|

시장보고서

상품코드

1833652

자동차 스타트 스톱 시스템 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Automotive Start-Stop System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

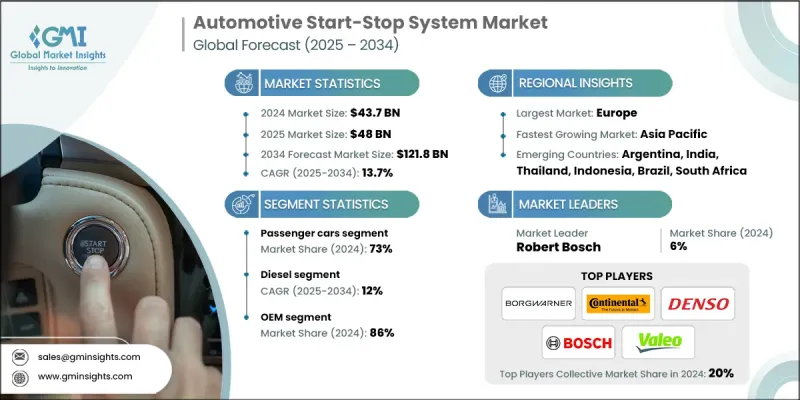

Global Market Insights Inc.가 발행한 최신 보고서에 따르면 세계의 자동차 스타트 스톱 시스템 시장은 2024년에 437억 달러로 평가되었고, CAGR 13.7%로 성장할 전망이며, 2025년 480억 달러에서 2034년에는 1,218억 달러로 성장할 것으로 예측되고 있습니다.

세계 정부가 배출 가스 규제 및 연비 기준을 엄격히 하고 있기 때문에 자동차 제조업체는 스타트 스톱 시스템과 같은 절연비 기술의 통합을 강요하고 있습니다. 이러한 시스템은 공회전시 배출 가스를 줄이고 전체 연비를 개선하는 데 도움이 되므로 컴플라이언스를 준수하는 최적의 솔루션이 되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 437억 달러 |

| 예측 금액 | 1,218억 달러 |

| CAGR | 13.7% |

승용차 수요 증가

승용차 부문은 일상 사용 차량의 저연비로 친환경 솔루션에 대한 왕성한 수요에 견인되어 2024년에 주목할만한 점유율을 차지했습니다. 자동차 제조업체는 배기가스 규제를 준수해, 연비 개선에 대한 소비자의 기대에 응하기 위해, 소형차, 중형차, 프리미엄차 등 폭넓은 차종에 스타트 스톱 시스템을 표준 장비하고 있습니다.

디젤 사용 증가

디젤 파워트레인이 승용차와 소형 상용차에 널리 보급됨에 따라 디젤 부문은 2024년에 큰 점유율을 얻었습니다. 높은 토크 및 연료 효율로 알려진 디젤 엔진은 공회전시 연료 소비 및 배출을 더욱 줄이는 스타트 스톱 시스템에서 큰 이점을 누리고 있습니다. 전동화로의 전환이 점차 진행되고 있음에도 불구하고, 스타트 스톱 기술을 탑재한 디젤차는 플릿 오퍼레이터와 비용 의식이 높은 소비자에게 계속 어필하고 있습니다.

견인력을 늘리는 OEM

OEM 분야는 신차 플랫폼에 대한 임베디드 기능에 의해 2024년에 큰 점유율을 차지했습니다. OEM 제조업체는 이 기술을 하이브리드 및 전기 드라이브 트레인으로 완전히 전환하지 않고 연비 목표 및 배기 가스 규제를 달성하기 위한 비용 효율적인 솔루션으로 간주합니다. OEM 각 회사는 Tier 1 공급업체와 긴밀하게 협력하여 차량 라인업 전반에 걸쳐 확장 가능한 보다 컴팩트하고 내구성 있고 효율적인 시스템을 공동 개발하고 있습니다.

추진력으로 대두하는 유럽

유럽 자동차 스타트 스톱 시스템 시장은 EU의 엄격한 배기가스 규제, 연료 가격 상승, 지속가능성의 중요성을 바탕으로 2024년에 견조한 수익을 올렸습니다. 독일, 프랑스, 영국 등 유럽 주요 국가들은 적극적인 탄소 감축 정책을 시행하고 있으며 스타트 스톱 시스템과 같은 연비 절감 기술의 보급을 촉진하고 있습니다. 또한, 성숙한 자동차 제조거점과 환경 친화적인 기능에 대한 소비자의 의식이이 지역에서 OEM의 강력한 섭취를 뒷받침하고 있습니다.

자동차 스타트 스톱 시스템 시장의 주요 기업은 Valeo, Hitachi Automotive, Robert Bosch, Magna, BorgWarner, Continental, ZF Friedrichshafen, Johnson Controls, Aisin Seiki 및 Denso입니다.

