차용 전기 진공 펌프 시장의 주요 기업은 ICE, 하이브리드, 전기 등 모든 파워트레인에 대응하는 경량, 콤팩트, 에너지 효율적인 EVP 시스템의 개발에 주력하고 있습니다. 모터 효율, 펌프 하우징 재료 및 전자 제어 장치의 혁신은 제품 차별화의 핵심입니다. 많은 제조업체들은 수요 증가에 대응하고 공급망에 대한 의존도를 줄이기 위해 고성장 지역에서 생산 능력을 확대하고 있습니다.

목차

제1장 조사 방법

- 시장의 범위 및 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역 및 국가

- 기본 추정 및 계산

- 기준 연도 계산

- 시장 예측의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제 및 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 엄격한 배출가스 규제 및 연비 규제

- 하이브리드 자동차 및 전기자동차의 보급 증가

- 전기 모터 및 센서의 기술적 진보

- 안전성 및 효율성의 향상을 요구하는 소비자 수요

- 전동화 및 그린 모빌리티에 대한 정부의 인센티브

- 업계의 잠재적 위험 및 과제

- 극한 조건 하에서의 신뢰성

- 차량 시스템과의 통합 복잡성

- 시장 기회

- 하이브리드 및 전동 파워트레인과의 통합

- 전기 모터 및 펌프 기술의 발전

- 고급 브레이크 및 안전 시스템과의 통합

- 규제 준수 및 배출 감축에 대한 관심 증가

- 성장 가능성 분석

- 규제 상황

- 세계 안전 기준 및 시험 요건

- 지역의 규제 틀 및 승인 프로세스

- 환경 규제 및 배출 가스 규제

- 품질경영시스템 및 ISO 규격

- 자동차 업계 규격(IATF 16949, ISO/TS)

- 기능안전요건(ISO 26262)

- 전자기 양립성(EMC) 규격

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 차세대 전동 모터 기술

- 스마트팜프 통합 및 IoT 연결

- 예측 유지 보수 및 상태 모니터링

- 에너지 효율 최적화 및 전력 관리

- 신흥 기술

- 소음 저감 및 음향 공학

- 소형화 및 경량화 기술

- ADAS(선진 운전 지원 시스템)와의 통합

- 인공지능 및 머신러닝 애플리케이션

- 무선 통신 및 원격 진단

- 지속 가능한 소재 및 순환형 경제 디자인

- 현재의 기술 동향

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출 및 수입

- 비용 내역 분석

- 특허 분석

- 지속가능성 및 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적인 노력

- 탄소발자국의 고려

- 리스크 평가 및 시장 정보

- 공급망의 리스크 분석 및 경감 전략

- 기술의 진부화 및 혁신의 위험

- 규제 준수 리스크 및 관리

- 시장 수요의 변동 및 시나리오 계획

- 경쟁 위협 및 전략적 대응 계획

- 경제 및 통화 위험 평가

- 지정학적 리스크 및 무역 정책의 영향

- 환경 및 지속가능성의 위험

- 미래 시장 전망 및 전략적 기회

- 전기자동차 시장 성장의 영향과 기회

- 자율주행차의 통합 요건

- 신흥 시장 진출 및 현지화 전략

- 기술의 융합 및 업계 횡단적인 용도

- 지속가능성의 동향 및 그린테크놀로지의 채용

- 투자 기회 및 시장 진출 전략

- 파트너십 및 협업 기회

- 장기적인 시장의 진화 및 파괴의 시나리오

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획 및 자금 조달

제5장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 경상용차

- 중형 상용차

- 대형 상용차

제6장 시장 추계 및 예측 : 추진력별(2021-2034년)

- 주요 동향

- 내연기관(ICE)

- 전기자동차(EV)

- 배터리 전기자동차(BEV)

- 플러그인 하이브리드 전기자동차(PHEV)

- 하이브리드 전기자동차(HEV)

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 브레이크 시스템

- 배출가스 제어 시스템

- HVAC 및 기후 제어 시스템

- 엔진 관리 시스템

- 기타

제8장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 스윙 피스톤

- 횡격막

- 잎

제9장 시장 추계 및 예측 : 판매 채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 포르투갈

- 크로아티아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 싱가포르

- 태국

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 세계 기업

- Aptiv

- BorgWarner

- Continental

- DENSO

- Magna International

- Mahle

- Rheinmetall Automotive

- Robert Bosch

- Schaeffler

- Valeo

- ZF Friedrichshafen

- 지역 기업

- Aisin

- Faurecia(Forvia)

- Hella

- Hitachi Astemo

- Hyundai Mobis

- Marelli

- Nexteer Automotive

- Pierburg

- Plastic Omnium

- Tenneco

- Tuopu

- Youngshin Precision

- 신흥 기업

- Aeromotive

- Classic Performance

- NAVAC

- Pfeiffer Vacuum Technology

- Thomas Magnete

The Global Automotive Electric Vacuum Pump Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 2.3 billion by 2034.

