|

시장보고서

상품코드

1833680

미니 스플릿 공조 시스템 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Mini Split Air Conditioning System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

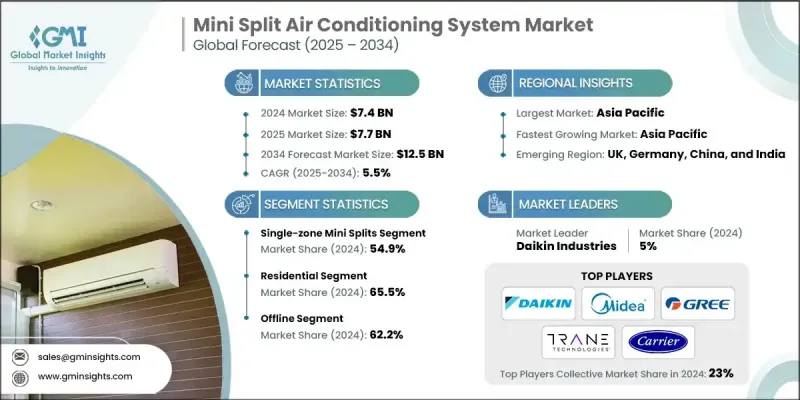

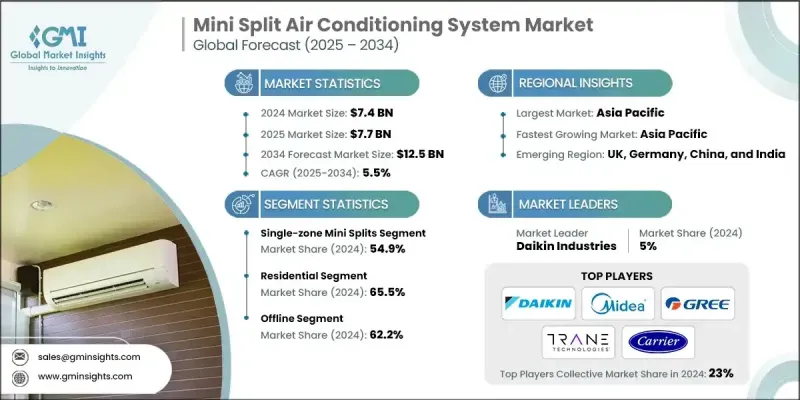

세계 미니 스플릿 공조 시스템 시장 규모는 2024년에 74억 달러로 평가되었으며, CAGR 5.5%로 성장하여 2034년에는 125억 달러에 달할 것으로 예측됩니다.

에너지 소비와 이산화탄소 배출량 감소가 중요시되는 가운데, 미니 스플릿 시스템은 SEER가 높고, 사용하지 않는 공간에 에너지를 낭비하지 않고 특정 구역을 냉방할 수 있어 인기를 끌고 있습니다.

| 시장 규모 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034 |

| 시장 규모 | 74억 달러 |

| 예측 금액 | 125억 달러 |

| CAGR | 5.5% |

싱글존 미니 스플릿 수요 증가

싱글 존 미니 스플릿 부문은 저렴한 가격, 단순성, 타겟팅된 냉각 효과로 인해 2024년 큰 점유율을 차지했습니다. 이 시스템은 소규모 주택, 개별 방 또는 홈 오피스에 이상적이며, 사용자는 전체 HVAC 설정을 재검토하지 않고도 특정 공간을 냉각시킬 수 있습니다. 덕트 공사가 필요 없는 에너지 효율적인 솔루션을 찾는 주택 소유자가 증가함에 따라, 싱글 존 유닛은 특히 공간과 비용이 중요한 도시 환경에서 최적의 대안으로 떠오르고 있습니다.

주택 분야 채용 확대

주택 부문은 주택 소유자가 편안함, 맞춤화, 에너지 절약을 우선시함에 따라 2034년까지 적절한 CAGR로 성장할 것입니다. 이 시스템은 중앙 공조 시스템을 대체할 수 있는 덕트리스를 제공하기 때문에 덕트 설치가 불가능한 오래된 주택이나 증축 및 개축에 특히 매력적입니다. 원격 근무 및 재택근무 시간이 증가함에 따라 주거 공간 전체의 유연한 공조 제어에 대한 요구가 증가하고 있습니다. 각 브랜드는 보다 조용한 모델, 깔끔한 외관, 스마트폰의 움직임에 맞춘 Wi-Fi 지원 기능 등을 도입하여 대응하고 있습니다.

오프라인 부문의 견인력 강화

오프라인 분야는 제품의 복잡성과 구매 시 전문가의 지도가 필요함에 따라 2024년 큰 점유율을 차지했습니다. 많은 고객들은 여전히 시스템 성능을 평가하고, 설치 지원을 받고, 애프터 서비스 가용성을 보장하기 위해 오프라인 소매점이나 공식 대리점을 선호합니다. 각 회사는 소매점과의 파트너십을 강화하고, 번들 설치 서비스를 제공하고, 매장 내 시연을 통해 소비자의 신뢰도를 높이고 구매 결정을 앞당기고 있습니다.

