|

시장보고서

상품코드

1833650

덤프 트럭 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Dump Truck Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

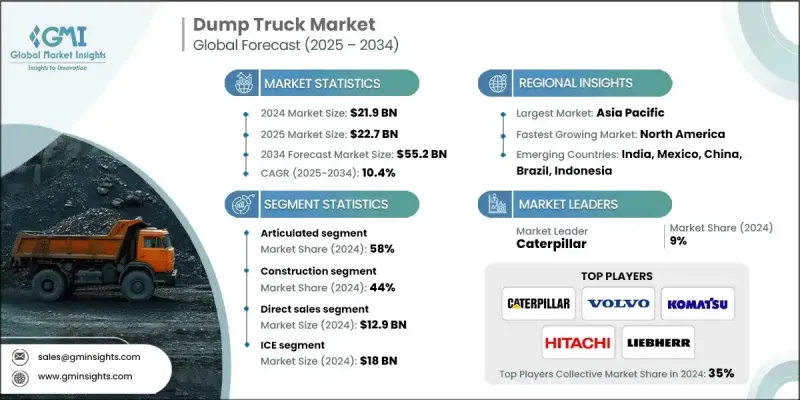

세계의 덤프 트럭 시장 규모는 2024년에 219억 달러로 평가되었고, CAGR 10.4%로 성장할 전망이며, 2034년에는 552억 달러에 이를 것으로 추정됩니다.

업계는 전동화 및 자율주행 기술에 대한 관심이 높아지면서 변혁기를 맞이하고 있습니다. 배출 가스를 삭감하고 에너지 효율을 높이는 제조업체에 대한 압력 증가가 전동 덤프 트럭의 개발을 뒷받침하고 있습니다. 동시에 운영 실수를 줄이고 비용을 낮추며 원격 조작 또는 완전 자율 주행을 통한 함대 운영을 가능하게 하는 기술로 자동화가 시작되고 있습니다. 이러한 진보는 기존의 운영 모델을 재구성하고 보다 깨끗하고 지능적이고 비용 효율적인 운송 솔루션으로 가는 길을 열고 있습니다. 한때 업계는 선형 공급망 및 전통적인 워크플로우 하에서 운영되었지만 COVID-19의 대유행 이후 상황이 크게 바뀌었습니다. 이전에는 꾸준하고 점진적인 성장과 최소한의 혼란이 특징이었지만, 시장은 현재 건강, 물류, 노동력 상호 작용의 과제에 대응하고 디지털 전환, 차량 기능의 혁신, 지속 가능한 생산의 필요성을 추진하고 있습니다. 진화하는 에코 시스템은 보다 민첩한 접근이 요구되고 있으며, 제조업체는 전통적인 설계와 생산에서 안전성, 지속가능성, 생산성에 대응하는 통합 기술 중심의 비즈니스 모델로 이동해야 합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 219억 달러 |

| 예측 금액 | 552억 달러 |

| CAGR | 10.4% |

아티큘레티드 덤프 트럭 부문은 2024년에 58%의 점유율을 차지했으며, 2025-2034년 CAGR 11%로 성장할 것으로 예측됩니다. 다관절 트랙은 적재량과 오프로드 성능의 지속적인 업그레이드를 볼 수 있습니다. 견고하고 울퉁불퉁한 노면에서의 유연성을 유지하면서 더 큰 짐을 다룰 수 있는 트럭에 대한 수요가 높아지는 가운데 제조업체는 설계 혁신에 중점적으로 투자하고 있습니다. 향상된 드라이브 트레인, 섀시 개선 및 개선된 서스펜션 시스템은 까다로운 조건에서 안정성, 적응성 및 더 나은 연비의 필요성을 해결하기 위해 도입되었습니다. 인프라 프로젝트가 더욱 복잡해지고 까다로운 환경에 배치됨에 따라 연결 트랙은 안전성과 내구성을 극대화하면서 자재를 효율적으로 이동할 수 있는 이상적인 솔루션을 제공합니다.

건설 부문은 2024년에 44%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 11.7%로 성장할 것으로 예측됩니다. 고도로 전문화된 덤프 트럭에 대한 건설 업계 수요 증가가 제품 개발을 재구성하고 있습니다. 제조업체는 도시 개발에 적합한 컴팩트한 유닛부터 광대한 인프라 프로젝트를 위해 설계된 대규모 오프로드 모델에 이르기까지 광범위한 건설 요구를 충족하는 모델 구축에 주력하고 있습니다. 용도의 다양화에 따라 기업은 범용성, 연비 효율, 텔레매틱스 및 적재 모니터링 시스템과의 통합을 선호합니다. 건설 회사가 특정 작업 및 환경에 맞는 장비를 찾는 동안 맞춤형 고성능 덤프 트럭에 대한 수요는 계속 급증하고 있습니다.