시장 포지션을 강화하기 위해 자동차 스타트 스톱 시스템 분야의 기업들은 혁신, 파트너십 및 비용 최적화에 주력하고 있습니다. 주요 공급업체는 시스템 성능과 내구성을 높이기 위해 보다 견고한 배터리 관리 시스템, 회생 브레이크 통합, 자동 시작 모터 개발을 추진하고 있습니다. OEM과 기술 제공업체 간의 협업은 특정 파워트레인 구성에 맞는 첨단 시스템 시장 출시 시간을 단축하고 있습니다. 동시에 기업은 공급망의 탄력성과 비용 효율성을 보장하기 위해 세계 생산 기지를 확대하고 있습니다. 성능, 신뢰성 및 저렴한 가격의 균형을 유지함으로써 이러한 전략적 움직임은 기업이 자동차 제조업체와 장기 계약을 확보하고 규제가 강화되는 업계에서 경쟁력을 유지하는 데 도움이 됩니다.

목차

제1장 조사 방법

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 기본 추정 및 계산

- 기준 연도 계산

- 시장 예측의 주요 동향

- GMI 독자적인 AI 시스템

- AI를 활용한 조사 강화

- 소스 일관성 프로토콜

- AI의 정밀도 지표

- 예측 모델

- 1차 조사 및 검증

- 시장 예측의 주요 동향

- 정량화된 시장 영향 분석

- 성장 파라미터 예측에 대한 수학적 영향

- 시나리오 분석 프레임워크

- 1차 정보의 일부(단, 이것에 한정되는 것은 아니다)

- 데이터 마이닝 소스

- 2차

- 유료소스

- 공개 정보원

- 지역별 정보원

- 2차

- 조사의 궤적 및 신뢰도 점수

- 조사 트레일의 컴포넌트 :

- 스코어링 컴포넌트

- 조사의 투명성에 관한 보충

- 소스 기여 프레임워크

- 품질 보증 지표

- 신뢰에 대한 헌신

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 엄격한 배출가스 규제 및 연비 규제

- 연료 가격 상승 및 소비자 효율성 요구

- 스타터 모터 및 배터리의 기술적 진보

- 하이브리드차 및 마일드 하이브리드차의 생산 급증

- 친환경 기술에 대한 정부의 우대조치

- 업계의 잠재적 위험 및 과제

- 시스템 및 컴포넌트의 높은 비용

- 배터리 소모 및 교체 빈도

- 시장 기회

- 하이브리드 및 전동 파워트레인과의 통합

- 배터리 기술 및 에너지 회수의 진보

- 신흥 자동차 시장 진출

- ADAS 및 스마트 모빌리티 플랫폼과의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신의 상황

- 특허 분석

- 지속가능성 및 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경 친화적인 노력

- 탄소발자국의 고려

- 이용 사례 및 용도 분석

- 도시 운전 용도

- 시가지 교통의 정지 및 발진의 시나리오

- 배송 차량 최적화

- 택시 및 라이드 공유 용도

- 대중교통기관 통합

- 고속도로 및 혼합 운전 조건

- 장거리 여행 용도

- 상용선의 운용

- 긴급 차량 응용

- 레크리에이션 차량의 통합

- 특수 이용 사례

- 건설 및 산업 차량

- 농업 기기의 용도

- 해양 및 오프로드 용도

- 도시 운전 용도

- 비용 편익 및 ROI 분석 프레임워크

- 총소유 비용 분석

- 초기 시스템 비용 내역

- 유지보수 및 교환 비용

- 연료 절약의 정량화

- 수명 주기 비용 모델링

- 투자수익률 지표

- 차종별 회수 기간 분석

- 순 현재 가치 계산

- 내부 수익률 평가

- 감도 분석 프레임워크

- 총소유 비용 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획 및 자금조달

제5장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 이륜차

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 경상용차

- 중형 상용차

- 대형 상용차

제6장 시장 추계 및 예측 : 연료별(2021-2034년)

- 주요 동향

- 디젤

- 가솔린

- CNG

- 하이브리드

제7장 시장 추계 및 예측 : 기술별(2021-2034년)

- 주요 동향

- 강화된 스타터

- 종래의 스타터

- 탠덤 솔레노이드 스타터

- 벨트 구동 교류 발전기 스타터(BAS)

- 직분사 엔진 시스템

- 통합 스타터 제너레이터(ISG)

제8장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 엔진 제어 유닛(ECU)

- 배터리

- 알터네이터

- 스타터 모터

- DC/DC 컨버터

- 센서

- 기타

제9장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 포르투갈

- 크로아티아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 싱가포르

- 태국

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 세계 기업

- Aisin Seiki

- BorgWarner

- Continental

- Denso

- Exide Technologies

- GS Yuasa

- Hitachi

- Infineon Technologies

- Johnson Controls

- Magna International Inc.