아시아태평양이 추진력 있는 지역이 될 것입니다.

아시아태평양의 미니 분할 공조 시스템 시장은 2024년 큰 점유율을 차지했으며, 이는 밀집된 도시화, 중산층 증가, 이 지역의 더운 기후가 원동력이 될 것으로 보입니다. 중국, 일본, 한국, 인도 등의 국가에서는 신규 주택 개발 및 리노베이션 프로젝트에서 컴팩트하고 에너지 효율적인 냉각 솔루션에 대한 수요가 급증하고 있습니다. 국내외 기업들은 생산시설 확대, 지역 취향에 맞는 디자인 커스터마이징, 대리점망을 활용한 판매망과 대응력 강화에 주력하고 있습니다.

미니 분할 공조 시스템 시장의 주요 업체는 Toshiba Corporation, Senville, Daikin Industries, LG Electronics, Trane Technologies, Fujitsu General, Haier Group Corporation, Hitachi, Mitsubishi Electric Corporation, Carrier Corporation, Panasonic Corporation, Samsung Electronics, GREE Electric Appliances, Johnson Controls International, Midea Group입니다.

시장에서의 입지를 강화하기 위해 미니 스플릿 공조 시스템 분야의 기업들은 연구개발, 스마트 기능, 지역 확장에 많은 투자를 하고 있습니다. 주요 발전 전략으로는 에너지 효율 향상을 위한 인버터 컴프레서 통합, 원격 제어를 위한 IoT 지원 모델 개발, 세계 환경 기준 준수를 위한 친환경 냉매 사용 등이 있습니다. 주요 브랜드는 또한 설치업체와 전략적 제휴를 맺고 서비스 네트워크를 육성하고 소비자들에게 덕트리스 기술의 이점을 알리는 캠페인을 전개하고 있습니다. 엔트리 레벨부터 프리미엄까지 확장 가능한 제품 라인을 제공함으로써 각 회사는 다양한 예산과 용도에 대응하고 시장의 지속적인 성장을 보장하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 미치는 요인

- 업계에 대한 영향요인

- 성장 촉진요인

- HVAC 시스템의 에너지 효율의 중요성

- 특정 존에 맞춘 기후 제어

- 설치 용이성과 유연성이 뛰어난 설계

- 업계의 잠재적 리스크와 과제

- 대체 기술과의 치열한 경쟁

- 시장 포화

- 기회

- 기존 건물 개선 공사 수요 증가

- 스마트홈과 IoT 테크놀러지와의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 향후 시장 동향

- 테크놀러지와 혁신 상황

- 현재 기술 동향

- 신기술

- 가격 동향

- 지역별

- 제품 유형별

- 규제 프레임워크

- 표준 및 컴플라이언스 요건

- 지역 규제 프레임워크

- 인증 기준

- 무역 통계(HS 코드 : 84158210)

- 주요 수입국

- 주요 수출국

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 파트너십과 협업

- 신제품 발매

- 확장 계획

제5장 시장 추정과 예측 : 제품 유형별, 2021-2034

- 주요 동향

- 싱글 존 미니 스플릿

- 멀티 존 미니 스플릿

제6장 시장 추정과 예측 : 설비별, 2021-2034

- 주요 동향

- 벽걸이식

- 바닥 설치형

- 천장 장착형

- 기타(자립형)

제7장 시장 추정과 예측 : 기술별, 2021-2034

- 주요 동향

- 인버터 미니 스플릿

- 비인버터 미니 스플릿

제8장 시장 추정과 예측 : 가격별, 2021-2034

- 주요 동향

- 저

- 중

- 고

제9장 시장 추정과 예측 : 용량별, 2021-2034

- 주요 동향

- 최대 9,000 BTU/시

- 9,000-12,000 BTU/시

- 12,000-18,000 BTU/시

- 18,000 BTU/시 이상

제10장 시장 추정과 예측 : 최종 용도별, 2021-2034

- 주요 동향

- 주거용

- 상업용

제11장 시장 추정과 예측 : 유통 채널별, 2021-2034

- 주요 동향

- 온라인

- 기업 웹사이트

- E-Commerce 웹사이트

- 오프라인

- 전문점

- 슈퍼마켓과 하이퍼마켓

- 팩토리 아울렛

- 기타 소매점

제12장 시장 추정과 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트

제13장 기업 개요

- Carrier Corporation

- Daikin Industries

- Fujitsu General

- GREE Electric Appliances

- Haier Group Corporation

- Hitachi

- Johnson Controls International

- LG Electronics

- Midea Group

- Mitsubishi Electric Corporation

- Panasonic Corporation

- Samsung Electronics

- Senville

- Toshiba Corporation

- Trane Technologies

The Global Mini Split Air Conditioning System Market was valued at USD 7.4 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 12.5 billion by 2034.