중국의 덤프 트럭 시장 점유율은 45%로, 2024년 시장 규모는 42억 달러로 평가되었습니다. 중국은 수입 의존도를 줄이기 위해 채굴 사업 확대 및 국내 석탄 생산 규모 확대를 적극 추진하고 있으며, 고용량 덤프 트럭의 일관된 수요로 이어지고 있습니다. 세계 철강 제조에서 중국의 이점과 세계 생산량의 대부분을 지배하는 희토류 생산에서 중국의 압도적인 역할은 견고한 덤프 트럭 함대의 필요성을 더욱 가속화하고 있습니다. 이러한 산업을 지원하기 위해, 특히 어려운 지형에서 장기간에 걸쳐 대량 가동을 유지할 수 있는 내구성 있는 대형 차량에 대한 투자가 증가하고 있습니다.

세계의 덤프 트럭 시장을 형성하는 주요 기업으로는 Hitachi, BelAZ, Volvo, Scania, Cummins, SANY, Parker Hannifin, Caterpillar, Liebherr 및 Komatsu 등이 있습니다. 덤프 트럭 업계의 주요 기업은 경쟁력을 강화하기 위해 기술 혁신, 제품 다양화 및 지역 시장 침투에 적극적으로 주력하고 있습니다. 많은 기업들이 세계 배기 가스 기준을 충족하기 위해 배터리 구동 모델과 하이브리드 모델을 개발하고 전동화를 진행하고 있습니다. 각 회사는 또한 GPS 추적, 자동 적재 시스템, 운행 관리 소프트웨어와 같은 디지털 도구를 통합하여 운행 효율성을 높입니다. 현지 유통업체 및 인프라 기업과의 전략적 제휴는 신흥 시장에서 브랜드의 존재감과 고객 충성도를 향상시키는 데 도움이 됩니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 원재료 공급자

- 제조업체

- 도매업체

- 최종 용도

- 비용 구조

- 이익률

- 각 단계에서의 부가가치

- 공급망에 영향을 미치는 요인

- 파괴자

- 공급자의 상황

- 영향요인

- 성장 촉진요인

- 인프라 확장으로 덤프 트럭 수요 증가

- 기술의 진보에 의해 덤프 트럭의 효율성 및 안전성 향상

- 교통 인프라에 대한 정부 투자가 수요 자극

- 광업 부문의 성장이 덤프 트럭의 매출 촉진

- 업계의 잠재적 위험 및 과제

- 경기 후퇴에 의해 건설업 및 광업 활동 감소

- 엄격한 배출 규제에 의해 제조 비용 상승

- 시장 기회

- 전기식 및 하이브리드식 덤프 트럭 도입 증가

- 스마트 차량 관리 및 텔레매틱스 통합

- 성장 촉진요인

- 기술 동향 및 혁신 생태계

- 현재의 기술

- 자율 시스템 개발 및 구현 로드맵

- 전기 및 하이브리드 파워트레인의 진화와 시장 도입

- 텔레매틱스 및 IoT 통합의 진보와 데이터 분석

- 예지보전 및 AI 애플리케이션 개발

- 신흥 기술

- 사이버 보안 솔루션 및 접속 기기의 보호

- 블록체인의 통합 및 공급망의 투명성

- 증강현실 및 가상 트레이닝 시스템의 개발

- 5G 연결 및 실시간 데이터 처리 용도

- 현재의 기술

- 규제 상황

- 세계의 배출 기준과 환경 규제

- 광산 안전 규제 및 MSHA 컴플라이언스

- 자율주행차 규제 및 기준

- 국제무역 및 관세의 영향

- 사이버 보안 규제 및 데이터 보호

- 애프터마켓 서비스 및 서포트 에코시스템

- 부품 및 컴포넌트의 애프터마켓 분석

- 유지관리 및 수리 서비스 시장

- 교육 및 인증 프로그램 시장

- 디지털 서비스 및 소프트웨어 솔루션

- 금융 및 임대 시장 분석

- 설비 대출 시장 역학

- 기기리스 시장 분석

- 임대 시장 및 단기적인 해결책

- 대체 자금 조달 솔루션

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 지속가능성과 환경 측면

- 환경영향 평가 및 라이프사이클 분석

- 사회적 영향 및 지역 사회의 관계

- 거버넌스 및 기업 책임

- 지속가능한 기술 개발

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획 및 자금조달

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 관절식

- 50톤 미만

- 50톤 이상

- 리지드

- 50톤 미만

- 50-100톤

- 101-150톤

- 151-200톤

- 201-250톤

- 251-300톤

- 300톤 이상

제6장 시장 추계 및 예측 : 드라이브 구성별(2021-2034년)