This market plays a critical role in enabling automotive manufacturers to enhance vehicle efficiency, comply with evolving emission norms, and support powertrain electrification. OEMs are increasingly relying on EVPs to provide a consistent and independent vacuum source for essential vehicle systems, particularly in hybrid and electric vehicles where engine-based vacuum sources are absent. The shift toward eco-friendly mobility and consumer preference for vehicles that are both energy-efficient and safe is accelerating the integration of EVPs into modern vehicles. Stringent government regulations focused on lowering carbon footprints have further fueled demand. As manufacturers strive to meet sustainability targets and operational efficiency, EVPs are being engineered to support advanced features such as regenerative braking, start-stop systems, and ECU-driven vehicle dynamics. With the automotive industry rebounding post-pandemic, the need for reliable, emission-reducing technologies is driving both innovation and adoption of electric vacuum pumps across all major automotive markets worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.3 Billion |

| CAGR | 5.7% |

The passenger car segment held a 46% share and is projected to grow at a CAGR of 7% from 2025 to 2034. Passenger cars continue to serve as the primary application area for EVPs due to their wide deployment in various vehicle categories, including SUVs, hatchbacks, and compact cars. These pumps ensure consistent braking performance, improve overall vehicle safety, and support vacuum needs in the absence of traditional engine vacuum sources, especially in electric and hybrid variants. Automakers prefer EVPs for their easy integration and cost-effectiveness, making them a practical solution for enhancing vehicle efficiency without extensive redesigns.

The internal combustion engine (ICE) segment held a 77% share in 2024 and is set to grow at a CAGR of 4.5% through 2034. Even as electrification gains momentum, ICE-powered vehicles continue to dominate global fleets, particularly in emerging economies. With stricter emissions and fuel efficiency mandates coming into effect globally, ICE vehicle manufacturers are increasingly implementing EVPs to reduce engine dependency and improve operational efficiency. These systems play a key role in enhancing brake booster functionality and auxiliary system performance during idle phases, start-stop cycles, and traffic congestion.

Asia Pacific Automotive Electric Vacuum Pump Market held 54% share in 2024, driven by the accelerating electrification of vehicles and increasingly stringent emissions regulations in major economies such as China, Japan, and South Korea. With EV and hybrid adoption growing rapidly across this region, automakers are under pressure to integrate energy-efficient components that comply with current and upcoming regulatory benchmarks. As a result, EVPs have become a critical part of modern vehicle architecture. The region's robust automotive production capacity, favorable policy frameworks, and increasing investments in electric mobility innovation have positioned Asia Pacific as a stronghold for automotive technology advancement.

Key players shaping the Global Automotive Electric Vacuum Pump Market include Valeo, Youngshin Precision, Continental, Aisin, Tuopu, Robert Bosch, ZF Friedrichshafen, Rheinmetall Automotive, Magna International, and Hella. Leading companies in the automotive electric vacuum pump market are focusing on developing lightweight, compact, and energy-efficient EVP systems compatible with all powertrain types such as ICE, hybrid, and electric. Innovation in motor efficiency, pump housing materials, and electronic control units is central to product differentiation. Many manufacturers are expanding production capabilities in high-growth regions to meet increasing demand and reduce supply chain dependencies.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicles

- 2.2.3 Propulsion

- 2.2.4 Application

- 2.2.5 Type

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Stringent emission and fuel economy regulations

- 3.2.1.3 Rising adoption of hybrid and electric vehicles

- 3.2.1.4 Technological advancements in electric motors and sensors

- 3.2.1.5 Consumer demand for enhanced safety and efficiency

- 3.2.1.6 Government incentives for electrification and green mobility

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Reliability under extreme conditions

- 3.2.2.2 Integration complexity with vehicle systems

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with hybrid and electric powertrains