With growing emphasis on reducing energy consumption and carbon emissions, mini split systems are gaining popularity due to their high SEER ratings and ability to cool specific zones without wasting energy on unused spaces.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.4 billion |

| Forecast Value | $12.5 billion |

| CAGR | 5.5% |

Rising Demand for Single-Zone Mini Splits

The single-zone mini splits segment held a significant share in 2024, driven by its affordability, simplicity, and targeted cooling benefits. These systems are ideal for small homes, individual rooms, or home offices, allowing users to cool specific spaces without overhauling their entire HVAC setup. As more homeowners seek energy-efficient solutions without the need for ductwork, single zone units are emerging as the go-to option, particularly in urban environments where space and cost are critical.

Increasing Adoption in the Residential Sector

The residential segment will grow at a decent CAGR through 2034, as homeowners prioritize comfort, customization, and energy savings. These systems offer a ductless alternative to central AC, making them especially attractive for older homes or additions where duct installation is not feasible. With remote work and time spent at home increasing, there's a growing need for flexible climate control across living spaces. Brands are responding by introducing quieter models, cleaner aesthetics, and Wi-Fi enabled features that align with smart home movement.

Offline Sector to Gain Traction

The offline segment generated a sizeable share in 2024, backed by the complexity of the product and the need for expert guidance during purchase. Many customers still prefer brick-and-mortar retailers or authorized dealers to assess system performance, get installation support, and ensure after-sales service availability. Companies are strengthening retail partnerships, offering bundled installation services, and conducting in-store demos to drive consumer confidence and accelerate purchase decisions.

Asia Pacific to Emerge as a Propelling Region

Asia Pacific mini split air conditioning system market held a significant share in 2024, driven by dense urbanization, rising middle-class income, and the region's hot climate. Countries like China, Japan, South Korea, and India are witnessing surging demand for compact, energy-efficient cooling solutions in both new residential developments and retrofit projects. Local and international players are focusing on expanding production facilities, customizing designs to meet regional preferences, and leveraging distributor networks to increase reach and responsiveness.

Major players in the mini split air conditioning system market are Toshiba Corporation, Senville, Daikin Industries, LG Electronics, Trane Technologies, Fujitsu General, Haier Group Corporation, Hitachi, Mitsubishi Electric Corporation, Carrier Corporation, Panasonic Corporation, Samsung Electronics, GREE Electric Appliances, Johnson Controls International, and Midea Group.

To strengthen their market presence, companies in the mini split air conditioning system space are investing heavily in R&D, smart features, and regional expansion. Key strategies include the integration of inverter compressors for enhanced energy efficiency, the development of IoT-enabled models for remote control, and the use of eco-friendly refrigerants to comply with global environmental standards. Leading brands are also forming strategic alliances with installers, training service networks, and launching awareness campaigns to educate consumers on the benefits of ductless technology. By offering scalable product lines-from entry-level to premium-companies are catering to a wide range of budgets and applications, ensuring sustainable market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Installation

- 2.2.4 Technology

- 2.2.5 Price

- 2.2.6 Capacity

- 2.2.7 End use

- 2.2.8 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 The significance of energy efficiency in HVAC systems

- 3.2.1.2 Tailoring climate control for specific zone

- 3.2.1.3 Ease of installation and flexibility design

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High competition from alternative technologies

- 3.2.2.2 Market saturation

- 3.2.3 Opportunities

- 3.2.3.1 Rising demand for retrofit installations in existing buildings

- 3.2.3.2 Integration with smart home & IoT technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory framework

- 3.7.1 standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS code: 84158210)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's five forces analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Single-zone mini splits

- 5.3 Multi-zone mini splits

Chapter 6 Market Estimates & Forecast, By Installation, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Wall mounted

- 6.3 Floor-mounted

- 6.4 Ceiling-mounted

- 6.5 Other (Free standing)

Chapter 7 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Inverter mini splits

- 7.3 Non-inverter mini splits

Chapter 8 Market Estimates & Forecast, By Price, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Estimates & Forecast, By Capacity, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Up to 9,000 BTU/hr

- 9.3 9,000 to 12,000 BTU/hr

- 9.4 12,000 to 18,000 BTU/hr

- 9.5 18,000 BTU/hr and above

Chapter 10 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Residential

- 10.3 Commercial

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Online

- 11.2.1 Company websites

- 11.2.2 E-commerce website

- 11.3 Offline

- 11.3.1 Specialty stores

- 11.3.2 Supermarket & hypermarkets

- 11.3.3 Factory outlets

- 11.3.4 Other retail stores

Chapter 12 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Carrier Corporation

- 13.2 Daikin Industries

- 13.3 Fujitsu General

- 13.4 GREE Electric Appliances

- 13.5 Haier Group Corporation

- 13.6 Hitachi

- 13.7 Johnson Controls International

- 13.8 LG Electronics

- 13.9 Midea Group

- 13.10 Mitsubishi Electric Corporation

- 13.11 Panasonic Corporation

- 13.12 Samsung Electronics

- 13.13 Senville

- 13.14 Toshiba Corporation

- 13.15 Trane Technologies