|

시장보고서

상품코드

1833638

수면무호흡증 기기 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Sleep Apnea Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

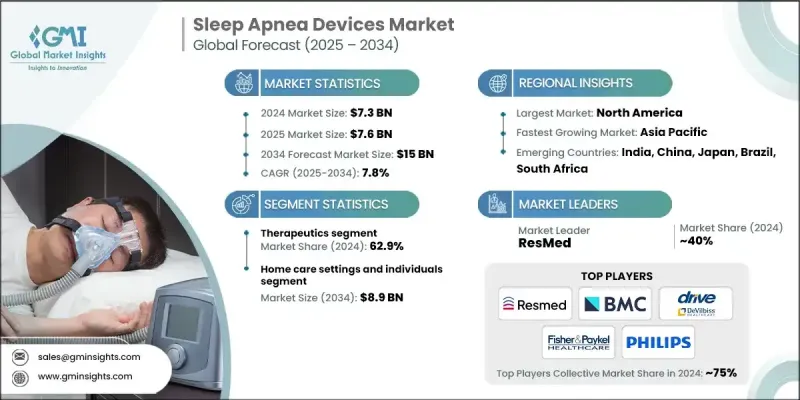

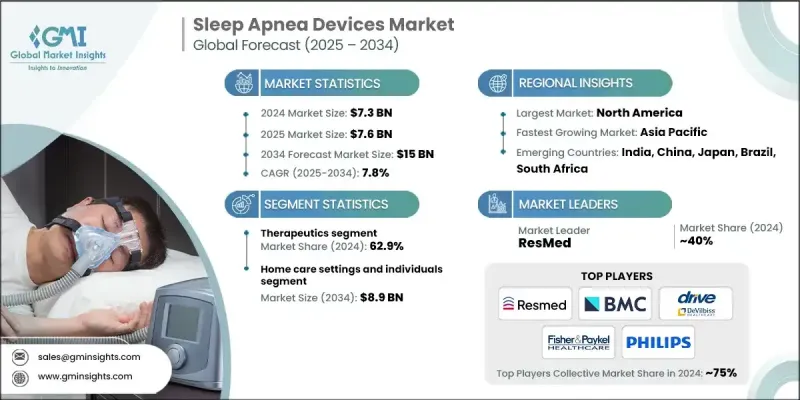

세계의 수면무호흡증 기기 시장 규모는 2024년에 73억 달러로 평가되었고, CAGR 7.8%를 나타내며 2034년까지는 150억 달러에 이를 것으로 예측됩니다.

이 성장을 이끌어내는 것은 세계 수면무호흡증 환자 수 증가, 수면장애에 대한 의식 증가, 고도로 휴대용 치료 솔루션에 대한 수요 증가입니다. 수면무호흡증 기기는 수면 호흡 장애의 진단과 관리에 모두 사용되며, 기도를 열린 상태로 유지하고 환자의 수면 상태를 효과적으로 모니터링하는 데 도움이 됩니다. 끈적거림, 낮의 피로감, 집중력 저하 등의 증상을 자각하는 사람이 늘어남에 따라, 진찰이나 수면장애의 진단이 일반적으로 되고 있습니다. 실험실 기반의 수면 폴리그래프 검사 및 가정용 검사 키트 등 수면 검사 방법의 혁신이 이 진단률의 급상승에 더욱 기여하고 있습니다. 더 많은 환자가 공식적으로 진단됨에 따라 CPAP, BiPAP 및 기타 수면무호흡 치료 기술과 같은 장비에 대한 수요가 증가하고 있습니다. 이 장치는 치료되지 않은 수면무호흡증의 건강 위험을 줄이고 환자 관리를 개선하고 전반적인 삶의 질을 향상시키는 데 도움이 됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 매출 | 73억 달러 |

| 예측 금액 | 150억 달러 |

| CAGR | 7.8% |

2024년 진단 분야는 37.1%의 점유율을 차지했습니다. 이 성장은 수면장애의 조기 발견에 대한 관심 증가와 컴팩트하고 인공지능이있는 진단 도구에 대한 액세스의 확대로 인해 발생합니다. 이러한 기술이 더욱 정교하고 합리적인 가격이 됨에 따라, 수면무호흡증의 스크리닝은 환자와 의료 제공업체 모두에게 더 빠르고 편리해지고 있습니다. 재택 검사와 실시간 데이터 분석의 진화는 진단 능력과 시장 확대를 계속 강화하고 있습니다.

재택치료 및 개인 부문은 2024년에 56.9%의 점유율을 차지했으며 임상 환경 이외의 비용 효율적인 장기 치료 솔루션에 대한 수요 증가에 힘입어 2034년까지 89억 달러를 창출할 전망입니다. 수면무호흡증을 집에서 관리하면 빈번한 통원과 입원 비용을 줄일 수 있습니다. 재택 치료에 대한 보험 적용이 확대되어 예산에 맞는 치료 옵션을 이용할 수 있게 됨으로써, 재택 수면 요법이 폭넓은 사람들에게 보다 친숙해지고, 보다 많은 사람들이 자신의 상태를 자립하고 적당한 가격으로 관리할 수 있게 되었습니다.