- 3.2.3.2 Advancements in electric motor and pump technology

- 3.2.3.3 Integration with advanced braking and safety systems

- 3.2.3.4 Growing focus on regulatory compliance and emission reduction

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Global safety standards & testing requirements

- 3.4.2 Regional regulatory frameworks & approval processes

- 3.4.3 Environmental regulations & emission compliance

- 3.4.4 Quality management systems & ISO standards

- 3.4.5 Automotive industry standards (IATF 16949, ISO/TS)

- 3.4.6 Functional safety requirements (ISO 26262)

- 3.4.7 Electromagnetic compatibility (EMC) standards

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Next-generation electric motor technologies

- 3.7.1.2 Smart pump integration & IoT connectivity

- 3.7.1.3 Predictive maintenance & condition monitoring

- 3.7.1.4 Energy efficiency optimization & power management

- 3.7.2 Emerging technologies

- 3.7.2.1 Noise reduction & acoustic engineering

- 3.7.2.2 Miniaturization & weight reduction technologies

- 3.7.2.3 Integration with advanced driver assistance systems

- 3.7.2.4 Artificial intelligence & machine learning applications

- 3.7.2.5 Wireless communication & remote diagnostics

- 3.7.2.6 Sustainable materials & circular economy design

- 3.7.1 Current technological trends

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Risk assessment & market intelligence

- 3.13.1 Supply chain risk analysis & mitigation strategies

- 3.13.2 Technology obsolescence & innovation risks

- 3.13.3 Regulatory compliance risks & management

- 3.13.4 Market demand volatility & scenario planning

- 3.13.5 Competitive threats & strategic response planning

- 3.13.6 Economic & currency risk assessment

- 3.13.7 Geopolitical risks & trade policy impact

- 3.13.8 Environmental & sustainability Risks

- 3.14 Future market outlook & strategic opportunities

- 3.14.1 Electric vehicle market growth impact & opportunities

- 3.14.2 Autonomous vehicle integration requirements

- 3.14.3 Emerging market expansion & localization strategies

- 3.14.4 Technology convergence & cross-industry applications

- 3.14.5 Sustainability trends & green technology adoption

- 3.14.6 Investment opportunities & market entry strategies

- 3.14.7 Partnership & collaboration opportunities

- 3.14.8 Long-term market evolution & disruption scenarios

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Hatchbacks

- 5.2.2 Sedans

- 5.2.3 SUVs

- 5.3 Commercial vehicles

- 5.3.1 Light commercial vehicle

- 5.3.2 Medium commercial vehicle

- 5.3.3 Heavy commercial vehicle

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Internal combustion engine (ICE)

- 6.3 Electric vehicles (EVs)

- 6.3.1 Battery electric vehicles (BEVs)

- 6.3.2 Plug-in hybrid electric vehicles (PHEVs)

- 6.3.3 Hybrid electric vehicles (HEVs)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Braking systems

- 7.3 Emission control systems

- 7.4 HVAC & climate control systems

- 7.5 Engine management systems

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Type, 2021 - 2034 (USD Mn, Units)

- 8.1 Key trends

- 8.2 Swing piston

- 8.3 Diaphragm

- 8.4 Leaf

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 (USD Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Portugal

- 10.3.9 Croatia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Aptiv

- 11.1.2 BorgWarner

- 11.1.3 Continental

- 11.1.4 DENSO

- 11.1.5 Magna International

- 11.1.6 Mahle

- 11.1.7 Rheinmetall Automotive

- 11.1.8 Robert Bosch

- 11.1.9 Schaeffler

- 11.1.10 Valeo

- 11.1.11 ZF Friedrichshafen

- 11.2 Regional Players

- 11.2.1 Aisin

- 11.2.2 Faurecia (Forvia)

- 11.2.3 Hella

- 11.2.4 Hitachi Astemo

- 11.2.5 Hyundai Mobis

- 11.2.6 Marelli

- 11.2.7 Nexteer Automotive

- 11.2.8 Pierburg

- 11.2.9 Plastic Omnium

- 11.2.10 Tenneco

- 11.2.11 Tuopu

- 11.2.12 Youngshin Precision

- 11.3 Emerging Players

- 11.3.1 Aeromotive

- 11.3.2 Classic Performance

- 11.3.3 NAVAC

- 11.3.4 Pfeiffer Vacuum Technology

- 11.3.5 Thomas Magnete