|

시장보고서

상품코드

1833636

출생 전 및 신생아 유전자 검사 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Prenatal and Newborn Genetic Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

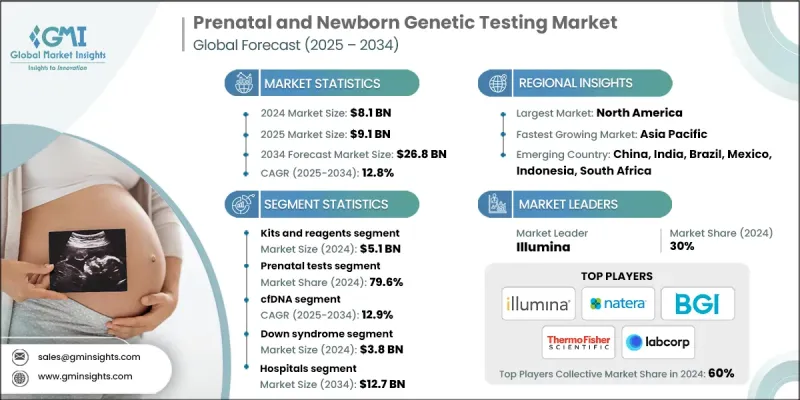

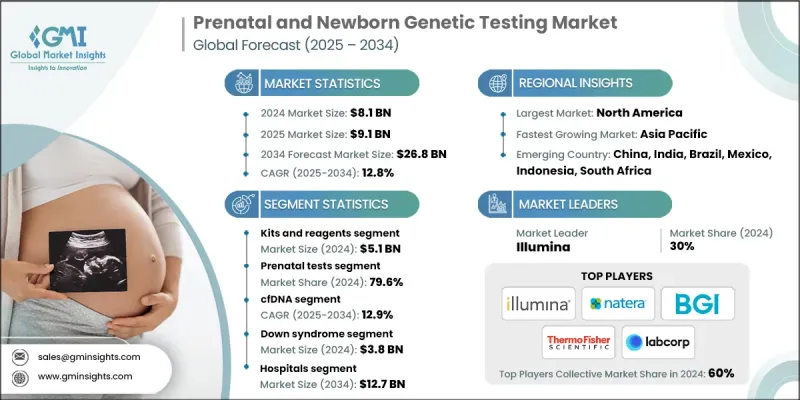

세계의 출생 전 및 신생아 유전자 검사 시장 규모는 2024년에 81억 달러로 평가되었고, CAGR 12.8%로 성장할 전망이며, 2034년에는 91억 달러에 이를 것으로 예측되고 있습니다.

다운증, 낭포성 섬유증, 척수성 근위축증 등 유전성 질환의 유병률 증가가 출생 전 및 신생아 유전자 검사에 의한 조기 발견 수요를 촉진하고 있습니다. 임신 중 부모는 안심감과 조기 개입의 선택을 점점 요구하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 81억 달러 |

| 예측 금액 | 91억 달러 |

| CAGR | 12.8% |

키트 및 시약 부문 채택 증가

키트 및 시약 부문은 2024년에 큰 점유율을 차지했습니다. 이러한 소모품은 임상 진단과 연구 워크플로우 모두에 필수적이기 때문입니다. 실험실 및 진단센터는 정확하고 재현성있는 결과를 얻기 위해 고품질의 신뢰할 수 있는 시약에 의존합니다. 조기 유전학적 스크리닝 수요 증가로 검사량이 증가하는 가운데 소모품의 반복적인 사용은 계속해서 이 분야의 실적을 끌어올립니다.

출생 전 검사 부문 수요 증가

임산부 연령의 상승, 위험 의식 증가, 비침습적 및 침습적 검사 옵션의 강력한 임상 채용에 의해 출생 전 검사 부문은 2024년에 큰 점유율을 차지했습니다. 이러한 검사는 염색체 이상, 유전자 변이, 태아 이상을 임신 초기에 검출하는 데 도움이 되고, 보다 많은 정보에 기초한 임상적 의사결정을 가능하게 합니다. 임신 초기 스크리닝으로의 이동과 확장 유전자 패널의 탑재가 이 분야의 지속적인 성장에 박차를 가하고 있습니다.

주목받는 cfDNA

무세포 DNA(cfDNA) 검사 분야는 Trisomy 21, 18, 13과 같은 일반적인 염색체 질환을 스크리닝하는 비침습적이고 고정밀 방법으로 2024년에 지속적인 점유율을 유지했습니다. 이 방법은 모체의 혈액을 순환하는 태아의 DNA 단편을 분석하므로 양수 천자와 같은 침습적 치료의 필요성을 줄일 수 있습니다.