북미의 수면무호흡증 기기 시장은 2024년에 37.6%의 점유율을 차지했으며, 견고한 헬스케어 인프라, 확립된 상환 생태계, 수면 관련 건강 문제에 대한 사람들의 높은 의식에 지지되고 있습니다. 이 지역에서는 수면무호흡증의 치료 및 진단 기술의 조기 도입이 계속 호조입니다. 원격 모니터링 플랫폼과 커넥티드 헬스 솔루션의 통합은 이 지역의 환자 관리를 더욱 발전시키고 있습니다. Drive DeVilbiss, BMC, ResMed, Teleflex, Fisher & Paykel, Philips와 같은 주요 업계 기업들은 CPAP, BiPAP, 원격 수면 검사 솔루션을 포함한 종합적인 포트폴리오를 제공함으로써 북미의 입지를 강화하고 있습니다.

세계의 수면무호흡증 기기 시장에서 활약하는 주요 기업으로는 Cadwell, DynaFlex, Asahi KASEI, Glidewell, Apnea Sciences, SomnoMed, NIHON KOHDEN, Natus, WEINMANN 등이 있습니다. 세계의 수면무호흡증 기기 시장에서의 지위를 강화하기 위해 기업은 몇 가지 핵심 전략을 개발하고 있습니다. 여기에는 장비의 정확성, 휴대성 및 환자의 편안함을 높이기 위한 R&D에 대한 일관된 투자가 포함됩니다. 기업은 실시간 데이터 모니터링 및 원격 의료와의 호환성을 지원하는 커넥티드 기술을 도입하고 있습니다. 게다가 수면 클리닉, 재택 케어 제공업체, 보험 네트워크와의 제휴가 유통 확대에 도움이 되고 있습니다. 마케팅 이니셔티브는 일반 시민의 인식을 높이고 조기 진단을 장려하는 데 중점을 둡니다. 또한, 각 회사는 규제 당국의 승인을 통해 신시장에 진입하고, 특히 재택치료에서의 세계적인 수요 증가에 대응하기 위해 확장 가능한 생산 체제를 구축하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 수면무호흡증 및 관련 합병증의 발생률 증가

- 휴대용 고성능 수면무호흡 솔루션 수요 증가

- 수면무호흡증과 수면장애에 대한 높은 의식

- 고령화가 진행됨에 따라 수요가 증가

- 기술적 진보

- 업계의 잠재적 리스크 및 과제

- 수면무호흡증의 치료 준수 부족

- 제품 리콜 및 안전성에 대한 우려

- 시장 기회

- 신흥 시장 진출

- AI와 디지털 건강의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술적 상황

- 현재의 기술

- 신흥기술

- 향후 시장 동향

- 환급 시나리오

- 수면무호흡증 치료 장비에서 수면무호흡증 임플란트의 역할 진화

- 파이프라인 분석

- 투자 상황

- 시작 시나리오

- 가격 분석(2024년)

- Porter's Five Forces 분석

- PESTEL 분석

- 갭 분석

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 기업 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카, 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계·예측 : 제품별(2021-2034년)

- 주요 동향

- 치료법

- 기도 청소 시스템

- 기도 양압 (PAP) 장치

- 지속적 기도 양압 (CPAP) 장치

- 이중 양압 (BiPAP) 장치

- 자동 양압 (APAP) 장치

- 적응형 서보 환기(ASV) 장치

- 구강 장치

- 하악 전진 장치

- 혀 고정 장치

- 급속 상악 확장

- 마우스 가드

- 기타 치료법

- 진단

- 수면다원검사(PSG) 장치

- 이동형 PSG 장치

- 임상용 PSG 장치

- 액티그래피 시스템

- 맥박 산소 측정기

- 가정용 수면 검사(HST) 장치

- 유형 2

- 유형 3

- 유형 4

- 호흡 다중 기록 장치

- 수면다원검사(PSG) 장치

제6장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 재택치료 및 개인

- 수면 검사실 및 병원

제7장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제8장 기업 프로파일

- Asahi KASEI

- BMC

- Cadwell

- Drive DeVilbiss

- FISHER & PAYKEL

- natus

- NIHON KOHDEN

- Philips

- ResMed

- Teleflex

- WEINMANN

- Glidewell

- DynaFlex

- SomnoMed

- Apnea Sciences

The Global Sleep Apnea Devices Market was valued at USD 7.3 billion in 2024 and is estimated to grow at a CAGR of 7.8% to reach USD 15 billion by 2034.