- 주요 동향

- 전륜 구동(FWD)

- 후륜 구동(RWD)

- 전륜 구동(AWD)

제7장 시장 추계 및 예측 : 추진력별(2021-2034년)

- 주요 동향

- 얼음

- 전기

- 하이브리드

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 광업

- 건설

- 기타

제9장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접 판매

- 리셀러

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 세계 기업

- Caterpillar

- Komatsu

- Liebherr

- Hitachi

- Volvo

- Scania

- Cummins

- Parker Hannifin

- Regional Champions

- John Deere

- SANY

- BelAZ

- XCMG

- Doosan Infracore

- Hyundai Construction Equipment

- Bell Equipment

- MAN Truck & Bus

- Terex

- Tadano

- 신흥 기업와 및 기술 교란 기업

- Autonomous Solutions(ASI)

- Modular Mining Systems

- Epiroc

- Sandvik Mining & Rock Solutions

- Kuhn Schweiz

- Allison Transmission

- Rio Tinto Technology & Innovation

The Global Dump Truck Market was valued at USD 21.9 billion in 2024 and is estimated to grow at a CAGR of 10.4% to reach USD 55.2 billion by 2034.

The industry is undergoing a transformative shift fueled by growing interest in electrification and autonomous technologies. Rising pressure on manufacturers to reduce emissions and improve energy efficiency is pushing the development of electric dump trucks. At the same time, automation is gaining ground, with technologies that reduce operational errors, lower costs, and enable remote-controlled or fully autonomous fleet operations. These advances are reshaping traditional operating models, making way for cleaner, more intelligent, and cost-efficient transport solutions. While the industry once operated under linear supply chains and conventional workflows, the landscape shifted significantly after the COVID-19 pandemic. Previously marked by steady, incremental growth and minimal disruption, the market now responds to challenges in health, logistics, and workforce interaction, driving the need for digital transformation, innovation in vehicle functionality, and sustainable production. The evolving ecosystem demands a more agile approach, compelling manufacturers to shift from traditional design and production toward integrated, technology-driven business models that address safety, sustainability, and productivity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.9 Billion |

| Forecast Value | $55.2 billion |

| CAGR | 10.4% |

The articulated dump truck segment held a 58% share in 2024 and is expected to grow at a CAGR of 11% between 2025 and 2034. Articulated trucks are seeing continuous upgrades in payload capacity and off-road performance. With demand rising for trucks that can handle larger loads while maintaining flexibility across rugged and uneven surfaces, manufacturers are heavily investing in design innovation. Enhanced drivetrains, chassis modifications, and improved suspension systems are being implemented to accommodate the need for stability, adaptability, and better fuel economy under tough conditions. As infrastructure projects become more complex and are in challenging environments, articulated trucks offer the ideal solution for moving materials efficiently while maximizing safety and durability.

The construction segment held a 44% share in 2024 and is forecasted to grow at a CAGR of 11.7% through 2034. The construction industry's growing demand for highly specialized dump trucks is reshaping product development. Manufacturers are focusing on building models that address a wide range of construction needs, from compact units suited for urban developments to large-scale off-road models designed for expansive infrastructure projects. With the increasing variety of applications, companies are prioritizing versatility, fuel efficiency, and integration with telematics and load monitoring systems. As construction firms look for equipment tailored to specific tasks and environments, the demand for customized and high-performance dump trucks continues to surge.

China Dump Truck Market held a 45% share and generated USD 4.2 billion in 2024. China's aggressive push to expand its mining operations and scale domestic coal production to reduce import dependence has led to consistent demand for high-capacity dump trucks. The country's dominance in global steel manufacturing and its commanding role in rare earth metals production, where it controls most global output, have further accelerated the requirement for robust dump truck fleets. To support these industries, there has been increased investment in durable and heavy-duty vehicles capable of sustaining high-volume operations over prolonged periods, especially in challenging terrain.

Leading companies shaping the Global Dump Truck Market include Hitachi, BelAZ, Volvo, Scania, Cummins, SANY, Parker Hannifin, Caterpillar, Liebherr, and Komatsu. Top players in the dump truck industry are actively focusing on innovation, product diversification, and regional market penetration to strengthen their competitive position. Many are advancing toward electrification by developing battery-powered and hybrid models to meet global emission standards. Companies are also integrating digital tools, including GPS tracking, automated loading systems, and fleet management software, to enhance operational efficiency. Strategic collaborations with local distributors and infrastructure firms help increase brand presence and customer loyalty in emerging markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.1.3 Base estimates and calculations

