|

시장보고서

상품코드

1936679

건설기계 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Construction Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

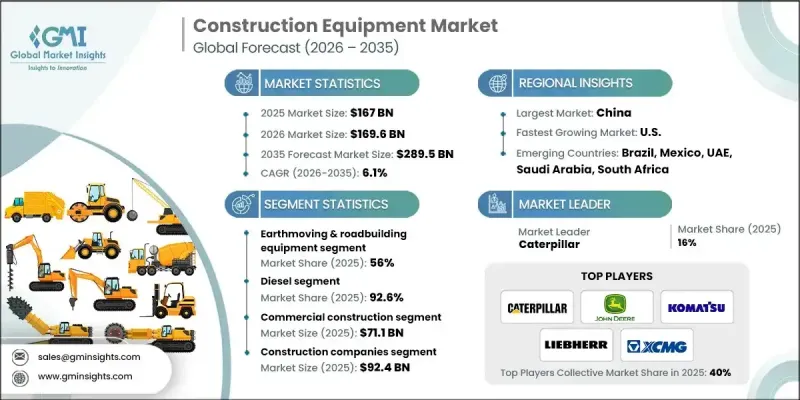

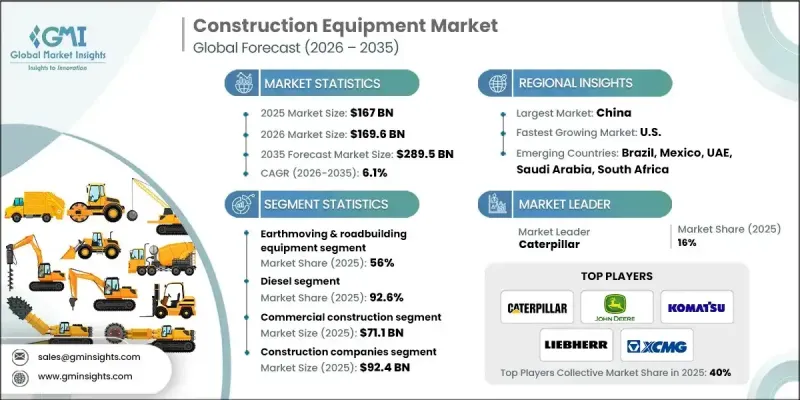

세계의 건설기계 시장은 2025년에 1,670억 달러로 평가되었으며, 2035년까지 CAGR 6.1%로 성장하여 2,895억 달러에 달할 것으로 예측됩니다.

시장 확대의 배경에는 경제 발전을 견인하는 인프라 및 건설 분야의 중요성과 대규모 공공 인프라 프로젝트에 대한 정부 투자 확대가 있습니다. 급속한 도시화, 산업화, 교통망의 고도화에 대한 수요 증가는 첨단 건설기계에 대한 강력한 수요를 창출하고 있습니다. 스마트 건설 솔루션과 디지털 통합과 같은 기술 혁신은 작업 효율성 향상, 정확성 및 안전성 향상을 실현하여 업무 형태를 변화시키고 있습니다. 자동화, 텔레매틱스, AI 지원 장비의 도입 확대와 더불어 장비 제조업체와 기술 제공업체 간의 전략적 제휴가 산업 전반의 디지털 전환을 가속화하고 있습니다. 또한, 건설기계 렌탈 서비스 확대로 하이엔드 장비에 대한 접근이 용이해져 신흥국 시장에서 보급이 확대되고 있습니다. 전반적으로 건설 활동의 증가, 기술 발전, 정부 주도의 정책으로 인해 시장은 견조한 성장세를 보이고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035 |