This growth is being driven by the rising number of sleep apnea cases worldwide, increased awareness around sleep disorders, and growing demand for advanced, portable treatment solutions. Sleep apnea devices are used both for diagnosing and managing sleep-disordered breathing, helping to keep the airway open and monitor patients' sleep health effectively. With more individuals recognizing symptoms such as persistent snoring, fatigue during the day, and difficulty focusing, medical consultations and sleep disorder diagnoses are becoming more common. Innovations in sleep testing methods, including lab-based polysomnography and home testing kits, are further contributing to this surge in diagnosis rates. As more patients are formally diagnosed, demand for devices like CPAP, BiPAP, and other sleep apnea treatment technologies continues to rise. These devices are instrumental in reducing the health risks of untreated sleep apnea, offering improved patient care and boosting overall quality of life.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.3 Billion |

| Forecast Value | $15 Billion |

| CAGR | 7.8% |

In 2024, the diagnostics segment held a 37.1% share. This growth stems from heightened attention to early sleep disorder detection and greater access to compact and AI-powered diagnostic tools. As these technologies become more sophisticated and affordable, screening for sleep apnea is becoming quicker and more convenient for both patients and providers. The evolution of home-based testing and real-time data analysis continues to enhance diagnostic capabilities and market expansion.

The home care settings and individuals segment held a share of 56.9% in 2024 and is expected to generate USD 8.9 billion by 2034, fueled by the rising demand for cost-effective, long-term treatment solutions outside of clinical settings. Managing sleep apnea at home helps cut down on frequent clinic visits and hospitalization expenses. Expanded insurance coverage for home-based care and the availability of budget-friendly treatment options are helping make home sleep therapy more accessible to a wide population base, encouraging more people to manage their condition independently and affordably.

North America Sleep Apnea Devices Market held a 37.6% share in 2024, supported by robust healthcare infrastructure, a well-established reimbursement ecosystem, and high public awareness around sleep-related health issues. The region continues to see strong early adoption of both therapeutic and diagnostic sleep apnea technologies. Integration of remote monitoring platforms and connected health solutions is further advancing patient care in the region. Major industry players such as Drive DeVilbiss, BMC, ResMed, Teleflex, Fisher & Paykel, and Philips have cemented their position in North America by offering comprehensive portfolios that include CPAP, BiPAP, and remote sleep testing solutions.

Key companies active in the Global Sleep Apnea Devices Market Include Cadwell, DynaFlex, Asahi KASEI, Glidewell, Apnea Sciences, SomnoMed, NIHON KOHDEN, Natus, WEINMANN, and others. To strengthen their position in the global sleep apnea devices market, companies are deploying several core strategies. These include consistent investment in research and development to enhance device accuracy, portability, and patient comfort. Firms are introducing connected technologies that support real-time data monitoring and telehealth compatibility. In addition, partnerships with sleep clinics, home care providers, and insurance networks are helping expand distribution. Marketing initiatives focus on increasing public awareness and encouraging early diagnosis. Moreover, companies are entering new markets through regulatory approvals and building scalable production to meet rising global demand, particularly in home care settings.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of sleep apnea and related comorbidities

- 3.2.1.2 Growing demand for portable, high-performance sleep apnea solutions

- 3.2.1.3 Surging awareness of sleep apnea and sleep disorders

- 3.2.1.4 Rising aging population amplifying demand

- 3.2.1.5 Technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of adherence to sleep apnea treatment

- 3.2.2.2 Product recalls and safety concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets

- 3.2.3.2 AI and digital health integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Reimbursement scenario

- 3.8 Evolving role of sleep apnea implants within sleep apnea treatment devices

- 3.9 Pipeline analysis

- 3.10 Investment landscape

- 3.11 Start-up scenario

- 3.12 Pricing analysis, 2024

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

- 3.15 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 North America

- 4.3.2 Europe

- 4.3.3 Asia Pacific

- 4.3.4 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Therapeutics

- 5.2.1 Airway clearance systems

- 5.2.2 Positive airway pressure (PAP) devices

- 5.2.2.1 Continuous positive airway pressure (CPAP) devices

- 5.2.2.2 Bilevel positive airway pressure (BiPAP) devices

- 5.2.2.3 Automatic positive airway pressure (APAP) devices

- 5.2.3 Adaptive servo-ventilation (ASV) devices

- 5.2.4 Oral appliances

- 5.2.4.1 Mandibular advancement devices

- 5.2.4.2 Tongue-retaining devices

- 5.2.4.3 Rapid maxillary expansion

- 5.2.4.4 Mouth guards

- 5.2.5 Other therapeutics

- 5.3 Diagnostics

- 5.3.1 Polysomnography (PSG) device

- 5.3.1.1 Ambulatory PSG devices

- 5.3.1.2 Clinical PSG devices

- 5.3.2 Actigraphy systems

- 5.3.3 Pulse oximeters

- 5.3.4 Home sleep testing (HST) devices

- 5.3.4.1 Type 2

- 5.3.4.2 Type 3

- 5.3.4.3 Type 4

- 5.3.5 Respiratory polygraph

- 5.3.1 Polysomnography (PSG) device

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Home care settings and individuals

- 6.3 Sleep laboratories and hospitals

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Asahi KASEI

- 8.2 BMC

- 8.3 Cadwell

- 8.4 Drive DeVilbiss

- 8.5 FISHER & PAYKEL

- 8.6 natus

- 8.7 NIHON KOHDEN

- 8.8 Philips

- 8.9 ResMed

- 8.10 Teleflex

- 8.11 WEINMANN

- 8.12 Glidewell

- 8.13 DynaFlex

- 8.14 SomnoMed

- 8.15 Apnea Sciences