- Mahle

- NXP Semiconductors

- Panasonic

- Robert Bosch

- Schaeffler

- Valeo

- ZF Friedrichshafen

- 지역 기업

- Calsonic Kansei

- Eaton Corporation

- Faurecia

- Hella GmbH & Co.

- Hyundai Mobis

- JTEKT Corporation

- Lear Corporation

- Schaeffler AG

- Visteon Corporation

- 신흥 기업

- ABB Ltd.

- Aptiv PLC

- Infineon Technologies

- LEM Holding

The global automotive start-stop system market was estimated at USD 43.7 billion in 2024 and is expected to grow from USD 48 billion in 2025 to USD 121.8 billion by 2034, at a CAGR of 13.7%, according to the latest report published by Global Market Insights Inc.

Governments across the globe are enforcing stricter emission norms and fuel economy standards, compelling automakers to integrate fuel-saving technologies like start-stop systems. These systems help reduce idling emissions and improve overall fuel efficiency, making them a go-to solution for compliance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $43.7 Billion |

| Forecast Value | $121.8 Billion |

| CAGR | 13.7% |

Growing Demand for Passenger Cars

The passenger cars segment held a notable share in 2024, driven by strong demand for fuel-efficient and environmentally friendly solutions in daily-use vehicles. Automakers are integrating start-stop systems as a standard feature across a wide range of car models, including compact, midsize, and premium offerings, to comply with emissions regulations and meet consumer expectations for improved fuel economy.

Rising Usage of Diesel

The diesel segment generated a significant share in 2024, as diesel powertrains remain prevalent in the passenger and light commercial vehicles. Diesel engines, known for their high torque and fuel efficiency, benefit significantly from start-stop systems that further reduce idle-time fuel consumption and emissions. Despite a gradual shift toward electrification, diesel vehicles equipped with start-stop technology continue to appeal to fleet operators and cost-conscious consumers.

OEM to Gain Traction

The OEM segment held a sizeable share in 2024, driven by built-in features across new vehicle platforms. Original Equipment Manufacturers view this technology as a cost-effective solution to meet fuel economy targets and emission mandates without fully transitioning to hybrid or electric drivetrains. OEMs are partnering closely with tier-1 suppliers to co-develop more compact, durable, and efficient systems that can be scaled across vehicle lineups.

Europe to Emerge as a Propelling Region

Europe automotive start-stop system market generated robust revenues in 2024, backed by stringent EU emission regulations, high fuel prices, and a strong emphasis on sustainability. Major European countries, including Germany, France, and the UK, have implemented aggressive carbon reduction policies, prompting widespread adoption of fuel-saving technologies like start-stop systems. Additionally, a mature automotive manufacturing base and consumer awareness around eco-friendly features are driving strong OEM uptake in the region.

Major players in the automotive start-stop system market are Valeo, Hitachi Automotive, Robert Bosch, Magna, BorgWarner, Continental, ZF Friedrichshafen, Johnson Controls, Aisin Seiki, and Denso.

To strengthen their market position, companies in the automotive start-stop system space are focusing on innovation, partnerships, and cost optimization. Leading suppliers are developing more robust battery management systems, regenerative braking integration, and silent start motors to enhance system performance and durability. Collaborations between OEMs and technology providers are accelerating time-to-market for advanced systems tailored to specific powertrain configurations. At the same time, firms are expanding their global production footprints to ensure supply chain resilience and cost efficiency. By balancing performance, reliability, and affordability, these strategic moves are helping companies secure long-term contracts with automakers and maintain a competitive edge in an increasingly regulated industry.

Table of Contents

Chapter 1 Methodology

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.1.3 Base estimates and calculations

- 1.1.4 Base year calculation

- 1.1.5 Key trends for market estimates

- 1.1.6 GMI proprietary AI system

- 1.1.6.1 AI-Powered research enhancement

- 1.1.6.2 Source consistency protocol

- 1.1.6.3 AI accuracy metrics

- 1.2 Forecast model

- 1.3 Primary research and validation

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario Analysis Framework

- 1.4 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Secondary

- 1.5.1.1 Paid Sources

- 1.5.1.2 Public Sources

- 1.5.1.3 Sources, by region

- 1.5.1 Secondary

- 1.6 Research Trail & Confidence Scoring

- 1.6.1 Research Trail Components:

- 1.6.2 Scoring Components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicles

- 2.2.3 Fuel

- 2.2.4 Technology

- 2.2.5 Component

- 2.2.6 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.1.1 Stringent emission and fuel economy regulations