북미가 추진력이 있는 지역이 될 전망

북미의 출생 전 및 신생아 유전자 검사 시장은 강력한 헬스케어 인프라, 첨단 실험실 기능, 유전학적 서비스에 대한 광범위한 접근에 견인되어 2024년에는 큰 점유율로 성장할 전망입니다. 미국과 캐나다에서는 조기 스크리닝이 널리 채택되고 있으며, 유리한 보험 적용, 규제의 뒷받침, 일반 시민의 의식 증가가 이를 지원하고 있습니다. 유전체 의료에 대한 지속적인 투자, NIPT 가이드라인 확대, AI 기반 진단 도구의 통합이 이 지역 시장 성장을 더욱 촉진하고 있습니다.

출생 전 및 신생아 유전자 검사 시장의 주요 기업은 Genes2me, Trivitron Healthcare, Retrogen, Aetna, Fulgent Genetics, Eurofins, Illumina, CENTOGENE, Genelab(Clevergene), Thermo Fisher Scientific, Myriad Genetics, Natera, Revvity, LaCAR, BGI Group, BillionToOne, LabCorp, Agilent, Yourgene Health입니다.

출생 전 및 신생아 유전자 검사 시장에서의 지위를 강화하기 위해, 기업은 혁신 주도형과 사업 확대 중시형의 전략을 병용하고 있습니다. 많은 기업들이 연구개발에 투자하여 고처리량 플랫폼을 개발하고 희귀 유전 질환 및 유전성 질환을 다루는 검사 포트폴리오를 확충하고 있습니다. 병원, 학술기관, 기술 파트너와의 전략적 제휴를 통해 시장에 빠르게 침투하고 다양한 환자 집단에 접근할 수 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 어머니의 고령화 및 출생 전 스크리닝 수요 증가

- NIPT 검사 수요 증가

- 유전성 질환의 발생률 상승

- 조기 진단에 대한 부모의 의식 및 수요 증가

- 정확성 및 접근성을 위한 기술 진보 확대

- 업계의 잠재적 위험 및 과제

- 고급 검사의 높은 비용

- 데이터의 프라이버시 및 보안

- 시장 기회

- 출산 전 케어에 있어서 맞춤형 의료 수요 증가

- 신흥 시장에 대한 침투 확대

- 관민 연계 대처의 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 유전자 검사 업계에서의 투자 및 자금 조달의 상황

- 기술적 상황

- 신흥 기술

- 현재의 기술

- 장래 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품 및 서비스별(2021-2034년)

- 주요 동향

- 키트 및 시약

- 서비스

제6장 시장 추계 및 예측 : 검사 유형별(2021-2034년)

- 주요 동향

- 출생 전 검사

- 스크리닝

- 비침습적 산전 검사(NIPT)

- 캐리어 스크리닝

- 혈청 스크리닝

- 경부 투과성 초음파 검사

- 진단

- 융모막 융모 채취(CVS)

- 양수 천자

- 스크리닝

- 신생아 검사

- 발뒤꿈치 천자 테스트

- 청각 스크리닝

- 심각한 선천성 심장 질환(CCHD)

- 기타 신생아 검사의 유형

제7장 시장 추계 및 예측 : 기술별(2021-2034년)

- 주요 동향

- 차세대 시퀀싱(NGS)

- 유리 DNA(cfDNA)

- 어레이 비교 유전체 하이브리드화(aCGH)

- 형광 in situ 하이브리드화(FISH)

- 분광분석

- 모든 엑솜 시퀀싱(WES)

- 기타 기술

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 다운증후군

- 페닐케톤뇨증(PKU)

- 낭포성 섬유증(CF)

- 겸상 적혈구 빈혈

- 선천성 갑상선 기능 저하증

- 펜드레드 증후군

- 기타 용도

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 진단 실험실

- 산과 및 전문 클리닉

- 기타 용도

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Aetna

- Agilent

- BGI Group

- BilliontoOne

- CENTOGENE

- Eurofins

- Fulgent Genetics

- Genelab(Clevergene)

- Genes2me

- Illumina

- Labcorp

- LaCAR

- Myriad Genetics

- Natera

- Retrogen

- Revvity

- Thermo Fisher Scientific

- Trivitron Healthcare

- Yourgene Health

The Global Prenatal and Newborn Genetic Testing Market was valued at USD 8.1 billion in 2024 and is estimated to grow at a CAGR of 12.8% to reach USD 9.1 billion by 2034.

The increasing prevalence of genetic conditions such as Down syndrome, cystic fibrosis, and spinal muscular atrophy is driving demand for early detection through prenatal and newborn genetic testing. Expectant parents are increasingly seeking reassurance and early intervention options.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.1 Billion |

| Forecast Value | $9.1 Billion |

| CAGR | 12.8% |

Rising Adoption of Kits and Reagents Segment

The kits and reagents segment held a significant share in 2024, as these consumables are essential for both clinical diagnostics and research workflows. Laboratories and diagnostic centers depend on high-quality, reliable reagents to ensure accurate and reproducible results. As testing volumes grow, driven by increasing demand for early genetic screening, the recurring nature of consumable use continues to boost segment performance.