- 1.1.4 Base year calculation

- 1.1.5 Key trends for market estimates

- 1.2 Forecast model

- 1.3 Primary research and validation

- 1.4 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Secondary

- 1.5.1.1 Paid Sources

- 1.5.1.2 Public Sources

- 1.5.1.3 Sources, by region

- 1.5.1 Secondary

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Drive Configuration

- 2.2.4 Propulsion

- 2.2.5 Application

- 2.2.6 Distribution Channels

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Manufacturer

- 3.1.1.3 Distributor

- 3.1.1.4 End use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Infrastructure expansion fuels demand for dump trucks

- 3.2.1.2 Technological advancements enhance dump truck efficiency and safety

- 3.2.1.3 Government investments in transportation infrastructure spur demand

- 3.2.1.4 Mining sector growth boosts dump truck sales

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Economic downturns reduce construction and mining activities

- 3.2.2.2 Stringent emissions regulations increase manufacturing costs

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of electric and hybrid dump trucks

- 3.2.3.2 Smart fleet management and telematics integration

- 3.2.1 Growth drivers

- 3.3 Technology Trends & Innovation Ecosystem

- 3.3.1 Current technologies

- 3.3.1.1 Autonomous systems development & implementation roadmap

- 3.3.1.2 Electric & hybrid powertrain evolution & market adoption

- 3.3.1.3 Telematics & IoT integration advances & data analytics

- 3.3.1.4 Predictive maintenance & AI applications development

- 3.3.2 Emerging technologies

- 3.3.2.1 Cybersecurity solutions & connected equipment protection

- 3.3.2.2 Blockchain integration & supply chain transparency

- 3.3.2.3 Augmented reality & virtual training system development

- 3.3.2.4 5G connectivity & real-time data processing applications

- 3.3.1 Current technologies

- 3.4 Regulatory landscape

- 3.4.1 Global emissions standards & environmental regulations

- 3.4.2 Mining safety regulations & MSHA compliance

- 3.4.3 Autonomous vehicle regulations & standards

- 3.4.4 International trade & tariff implications

- 3.4.5 Cybersecurity regulations & data protection

- 3.5 Aftermarket services & support ecosystem

- 3.5.1 Parts & components aftermarket analysis

- 3.5.2 Maintenance & repair services market

- 3.5.3 Training & certification programs market

- 3.5.4 Digital services & software solutions

- 3.6 Financing & leasing market analysis

- 3.6.1 Equipment financing market dynamics

- 3.6.2 Equipment leasing market analysis

- 3.6.3 Rental market & short-term solutions

- 3.6.4 Alternative financing solutions

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Environmental impact assessment & lifecycle analysis

- 3.10.2 Social impact & community relations

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable technological development

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($ Bn & Units)

- 5.1 Key trends

- 5.2 Articulated

- 5.2.1 Below 50 Metric Tons

- 5.2.2 50 Metric Tons and above

- 5.3 Rigid

- 5.3.1 Below 50 metric tons

- 5.3.2 50 to 100 metric tons

- 5.3.3 101 - 150 metric tons

- 5.3.4 151 - 200 metric tons

- 5.3.5 201 - 250 metric tons

- 5.3.6 251 - 300 metric tons

- 5.3.7 Above 300 metric tons

Chapter 6 Market Estimates & Forecast, By Drive Configuration, 2021 - 2034 ($ Bn & Units)

- 6.1 Key trends

- 6.2 Front-wheel drive (FWD)

- 6.3 Rear-wheel drive (RWD)

- 6.4 All-wheel drive (AWD)

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($ Bn & Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($ Bn & Units)

- 8.1 Key trends

- 8.2 Mining

- 8.3 Construction

- 8.4 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channels, 2021 - 2034 ($ Bn & Units)

- 9.1 Key trends

- 9.2 Direct Sales

- 9.3 Distributors/Dealers

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($ Bn & Units)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Caterpillar

- 11.1.2 Komatsu

- 11.1.3 Liebherr

- 11.1.4 Hitachi

- 11.1.5 Volvo

- 11.1.6 Scania

- 11.1.7 Cummins

- 11.1.8 Parker Hannifin

- 11.2 Regional Champions

- 11.2.1 John Deere

- 11.2.2 SANY

- 11.2.3 BelAZ

- 11.2.4 XCMG

- 11.2.5 Doosan Infracore

- 11.2.6 Hyundai Construction Equipment

- 11.2.7 Bell Equipment

- 11.2.8 MAN Truck & Bus

- 11.2.9 Terex

- 11.2.10 Tadano

- 11.3 Emerging Players & Technology Disruptors

- 11.3.1 Autonomous Solutions (ASI)

- 11.3.2 Modular Mining Systems

- 11.3.3 Epiroc

- 11.3.4 Sandvik Mining & Rock Solutions

- 11.3.5 Kuhn Schweiz

- 11.3.6 Allison Transmission

- 11.3.7 Rio Tinto Technology & Innovation