- 3.2.1.1.2 Rising fuel prices and consumer demand for efficiency

- 3.2.1.1.3 Technological advancements in starter motors and batteries

- 3.2.1.1.4 Surge in hybrid and mild-hybrid vehicle production

- 3.2.1.1.5 Government incentives for eco-friendly technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system and component costs

- 3.2.2.2 Battery wear and replacement frequency

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with hybrid and electric powertrains

- 3.2.3.2 Advancements in battery technology and energy recovery

- 3.2.3.3 Expansion into emerging automotive markets

- 3.2.3.4 Integration with ADAS and smart mobility platforms

- 3.2.1.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.8 Patent analysis

- 3.9 Sustainability and environmental aspects

- 3.9.1 Sustainable practices

- 3.9.2 Waste reduction strategies

- 3.9.3 Energy efficiency in production

- 3.9.4 Eco-friendly Initiatives

- 3.9.5 Carbon footprint considerations

- 3.10 Use cases and application analysis

- 3.10.1 Urban driving applications

- 3.10.1.1 City traffic stop-start scenarios

- 3.10.1.2 Delivery vehicle optimization

- 3.10.1.3 Taxi & ride-sharing applications

- 3.10.1.4 Public transportation integration

- 3.10.2 Highway and mixed driving conditions

- 3.10.2.1 Long-distance travel applications

- 3.10.2.2 Commercial fleet operations

- 3.10.2.3 Emergency vehicle applications

- 3.10.2.4 Recreational vehicle integration

- 3.10.3 Specialized use cases

- 3.10.3.1 Construction & industrial vehicles

- 3.10.3.2 Agricultural equipment applications

- 3.10.3.3 Marine & off-road applications

- 3.10.1 Urban driving applications

- 3.11 Cost-benefit and ROI analysis framework

- 3.11.1 Total cost of ownership analysis

- 3.11.1.1 Initial system cost breakdown

- 3.11.1.2 Maintenance & replacement costs

- 3.11.1.3 Fuel savings quantification

- 3.11.1.4 Lifecycle cost modeling

- 3.11.2 Return on investment metrics

- 3.11.2.1 Payback period analysis by vehicle type

- 3.11.2.2 Net present value calculations

- 3.11.2.3 Internal rate of return assessment

- 3.11.2.4 Sensitivity analysis framework

- 3.11.1 Total cost of ownership analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD Mn)

- 5.1 Key trends

- 5.2 Two wheelers

- 5.3 Passenger cars

- 5.3.1 Hatchbacks

- 5.3.2 Sedans

- 5.3.3 SUVs

- 5.4 Commercial vehicles

- 5.4.1 Light commercial vehicle

- 5.4.2 Medium commercial vehicle

- 5.4.3 Heavy commercial vehicle

Chapter 6 Market Estimates & Forecast, By Fuel, 2021 - 2034 (USD Mn)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 Gasoline

- 6.4 CNG

- 6.5 Hybrid

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 (USD Mn)

- 7.1 Key trends

- 7.2 Enhanced starter

- 7.2.1 Conventional starter

- 7.2.2 Tandem solenoid starter

- 7.3 Belt-driven alternator starter (BAS)

- 7.4 Direct injection engine systems

- 7.5 Integrated starter generator (ISG)

Chapter 8 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Mn)

- 8.1 Key trends

- 8.2 Engine control unit (ECU)

- 8.3 Battery

- 8.4 Alternator

- 8.5 Starter Motor

- 8.6 DC/DC converter

- 8.7 Sensors

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 (USD Mn)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Portugal

- 10.3.9 Croatia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Aisin Seiki

- 11.1.2 BorgWarner

- 11.1.3 Continental

- 11.1.4 Denso

- 11.1.5 Exide Technologies

- 11.1.6 GS Yuasa

- 11.1.7 Hitachi

- 11.1.8 Infineon Technologies

- 11.1.9 Johnson Controls

- 11.1.10 Magna International Inc.

- 11.1.11 Mahle

- 11.1.12 NXP Semiconductors

- 11.1.13 Panasonic

- 11.1.14 Robert Bosch

- 11.1.15 Schaeffler

- 11.1.16 Valeo

- 11.1.17 ZF Friedrichshafen

- 11.2 Regional Players

- 11.2.1 Calsonic Kansei

- 11.2.2 Eaton Corporation

- 11.2.3 Faurecia

- 11.2.4 Hella GmbH & Co.

- 11.2.5 Hyundai Mobis

- 11.2.6 JTEKT Corporation

- 11.2.7 Lear Corporation

- 11.2.8 Schaeffler AG

- 11.2.9 Visteon Corporation

- 11.3 Emerging Players

- 11.3.1 ABB Ltd.

- 11.3.2 Aptiv PLC

- 11.3.3 Infineon Technologies

- 11.3.4 LEM Holding