Increasing Demand for the Prenatal Tests Segment

The prenatal tests segment held a sizeable share in 2024, owing to rising maternal age, increased risk awareness, and strong clinical adoption of non-invasive and invasive testing options. These tests help detect chromosomal abnormalities, genetic mutations, and fetal anomalies early in pregnancy, enabling more informed clinical decision-making. The shift toward first-trimester screening and the inclusion of expanded genetic panels have fueled sustained growth in this segment.

cfDNA to Gain Traction

The cell-free DNA (cfDNA) testing segment held a sustainable share in 2024, driven by a non-invasive, highly accurate method to screen for common chromosomal conditions like trisomy 21, 18, and 13. This method analyzes fetal DNA fragments circulating in maternal blood, reducing the need for invasive procedures like amniocentesis.

North America to Emerge as a Propelling Region

North America prenatal and newborn genetic testing market is poised to grow at a sizeable share in 2024, driven by strong healthcare infrastructure, advanced lab capabilities, and widespread access to genetic services. In the U.S. and Canada, early screening is widely adopted, supported by favorable insurance coverage, regulatory backing, and increasing public awareness. Continued investment in genomic medicine, expansion of NIPT guidelines, and integration of AI-based diagnostic tools are further fueling market growth across this region.

Major players in the prenatal and newborn genetic testing market are Genes2me, Trivitron Healthcare, Retrogen, Aetna, Fulgent Genetics, Eurofins, Illumina, CENTOGENE, Genelab (Clevergene), Thermo Fisher Scientific, Myriad Genetics, Natera, Revvity, LaCAR, BGI Group, BillionToOne, LabCorp, Agilent, and Yourgene Health.

To strengthen their position in the prenatal and newborn genetic testing market, companies are pursuing a mix of innovation-driven and expansion-focused strategies. Many are investing in R&D to develop high-throughput platforms and broaden their test portfolios to cover rare genetic conditions and inherited disorders. Strategic collaborations with hospitals, academic institutions, and technology partners are enabling faster market penetration and access to diverse patient populations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product and services trends

- 2.2.3 Test type trends

- 2.2.4 Technology trends

- 2.2.5 Application trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising maternal age and increasing demand for prenatal screening

- 3.2.1.2 Increasing demand for NIPT testing

- 3.2.1.3 Rising incidence of genetic disorders

- 3.2.1.4 Growing parental awareness and demand for early diagnosis

- 3.2.1.5 Expanding advancement in technologies for accuracy and accessibility

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced tests

- 3.2.2.2 Data privacy and security

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for personalized medicine in prenatal care

- 3.2.3.2 Increasing penetration in emerging markets

- 3.2.3.3 Expanding public-private initiatives

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Investment and funding landscape in the genetic testing industry

- 3.6 Technological landscape

- 3.6.1 Emerging technologies

- 3.6.2 Current technologies

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product and Services, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Kits and reagents

- 5.3 Services

Chapter 6 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Prenatal tests

- 6.2.1 Screening

- 6.2.1.1 Non-invasive prenatal testing (NIPT)

- 6.2.1.2 Carrier screening

- 6.2.1.3 Serum screening

- 6.2.1.4 Nuchal translucency ultrasound

- 6.2.2 Diagnostic

- 6.2.2.1 Chorionic villus sampling (CVS)

- 6.2.2.2 Amniocentesis

- 6.2.1 Screening

- 6.3 Newborn tests

- 6.3.1 Heel prick test

- 6.3.2 Hearing screening

- 6.3.3 Critical congenital heart defect (CCHD)

- 6.3.4 Other newborn test types

Chapter 7 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Next-generation sequencing (NGS)

- 7.3 Cell-free DNA (cfDNA)

- 7.4 Array-comparative genomic hybridization (aCGH)

- 7.5 Fluorescence in-situ hybridization (FISH)

- 7.6 Spectrometry

- 7.7 Whole exome sequencing (WES)

- 7.8 Other technologies

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Down syndrome

- 8.3 Phenylketonuria (PKU)

- 8.4 Cystic fibrosis (CF)

- 8.5 Sickle cell anemia

- 8.6 Congenital hypothyroidism

- 8.7 Pendred syndrome

- 8.8 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Diagnostic laboratories

- 9.4 Maternity and specialty clinics

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Aetna

- 11.2 Agilent

- 11.3 BGI Group

- 11.4 BilliontoOne

- 11.5 CENTOGENE

- 11.6 Eurofins

- 11.7 Fulgent Genetics

- 11.8 Genelab (Clevergene)

- 11.9 Genes2me

- 11.10 Illumina

- 11.11 Labcorp

- 11.12 LaCAR

- 11.13 Myriad Genetics

- 11.14 Natera

- 11.15 Retrogen

- 11.16 Revvity

- 11.17 Thermo Fisher Scientific

- 11.18 Trivitron Healthcare

- 11.19 Yourgene Health