| 개시 금액 | 2,895억 달러 |

| 예측 금액 | 2,895억 달러 |

| CAGR | 6.1% |

토목 건설기계 부문은 2025년 56%의 점유율을 차지했으며, 2035년까지 연평균 5.5%의 성장률을 보일 것으로 전망됩니다. 굴착기, 백호, 로더, 콤팩터 등의 기계류는 대규모 인프라 프로젝트와 도로망 확장으로 인해 높은 수요가 예상됩니다. 정부가 도시 및 외딴 지역의 연결성과 접근성 향상에 주력하면서 고품질 기계에 대한 지속적인 수요가 발생하고 있습니다. 이 부문의 성장은 정밀한 토목 및 건설 작업을 위한 특수 장비를 필요로 하는 진행 중인 공공 사업 프로그램에 의해 더욱 뒷받침되고 있습니다. 이 부문의 우위는 도로 건설 및 인프라 개발이 건설기계 시장을 주도하는 데 있어 핵심적인 역할을 하고 있음을 강조합니다.

디젤 엔진 탑재 장비 부문은 2025년 92.6%의 점유율을 차지했으며, 2026년부터 2035년까지 CAGR 5.6%로 성장할 것으로 예측됩니다. 각 제조사들은 연비 향상, 배기가스 배출량 감소, 기계 전체 성능 향상을 위해 디젤 엔진에 첨단 기술을 접목하고 있습니다. GPS 추적, 차량 진단, 원격 모니터링을 결합한 텔레매틱스 통합을 통해 실시간 성능 분석 및 예지보전이 가능합니다. 렌탈업체와 계약업체들은 차량 관리, 운영 효율성 최적화, 다운타임 감소를 위해 텔레매틱스 지원 장비의 도입을 확대하고 있습니다. 클라우드 기반 솔루션을 통해 운영자는 기계를 모니터링하고, 사용량을 추적하고, 유지보수 일정을 계획할 수 있어 대규모 프로젝트와 임대 사업 모두에서 디젤 구동 기계의 매력을 높일 수 있습니다.

2025년 중국 건설기계 시장은 50%의 점유율을 차지하며 387억 달러 규모에 달할 것으로 예상됩니다. 이 지역의 성장은 급속한 도시화, 산업 확장, 인건비 상승을 상쇄하기 위한 건설기계 렌탈 모델의 도입 증가에 의해 주도되고 있습니다. 중국 제조업체와 임대 사업자들은 계약자 및 대규모 인프라 개발업체를 유치하기 위해 고도의 자동화, 연료 효율성, 텔레매틱스 통합을 갖춘 기술적으로 진보된 기계에 중점을 두고 있습니다. 인프라 투자 증가와 비용 효율적인 렌탈 솔루션의 조합은 시장 수요를 강화하고 지역 전체에서 고성능 건설 장비의 도입을 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제품별, 2022-2034

제6장 시장 추정 및 예측 : 추진력별, 2022-2034

제7장 시장 추정 및 예측 : 용도별, 2022-2034

제8장 시장 추정 및 예측 : 최종 용도별, 2022-2034

제9장 시장 추정 및 예측 : 지역별, 2022-2034

제10장 기업 개요

KSM 26.03.05The Global Construction Equipment Market was valued at USD 167 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 289.5 billion by 2035.

Market expansion is fueled by the critical role of infrastructure and construction in driving economic development, alongside significant government investments in large-scale public infrastructure projects. Rapid urbanization, increasing industrialization, and rising demand for improved transportation networks are creating strong demand for advanced construction machinery. Technological innovations, including smart construction solutions and digital integration, are transforming operations, enabling improved productivity, precision, and safety. The rising adoption of automation, telematics, and AI-assisted equipment, coupled with strategic partnerships among equipment manufacturers and technology providers, is accelerating the digital shift across the sector. Additionally, growing rental services for construction machinery are making high-end equipment more accessible, enhancing market penetration in emerging economies. Overall, the market is witnessing robust growth driven by increasing construction activity, technological evolution, and government-backed initiatives.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $289.5 Billion |

| Forecast Value | $289.5 Billion |

| CAGR | 6.1% |

The earthmoving and road-building equipment segment held 56% share in 2025 and is expected to grow at a CAGR of 5.5% through 2035. Equipment such as excavators, backhoes, loaders, and compactors is experiencing high demand due to large-scale infrastructure projects and road network expansions. Governments' focus on improving connectivity and accessibility in urban and remote regions is creating sustained demand for high-quality machinery. The segment's growth is further supported by ongoing public works programs, which require specialized equipment for precise earthmoving and construction operations. This segment's dominance underscores the central role of road-building and infrastructure development in driving the construction equipment market.

The diesel-powered equipment segment held a 92.6% share in 2025 and is forecasted to grow at a CAGR of 5.6% from 2026 to 2035. Manufacturers are incorporating advanced technologies in diesel engines to improve fuel efficiency, reduce emissions, and enhance overall machine performance. Integration of telematics, combining GPS tracking, onboard diagnostics, and remote monitoring, is allowing real-time performance analysis and predictive maintenance. Rental companies and contractors are increasingly adopting telematics-enabled equipment for fleet management, optimizing operational efficiency and reducing downtime. Cloud-based solutions allow operators to monitor machinery, track usage, and plan maintenance schedules, reinforcing the appeal of diesel-powered machines in both large-scale projects and rental operations.

China Construction Equipment Market held 50% share in 2025, generating USD 38.7 billion in 2025. The region's growth is driven by rapid urbanization, industrial expansion, and the rising adoption of construction equipment rental models to offset labor cost increases. Chinese manufacturers and rental providers are emphasizing technologically advanced machinery with enhanced automation, fuel efficiency, and telematics integration to attract contractors and large-scale infrastructure developers. The combination of rising infrastructure investments and cost-effective rental solutions is strengthening market demand and driving the adoption of high-performance construction equipment throughout the region.

Key players operating in the Global Construction Equipment Market include Caterpillar, CNH Industrial, Deere & Co., Doosan, Hitachi Construction Machinery, Komatsu, Liebherr, Sany, Terex, Volvo, and XCMG. Companies in the construction equipment market are adopting multiple strategies to consolidate their presence and expand market share. These include investing heavily in R&D to develop smart, energy-efficient, and telematics-enabled machinery. Firms are entering strategic partnerships with technology providers to integrate AI, IoT, and automation into their products. Expanding service networks and rental solutions enhance accessibility, particularly in emerging markets. Companies are also pursuing mergers and acquisitions to strengthen their global footprint, optimize supply chains, and gain access to new customer bases.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Propulsion

- 2.2.4 Application

- 2.2.5 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Urbanization and infrastructure development

- 3.2.1.2 Rising government investments in smart cities & public works

- 3.2.1.3 Technological advancements

- 3.2.1.4 Shift toward electric and hybrid construction equipment

- 3.2.1.5 Rental and leasing boom

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital and maintenance costs

- 3.2.2.2 Volatility in raw material prices

- 3.2.2.3 Shortage of skilled operators

- 3.2.2.4 Regulatory and emission compliance requirements

- 3.2.2.5 Intense competition from rental and used equipment

- 3.2.3 Market opportunities

- 3.2.3.1 Electric & Hybrid Equipment Adoption Acceleration

- 3.2.3.2 Autonomous Construction Operations & AI Integration

- 3.2.3.3 Precision Construction Technology & GPS Guidance

- 3.2.3.4 Equipment-as-a-Service (EaaS) Business Models

- 3.2.3.5 Retrofit & Upgrade Market for Legacy Equipment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Environmental Protection Agency (EPA)

- 3.4.1.2 Canadian Standards Association, CSA C225-00

- 3.4.2 Europe

- 3.4.2.1 Committee for European Construction Equipment (CECE)

- 3.4.2.2 Construction Equipment Standards and Regulations Committee (CESRC)

- 3.4.2.3 Construction Products Regulation (EU 2011/305) (CPR)

- 3.4.3 Asia Pacific

- 3.4.3.1 ICEMA - Indian Construction Equipment Manufacturers’ Association

- 3.4.3.2 China Construction Machinery Association (CCMA)

- 3.4.3.3 The International Council on Clean Transportation

- 3.4.4 Latin America

- 3.4.4.1 Chilean Construction Chamber (CChC)

- 3.4.4.2 International Council on Clean Transportation (ICCT)

- 3.4.4.3 Brazilian Regulatory Standards (NR)

- 3.4.5 MEA

- 3.4.5.1 ASTM international standards

- 3.4.5.2 Presidential Legislative Decree 7/11

- 3.4.5.3 Driven machinery regulations

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Patent analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Cost breakdown analysis

- 3.10.1 Raw material costs

- 3.10.2 Powertrain & propulsion system costs

- 3.10.3 Hydraulic & mechanical system costs

- 3.10.4 Electrical & electronic component costs

- 3.10.5 Manufacturing & assembly costs

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Import and export

- 3.11.3 Major import countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Customer & demand-side intelligence

- 3.13.1 Purchase vs rental decision drivers

- 3.13.2 Total cost of ownership (TCO) considerations

- 3.13.3 Brand loyalty vs price sensitivity

- 3.13.4 Replacement cycle & fleet renewal trends

- 3.14 Demand-supply gap & capacity utilization analysis

- 3.14.1 Capacity utilization rates (OEM vs regional players)

- 3.14.2 Demand-supply mismatch hotspots

- 3.14.3 Short-term vs long-term capacity outlook

- 3.15 Aftermarket & Lifecycle Revenue Analysis

- 3.15.1 Parts & service revenue share

- 3.15.2 Maintenance contracts & service bundling

- 3.15.3 Digital service monetization

- 3.15.4 Impact on OEM margins

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Earthmoving & roadbuilding equipment

- 5.2.1 Backhoe

- 5.2.2 Excavator

- 5.2.3 Loader

- 5.2.4 Compaction equipment

- 5.2.5 Others

- 5.3 Material handling and cranes

- 5.3.1 Storage and handling equipment

- 5.3.2 Engineered systems

- 5.3.3 Industrial trucks

- 5.3.4 Bulk material handling equipment

- 5.4 Concrete equipment

- 5.4.1 Concrete pumps

- 5.4.2 Crusher

- 5.4.3 Transit mixers

- 5.4.4 Asphalt pavers

- 5.4.5 Batching plants

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 CNG/LNG

- 6.4 Electric

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Residential construction

- 7.3 Commercial construction

- 7.4 Industrial construction

- 7.5 Mining & quarrying

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Construction companies

- 8.3 Mining operators

- 8.4 Rental companies

- 8.5 Government & municipalities

- 8.6 Industrial users

Chapter 9 Market Estimates & Forecast, By Region, 2022-2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Denmark

- 9.3.8 Finland

- 9.3.9 Norway

- 9.3.10 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Singapore

- 9.4.7 Thailand

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Caterpillar

- 10.1.2 Komatsu

- 10.1.3 John Deere

- 10.1.4 Volvo

- 10.1.5 Liebherr

- 10.1.6 Hitachi

- 10.1.7 JCB

- 10.1.8 Sany

- 10.2 Regional Champions

- 10.2.1 Case

- 10.2.2 New Holland

- 10.2.3 Doosan

- 10.2.4 Hyundai

- 10.2.5 XCMG

- 10.2.6 Zoomlion

- 10.2.7 Terex

- 10.2.8 Manitou

- 10.2.9 Wacker Neuson

- 10.3 Emerging Players & Service Providers

- 10.3.1 United Rentals

- 10.3.2 Ashtead / Sunbelt Rentals

- 10.3.3 H&E Equipment Services

- 10.3.4 Home Depot Tool Rental

- 10.3.5 Built Robotics

- 10.3.6 SafeAI

- 10.3.7 Trimble

- 10.3.8 Topcon